Автор: Чжао Ин

Источник: Wall Street CN

Трамп лично проведет церемонию приведения к присяге нового председателя ФРС Кевина Уорша. Это нарушающее недавние традиции решение вновь выводит на первый план продолжающуюся уже 70 лет борьбу за власть между Белым домом и Федеральной резервной системой. История показывает, что каждый председатель ФРС ищет баланс между политическим давлением и независимостью политики, и Уорш не исключение — однако ситуация, в которой он оказался, гораздо сложнее, чем кажется со стороны.

Как сообщили источники из Белого дома, на которые ссылается The Wall Street Journal, Трамп проведет церемонию присяги Уорша в Белом доме в эту пятницу. Этот шаг нарушает недавние традиции — обычно инаугурация проходит внутри ФРС, и действующий президент редко присутствует. Последний раз церемония приведения к присяге председателя ФРС в Белом доме проходила в 1987 году, когда в должность вступал Алан Гринспен, почти сорок лет назад.

Команда по анализу облигаций Caitong Securities (Сунь Биньбинь, Суй Сюпин, Лу Синьчэнь) в своем последнем исследовательском отчете отмечает, что хотя Уорш не является «голубиным председателем», нельзя исключать, что снижения ставок в этом году не будет — отношения между председателем ФРС и президентом США не статичны, а меняются в зависимости от обстоятельств.

Однако Уорш возглавляет не готовую к действию ФРС. На заседании FOMC в конце апреля три члена совета управляющих — Хаммак из Кливленда, Кашкари из Миннеаполиса и Логан из Далласа — подали самые необычные с октября 1992 года голоса «против» — они возражали не против самого снижения ставок, а считали, что даже намеков на него быть не должно. Это означает, что Уорш унаследовал центральный банк, внутри которого уже появились трещины, в то время как Трамп от него, как раз, ожидает снижения ставок.

Инаугурация в Белом доме: мероприятие, наполненное политическими сигналами

Сама организация церемонии инаугурации уже посылает сильный сигнал. Когда Джером Пауэлл вступал в должность в 2018 году, церемония проходила внутри ФРС, и Трамп лично не присутствовал; последним действующим президентом, посетившим инаугурацию, был Джордж Буш-младший, присутствовавший на церемонии присяги Бена Бернанке в 2006 году. Личное проведение церемонии Трампом прямо демонстрирует его пристальное внимание к данному назначению в ФРС.

На процедурном уровне процесс передачи полномочий также оказался необычно длительным. Уорш был утвержден Сенатом на прошлой неделе, получив четырехлетний срок полномочий; срок полномочий Пауэлла на посту председателя истек в прошлые выходные, но он заявил, что останется в совете управляющих ФРС в качестве члена совета, чей срок полномочий продлится до января 2028 года. Уорш ранее также согласился избавиться от части личных инвестиций до официального вступления в должность, что в определенной степени замедлило процесс передачи полномочий. В переходный период вице-председатель ФРС Филип Джефферсон представлял центральный банк на встрече министров финансов и глав центральных банков стран «Большой семерки» в Париже в этот понедельник.

