Author: Jay Yu

Compiled by: Jiahuan, ChainCatcher

For the world's fastest-growing tech companies, the public markets are not what they used to be. Thirty years ago, Amazon went public three years after its founding, with a valuation of $438 million. Netscape went public just eighteen months after its inception.

Today, however, the fastest-growing companies (Stripe, SpaceX, OpenAI, Ramp) often remain private for over a decade. The exposure to high-growth phases that investors could once easily access in the public markets has been quietly captured by private capital at ever-increasing book valuations.

“To put it cynically, [venture capital] captured the growth phase of early public companies. Amazon went public when its market cap was less than a billion dollars. That's almost unimaginable today.” – Bill Gurley

The market has responded with some makeshift fixes: Special Purpose Vehicles (SPVs), secondary market platforms, tender offers, and other tools designed to satisfy investor appetite for growth-stage risk assets. But these are patches, not fundamental solutions.

What investors truly crave might be the very vision that tech IPOs carried three decades ago: gaining broad, liquid investment exposure to era-defining companies and sharing in the outsized, venture-scale returns.

Tokenized risk assets could be part of the answer. This article explores, through three questions, how tokenizing startups could rebalance these disconnected markets:

(1) Why is now the right time for tokenized startups

(2) What does the landscape of tokenized startups look like

(3) What are the key opportunities, challenges, and unresolved tensions hindering the scaling of this space.

Part I: Why Tokenized Startups Are Timely?

Tokenized startups stand at the confluence of three major trends:

(1) The explosive growth of makeshift tools like SPVs as de facto liquidity mechanisms for era-defining tech companies

(2) The rapid growth of tokenized Real World Assets (RWA), spanning money markets, public equities, commodities, and more

(3) The breakdown of the “tokens vs. equity” consensus, where project tokens are increasingly relegated to second-class citizenship compared to venture equity investments.

1.1 The Rise of SPVs

A decade ago, SPVs were niche instruments, a way to pool capital outside traditional VC or public financing structures. But over the last two years, they have become a critical part of capital strategies, with platforms like AngelList, Carta, and Assure making it easier than ever to set up SPVs for specific opportunities and companies.

Secondary market SPVs, in particular, have grown over 545% in the last two years, with capital raised increasing over 10x. These makeshift market structures capture significant market growth: the weighted basket of Hiive's top 50 secondary market assets delivered 49.1% growth in 2025, significantly outperforming the S&P 500.

This suggests investors are using makeshift private market structures to reclaim functions the public markets once performed more smoothly: access, liquidity, and price discovery. As companies stay private longer, SPVs have become one of the primary alternatives.

1.2 RWA, Tokenization, and the Perpetualization of Everything

The second trend is the rise of tokenization and perpetual markets across asset classes.

