Автор: David, Deep Chao TechFlow

Оригинальное название: На этой неделе все помогают ИИ открыть банковский счет

18 марта еще один блокчейн запустил мейннет.

Он называется Tempo, за ним стоят Stripe и Paradigm. Stripe — одна из крупнейших в мире компаний по онлайн-платежам, в прошлом году обработавшая транзакции на 1,9 триллиона долларов; Paradigm — один из крупнейших венчурных фондов в криптоиндустрии. В прошлом году они совместно инвестировали в Tempo 5 миллиардов долларов, оценка проекта:

50 миллиардов.

Блокчейн стоимостью 50 миллиардов долларов, который не торгует криптовалютой, не занимается DeFi, не выпускает мемы. В день запуска мейннета Tempo громко анонсировал продукт:

Позволить машинам платить машинам.

Звучит абстрактно, но можно понять так: теперь ИИ за каждый шаг платит деньги. За вызов API — деньги, за вычислительную мощность — деньги, за выгрузку данных из базы — тоже деньги...

Но существующие платежные системы созданы для людей: банковский счет требует паспорта, кредитная карта — идентификации по лицу, Alipay — кода из SMS.

ИИ не пройдет ни одну из них.

Он может выполнить весь рабочий процесс, но на этапе оплаты должен остановиться и ждать, пока человек нажмет «Подтвердить».

Поэтому вместе с мейннетом запустили открытый протокол MPP (Machine Payments Protocol), написанный совместно со Stripe.

Проще говоря, это набор правил для транзакций между машинами, включая запрос платежа, авторизацию, расчеты и т.д.

Предполагается, что ИИ сможет самостоятельно тратить деньги в пределах установленного лимита, без необходимости получать одобрение человека на каждую транзакцию. В день запуска уже подключились более 100 поставщиков услуг, включая OpenAI, Anthropic и Shopify.

Но Tempo — не единственный, кто занимается этим на этой неделе.

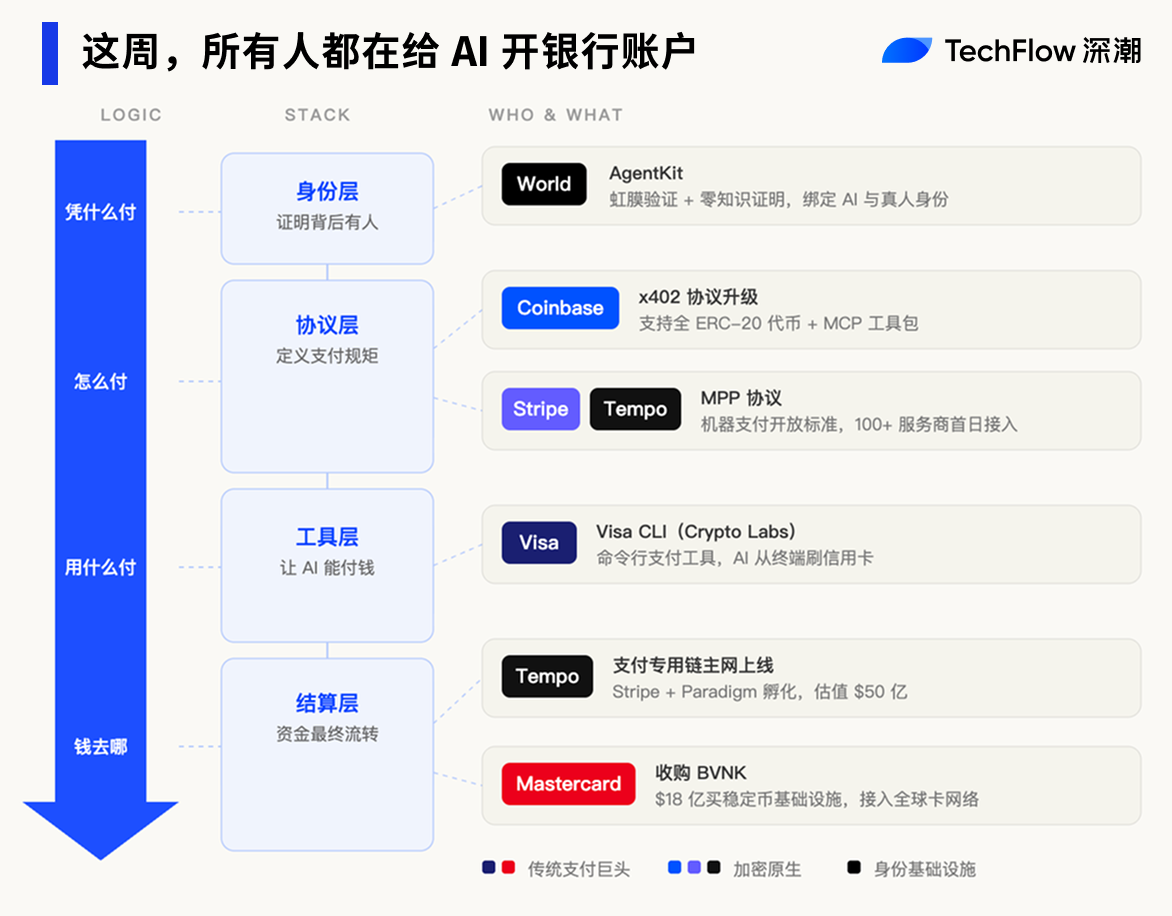

За пять дней Visa создала новое подразделение и выпустила инструмент для платежей ИИ, платежный протокол Coinbase получил крупное обновление, Mastercard потратил 1,8 миллиарда долларов на покупку компании-эмитента стейблкоинов, а World Сэма Олтмана выпустил инструментарий для аутентификации ИИ.

