Background

⠀

A journalist asked the following question;

⠀

“With high yields being long gone and DeFi seeing almost zero growth since Terra, we want to know what could be the next thing for DeFi?

⠀

A lot of chatter is centered at bringing real-world assets to blockchain like investing in US Treasuries and bonds via DeFi, on-chain credit etc. But I am not sure the sustainability of it — the RWA topic has been going for a long time and obviously, there are reasons why it didn’t work in the past.”

⠀

Defi is dead

⠀

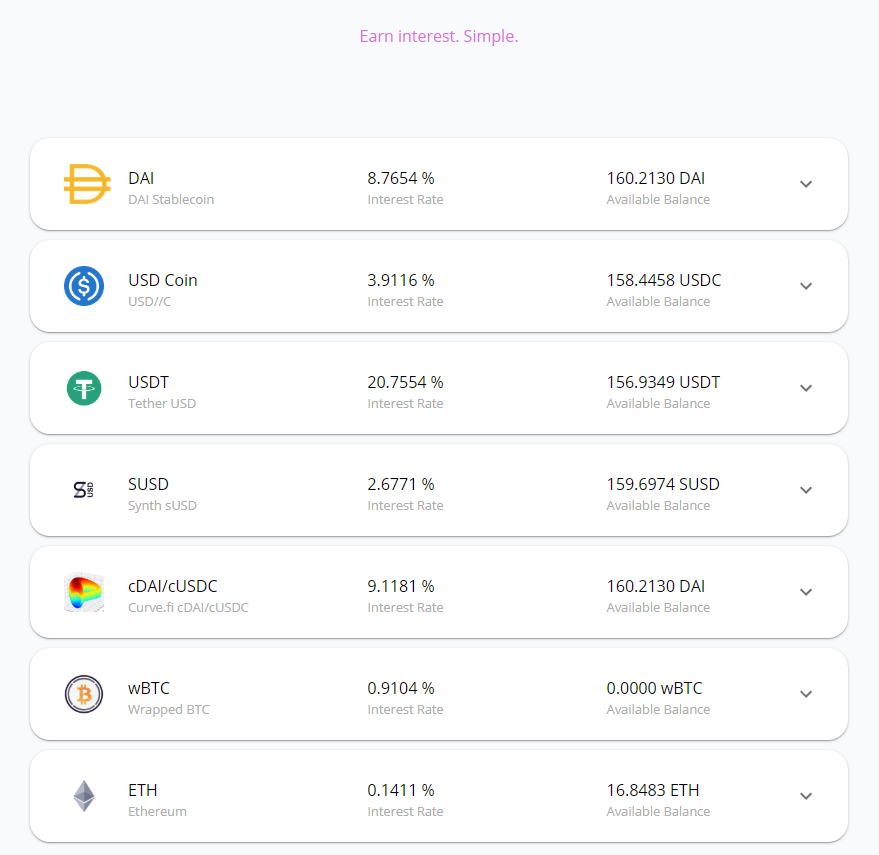

Jumping back to 5 Feb 2020;

⠀

Above is the original Yearn dashboard. DAI at the time had the DAI Savings Rate (DSR), which was providing ~7% subsidised via high interest rates, the “real” DAI yield was between 1%-2%. USDC was at ~4%. USDT was at the height of its FUD and people were shorting, but normally USDT would be around ~2%-4%. SUSD at 2%. BTC at 0.9%, ETH at 0.14%.

