На фоне двойного удара геополитического конфликта и возобновления инфляции ожидания рынка относительно снижения ставок ФРС переживают сильные колебания.Ключевой вопрос рыночной игры заключается в следующем: приведут ли высокие энергетические цены к устойчивой инфляции или же они подорвут потребительский спрос, вынудив ФРС пойти на снижение ставок?

21 апреля, по данным трейдинговой платформы, Citi в своем последнем исследовательском отчете привела четкие аргументы в пользу снижения ставок, считая, что перебои с поставками нефти носят временный характер, и хотя снижение ставок будет непростым, направление движения очевидно; в то время как Deutsche Bank выступила с пессимистичным прогнозом, предупредив, что политика ФРС уже находится в нейтральной зоне, и ожидается, что текущие ставки будут сохраняться неопределенно долго.

На фоне противостояния мнений двух крупных инвестиционных банков,即将公布的 данные о розничных продажах за март станут ключевым пробным камнем для打破僵局. Эти данные не только раскроют реальное разрушительное воздействие высоких цен на нефть на核心消费, но и напрямую определят近期路径 политики ФРС.

Citi: Геополитические потрясения временны, основное направление снижения ставок неизменно

Несмотря на continued влияние геополитических событий на рынок, Citi твердо уверена, что путь к более низким ставкам и более мягкой политике ФРС依然 существует.

Ключевая логика этого заключения заключается в следующем:воздействие ситуации в Ормузском проливе на поставки нефти все более вероятно является кратковременным, а не устойчивым источником инфляции.18 апреля появились сообщения о том, что Ормузский пролив будет вновь открыт, и хотя позже они были поставлены под сомнение, доходности по казначейским облигациям и цены на нефть уже отступили от максимумов в четверг и остаются на относительно низких уровнях — это само по себе говорит о том, что рынок закладывает в цены сценарий «кратковременного шока».

В отчете указывается, что логическая цепочка Citi清晰:краткосрочный геополитический конфликт → нефтяной шок не持久 → инфляционное давление не распространяется → ФРС имеет условия для возврата на track снижения ставок.

Кроме того, ряд отслеживаемых Citi базовых экономических данных показывает, что макрофинансовая среда претерпевает微妙ные изменения:

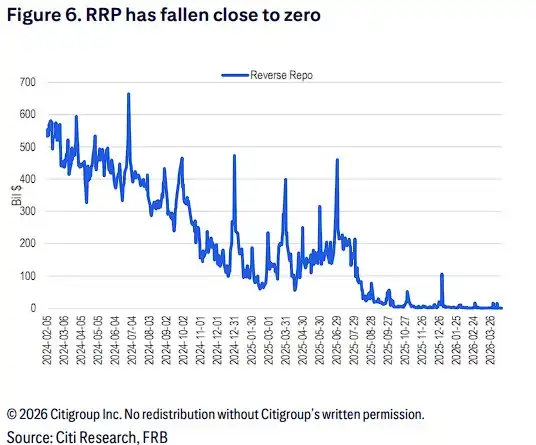

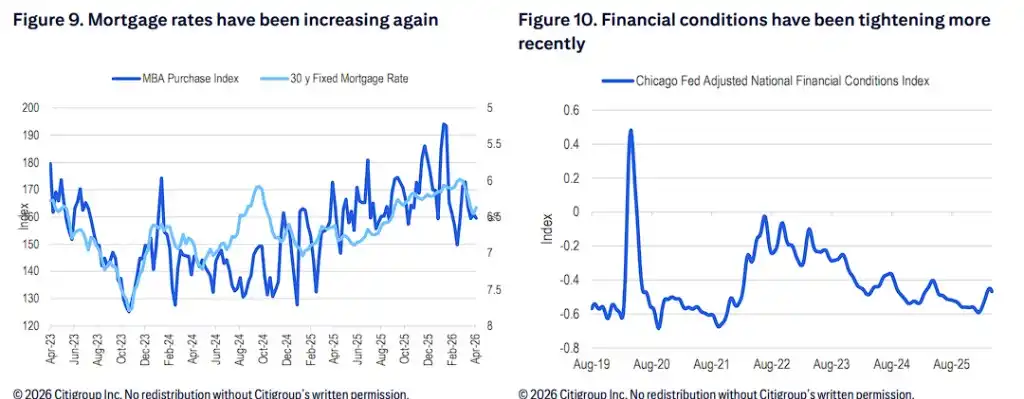

Ликвидность и финансовые условия:Объем операций обратного РЕПО (RRP) ФРС значительно сократился, приблизившись к нулевому уровню; в то же время,近期 финансовые условия ужесточаются, ипотечные ставки также вновь демонстрируют тенденцию к росту.

