Редакционное примечание: На фоне роста широкого спектра активов, временная стагнация BTC и ETH часто упрощенно объясняется их «характеристиками рисковых активов». В данной статье утверждается, что ядро проблемы заключается не в макроэкономике, а в этапе декредитования (делевериджа) самого крипторынка и его структуре.

По мере того как процесс избавления от杠杆 (левериджа) подходит к концу, а активность торгов снижается до низких уровней, существующим на рынке капиталам трудно противостоять краткосрочным колебаниям, усиленным высоким杠杆ом мелких инвесторов, пассивными капиталами и спекулятивными сделками. До возвращения новых капиталов и настроений FOMO (страх упустить выгоду) рынок более чувствителен к негативным нарративам, что является структурным результатом.

Исторические аналогии показывают, что такое поведение, скорее всего, является фазой корректировки в рамках длительного цикла, а не отказом фундаментальных основ. Данная статья пытается выйти за рамки краткосрочных взлетов и падений, чтобы с позиций циклов и структуры заново осмыслить текущее положение BTC и ETH.

Далее следует оригинальный текст:

Биткоин (BTC) и Эфириум (ETH) в последнее время явно отстают от других рисковых активов.

Мы считаем, что основными причинами этого явления являются: этап торгового цикла, микроструктура рынка, а также манипуляционные действия некоторых бирж, маркет-мейкеров или спекулятивных фондов.

Контекст рынка

Во-первых, начавшееся в октябре прошлого года падение, связанное с делевериджем, нанесло тяжелый удар по участникам с высоким杠杆ом, особенно трейдерам-ритейлерам. Большое количество спекулятивных капиталов было вымыто с рынка, что сделало рынок в целом уязвимым и склонным к избеганию риска.

В то же время акции, связанные с ИИ, в Китае, Японии, Южной Корее и США пережили чрезвычайно агрессивный рост; рынок драгоценных металлов также пережил всплеск, движимый настроением FOMO (страх упустить выгоду), похожий на «мем-тренд». Рост этих активов поглотил значительные средства мелких инвесторов — и это особенно важно, поскольку розничные инвесторы из Азии и США по-прежнему остаются основной торговой силой на крипторынке.

Другая структурная проблема заключается в том, что криптоактивы еще не интегрированы в традиционную финансовую систему. В традиционной финансовой системе товары, акции и иностранная валюта могут торговаться на одном счете, а переключение между активами практически не имеет трения; однако в реальности перевод средств из TradFi (традиционные финансы) на крипторынок по-прежнему сталкивается с множеством препятствий — регуляторных, операционных и психологических.

Кроме того, доля профессиональных институциональных инвесторов на крипторынке все еще ограничена. Большинство участников не являются профессиональными инвесторами, им не хватает независимых аналитических框架ов, они легко подвержены влиянию спекулятивных капиталов или бирж, совмещающих роль маркет-мейкеров, и, следовательно, управляются эмоциями и нарративами. Такие нарративы, как «четырехлетний цикл» или «рождественское проклятие», постоянно муссируются, хотя им не хватает ни строгой логики, ни надежной статистической поддержки.

На рынке широко распространено чрезмерно линейное мышление, например, прямое приписывание колебаний цены BTC таким единичным событиям, как укрепление иены в июле 2024 года, без более глубокого анализа. Подобные нарративы往往 быстро распространяются и оказывают прямое влияние на цену.

Далее мы оставим в стороне краткосрочные нарративы и проанализируем эту проблему с точки зрения независимого мышления.

