В Корее этим месяцем, если вы не сотрудник SK Hynix и у вас нет акций SK Hynix, вы, скорее всего, «несчастный человек».

Как только квартальный отчет показал колоссальную прибыль, инвестиционные банки, никогда не упускающие случая позлословить, не только активно пересмотрели в сторону повышения прогнозы прибыли Hynix на этот год, но и подогрели ожидания сотрудников Hynix в отношении годовых бонусов. Используя правило распределения 10% от операционной прибыли в фонд премирования, они подсчитали, что в этом году на человека придутся годовые дивиденды в несколько миллионов юаней, одновременно поставив капиталистов из соседнего Samsung в неловкое положение.

После этого все, что связано с IP Hynix, получило безумный ажиотаж.

Рабочая форма Hynix стала приоритетным пропуском на корейском рынке знакомств; риелторы в Ичхоне, где расположена штаб-квартира, пережили фантастический квартал, цены на жилье и объемы сделок выросли во многих районах вдоль маршрутов корпоративных автобусов Hynix; даже корейско-китайские полупроводниковые ETF, лишь косвенно связанные с компанией, были раскачаны до премии в 30%, регулярно сталкиваясь с приостановкой торгов.

Даже фондовый рынок Гонконга, который всегда критиковали за недостаток технологичности, немного оживился.

По состоянию на 13 мая 2026 года, активы ETF с двойным кредитным плечом на SK Hynix (07709.HK), торгуемого на Гонконгской бирже (далее — ETF 2x лонг на Hynix), приблизились к 600 млрд гонконгских долларов, превзойдя долго лидировавший на рынке США ETF с двойным плечом на Tesla (TSLL.NASDAQ) и заняв первое место в мире по размеру среди продуктов с кредитным плечом на отдельные акции.

Неважно, насколько нишевым является инвестиционный инструмент, когда рост доходит до таких масштабов, достаточно просто выйти в интернет, даже если вы просто читаете обновления технологических блогеров, чтобы в комментариях то и дело натыкаться на эмоциональные сообщения от неравнодушных пользователей — «Почему бы тебе не купить 2x лонг на Hynix?».