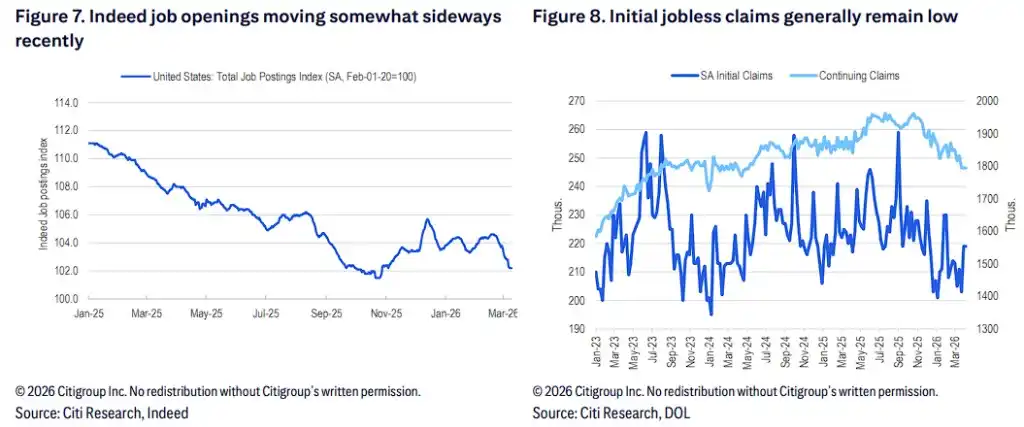

Рынок труда:Данные по вакансиям Indeed в近期 демонстрируют боковой тренд, однако количество первичных заявок на пособие по безработице в целом остается на низком уровне.

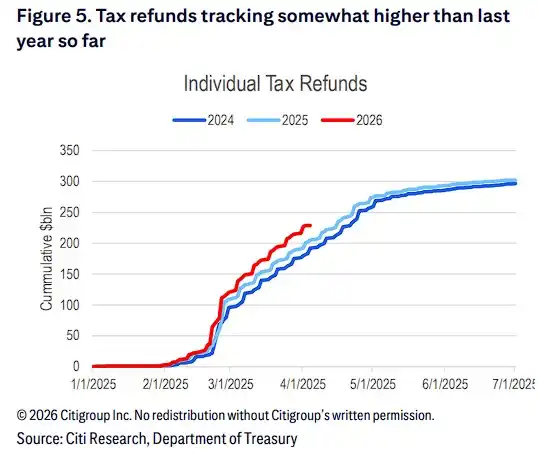

Денежные потоки:На данный момент, налоговые возвраты для физических лиц в этом году (совокупный объем исчисляется миллиардами долларов) в целом slightly выше, чем за аналогичный период прошлого года.

Ключевой пробный камень сегодня: почему данные по «контрольной группе» розничных продаж за март так важны?

В условиях колебаний ожиданий снижения ставок,即将公布的 данные о розничных продажах за март предоставят инвесторам первые зацепки, раскрывая, в какой степени высокие цены на бензин сократили потребительские расходы на другие товарные категории.

Citi подчеркивает, что инвесторы должны «отделять表象» при интерпретации этих данных. Из-за роста цен на бензин, номинальный объем розничных продаж в марте必然 резко возрастет. Однако,真正 определяющим для политического курса ФРС являются данные по продажам «контрольной группы» (Control group).

В отчете указывается, что эти данные исключают продажи на АЗС и某些特定 категорий, что позволяет более真实но и точно отразить, привело ли подорожание бензина к слабости потребительских расходов в других сферах. Если данные по «контрольной группе» неожиданно окажутся слабыми, это станет веским подтверждением того, что высокая инфляция подрывает спрос, предоставив thus ключевую数据支撑 для логики снижения ставок ФРС.

Холодный душ от Deutsche Bank: политика достигла нейтрального уровня, ФРС может бездействовать неопределенно долго

В резком контрасте с оптимистичными ожиданиями Citi, Deutsche Bank дала крайне осторожную оценку перспективам снижения ставок. В своем исследовательском отчете Deutsche Bank четко указала: ФРС, как ожидается, будет维持 текущие ставки неопределенно долго, поскольку текущая политика уже находится в нейтральном положении.

Пессимистичные ожидания Deutsche Bank в основном основаны на следующих ключевых моментах:

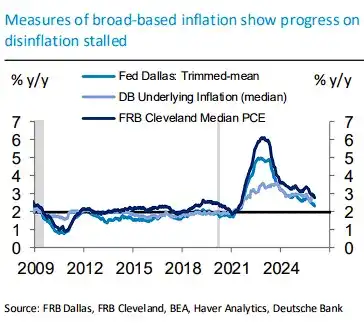

Застой в снижении инфляции:Широкие показатели инфляции показывают, что прогресс США в борьбе с инфляцией застопорился.