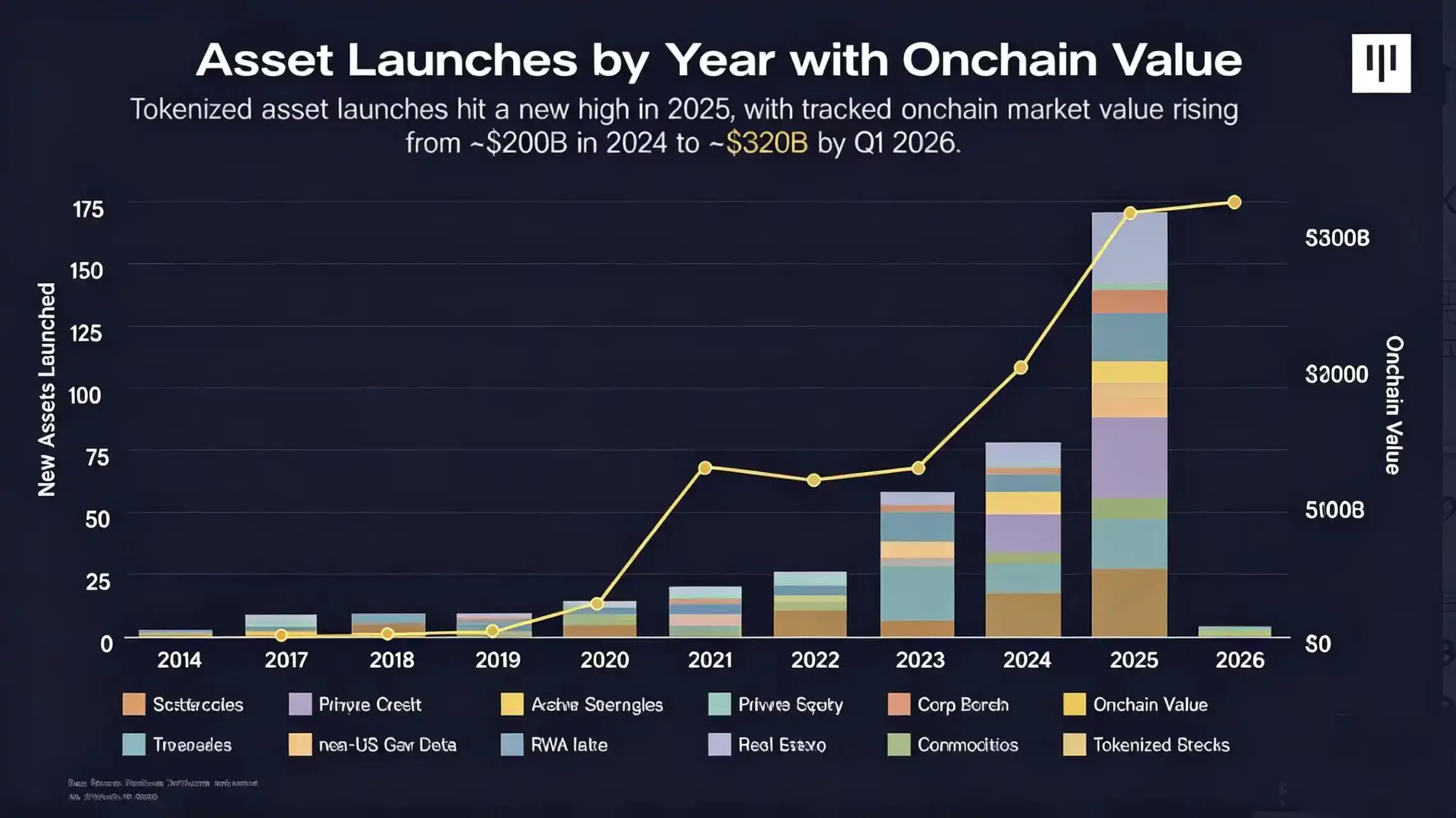

In Q1 2026, the value of on-chain RWAs reached approximately $320 billion. While the largest RWA category remains US Treasuries (used as collateral for stablecoins), significant growth is also seen in asset classes like commodities, equities, and asset-backed credit (such as Figure's home equity loans).

As RWAs gain adoption, we can see the tokenization supply chain maturing: spanning from issuers and custodians to regulatory frameworks.

Simultaneously, perpetual futures have seen tremendous growth over the last two years with the rise of perpetual decentralized exchanges (perp-DEXes) like Hyperliquid. Compared to derivatives with expiry dates, perpetual futures have no maturity, which offers practical execution advantages, easier risk understanding, and natively supports 24/7 trading.

Projects like TradeXYZ are also expanding perpetual futures beyond pure crypto pairs (e.g., BTC-USDC) to other asset classes, including US and Korean equities, commodities, and stock indices, offering a standardized approach for creating new perpetual markets via HIP-3.

1.3 The Breakdown of the “Tokens vs. Equity” Consensus

The third growing trend is the value-capture dilemma between tokens and equity.

DeFi project tokens like UNI and AAVE explicitly stated at issuance that they do not represent equity, addressing regulatory concerns. This created a “tokens vs. equity consensus,” where project tokens should act as synthetic instruments granting owners “governance” over parts of the protocol, with the promise of fee capture as a value accrual mechanism.

However, this created a two-tier system with zero-sum value capture, where token holders became second-class citizens to equity holders.

This issue became clear in recent events like the Aave DAO vs. Labs standoff and the controversial Circle acquisition of Axelar, where token holder interests were subordinated to equity interests.

All this prompts a reconsideration of the existing “tokens vs. equity consensus”: how can we design tokens that better reflect a project's upside potential?