Смертельное плечо

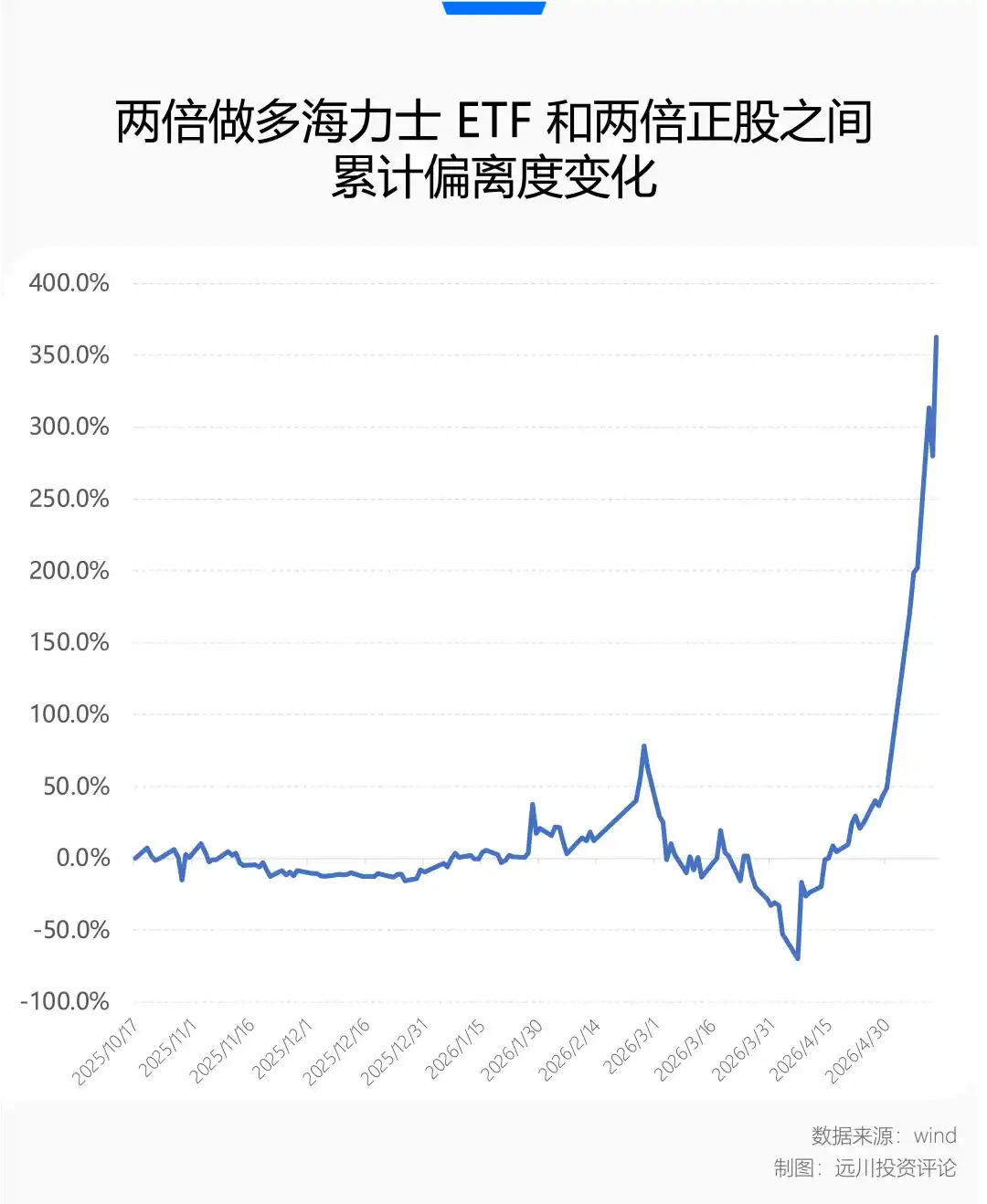

Когда ETF 2x лонг на Hynix впервые был размещен на Гонконгской бирже 16 октября 2025 года, его объем размещения составлял менее 50 млрд гонконгских долларов. Если взять цену закрытия на 13 мая 2026 года, то за 7 месяцев стоимость чистых активов этого продукта с кредитным плечом выросла на 1011,58%, а его размер увеличился более чем в 13 раз.

Акции Yunji Technology, которые были размещены в тот же день в Гонконге и позиционировались как «первые акции робота для отелей», даже при довольно крутом росте, увеличили свою капитализацию менее чем в 4 раза по сравнению с моментом IPO.

Если вы думаете, что это пугающая эффективность двойного плеча, то обыкновенные акции SK Hynix на корейском рынке с 17 октября прошлого года по 13 мая этого года выросли «всего» на 324,49%. Благодаря поддержке одностороннего ралли, отклонение этого ETF с кредитным плечом от теоретической двойной доходности составило дополнительные 362% сверхдоходности. Перед лицом такого агрессивного обогащения, кажется, более уместно называть его «тройным плечом».

Однако, если взглянуть на последние 7 месяцев в целом, эта бумажная сверхдоходность временна.

Всего два месяца назад Ормузский пролив оказался в состоянии квантовой суперпозиции — блокирован и не блокирован одновременно, мировые рынки погрузились в панику из-за внезапного перебоя поставок нефти и газа. В условиях колебаний и быстро меняющейся ситуации рынок не испытал традиционного одностороннего падения, а в этой нетипичной геополитической конфронтации сошел с ума.

Днем еще торговали логикой ухода от рисков «началась Третья мировая, разорваны цепочки поставок», а ночью из-за двусмысленных заявлений пресс-секретаря Белого дома могли быстро переключиться на «снижение напряженности, возврат к технологической теме» и ралли шорт-сквиза. Неопределенность пути развития, усиленная быстрым распространением в соцсетях, передавалась на рынки капитала в виде резких продаж технологических акций или безумных покупок на коррекциях.

Хотя здравый смысл подсказывает, что война в конечном итоге закончится, а ежедневное потребление токенов в мире AI-индустрии продолжает ускоряться, когда волатильность рынка становится слишком высокой, нельзя полностью игнорировать извилистость процесса.

Именно в этот период больше людей почувствовали на себе эффект потерь от волатильности этого продукта ETF с кредитным плечом.

Судя по реальным торговым данным с марта по апрель 2026 года, за этот период акции Hynix снижались на фоне сильных колебаний. Падение само по себе проблема, но множественные резкие отскоки более чем на 10% стали настоящим катализатором убытков.

Для ETF 2x лонг на Hynix, который ежедневно ребалансирует позиции, одностороннее падение, возможно, еще можно пережить, но нисходящий тренд с высокой волатильностью — настоящая мясорубка. В самые трудные моменты он падал более чем на 50% сильнее, чем удвоенное падение базового актива.

Если не учитывать другие торговые издержки и комиссию за управление, механизм ежедневной ребалансировки, заложенный в конструкцию продукта, означает, что на одностороннем растущем рынке вчерашняя прибыль автоматически становится сегодняшним «основным капиталом», на который снова накладывается двойное плечо, принося дополнительную положительную сверхдоходность. И наоборот, при одностороннем обвале, поскольку ежедневная база для расчета уменьшается, фактические убытки будут меньше теоретических в два раза.

