Written by: Heechang

Compiled by: Block unicorn

Key Takeaways

Until 2025, many on-chain assets were still just concepts. Today, they are moving towards clarity and gradually becoming reality. Structural changes are happening simultaneously in the three dimensions of the form, meaning, and use of money.

First Transformation: The form of money is diversifying. Stablecoins, tokenized bank deposits, and central bank digital currencies (CBDCs) will coexist in different roles. Fiat on/off-ramps, payment infrastructure, and IT platforms are rapidly adopting stablecoins to expand the post-issuance commercial landscape and usage ecosystem at a faster pace.

Second Transformation: The concept of money is broadening. Tokenization is turning not only physical and financial assets but also intangible elements like attention and predictions into assets. This blurs the line between money and assets, redefining both towards a world where "everything we own" becomes a unit of liquid value.

Third Transformation: The use of money is expanding. Centralized exchanges are moving beyond being mere trading venues to building full-stack financial ecosystems encompassing derivatives, risk-weighted assets (RWA), on-chain debit/credit cards, and on-chain decentralized finance (DeFi). Consequently, real-world blockchain use cases are diversifying around the central hub of exchanges.

All finance will eventually run on the blockchain.

This was my original purpose for entering the blockchain industry. Even if a crisis like the Terra collapse happens again, I cannot imagine an ideal financial system—an efficient, transparent, and programmable one—being possible without the blockchain at its core. I personally believe the most advanced financial infrastructure can only be built on-chain, and over time, existing systems will inevitably converge towards this structure.

2025 is the year this transition becomes tangible reality. With regulatory clarity, financial institutions, fintech companies, and governments are no longer debating whether to adopt blockchain. The question has now completely shifted from "when to adopt" to "how to participate."

Changes that once seemed distant and conceptual are now being implemented with clear direction. The essence of money—its form, its concept, its use cases—is undergoing structural transformation simultaneously across three dimensions.

Now, let's explore how these transformations are unfolding and examine the key forces driving this change.

1. First Transformation: Stablecoins Bring Diversification in the Form of Money

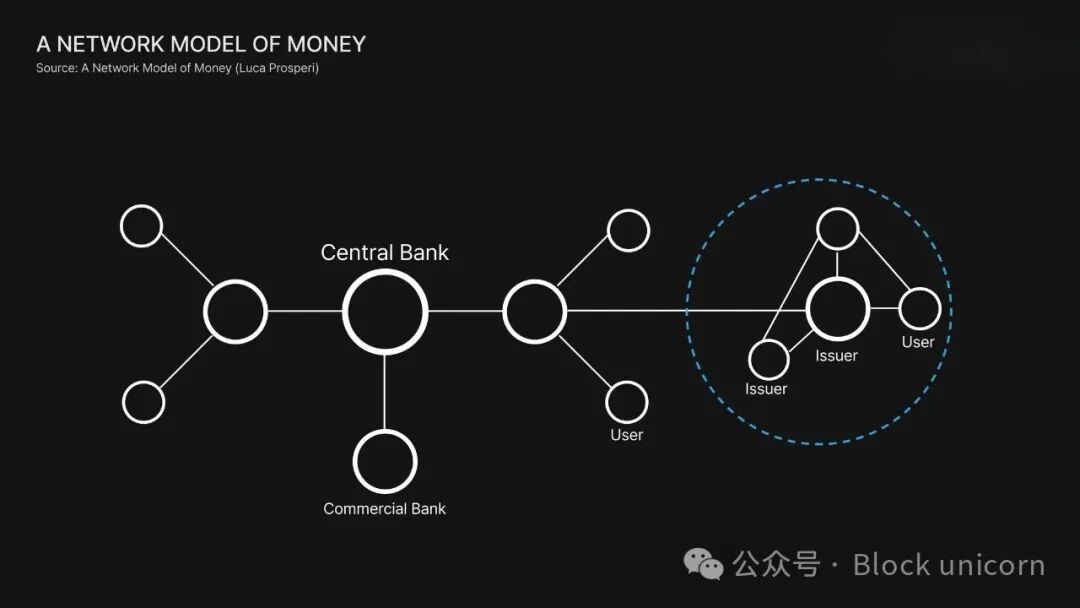

Source: "The Network Model of Money" — Luca Prosperi

The core of money is that it is the asset benchmark we use to measure value. When we buy or exchange goods, we price them in our national fiat currency. Historically, only two types of institutions issued and operated this money: central banks and commercial banks. Central banks manage the money supply and stability, while commercial banks operate the channels for fund flow between institutions and retail.