Временное измерение крайне важно

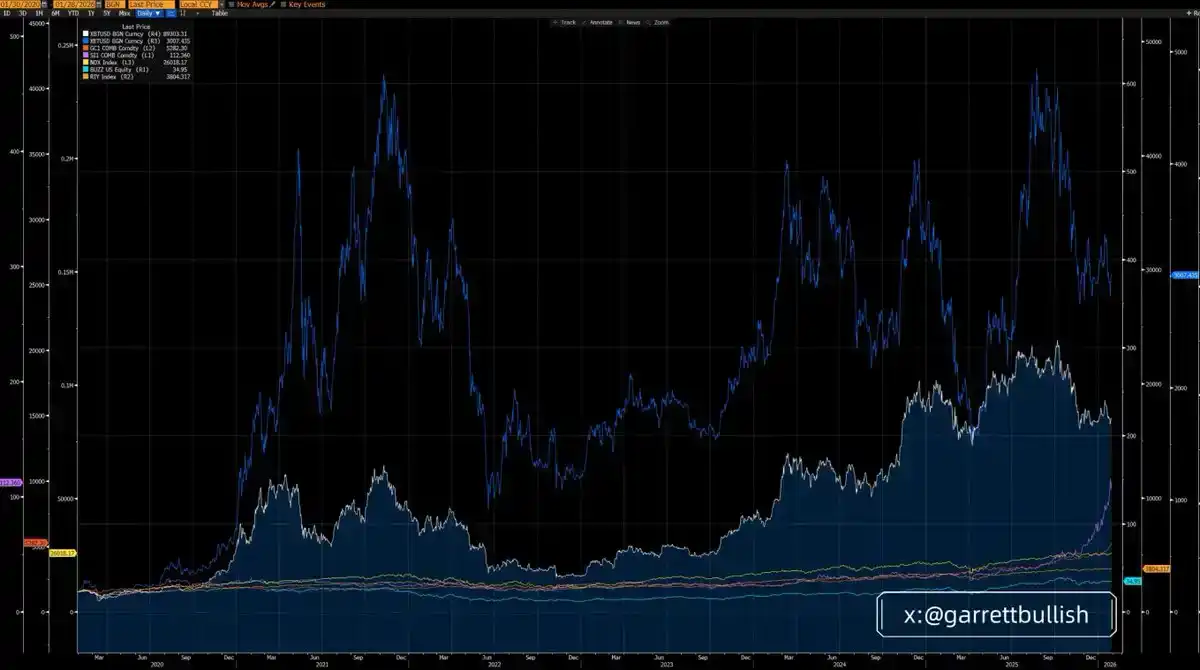

Если рассматривать трехлетний цикл, то BTC и ETH действительно отстают по表現 (производительности) от большинства основных активов, причем ETH показывает наихудшие результаты.

Но если расширить горизонт до шестилетнего цикла (с 12 марта 2020 года), то BTC и ETH явно опережают большинство активов, а ETH, наоборот, становится активом с наилучшими показателями.

Если смотреть с более длительной временной перспективы и в макроэкономическом контексте, текущее так называемое «краткосрочное отставание» по сути является процессом возврата к среднему значению в рамках более длительного исторического цикла.

Игнорирование базовой логики и концентрация только на краткосрочных ценовых колебаниях — одна из самых распространенных и фатальных ошибок в инвестиционном анализе.

Ротация — это нормальное явление

До того как в октябре прошлого года на рынке серебра произошел сqueeз (squeeze, сжатие), серебро также было одним из активов с наихудшими показателями среди рисковых активов; а теперь, в рамках трехлетнего цикла, серебро стало активом с наилучшими показателями.

Это изменение очень похоже на текущую ситуацию с BTC и ETH. Хотя в краткосрочной перспективе они показывают слабые результаты, в шестилетнем цикле они по-прежнему остаются одними из самых выгодных классов активов.

Пока нарратив о BTC как о «цифровом золоте» и инструменте сохранения стоимости не опровергнут фундаментально, пока ETH продолжает интегрироваться с волной ИИ и остается ключевой инфраструктурой в тренде RWA (реальные мировые активы), нет никаких rational оснований полагать, что они будут consistently отставать от других активов в долгосрочной перспективе.

Повторим: игнорирование фундаментальных основ и выводы, основанные solely на краткосрочных ценовых движениях, являются серьезной аналитической ошибкой.