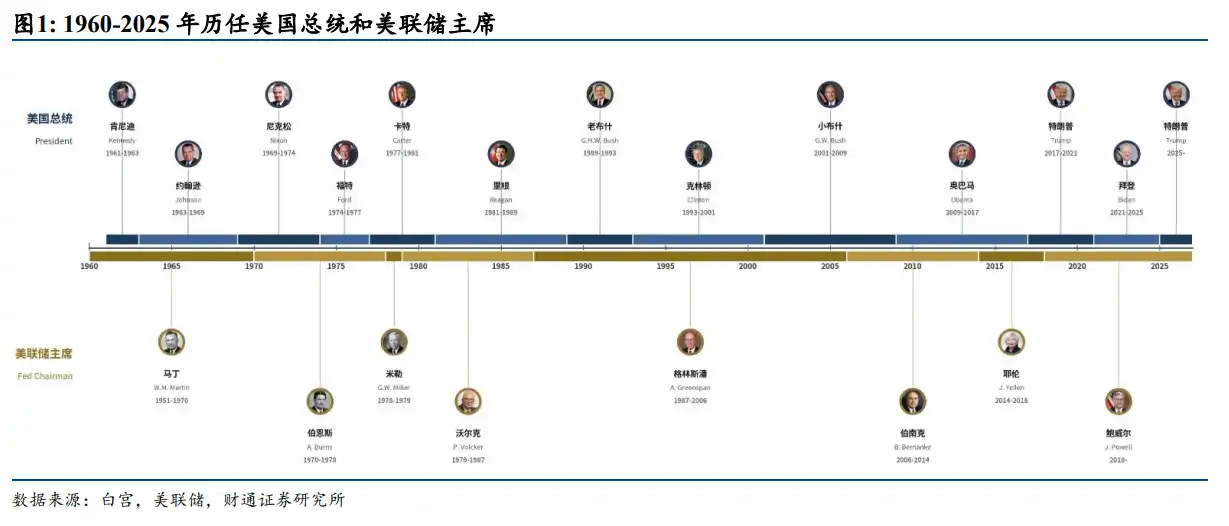

70-летняя история противостояния: от Мартина до Пауэлла

Отчет Caitong Securities систематически описывает историю отношений между председателями ФРС и президентами с 1960 года, рисуя четкую эволюционную траекторию.

Уильям Мартин, в отсутствие защитных институциональных барьеров, мог защищать независимость, полагаясь только на личную репутацию. Вступив в должность, он отказался быть агентом Министерства финансов, способствовал переносу центра принятия решений ФРС из Нью-Йорка в Вашингтон и расширил полномочия по принятию решений на весь FOMC. Трумэн, встретив его на улице Нью-Йорка, только бросил: «Предатель» и ушел.

Провал Артура Бернса был вызван тем, что он сам не верил, что монетарная политика может положить конец инфляции, что открыло двери для политического давления со стороны Никсона. Никсон оказывал давление через личные письма, вмешивался в состав совета управляющих и даже отправлял старших советников для прямых выговоров сотрудникам ФРС. Бернс формально сохранил институциональную независимость, но пошел на серьезные уступки в содержательном направлении политики, что в конечном итоге подорвало доверие к ФРС.

Уильям Миллер представлял собой наиболее прямой режим политической координации — его намеренно выбрали для соответствия политическим целям Картера, но в итоге это обернулось против него перед лицом внешнего кризиса. Летом 1979 года инфляция стала самым большим политическим кризисом для Картера, Миллер был переведен на пост министра финансов, освободив место для назначения настоящего ястреба в борьбе с инфляцией.

Пол Волкер повысил уровень независимости от «защиты личной репутации» до тройной линии обороны: «личная репутация + институциональные рамки + рыночная репутация». Картер, зная, что назначение Волкера будет иметь политическую цену, все равно сделал этот выбор — как сказал его политический советник Айзенштадт, это «в конечном итоге вытеснило его со второго срока, одновременно вытеснив инфляцию ценой высокой безработицы». Рейган, хотя и отдал Волкеру «приказ» не повышать ставки перед выборами 1984 года, а в 1986 году попытался организовать «засаду в FOMC» через назначенных им членов совета, в конечном итоге так и не смог существенно изменить курс политики.

Алан Гринспен технократической риторикой свел противостояние под ковер, вступив в ожесточенный конфликт с Джорджем Бушем-старшим, достигнув «вашингтонского перемирия» с Клинтоном, но при Джордже Буше-младшем перешел границы, поддержав снижение налогов, став первым в истории председателем ФРС, активно «вторгшимся» в сферу фискальной политики.

Бен Бернанке олицетворяет модель естественного сближения Белого дома и ФРС в условиях кризиса, основное давление на него оказывали Конгресс и сама ФРС, а не Белый дом. Джанет Йеллен отвечала на атаки Трампа «неполитизированным языком + строгим самоограничением», став первым со времен отказа Картера переназначить Бернса председателем ФРС, замененным новым президентом.

Джером Пауэлл столкнулся с наиболее серьезным со времен Бернса давлением со стороны президента. Во время первого срока Трампа Пауэлл, под совместным воздействием внешнего политического давления и внутренней экономической оценки, трижды подряд снизил ставки в 2019 году и прекратил сокращение баланса; во время второго срока, столкнувшись с такими методами, как запущенное Трампом расследование по поводу перерасхода средств на реконструкцию здания ФРС в Вашингтоне и намеки на увольнение, ответ Пауэлла значительно ужесточился, подняв защиту независимости ФРС до беспрецедентно высокого уровня: юридическое оформление, документальное закрепление, публичность. На своем последнем заседании в качестве председателя FOMC проголосовал с редким разрывом 8 против 4 за сохранение ставок без изменений.