Stablecoins add a completely new layer to this. They enable any company to create its own form of money and build financial infrastructure around it, creating particularly powerful synergies with digital platforms. This does not mean stablecoins will replace central banks or commercial banks. Instead, just as PayPal and Stripe reshaped payments, and Robinhood changed how people invest, save, and spend, stablecoins introduce a new type of money designed for the digital world.

Three major trends emerged in 2025.

Stablecoins, Tokenized Bank Deposits, and CBDCs Will Coexist Long-Term

Source: "State of Crypto 2025: The Year Crypto Goes Mainstream"- a16z crypto

In the US, the first comprehensive federal stablecoin bill—the GENIUS Act—was passed by both houses of Congress and signed into law on July 18. The act introduces a licensing system for banks and stablecoin issuers and mandates that reserves must be held 1:1 in cash or short-term Treasury bonds.

Hong Kong acted more swiftly. The Legislative Council passed the Stablecoin Ordinance in May 2025. Starting August 1, stablecoin issuance officially became a regulated and licensed activity, with approvals expected in early 2026.

Japan, building on its 2023 amendments to the Payment Services Act, clarified eligibility for stablecoin issuance and launched its first large-scale issuance in the second half of 2025. JPYC issued a yen-backed stablecoin, with reserves fully held in domestic Japanese deposits and government bonds, and fully redeemable for yen. Japan's framework strictly limits issuers to licensed financial institutions and allows for trust structures to enhance the segregation of investor assets.

Among commercial banks, JPMorgan continues to expand deposit tokenization and real-time settlement through its private blockchain network, Kinexys. JPM Coin allows corporate clients to convert US dollars in their JPMorgan accounts into on-chain tokens, which can be used for instant transfers between global subsidiaries or for large-value settlements.

I believe stablecoins are not here to replace the existing monetary system. Instead, they will coexist with central bank money, bank deposits, and new digital assets—each playing a different role. Let's review these roles.

Central banks play the role of controllers. They issue fiat currency like the US dollar, manage the money supply, and provide a final backstop during times of financial stress.

Commercial banks play the role of coordinators. Regulated by central banks, they operate deposit accounts, provide credit, and facilitate the flow of funds between savers and borrowers. In short: if central banks issue the US Dollar, commercial banks create deposit forms like "JPMorganUSD".

Stablecoins play the role of catalysts. Backed by cash or short-term sovereign debt, stablecoins are not designed to replace central or commercial banks. Instead, they enable companies to build digital-first financial ecosystems and allow money to flow faster and more widely across various services.

Ultimately, the future is not about replacement, but about coexistence. Central Bank Digital Currencies (CBDCs) will reinforce monetary sovereignty and macro-level stability. Tokenized deposits will maintain the system of regulated financial intermediation. Stablecoins will compensate for the slower pace of central and commercial banks while meeting the speed, programmability, and interoperability required by the digital economy.

Each form of money will play a complementary role in an increasingly on-chain financial system.