Структура рынка и делеверидж

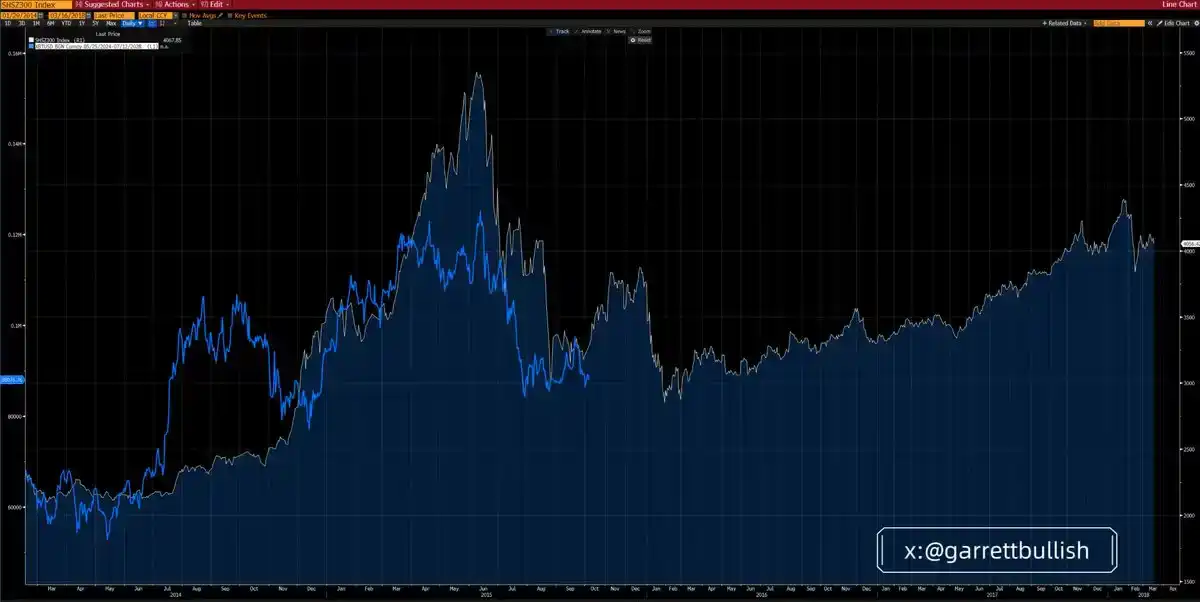

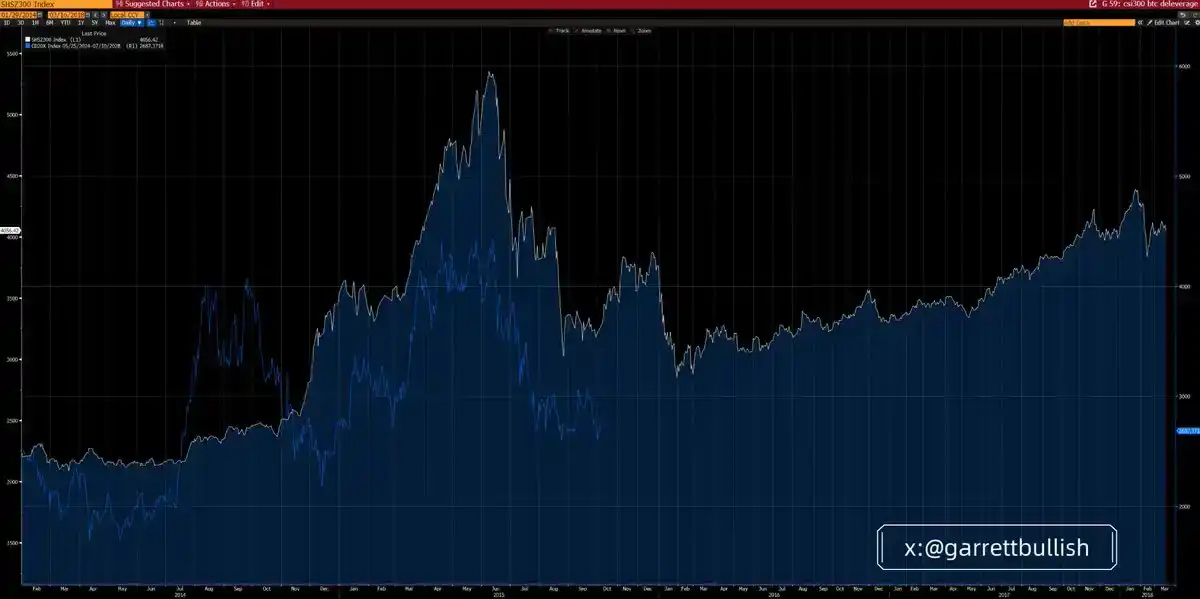

Текущий крипторынок демонстрирует поразительное сходство с ситуацией на китайском фондовом рынке А-shares в 2015 году, когда он вошел в фазу делевериджа после бума, подпитываемого杠杆ом.