Однако, как только рынок входит в фазу «чередования роста и падения» (боковик), ETF с кредитным плечом показывает свою истинную сущность.

ETF 2x лонг на Hynix неоднократно переживал «двойной удар» — после сильного роста вчера и перебалансировки, сегодняшнее резкое падение вычитало больше стоимости, затем снова перебалансировка, а завтрашний отскок снова наносил удар из-за уменьшенной базы.

Чередование роста и падения, вызывающее постоянное трение, приводит к тому, что фактическая просадка стоимости чистых активов продукта значительно превышает двукратное падение базового актива, создавая заметные негативные потери от волатильности, разъедающие капитал инвесторов.

Просто сейчас рынок снова вернулся к теме AI, горячие деньги вновь хлынули потоком, принеся всеобщую радость одностороннего ралли.

Когда капитализация Hynix неоднократно обновляет максимумы, когда продукт с кредитным плечом объемом в сотни миллиардов вызывает ажиотажную активность, рынок неизбежно возвращается к вопросу, который повторяется изо дня в день: в этой технологической революции циклов действительно не существует?

Кремниевые циклические акции

Нельзя не признать, что с точки зрения времени размещения, ETF 2x лонг на Hynix получил максимум возможных преимуществ — удачное стечение обстоятельств и благоприятную конъюнктуру.

До этого довольно долгое время память не была абсолютным фокусом для игры на повышение на AI-тематике на вторичном рынке. Ведь память с 90-х годов, когда человечество село на скоростной поезд информационной эпохи, часто становилась тем местом, где после бурного роста оставались горы трупов, ужас цикличности здесь всегда перевешивал мечты о росте.

Микросхемы памяти (особенно традиционные DRAM и NAND) — это крайне стандартизированный биржевой товар. Память от разных производителей, за исключением наклеенного логотипа, практически не отличается по физическим характеристикам, их можно назвать свининой в мире кремния. Вся отрасль долгое время находилась в жестоком циклическом круговороте:

Дефицит → рост цен → безумное расширение производства гигантами → перепроизводство → обвал цен → убытки и сокращение производства → снова дефицит.

Каждый подъем на фоне сверхоптимистичных ожиданий окрещивают «суперциклом». Каждое падение сопровождается жестокой ценовой войной и убытками в десятки миллиардов, оставляя за собой груды костей.

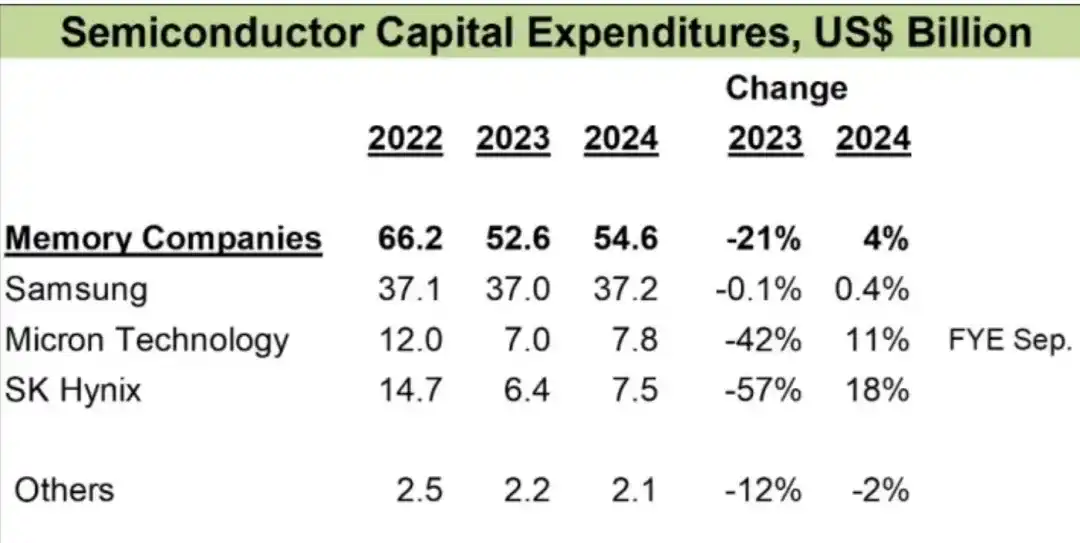

Пережив самую жестокую за всю историю зиму на рынке полупроводников с 2022 по 2023 год, выжившая тройка олигополистов памяти — Micron, Samsung, Hynix — молчаливо сократили капитальные расходы, отказавшись от злонамеренного расширения производства по принципу «потерять тысячу, чтобы нанести ущерб в восемьсот».