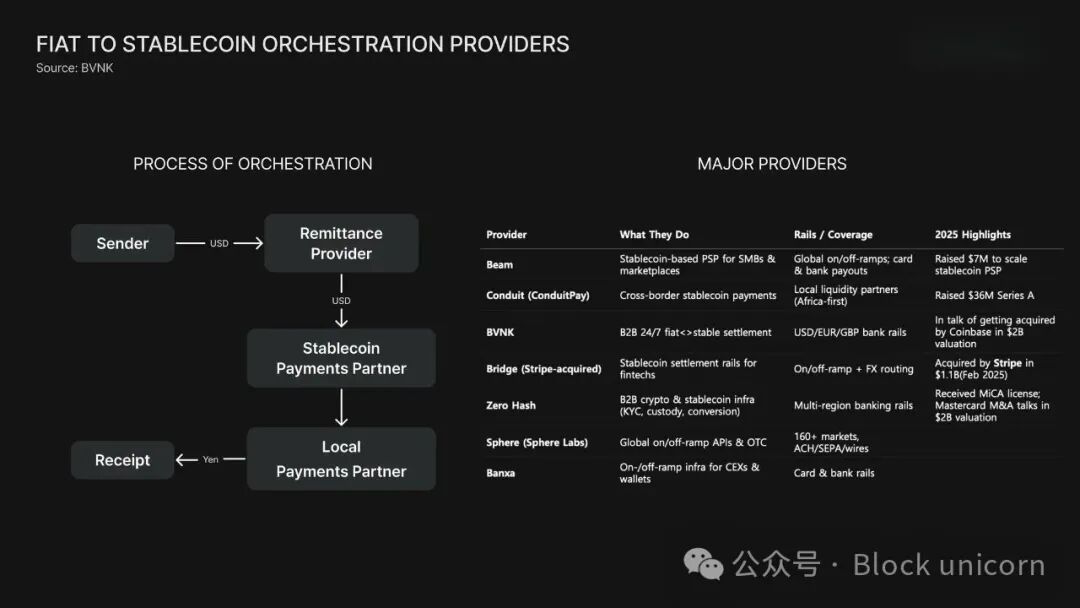

Companies Controlling the 'Next Layer' of Stablecoin Issuance Will Rise Rapidly

For stablecoins to be truly used, the primary condition is issuance. But for stablecoins to function in daily life or business operations, a critical step is needed: converting stablecoins to local currency, and vice versa. In 2025, a host of companies began integrating the infrastructure required for these on/off-ramp payment processes.

Yellowcard, Africa's largest crypto payments on-ramp company, has become a regional hub, able to connect stablecoins with local currencies, fully compliant with each country's regulations. Bridge, acquired by Stripe for $1.1 billion, plays a similar role. Companies like Zero Hash and BVNK—reportedly considered for acquisition by Mastercard and Coinbase for around $2 billion—now provide backend infrastructure for enterprises, exchanges, and fintech platforms, enabling the practical use of stablecoins at scale.

These services offer secure payment settlement and AML/KYC workflows, allowing businesses to accept stablecoins and convert them to local currency without bypassing domestic payment regulations. This architecture indicates that stablecoins are being deeply integrated into the existing financial system, rather than operating outside it.

Large exchanges like Binance, Bybit, and OKX are also expanding their own on/off-ramp functionalities, some building in-house, others outsourcing fiat ramps to specialized partners. Payment companies like Banxa, Mercuryo, and OpenPayd play a central role in this ecosystem, providing fiat payment channels that seamlessly connect with stablecoin trading flows.

All this points to a clear shift: the definition of stablecoins is no longer confined to their issuance but is increasingly about empowering individuals and businesses to use them.

IT Platforms Will Begin to Fully Embrace Stablecoins

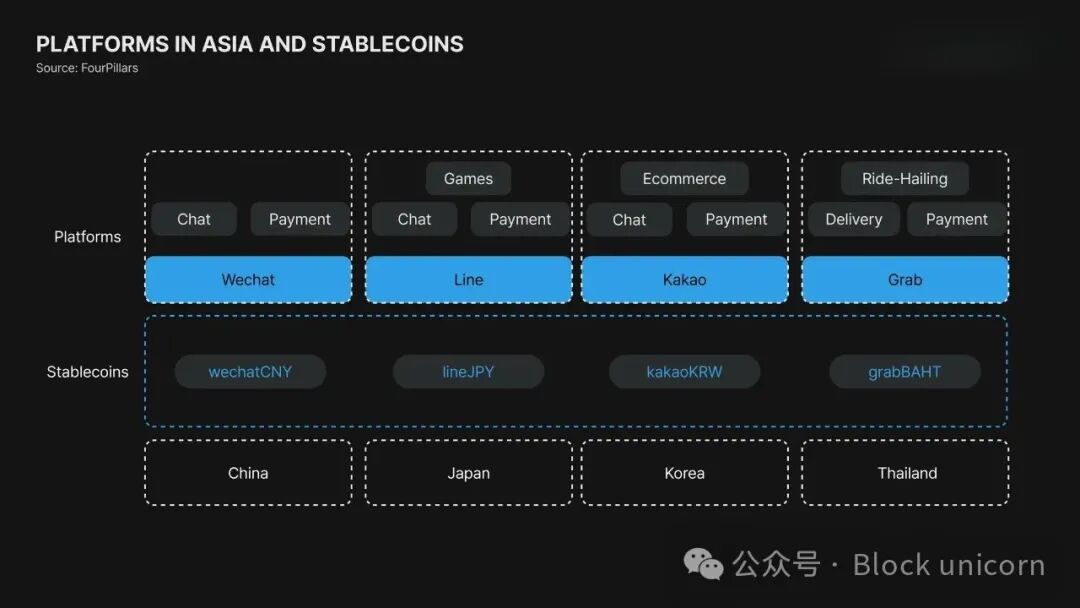

IT platforms, the hubs of daily consumer activity and business operations, are becoming the most powerful nexus for expanding stablecoin adoption. Asia's "super apps," which blend instant messaging, shopping, payments, and financial services, have already created massive user engagement and transaction volumes with their (non-crypto) digital wallets. By integrating stablecoins internally, these platforms can build their own native financial ecosystems and significantly boost user engagement.

By 2025, both PayPal and Cloudflare had launched stablecoin initiatives aimed at making them mainstream payment and internet infrastructure.