В июне 2015 года, после остановки бычьего рынка, движимого杠杆ом, и лопнувшего пузыря оценок, рынок А-shares вошел в трехфазную структуру падения A–B–C по теории волн Эллиотта (Elliott Wave). После достижения дна волны C рынок пережил несколько месяцев консолидации, прежде чем постепенно перейти к бычьему рынку, который длился несколько лет.

Ключевыми драйверами того длительного бычьего рынка были низкие оценки blue-chip активов, улучшение макрополитической среды и значительное смягчение денежных условий.

Биткоин (BTC) и индекс CD20 в этом цикле почти полностью повторили этот путь эволюции «добавление杠杆а — избавление от杠杆а», демонстрируя высокую согласованность как по временному ритму, так и по структурной форме.

Базовое сходство совершенно ясно: обе рыночные среды характеризуются следующими чертами — высокий杠杆, экстремальная волатильность, пики, движимые пузырями оценок и групповым поведением, repeatedly возникающие шоки делевериджа, длительный и медленный процесс падения,持续ное снижение волатильности, а также长期ная структура контанго (contango) на фьючерсных рынках.

На текущем рынке эта структура контанго проявляется в том, что акции связанных с цифровыми активами (DAT) публичных компаний (таких как MSTR, BMNR) торгуются с дисконтом к их mNAV (скорректированной чистой стоимости активов).

В то же время макросреда постепенно улучшается. Регуляторная определенность усиливается, например, продолжается продвижение законодательных инициатив, таких как «Закон о ясности» (Clarity Act); Комиссия по ценным бумагам и биржам США (SEC) и Комиссия по торговле товарными фьючерсами (CFTC) также активно продвигают развитие торговли акциями США на блокчейне (on-chain US equities).

Денежные условия также смягчаются: растут ожидания снижения процентных ставок, количественное ужесточение (QT)接近尾声,持续ное注入 ликвидности на рынке repo, а также ожидания более鸽олистой (dovish) позиции следующего председателя ФРС — все это вместе улучшает общую环境 ликвидности.