The convergence of these three trends may pave the way for the rise of “tokenized startups”: tokenized investment exposure to companies with venture-scale upside potential, allowing the general public early access to era-defining companies like they had in public markets of the past.

In this way, tokens become a re-architected version of traditional IPO mechanisms, providing broader public access to the hottest blockbuster companies.

Part II: The Landscape of Tokenized Startups

2.1 Current Design Approaches and Trading Volumes

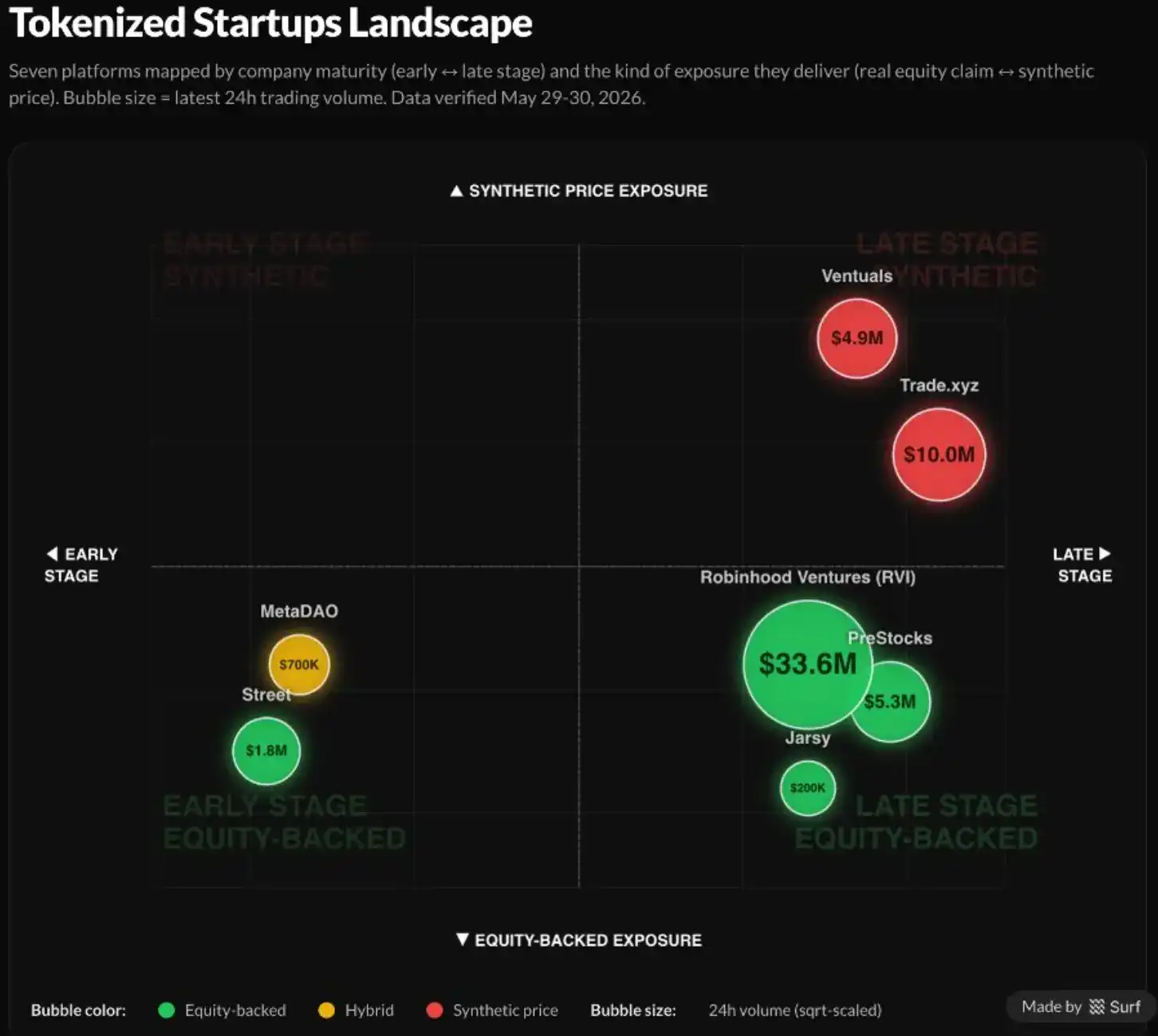

Today, tokenized startups vary widely across two main dimensions: the investment mechanism and the startup stage.