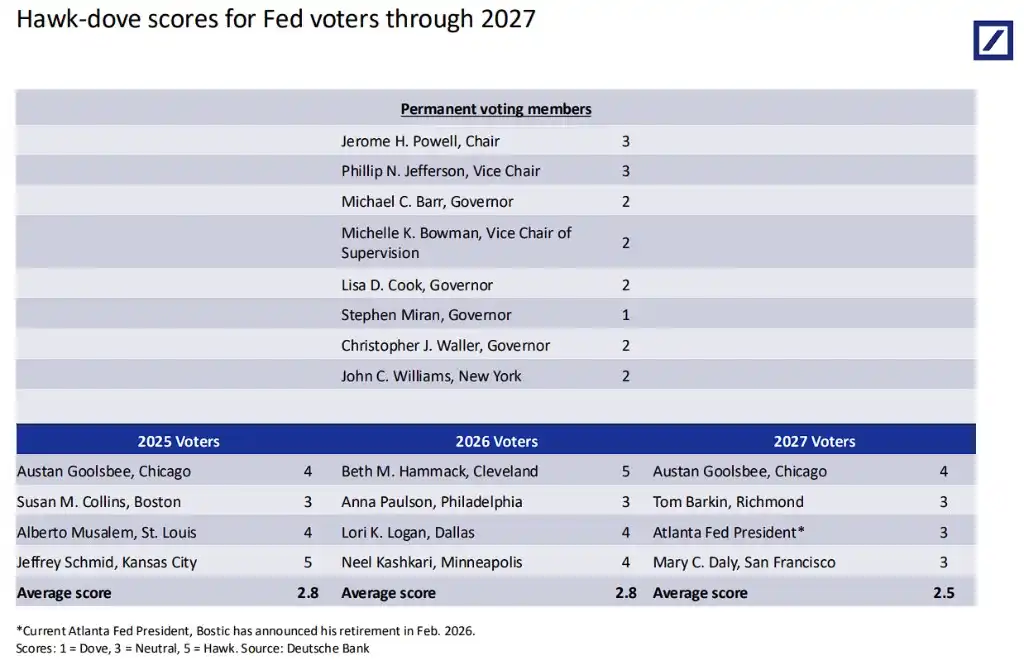

Ужесточение позиции официальных лиц:Мониторинг Deutsche Bank выступлений официальных лиц ФРС показывает, что Уоллер (Waller) и Миран (Miran)等 уже заняли более ястребиный тон, в то время как большинство其他官员 продолжают считать текущую политическую позицию «очень подходящей» (well positioned). Конкретно如下:

· Уоллер (Waller): Настроен более ястребино. Он указал, что затяжной ближневосточный конфликт заблокирует путь к снижению ставок; серия шоков (пошлины плюс цены на нефть) может вызвать более устойчивый рост инфляции; он также подчеркнул, что базовая инфляция с учетом влияния пошлин близка к 2%, а на рынке труда存在уязвимости;

· Миран (Miran): В настоящее время является самым голубиным голосом, поддерживает снижение ставок 3 или даже 4 раза в этом году, считает, что война не изменила инфляционные перспективы через 12-18 месяцев, шок от цен на нефть носит временный характер;

· Уильямс (Williams): Считает, что политика «находится именно там, где нужно», повысил прогноз по инфляции на 2026 год до около 2.75%, понизил прогноз экономического роста на 2026 год до 2%-2.5%;

· Хаммак (Hammack): Четко заявил, что ставки будут «оставаться неизменными в течение довольно долгого времени»;

· Гулсби (Goolsbee): Предупредил, что если цены на нефть останутся на уровне 90 долларов за баррель, это может распространиться на другие цены; дальнейшее снижение ставок в 2026 году маловероятно, снижение, возможно, придется ждать до 2027 года;

· Дейли (Daly): Считает, что текущая политика находится в «очень хорошем положении», если шок от цен на нефть продлится до конца года, не будет неожиданностью, если рыночные цены сместятся в сторону «нулевого снижения ставок».

Протоколы мартовского заседания ФРС также показали, что подавляющее большинство官员 считают, что процесс возврата инфляции к цели в 2% затянется; некоторые官员甚至 обсуждали необходимость включения в заявление формулировок о «двусторонних рисках», намекая, что возможность повышения ставок не полностью исключена.

Рейтинг ястребов и голубей ФРС от Deutsche Bank показывает, что средний балл комитета по голосованию 2026 года составляет 2.8 балла (1 — самый голубиный, 5 — самый ястребиный), в целом склоняясь к нейтрально-голубиному, но голубиные голоса явно находятся в меньшинстве.

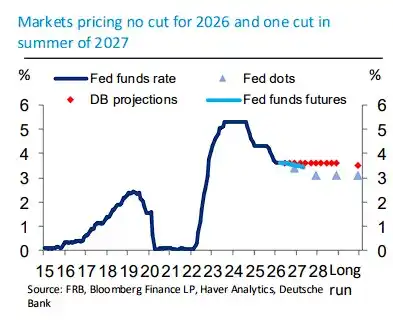

Полный разворот рыночных цен:Перед лицом устойчивого инфляционного давления и强劲的经济韧性 рыночные ожидания претерпели drastic changes. Согласно данным Deutsche Bank, в настоящее время рыночные цены предполагают «нулевое снижение ставок» в течение всего 2026 года, и лишь к лету 2027 года произойдет одно снижение.

Deutsche Bank ожидает, что в базовом сценарии ставка по федеральным фондам будет维持 на уровне 3.63% в течение всего периода с 2026 по 2028 год, без какого-либо снижения в течение года.