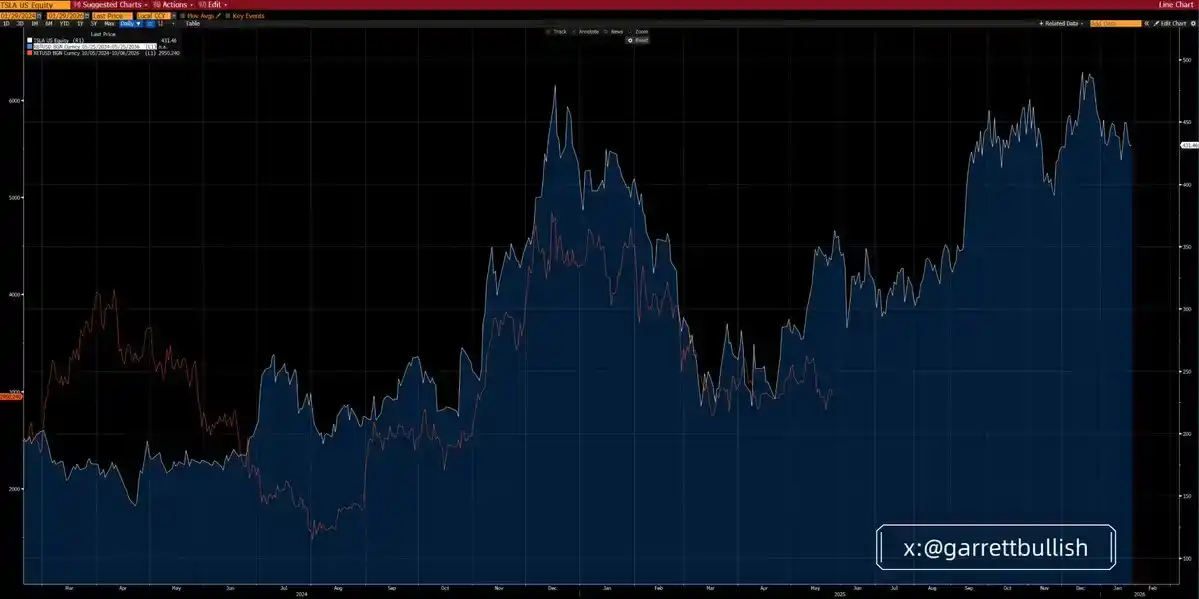

ETH и Tesla: ценная аналогия

Недавнее ценовое движение ETH高度 похоже на поведение акций Tesla (Тесла) в 2024 году.

В то время акции Tesla сначала сформировали структуру перевернутой головы и плеч (head and shoulders bottom), затем последовал отскок, консолидация, повторный рывок вверх, после чего началась длительная фаза формирования вершины, за которой последовало быстрое падение и длительная横向ная консолидация на низких уровнях.

Только в мае 2025 года Tesla finalmente пробила вверх и официально начала новый бычий рынок. Его восходящий импульс в основном был обусловлен ростом продаж на рынке Китая, повышением вероятности избрания Трампа и монетизацией политической сети.

На текущем этапе ETH, как с точки зрения технической формации, так и фундаментального фона,高度 напоминает Tesla того времени.

Базовая логика также сопоставима: оба актива несут в себе как технологический нарратив, так и мем-атрибуты, оба привлекли значительные средства с высоким杠杆ом, пережили резкие колебания, достигли пика на пузыре оценок, подпитываемом групповым поведением, а затем вошли в цикл корректировки с repeatedным делевериджем.

С течением времени волатильность рынка постепенно снижается, в то время как фундаментальные и макроэкономические условия持续но улучшаются.

Судя по объему фьючерсных торгов, рыночная активность BTC и ETH уже接近历史ческих минимумов, что указывает на то, что процесс делевериджа接近尾声.

Являются ли BTC и ETH «рисковыми активами»?

В последнее время на рынке появился довольно странный нарратив: простое определение BTC и ETH как «рисковых активов» для объяснения, почему они не跟随овали росту американских акций, китайских А-shares, драгоценных или промышленных металлов.

По определению, рисковые активы обычно характеризуются высокой волатильностью и высоким бета-коэффициентом. С точки зрения поведенческих финансов или количественной статистики, американские акции, китайские А-shares, промышленные металлы, BTC и ETH соответствуют этому критерию и往往 выигрывают в условиях «risk-on» (склонности к риску).

Но BTC и ETH обладают дополнительными свойствами. Благодаря экосистеме DeFi и механизму расчетов на链е, они в определенных ситуациях также проявляют characteristics, подобные драгоценным металлам, как активы-убежища, особенно при росте геополитического давления.

Наклеивание на BTC и ETH ярлыка «чисто рисковых активов» и утверждение на этом основании, что они не могут выиграть от макроэкспансии, по сути, является нарративом, избирательно强调ющим негативные факторы.

Часто приводимые примеры включают:

Потенциальный таможенный конфликт между ЕС и США из-за проблемы Гренландии

Таможенный спор между Канадой и США

А также возможный военный конфликт между США и Ираном

Такой способ аргументации по своей сути является «выборочным подбором нарративов» (cherry-picking) и двойными стандартами.

Теоретически, если бы эти риски действительно были системными, то все рисковые активы, за исключением, возможно, промышленных металлов, которые могут выиграть от военного спроса, должны были бы同步но упасть. Но реальность такова, что эти риски не имеют основы для эскалации в серьезный системный шок.

Спрос, связанный с ИИ и высокими технологиями, остается чрезвычайно сильным и в значительной степени не подвержен геополитическому шуму, особенно в ключевых экономиках, таких как Китай и США. Поэтому фондовый рынок не закладывает эти риски в цены по существу.