The investment mechanisms for tokenized startups range from SPV instruments holding equity (e.g., PreStocks), closed-end funds offering access to company equity (e.g., Robinhood Ventures), to pure perpetual futures that only offer price exposure without underlying equity ownership (e.g., TradeXYZ and Ventuals).

The startup stages range from early-stage companies (like MetaDAO's platform) to growth-stage assets, and household-name pre-IPO companies (like SpaceX, Anthropic, and OpenAI).

Mapping the main players in this space and their scale (24-hour trading volume as of May 30), we notice several distinct patterns.

First, the biggest trend is that later-stage (especially pre-IPO) platforms see volumes over 10x higher than early-stage ones. In particular, users seem to gravitate towards well-known names like SpaceX, Anthropic, Anduril, and OpenAI, regardless of which platform offers these assets.

Second, equity-backed tokenized startups (e.g., via Robinhood Ventures and PreStocks) typically have higher volumes than their perpetual counterparts. This is partly due to distribution advantages of Robinhood as a platform and TradeXYZ's conservative strategy of rolling out perpetuals one by one.

Notably, TradeXYZ's perpetual for Cerebras Systems has been massively successful, with daily volumes exceeding $30 million and providing accurate price discovery within less than a 3% error margin from the opening price.

Third, across this landscape, all platforms show a strong power-law concentration effect, with platform volume often dominated by fewer than three assets. For example, MetaDAO's volume is dominated by META, Avici, and Umbra; Street's volume is dominated by KLED.

Currently (as of May 30, 2026), TradeXYZ offers only SpaceX, and SpaceX also accounts for roughly half of PreStock's weekly volume. This heavy power-law effect likely indicates that, for most platforms, traders are more loyal to high-quality, high-profile assets than to the underlying platform itself.

2.2 Project Design Architectures

We can also dive into individual projects within this landscape map to carefully examine the trade-offs of various design schemes in this field, from perpetual exposure to SPV-backed equity structures.

Note: Platform comparisons and feature descriptions in this analysis represent the author's perspective based on public information as of May 30, 2026. Descriptions of platform strengths and weaknesses do not constitute investment advice.

Part III: Challenges and Opportunities for Tokenized Startups

Today, tokenized startups are still in their infancy, and their design space is filled with numerous opportunities and challenges.

3.1 Transfer Consent and Team Alignment

Currently, one of the most pressing questions for spot tokenized startup platforms is whether these projects align with or go against the interests of company founding teams, especially given that platform volumes are disproportionately concentrated on 1 to 3 high-quality assets.

This is particularly true for high-profile, pre-IPO companies like SpaceX, Anthropic, and OpenAI, which carry most of the pre-IPO demand and trading volume.

Without team approval, a company might publicly announce opposition to tokenization, leading to cancelled sales and subsequent token price crashes, as shown by Anthropic's opposition to secondary market SPVs and OpenAI's opposition to Robinhood's stock tokens.

Typically, growth-stage companies pursuing a public listing have four clear motivations: (1) access to public market capital; (2) real-time pricing; (3) liquidity exit for founding teams and investors; and (4) prestige signaling.

Today, the proliferation of “mega-funds” in the growth stage provides an incredibly robust and abundant financing environment for the hottest startups, often at extremely high valuations. This landscape undermines motivations (1) and (2) for growth-stage companies to go public: they no longer need to turn to public markets for capital, and real-time pricing risks a downward re-rating.

Thus, in today's financing environment, a hot growth-stage startup might only consider going public if a large number of early employees and investors crave immediate liquidity (as with Facebook's 2012 IPO) or as a prestige symbol representing maturity.

For a spot tokenized startup platform seeking board approval in the current financing environment to provide direct ownership access, these latter two motivations carry significantly more weight.

Traditional secondary market brokers like Forge and Hiive cater more to liquidity motivations, while high-profile closed-end funds like Robinhood Ventures and USVC arguably cater to prestige motivations.