PayPal has integrated PYUSD into remittances, commerce, and e-commerce settlements, and recently invested in Stable. Stable is a Layer 1 blockchain optimized for USDT-based payments, which could further streamline PayPal's global payment infrastructure.

Cloudflare launched Net Dollar, a stablecoin designed to enable AI agents to autonomously settle API fees and cloud usage fees, effectively embedding programmable money into internet services.

This signals a broader shift: stablecoins are becoming the base monetary unit of the platform economy. Whether a platform issues its own stablecoin or partners with external issuers like Circle and Tether, stablecoins are beginning to function as the standard currency for these digital ecosystems.

2. Second Transformation: Tokenization Expands the Concept of Money

Through tokenization, asset ownership is moved onto the blockchain. In the past, ownership was recorded on paper documents, bank accounts, or centralized databases.

On-chain, ownership can be fractionalized, these fractions can be transferred under specific conditions, automatically distributed as yield, or deposited and traded via smart contracts.

This structure vastly expands asset accessibility. Historically, markets for assets like stocks, bonds, or private credit were only accessible to institutions or high-net-worth individuals. Yet, once tokenized, the same asset can be split into thousandths of a share and traded in real-time. Individuals can now participate through fractional ownership, opening up entirely new models of investing and consumption.

Ultimately, tokenization expands the very definition of money.

What we traditionally call "money"—a medium of exchange, store of value, and unit of account—is no longer limited to fiat currency. Increasingly, assets themselves are functioning as money. Treasury bonds, money market funds, investment funds, real estate, and even company equity are becoming programmable forms of money that can be programmed and used.

The Tokenized Asset Market Will Accelerate Growth

Source: RWA News: Ripple and BCG Report Tokenized Real-World Assets Could Reach $18.9 Trillion by 2033

Just five years ago, the stablecoin market was only $20 billion. Today, it exceeds $300 billion, while the tokenized real-world asset (RWA) market has grown from $13 million to $34.7 billion. Digital dollars, tokenized treasuries, and tokenized money market funds have become tangible tools for investment and settlement for both institutional and individual investors.

At the core of this trend are global financial institutions. BlackRock offers on-chain exposure to US Treasuries through its tokenized money market fund, BUIDL. Apollo has tokenized private credit funds, opening new liquidity channels for traditionally illiquid assets. Securitize, which provides infrastructure for these products, can now tokenize funds, equity, and alternative assets, and is even seeking to list in the US. Tokenization has moved far beyond blockchain startups to global financial giants.

According to a joint report by Boston Consulting Group (BCG) and Ripple, the tokenization market is projected to grow 30-fold over the next eight years, reaching approximately $18.9 trillion by 2033.

The direction is clear: tokenized assets are becoming one of the fastest-growing segments of the global financial system.

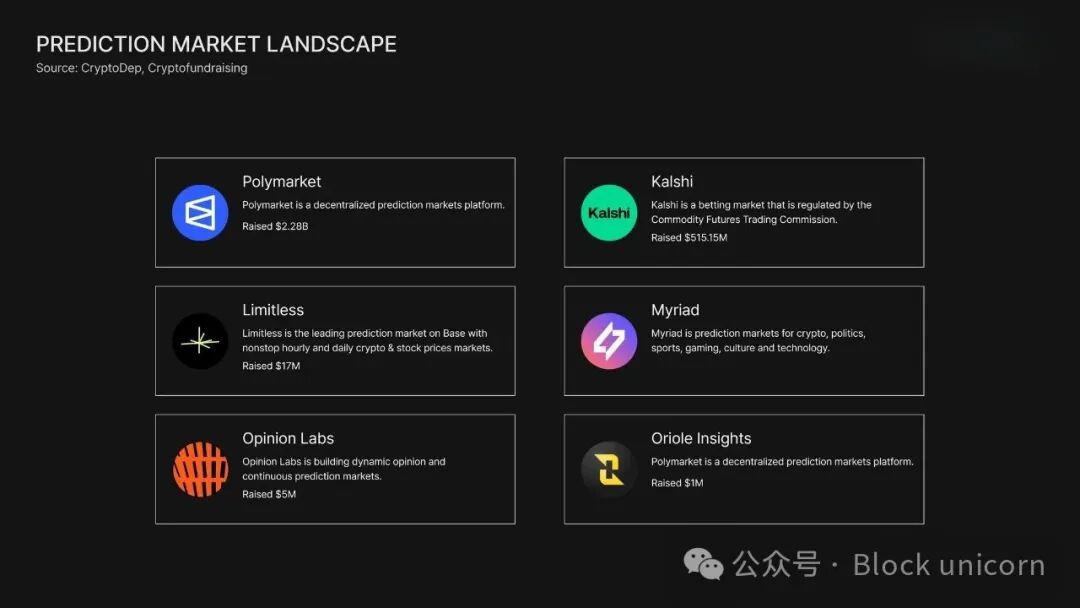

Even Intangibles Will Be Tokenized

Source: Kalshi founders Tarek Mansour and Luana Lopes Lara on turning events into assets

This year, Kaito pioneered a new concept. Kaito uses a unit called "yap" to measure and quantify the mention or promotion of a topic on Twitter, introducing the concept of an attention economy. In short, public attention is transformed into a measurable unit of value.