⠀

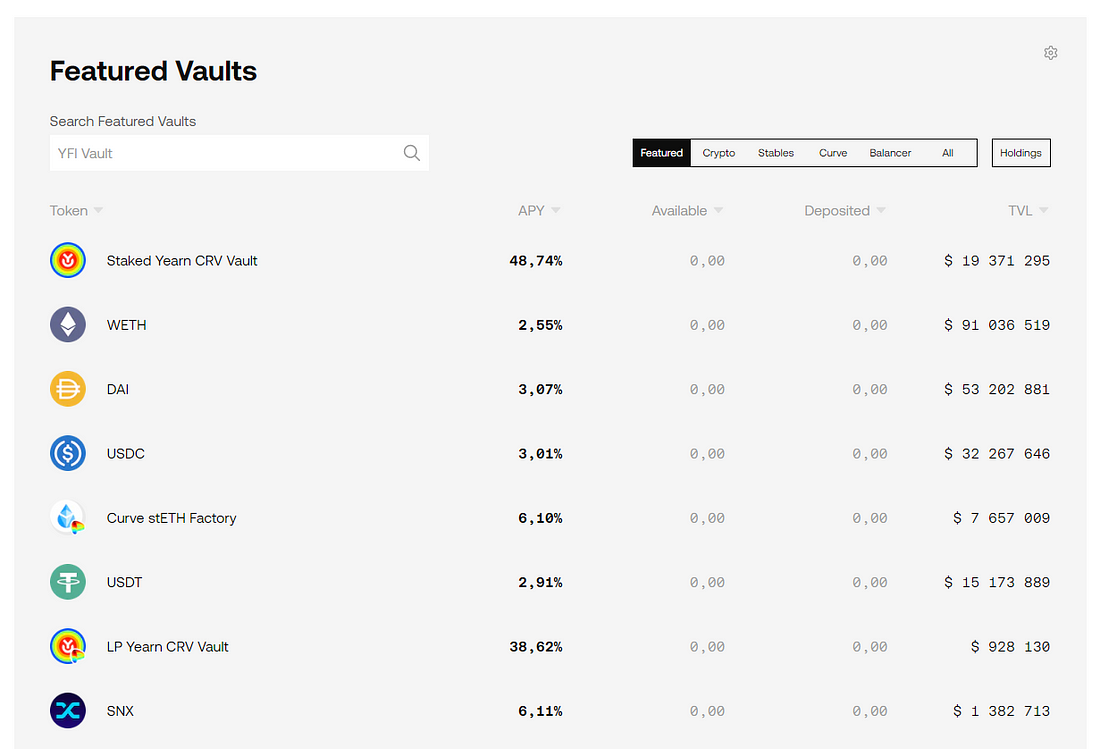

Fast forward to today, and if we look at Yearn again;

⠀

⠀

ETH at 2.5%, DAI at 3%, USDC at 3%, USDT at 3%. And this is all in an inactive market. All real yield is from lending markets and trading fees; lending markets are fueled by long/short activity. In a bear market, people enter short positions, they use stablecoins to collateralize their positions (increasing stable coin supply and pushing down stablecoin real yield), borrow crypto and sell (increasing crypto yield, as is evident by increases in real yield on ETH/BTC), and adding the stablecoins received from the sale as further collateral (further decreasing stable coin real yield). In a bull market, people enter long positions, they use their crypto to collateralize their position (decreasing crypto real yield), borrow stablecoins to buy more crypto off of the market (increasing stable coin real yield), and deposit the purchased crypto as further collateral (further decreasing crypto real yield).

⠀

Right now, we are in a low volatility phase of a prolonged bear market. At this point (using the past 2 bull markets as the basis), we see very little trade activity, everyone that was trying to short has shorted, but they aren’t confident enough yet to close their positions (causing rebuy’s and longs). So this is a “real yield low point”. Taking that into account, real yield is still higher than it was when Yearn was first created.

⠀

So I disagree with the statement “high yields being long gone and DeFi seeing almost zero growth”. That statement is based on comparing the current market with an unsustainable and highly delusional market peak, and not its progression. If you plot a growth chart on TVL, yield, and trade volume, and you flatten the curve to avoid oscillating, it is a clear linear growth chart. On every feasible metric, real yield and defi have grown substantially. The dot com bubble did not destroy the internet and require a next narrative, it was those projects that were given birth during that insanity that became the anchor products we use today.

⠀

Long Live Defi

⠀

To answer “what could be the next thing for DeFi”, defi is the next thing for defi. It doesn’t need a “new narrative”, it doesn’t need a “new shiny toy”, it just works.

⠀

Real World Assets (RWA)

⠀

Now to comment on the second part, it’s important to add some distinctions;

⠀

0 trust finance (where no trust is required or assumed), examples here are bitcoin, ethereum, fantom, uniswap, or yearn v1

⠀

Verifiable finance (where there are trust assumptions, but you can verify), examples here are aave, compound, yearn v2, where you can verify timelocked execution by multisigs.

⠀

Trusted finance (where absolute trust is required), centralised exchanges and prime brokers, examples Binance, Wintermute, etc

⠀

The next distinction is on regulated crypto vs crypto regulation. Regulated crypto are traditional products or companies that simply leverage crypto technology. They need to be fully legal, compliant, and regulated entities. Crypto regulation is the notion of trying to add regulation to decentralized protocols. The latter is not feasible and only creates friction for all parties involved.

⠀

RWA would need to exist in “trusted finance” or “verifiable finance”, and it would need to be “regulated crypto”. As you point out, RWA discussions have been going on for a long time. I myself had my first chats with traditional custodians, regulators, and governments on this topic back in 2018. At this point, regulated crypto does not yet exist. It is starting to exist, but it is a dependency for any RWA projects to succeed. Notable regulated crypto legislation examples include; South Korean Financial Services Commission allowing issuance of security tokens and the Swiss Parliament adopting the Federal Act on the DLT bill. The regulation is one part, the second part is on-boarding traditional auditors with the ability to verify and understand RWA on-chain and provide these reports, without which, again, it fails. So as these continue to develop, we will see more real world assets being tokenized on-chain. But it needs to be stated, these are not a new narrative, nor are they going to have any revolutionary change on defi. Defi will still simply be defi, it is just another tokenized asset being added as collateral or as a trading pair.

⠀

So I don’t see the requirement for a next trend in defi, I see defi as the trend. What we at Fantom Foundation are focusing on is;

⠀

Regulatory frameworks

Auditing tools

Layer 1 throughput and scalability

Layer 1 account UX and social recovery

⠀

Defi, and other blockchain verticals (social media, gaming, art, news, etc), are here to stay, but they are limited by the current state and access of the underlying technology (just like early web was limited by the underlying technology and access). There is no “new narrative” there is no “new trend”, simply more of the same. And that’s a good thing.