Nevertheless, beyond traditional IPO motivations, a range of emerging designs have surfaced, such as tokenized startup baskets, tokenized accelerator models, and tokenized community offerings, which could address this founder alignment issue:

Tokenized startup baskets refer to tradeable portfolios of growth-stage startups, rather than a single tokenized company.

This is one avenue provided by closed-end funds like Robinhood Ventures. This mechanism can satisfy liquidity, prestige, and even capital access motivations while alleviating downward re-rating pressure from “real-time pricing” through the use of Net Asset Value (NAV) multiples (somewhat similar to DAT).

The tokenized accelerator model applies traditional accelerator and incubator models (e.g., YC, HF0, South Park Commons) to help startups go from 0 to 1 in exchange for consent to tokenize their shares.

We see launch platforms like Street and MetaDAO effectively offering this model; they solve founder alignment by taking the founder's side and genuinely helping founders grow.

Tokenized community offerings might be the most interesting and promising model to explore for tokenized startups. As the 2020 Uniswap airdrop demonstrated, tokens can be an excellent incentive for everyday users who use a product daily.

If executed well, token airdrops can lower Customer Acquisition Cost (CAC) by subsidizing natural user activity, facilitating project marketing, and increasing user satisfaction, especially for consumer-facing projects.

For example, Revolut conducted a community equity round, raising $1.3 million from early users at a $40 million valuation. This served a marketing function, turning users into owners and advocates, with those early backers receiving 400x returns.

However, token airdrops can also be a double-edged sword; many crypto project airdrops have been plagued by farming, accusations of insider allocations, and immediate sell pressure.

3.2 Non-U.S. Jurisdictions

Another avenue to bypass founder alignment issues is going global. Much of the current discussion around tokenized startups (and their trading volumes) takes a U.S.-centric view, focusing on the hottest U.S. companies and assuming a U.S. public listing.

But the U.S. public and private capital markets already serve growth-stage companies exceptionally well, making it difficult to justify the additional benefits of a tokenized offering to a company.

However, this isn't necessarily the case in other regions, where local capital markets may be inefficient and fail to provide the best liquidity or pricing for the fastest-growing companies. For example, Wise initially listed on the London Stock Exchange in 2021.

But in May 2026, it moved its primary listing to Nasdaq in the U.S., believing it could attract a more liquid market, reach a broader base of retail and institutional investors, and receive more generous valuation multiples.

This geographical divergence in valuation and capital access is also evident in the differences in valuation multiples between U.S. and Chinese AI companies.

U.S. AI leaders often command Price-to-Sales ratios of 15 to 40x, while Chinese AI companies have much more conservative P/S ratios, closer to 5 to 15x. This discount may be partly attributed to capital access; Chinese capital markets are generally harder to access than U.S. markets.

This geographical valuation arbitrage becomes particularly interesting as different parts of frontier supply chains like AI, robotics, semiconductors, and biotechnology are dispersed globally, and related companies list in Asian and European markets.

Despite this structural advantage for tokenized startups in non-U.S. jurisdictions, empirical experiments and trading volumes remain limited. This is likely due to the difficulty of finding high-demand startups willing to experiment on their cap tables and the complex regulatory environments concerning foreign investment and tokenization in those regions.

South Korea is a particularly interesting non-U.S. market for tokenized startups.

Korea possesses:

(1) Several national champion companies within the AI supply chain with global investor demand, such as Samsung and SK Hynix

(2) A new legal framework for “stock tokens”;

(3) Brokers actively focusing on pre-IPO investments;

(4) More crypto investors than stock investors.

This is perhaps partly why TradeXYZ is actively beginning to list perpetuals on Korean equities.

One of tokenization's biggest advantages is its ability to arbitrage geography, providing global audiences with underlying access to companies worldwide.

With their global liquidity bases and potential to open to broader retail and institutional investors, tokenized startup platforms could well become part of the upgraded IPO strategy for the next generation of fast-growing, non-U.S. companies that lack strong local capital markets, like Wise.

3.3 Price Discovery Design for Perpetuals

Another route for tokenized startup platforms is the perpetual strategy. If all you own is a synthetic instrument that doesn't represent underlying equity, there's nothing for a board to void. This circumvents the need for team intervention and board approval. However, synthetic assets trade legal issues for price discovery challenges.