Prediction markets have similarly gained significant traction. Strictly speaking, prediction markets are not the same as tokenization, but they are conceptually similar in that they turn non-financial information or future events into tradable assets.

Tokenization converts tangible assets or financial products like treasury bonds, real estate, and funds into on-chain tokens. Prediction markets convert future possibilities, such as "Will a certain candidate win the election?", into tradable contracts.

In other words, tokenization grants ownership of an existing asset, while prediction markets grant value to a probability.

Platforms like Polymarket and Kalshi issue "yes/no" tokens for each event. After the event concludes, the winning side receives a $1 settlement. Unlike tokenized assets, which use collateral or legal trust structures for redemption, prediction markets use oracles and verified data for settlement, relying on the "truth of the outcome."

However, both systems follow a core principle: they transform previously non-tradable subjects into market-native assets with price and liquidity.

Ultimately, prediction markets represent the tokenization of belief and information, shifting the focus from "What do you own?" to "What do you believe, and how do you value it?"—thereby expanding the scope of assets in the blockchain world.

Source: X user — Crypto_Dep

Tokenization Will Fundamentally Change Our Perception of Money

The essence of tokenization is not merely moving assets onto the blockchain but changing how assets operate. Traditionally, "money" (dollars, euros, etc.) and "assets" (bonds, stocks, real estate) were seen as two distinct domains. Tokenization merges these two domains into a unified system.

Treasury bonds, venture funds, even real estate can now be represented as programmable, interoperable tokens that can be transferred instantly and integrated directly into various services. Once tokenized, assets can be used, stored, and priced in real-time. This breaks down the boundaries between what we own and what we can use, erasing the lines that previously separated financial products from liquidity.

Our traditional financial thinking is linear: we earn money → save money → invest → spend. Tokenization blurs the distinction between "money" and "assets." Everything we own becomes an expression of liquid value.

3. Third Transformation: The Rise of Centralized Exchanges (CEX), Expanding the Use of Money

Source: Gate Research: "Ecosystem Landscape and Convergence Trends of Centralized and Decentralized Exchanges"

"How much did it go up?"

For a long time, this simple question has driven the crypto market. News of Bitcoin rising 1000%, Ethereum soaring, or a new token's price skyrocketing always captures public attention. Price volatility became the market's focus, and trading became the core of everything.

And centralized exchanges are the hubs of this trading activity.

Binance, founded in 2017, now sees daily trading volumes of around $100 billion, making it one of the most liquid exchanges in the financial markets. Bybit (2018) and OKX (2017) follow closely, while exchanges like Upbit and Coinbase serve as the primary entry points for crypto in their respective markets.