Источник изображения: IC Insights

И тут появился нарратив AI, снова начались дефицит и рост цен, по сути установив всем печатный станок.

Особенно с прошлого года, когда фокус конкуренции в AI-индустрии сместился с «обучения» на «инференс», потребность в инфраструктуре сместилась с «вычислительной мощности» на «емкость памяти», а узкое место предложения переместилось с пропускной способности на объем, всеобщий дефицит памяти стал самым горячим торговым нарративом.

На данный момент, если кто-то еще скажет: «А разве не говорили, что предел AI — это электроэнергия?», то, скорее всего, он просто не успел войти в позицию.

После третьего квартала 2025 года новости из AI-индустрии почти все были о дефиците чипов памяти: то гиганты объявляют, что заказы на HBM расписаны до 2027 года и позже; то уведомляют клиентов, что DDR5 тоже начинает не хватать, поэтому, извините, но теперь у нас, независимо от сегмента — высокого или низкого, действует политика повсеместного повышения цен.

Hynix, будучи основным поставщиком HBM для Nvidia, получила огромное преимущество первопроходца и долю рынка. Родившийся в нужное время ETF 2x лонг на Hynix практически сразу после размещения попал в золотые времена, когда цена за грамм модулей памяти поднялась выше золота, а одна коробка могла обменяться на квартиру в Шанхае.

Так значит, запрыгнув в скоростной поезд AI, можно избежать гравитации циклов? Важно не делать сейчас окончательных выводов, а искать, где могут произойти изменения.

Hynix, благодаря барьеру в виде выхода годных HBM, сформировала доминирующее положение. В первом квартале 2026 года валовая маржа SK Hynix достигла исторического пика около 79%, даже превысив прибыльность Nvidia в тот же период.

Человеческая природа подсказывает, что предельная сверхприбыль обязательно привлечет лавинообразное желание расширять производство. Молчаливая договоренность между гигантами памяти, достигнутая, казалось бы, благодаря «сокращению производства», не заслуживает доверия перед лицом абсолютной сверхприбыли.

Таким образом, вопрос о том, сможет ли Samsung или Micron в какой-то момент в будущем добиться прорыва в выходе годных, что поставит под сомнение нарратив о дефицитности HBM, и увеличение расхождений между быками и медведями вызовет волатильность в секторе, является переменной, требующей постоянного отслеживания.

Кроме изменений на стороне предложения, споры на стороне спроса также не полностью рассеялись, несмотря на ускорение распространения Agent'ов и увеличение потребления токенов.

В конечном счете, безумие Hynix основано на безумии Nvidia; а безумие Nvidia основано на ежегодных AI-капитальных затратах downstream-гигантов в сотни миллиардов долларов.

Предельные изменения в капитальных затратах (Capex) по-прежнему остаются главной причиной всей тревоги и гордости, связанной с AI, на вторичном рынке.

Заключение

Будете вы покупать ETF 2x лонг на Hynix или нет, он станет тонкой заметкой на полях истории, оглядываясь на этот период.

В нашу эпоху быки и медведи часто говорят о двух разных вещах: быки — о вере в AI-индустрию, медведи — о макроэкономических и геополитических рисках.

Люди всегда привычно открывают учебники истории, пытаясь найти аналогии в интернет-буме рубежа тысячелетий или более ранних макроэкономических потрясениях. Но способ развития каждой технологической революции различен, а на этот раз «инаковость» заключается в следующем: скорость颠覆отности промышленной революции беспрецедентна.

AI с невиданной ранее скоростью перестраивает глобальные производительные силы и производственные отношения. Эта экстремальная «скорость» ломает долгий процесс проникновения и созревания в традиционных технологических циклах. Она не оставляет рынку много времени на постепенное переваривание оценок и не дает «старичкам» немного внимания от разлившейся ликвидности для небольшой ротации.

И промышленные гиганты, и деньги на вторичном рынке вынуждены в крайне сжатые сроки определяться с позицией и оценкой. Поэтому рост акций измеряется в кратности; поэтому опытные специалисты в области AI уже по умолчанию считают, что в нашу эпоху шесть месяцев — это уже долгосрочная перспектива.

Однако буря над Ормузским проливом снова поставила эту технологическую революцию в общий контекст всех прошлых технологических циклов: отрасль определяет конечный результат и доходность, а макроэкономика влияет на путь и волатильность — причиной огромного негативного отклонения ETF 2x лонг на Hynix стала не остановка процесса AI, а крайняя неопределенность глобальных макроэкономических ожиданий в течение того месяца.

А уязвимые места реального мира не ограничиваются лишь 33 километрами в самом узком месте Ормузского пролива.