Existing perpetual markets (e.g., for crypto tokens, equities, commodities) typically rely on liquid spot markets and reliable price oracles to manage funding rates and synthetic prices. However, by definition, private startups lack liquid public markets.

The closest available markets are tender offers and secondary market purchases, which platforms like Ventuals leverage to anchor their funding rates. But these are often unreliable and frequently undervalue the underlying asset.

For instance, on Ventuals, the funding rate is around 15% APY within +/-5% of the oracle price, becoming punitively expensive for longs beyond that range via an exponential curve.

TradeXYZ takes the opposite approach, relying on oracle-free price discovery. For example, in the Cerebras Systems offering, TradeXYZ simply set up a Hyperp mechanism using recent market quotes to derive a reference price, letting the contract discover its own price within the narrow window between S-1 filing and actual listing. It outperformed any other mechanism on the market.

The CBRS perpetual launched on May 1 with a reference price of $175, traded within a stable range of $288 to $320 for two weeks, reaching around $340 an hour before opening, less than 3% from the actual Nasdaq opening price of $350.

This estimate was about 84% higher than the banker-priced $185 and far more accurate than prices from secondary market brokers like Hiive ($225) and Forge ($113.50). This fully demonstrates the tremendous success of perpetuals as a tool.

However, this process is not necessarily scalable, as clear price discovery relies on an imminent, verifiable convergence event. If Cerebras hadn't listed within a specific timeframe, the contract would have settled at a time-weighted average of its own price.

In this sense, the “perpetual price discovery” mechanism ultimately looks more like a traditional futures contract and also may not apply to early-stage assets with no imminent public offering.

Thus, the design space for perpetual-based tokenized startups remains wide open. Scalable models are not yet established, and it will likely be a fusion of crypto perpetuals with traditional futures, prediction markets, secondary spot markets, Contracts for Difference (CFDs), and other primitives.

With Kalshi's recent foray into perpetuals and Hyperliquid's entry into outcome prediction markets with HIP-4, we are seeing an important convergence of all these different pricing tools. Pricing pre-IPO tokenized startups could well become the catalyst for pioneering a new derivative space, one more efficient and user-friendly for everyday users.

3.4 Legal Structures and Regulation

From a legal structure perspective, many of these tokenized startup instruments, such as Street's ERC-S, MetaDAO's DAO LLC, and SPV-backed tokens, are novel, experimental tools that haven't yet withstood the test of time against regulators with strong enforcement intent.

Even the recent U.S. Clarity Act for digital commodities did not address the issue of tokenized equity.

Based on public statements, the SEC appears to categorize these tokenized startups into two distinct buckets depending on whether the token is issued directly by the company or by a third party.

Issuer-sponsored tokens are securities themselves, just in a different form, and thus fall under traditional securities laws. Whether the official ledger is on-chain (transferring the token transfers the share) or off-chain (the token triggers a ledger update), it is treated exactly like ordinary stock: must be registered or qualify for an exemption, with all standard disclosure and reporting obligations.

Third-party tokens are treated based on what they actually convey. Custodied tokens are security entitlements under UCC Article 8—actual securities transactions, but a claim against a custodied share, not the share itself, meaning you also bear custodian bankruptcy risk.

Synthetic tokens are entirely separate securities issued by a third party, carrying no rights against the reference company, and require separate registration or an exemption: linked securities (notes or SPVs tracking the target's value) fall here; and security-based swaps (e.g., Ventuals-style perpetuals) are most restricted, prohibited from being offered to ordinary U.S. retail unless registered and traded on a national exchange.

Conclusion

Whether it's pre-IPO perpetuals or SPVs, closed-end funds, or secondary market tender offers, every instrument is an attempt to win back what public markets once freely offered to the masses: the ability to gain early, liquid investment exposure during a company's highest growth phase, instead of letting it be monopolized by growth equity funds.

Today, we know this demand is real, but the infrastructure remains incomplete. For tokens, the stakes are higher. The past few years have been an identity crisis: project tokens relegated to second-class citizens, governance becoming a charade, and value accumulating elsewhere.

Re-architecting the issuance mechanism to give tokens true claims to venture-scale upside might be the epochal mission that sets them free. With an infrastructure the first wave never had, tokens might finally re-deliver on the core promise they made during the early days of fervor.