Дилемма Уорша: новый председатель под двойным давлением

Ситуация, которую унаследовал Уорш, исторически довольно необычна — он одновременно сталкивается с давлением со стороны Белого дома на снижение ставок и с сопротивлением ястребов внутри FOMC.

Уорш не является традиционным голубем. В 2006 году, в возрасте 35 лет, он был назначен Джорджем Бушем-младшим членом совета управляющих ФРС, став одним из самых молодых членов совета в истории ФРС. После официального запуска QE2 в 2010 году он стал единственным членом FOMC, публично подвергшим сомнению направление экспансии, и ушел в отставку досрочно в 2011 году, что рынок широко интерпретировал как молчаливый протест против чрезмерного смягчения ФРС. Его происхождение из инвестиционного банкинга Morgan Stanley, опыт работы исполнительным секретарем Совета по национальной экономике (NEC) Белого дома, а также тесные связи с ядром Республиканской партии делают ожидания в отношении его политической независимости не ниже, чем у председателей с аналогичным бэкграундом в истории.

В отчете Caitong Securities изложены четыре ключевых момента из недавних выступлений и ответов на вопросы журналистов Уорша:

- Во-первых, его определение независимости ФРС более тонкое, чем у предшественников. Он считает, что высказывания политиков о монетарной политике не влияют на независимость ФРС. Это одновременно является способом десенсибилизации к давлению Трампа и оставляет пространство для защиты независимости политики в будущем без открытого конфликта.

- Во-вторых, он негативно относится к прогнозным ориентирам (forward guidance), и рынку, возможно, придется привыкнуть к более «молчаливой» ФРС.

- В-третьих, он очень серьезно относится к проблеме инфляции, прямо отвергая мнение Трампа о том, что рост цен на нефть — это «фальшивая инфляция».

- В-четвертых, он считает, что рост производительности благодаря искусственному интеллекту сделает снижение ставок возможным, что имеет схожую логическую структуру с прозрением Гринспена о бусте производительности в конце 1990-х годов.

Снижение ставок и сокращение баланса: направление определено, темп осторожен

Caitong Securities считает, что монетарная политика после вступления Уорша в должность, скорее всего, будет характеризоваться как «направление определено, но темп осторожен».

В отношении темпа снижения ставок, инфляция уже пять лет подряд превышает целевой показатель, приоритетом является стабилизация инфляционных ожиданий. Серьезное отношение Уорша к инфляции, особенно его отрицание «теории фальшивой инфляции», указывает на то, что он не станет легко снижать ставки, пока инфляция не вернется в целевой диапазон. В краткосрочной перспективе рост спроса, вызванный инвестициями в дата-центры, может дополнительно нейтрализовать пространство для снижения ставок, что приведет к замедлению темпов снижения из-за ограничений по данным. В отчете отмечается, что если Трамп проявит больше уважения к Уоршу, снижение ставок может наступить раньше; если Трамп продолжит оказывать сильное давление, для защиты независимости ФРС Уорш, напротив, будет склонен отложить снижение ставок.

Что касается темпа сокращения баланса, Уорш считает, что расширенный баланс фактически расширил границы монетарной политики ФРС до фискальной сферы, поэтому сокращение баланса логически необходимо. Однако он также признает, что ФРС потратила 18 лет на накопление такого размера баланса, и сокращение — не дело одного дня; ожидается, что оно будет проходить медленно и методично. Кроме того, запуск сокращения баланса без снижения ставок почти равносилен сознательному разжиганию конфликта с Белым домом — это также определяет, что сокращение будет продвигаться такими темпами, чтобы избежать прямого противостояния до начала цикла снижения ставок.

Ключевой вывод Caitong Securities: воспроизведение стиля управления Гринспена и возвращение к режиму дефицита резервов (scarce reserves) прежде всего требует заручиться поддержкой внутри самой ФРС, спешка может привести к обратным результатам. При оценке будущего политического курса Уорша не следует смотреть только на его личную позицию или текущие отношения с Белым домом, а нужно вернуться к макротенденциям — уровню инфляции, эластичности роста, направлению цен на нефть, жесткости/слабости финансовых условий — и моделировать его наиболее вероятный выбор в различных сценариях.