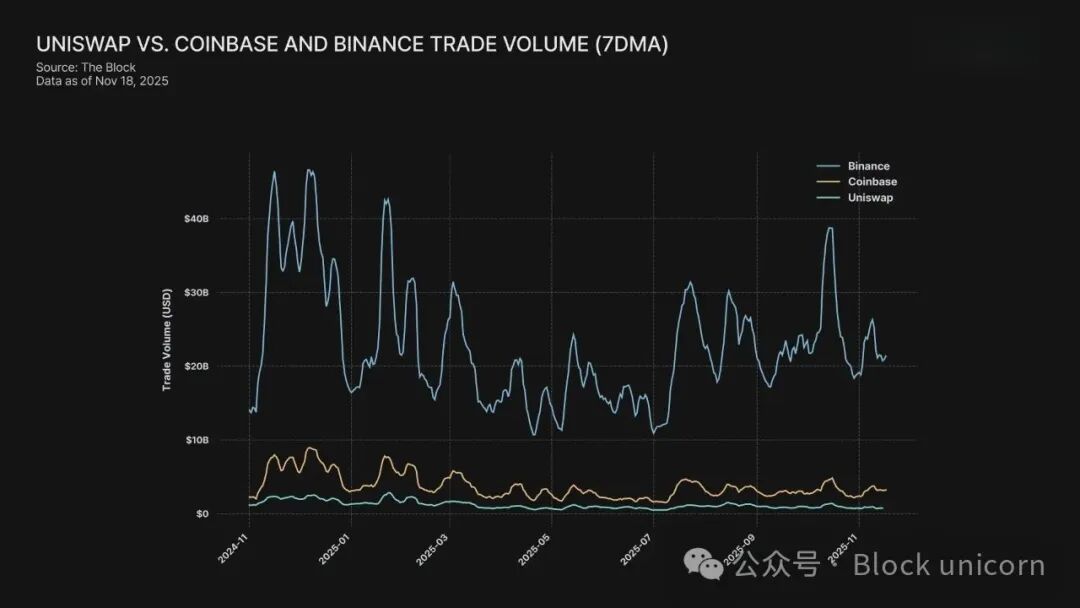

While decentralized exchanges are growing rapidly, the vast majority of trading volume still occurs off-chain, within centralized platforms.

In regions like South Korea, Japan, and Taiwan, regulatory restrictions and user awareness mean on-chain activity is only accessible to a subset of users. Migrating users from centralized exchanges to decentralized ecosystems requires not just a technical shift, but a psychological one—a transition that is by no means easy.

Centralized exchanges remain the primary entry point for most users into cryptocurrency, shaping how money moves, trades, and circulates in the digital economy.

Source: Uniswap vs. Coinbase and Binance trading volume (7-day average)

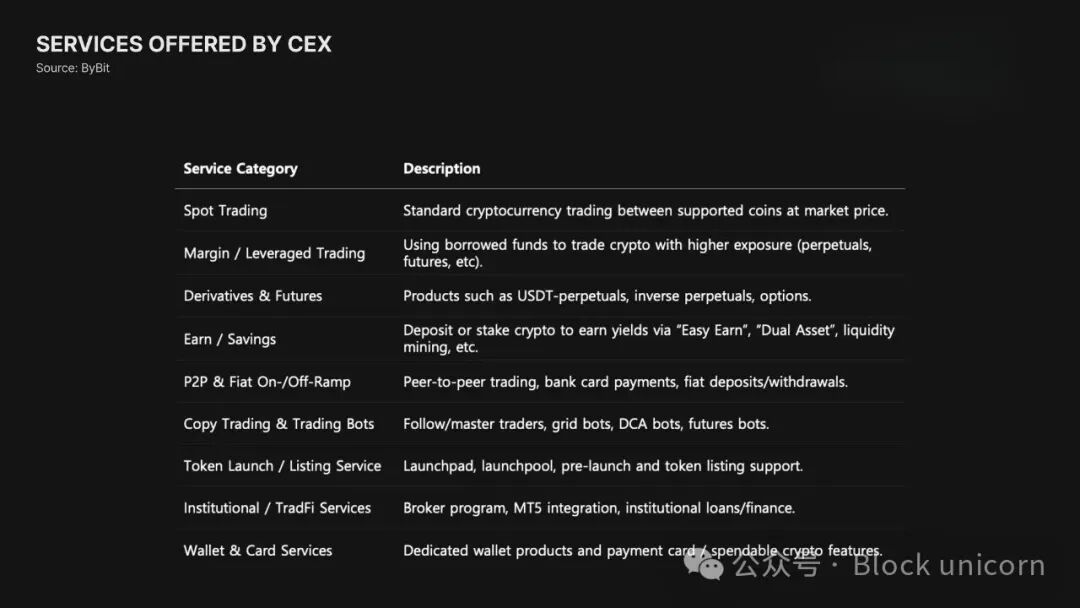

These platforms are no longer just cryptocurrency exchanges—they are evolving into comprehensive digital asset financial ecosystems.

Exchanges today offer far more than simple spot trading. They now provide perpetual contracts, options, and various structured derivatives, and recently even support trading of tokenized stocks and risk-weighted assets (RWA).

For example, Bybit integrated tokenized stocks through xStocks, enabling 24/7 trading of tokenized equities; Binance expands its business through derivatives and Launchpad, becoming a platform encompassing the entire token economy.

Exchanges are also building complete financial stacks, integrating trading → deposits → lending → spending.

As centralized exchanges transform into comprehensive financial infrastructure, it's necessary to examine the strategies they are deploying and how they are preparing for the next phase of on-chain finance. Let's delve into these strategies.

Exchange Services Will Continue to Expand

Exchanges are evolving from mere trading venues into "financial super apps."

In the past, users could only trade listed tokens. Now, with the launch of pre-sale platforms, users can trade even before the Token Generation Event (TGE). This allows users to directly participate in early-stage projects with high growth potential, equivalent to participating in pre-IPO financing opportunities on-chain.