Что еще более важно, большинство этих опасений были понижены в статусе или опровергнуты фактами. Это также поднимает ключевой вопрос: почему BTC и ETH异常но чувствительны к негативным нарративам, но медленно реагируют на позитивные developments или消退ение негативных факторов?

Реальная причина

Мы считаем, что причина в основном кроется в структурных проблемах самого крипторынка. Текущий рынок находится на заключительной стадии цикла делевериджа, общие настроения участников склонны к сжатию, и они高度 чувствительны к downside рискам.

Крипторынок по-прежнему ориентирован на розничных инвесторов, участие профессиональных институтов ограничено. Потоки ETF в большей степени отражают пассивное следование настроениям, а не активное распределение, основанное на фундаментальных показателях и суждениях.

Точно так же большинство DAT (хранилищ цифровых активов) также используют пассивные методы накопления — будь то прямые операции или через сторонних пассивных управляющих фондами, обычно с использованием неагрессивных алгоритмических торговых стратегий, таких как VWAP, TWAP, с основной целью снижения внутридневной волатильности.

Это резко контрастирует со спекулятивными фондами. Основная цель последних как раз и заключается в создании внутридневной волатильности — и на текущем этапе эта волатильность чаще проявляется в сторону снижения, для манипулирования ценовым поведением.

В то же время трейдеры-ритейлеры普遍но используют杠杆 в 10–20 раз. Это побуждает биржи, маркет-мейкеров или спекулятивные фонды больше склоняться к использованию микроструктуры рынка для получения прибыли, а не к承受нию среднесрочных и долгосрочных ценовых колебаний.

Мы часто наблюдаем集中ные продажи в периоды низкой ликвидности, особенно когда азиатские или американские инвесторы спят, например, с 00:00 до 08:00 по азиатскому времени. Подобные колебания往往 вызывают каскадный эффект, включающий принудительное закрытие (ликвидацию), маржин-коллы и пассивные продажи, further усиливающие幅度 падения.

При отсутствии существенного притока новых средств или возвращения настроений FOMO,仅依靠现有存量资本лов недостаточно, чтобы противостоять上述类型的 рыночному поведению.

Определение рискового актива

Рисковые активы (Risk Assets) — это финансовые инструменты, обладающие определенными risk characteristics, включая акции, товары, высокодоходные облигации, недвижимость, а также валюты.

В широком смысле, рисковый актив — это любая финансовая ценная бумага или инвестиционный инструмент, который не считается «безрисковым». Общей чертой таких активов является то, что их цена волатильна и стоимость может significantly меняться с течением времени.

Распространенные типы рисковых активов включают:

Акции (Equities / Stocks):

Доли в публичных компаниях, цена на которые влияет множество факторов, включая рыночную конъюнктуру, операционные показатели компании и т.д., амплитуда колебаний может быть значительной.

Товары (Commodities):

如 нефть, золото, сельскохозяйственная продукция等 материальные активы, цена в основном зависит от изменений спроса и предложения.

Высокодоходные облигации (High-Yield Bonds):

Облигации, предлагающие более высокую процентную ставку из-за низкого кредитного рейтинга, но также сопровождающиеся более высоким риском дефолта.

Недвижимость (Real Estate):

Инвестиции в недвижимость, стоимость которой колеблется в зависимости от рыночного цикла, экономической环境 и изменений политики.

Валюты (Currencies):

Различные валюты на外汇ном рынке, цена которых может быстро колебаться из-за геополитических событий, макроэкономических данных и изменений политики.

Основные characteristics рисковых активов

Волатильность (Volatility)

Цены рисковых активов часто колеблются, что может приносить как прибыль, так и убытки.

Сосуществование доходности и риска (Investment Returns)

Как правило, чем выше риск актива, тем выше потенциальная доходность, но при этом также выше вероятность убытков.

Высокая чувствительность к рыночной environment (Market Sensitivity)

Стоимость рисковых активов зависит от множества факторов, включая изменения процентных ставок, макроэкономической ситуации, а также настроений инвесторов.