Launchpad platforms are also developing rapidly, becoming a way for new projects to distribute tokens before listing on exchanges. Binance, Bybit, and OKX all operate their own Launchpads, attracting millions of participants and becoming key drivers of user acquisition. In this model, users are no longer just traders; they become early stakeholders in projects.

Exchanges are also expanding their scope from cryptocurrency to tokenized real-world assets (RWA).

Bybit's xStock is a prime example: users can trade tokenized global stocks and ETFs 24/7, signaling a growing trend of "decentralized access to traditional assets." Demand for on-chain real-world investments is steadily increasing.

Coinbase launched Bitcoin-backed lending through an integration with the lending protocol Morpho; Robinhood is experimenting with prediction markets, further integrating new financial primitives directly into its platform.

Beyond trading, exchanges are building a full suite of services aimed at maximizing the utility of customer assets, covering yield, credit, and spending.

Yield products like staking and yield-bearing vaults offer substantial returns on assets held on the exchange. On the spending side, products like the Bybit Card and Coinbase Card connect cryptocurrency balances directly to everyday real-world payments.

In other words, exchanges are no longer mere intermediaries for buying and selling tokens.

They are becoming integrated on-chain financial platforms where saving, investing, borrowing, and spending all occur within the same ecosystem.

Mature On-Chain Services Will Be Integrated into Exchanges

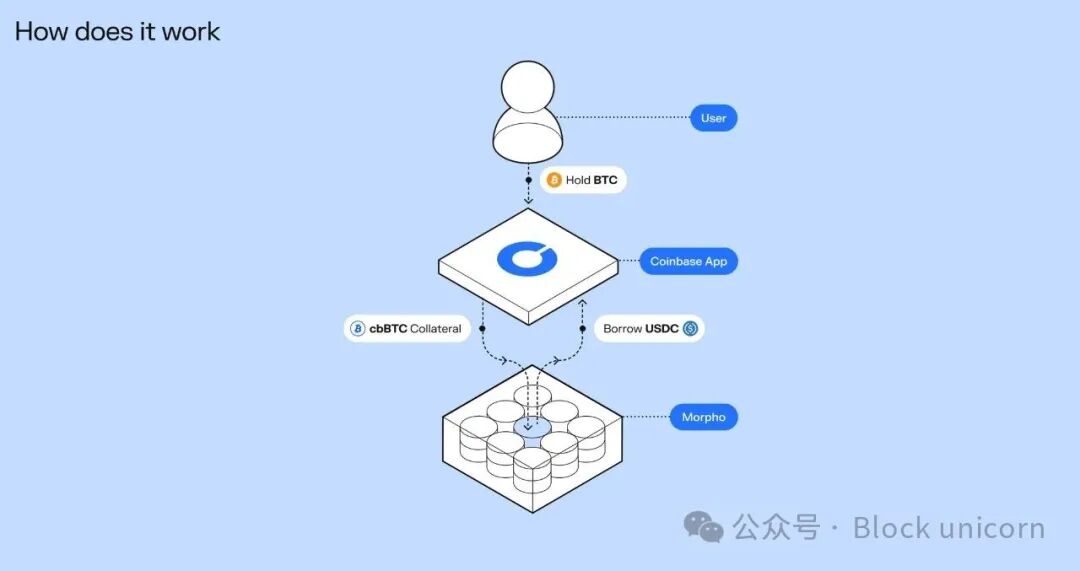

Source: Morpho's Bitcoin-backed loans

Exchanges are no longer sticking to their closed ecosystems but are expanding user functionality by directly integrating on-chain financial services.

A prime example is Bybit integrating Ethena's USDe into its trading pairs and yield products. This allows users to add a yield-bearing synthetic dollar, created and managed entirely on-chain, to their asset mix. This indicates a growing tendency for exchanges to view decentralized protocols as modular service components rather than external partners, embedding them directly into their platforms.

Coinbase is pushing this trend even further. By connecting its main exchange app with the Base app, Coinbase now supports DEX trading and provides access to millions of on-chain assets. The line between centralized and decentralized exchanges is becoming increasingly blurred.

Users, while maintaining the familiar centralized exchange interface, gain direct access to on-chain liquidity, pushing exchanges towards a hybrid CEX/DeFi model.

Coinbase also integrated Morpho's lending infrastructure directly into the exchange app. Users can deposit Bitcoin and borrow USDC using Bitcoin as collateral, all powered by underlying on-chain vaults. Since its launch in January, Coinbase's Morpho-based vaults have grown rapidly, with $1.48 billion in deposits and $840 million in loans.

These developments point to a grander direction:

Exchanges will increasingly support battle-tested on-chain services within their applications. This provides users higher yield opportunities and greater asset utility while allowing exchanges to expand services without taking on protocol risk.

In effect, on-chain services are being integrated into the backend of centralized exchanges, and the user experience is gradually migrating seamlessly on-chain.

Exchanges Will Build Their Own Ecosystems

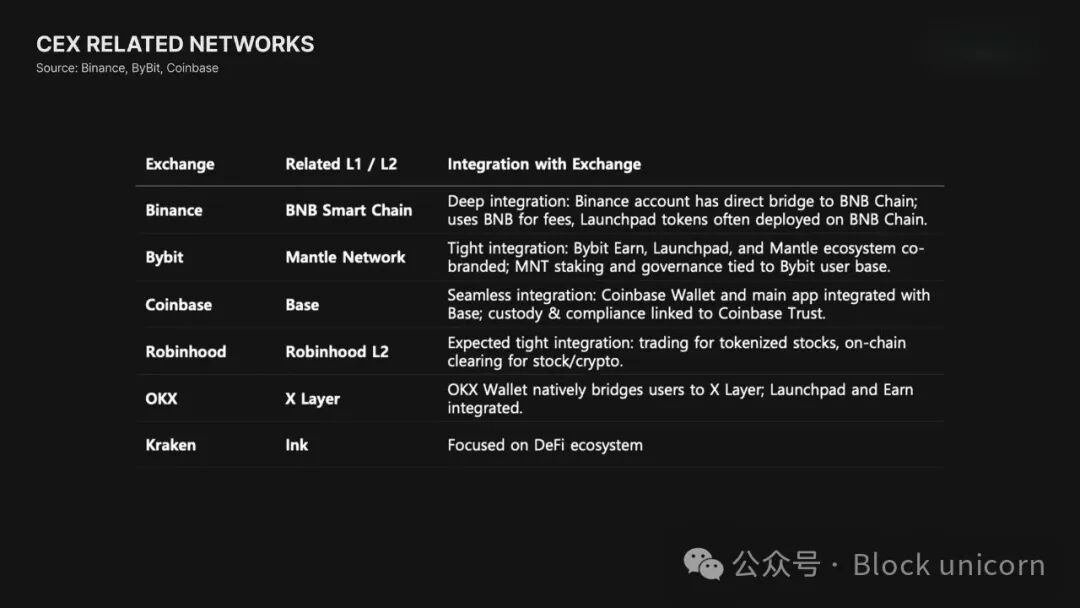

Exchanges no longer rely solely on external blockchains. They are increasingly building their own or closely partnering with blockchains that support their vertically integrated ecosystems.

The most prominent example is Binance's BNB Chain.

BNB started as a simple transaction fee discount token but has now evolved into a fully independent ecosystem hosting hundreds of projects, including DEXs, NFT marketplaces, RWA, and more. Binance uses this architecture to seamlessly migrate exchange users to its own on-chain services, thereby increasing the utility and demand for the BNB token.

Bybit has adopted a similar strategy with Mantle. Bybit builds trading incentives around the MNT token, bootstrapping users through designed liquidity incentives and ecosystem partnerships.

Coinbase, with its tens of millions of users, leverages Base to provide on-chain services for its exchange customers. Base has become home to popular apps like Morpho and Aerodrome, demonstrating how blockchains operated by centralized exchanges (CEX) can develop into vibrant on-chain environments.

In the US, Robinhood is preparing to launch its own Layer 2 blockchain, aiming to process tokenized stocks, options, and cryptocurrency trades directly on-chain, effectively merging its traditional brokerage infrastructure with a blockchain settlement system.

Vertical integration allows them to control trading, liquidity, user traffic, and settlement on a unified platform, creating tightly knit ecosystems for end-to-end circulation of digital assets.

4. Understanding Change is More Important Than Feeling It

Ethereum was born less than a decade ago. Just five years ago, the stablecoin market was only a few tens of billions of dollars, and the tokenization market was almost non-existent. Today, both have grown into multi-hundred-billion-dollar markets, becoming new cornerstones of global financial infrastructure.

The pace of future change will be faster, and its impact more diverse. Of course, on-chain services are not yet perfect; challenges related to security, ease of use, and regulation remain. But without understanding the current environment, one cannot grasp the next wave of opportunity. Change is not arriving slowly in the distant future; it is accelerating from subtle shifts that began long ago.

The elements of blockchain are no longer described in technical terms like "decentralization" but are expressed in the language of finance—yield products, cross-border remittances, payments. Only when more people learn to read and understand the world in the language of on-chain will they truly comprehend the changes reshaping the financial landscape.

This year marks the beginning of this shift. I hope more people can move beyond merely "feeling" this change and begin to truly understand and prepare for what comes next.