Пять гигантов за неделю ворвались в одну дверь, торопясь открыть банковские счета для ИИ.

Два пути, одна дверь

Tempo занимается расчетами для ИИ. Но расчеты — лишь часть платежной системы. Чтобы AI Agent мог действительно самостоятельно тратить деньги, ему нужны платежные инструменты, каналы для движения средств и аутентификация.

Здесь и традиционные платежные компании, и криптокомпании пытаются отхватить кусок пирога своими методами.

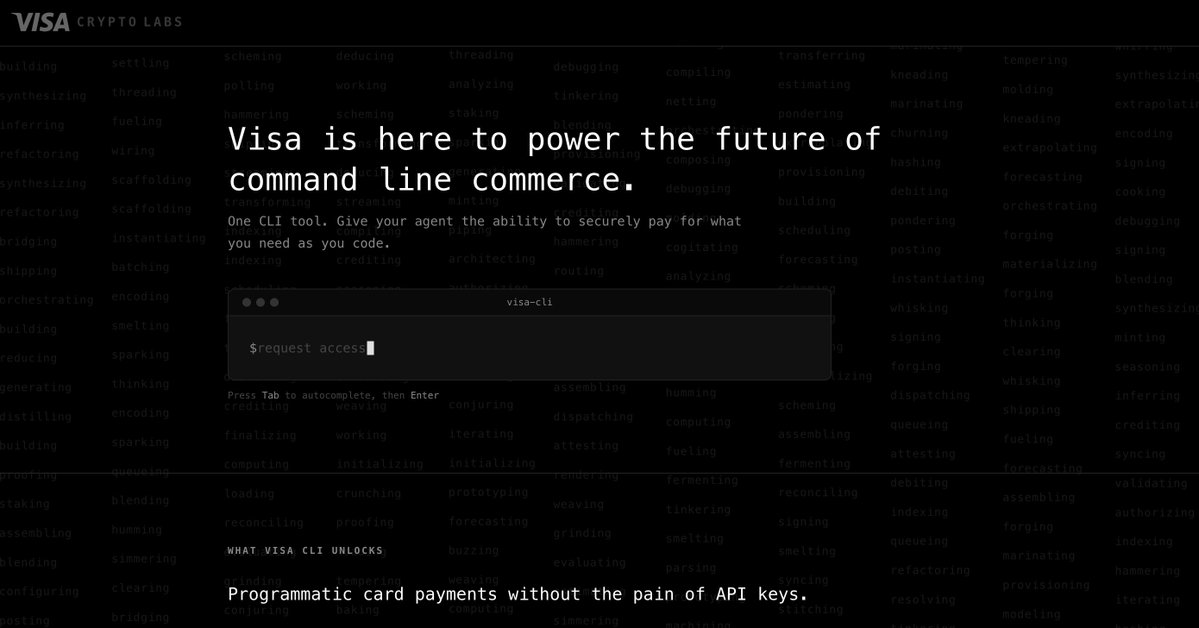

18 марта, в день запуска мейннета Tempo, гигант платежей Visa тоже сделал ход. Новое подразделение Crypto Labs выпустило первый продукт: Visa CLI, инструмент, позволяющий AI Agent напрямую из терминала инициировать платеж по кредитной карте.

Без API-ключей, без предварительной регистрации. Если ИИ в процессе выполнения задачи needs купить какую-то услугу, достаточно ввести одну команду для оплаты. Visa называет это «командным коммерсом».

Глобальная карточная сеть Visa подключена к миллиардам карт и миллионам merchants. Если платежи ИИ пойдут по этой готовой сети, им не нужно ждать созревания какой-либо новой инфраструктуры.

Visa продлевает старый путь. Ее конкурент Mastercard выбрал другой способ: просто купить дорогу.

17 марта Mastercard объявил о покупке лондонской компании BVNK, занимающейся инфраструктурой стейблкоинов, за 1,8 миллиарда долларов. Это крупнейшая сделка по покупке стейблкоин-компании в истории криптоиндустрии.

Цель этой покупки проста: если деньги для платежей ИИ пойдут в стейблкоинах, то пусть стейблкоины идут через мой管道.

Со стороны нативных криптокомпаний активность также высока.

Протокол x402 от Coinbase получил крупное обновление, расширив диапазон платежей с нескольких стейблкоинов на все токены ERC-20, одновременно выпустив инструментарий MCP, позволяющий разработчикам одним щелчком подключить инструменты ИИ к платежной сети.

Кажется, что стороны исходят из разного, но их действия направлены в одну сторону: традиционные платежные компании embrace крипто, криптокомпании embrace ИИ. В итоге криптоинфраструктура становится底层管道 для платежей ИИ.

Остался один элемент. ИИ может тратить деньги, но как продавец узнает, стоит ли за этим ИИ ответственный человек?

17 марта World, соучредителем которой является Сэм Олтман, выпустила AgentKit, подключенный к x402 от Coinbase. Он делает только одно: позволяет ИИ при оплате доказать, что за ним стоит верифицированный реальный человек. Продавец может подтвердить, что за транзакцию кто-то отвечает, но не видит, кто это.

Пять дней, пять компаний, расчеты, каналы, инструменты, протоколы, идентичность — каждый элемент занят.

Пирог ИИ поделен, осталась только касса

За последние три года все возможные места в цепочке создания стоимости ИИ в основном заняты.

На уровне моделей за столом сидят OpenAI, Anthropic, Google и ряд китайских компаний, вычислительные мощности надежно заблокированы NVIDIA, на уровне приложений от помощников по программированию до поисковых систем бушует красный океан...

Каждый уровень переполнен людьми, конкурентные барьеры на каждом уровне становятся все выше.

Но уровень платежей остается относительно пустым.

Не то чтобы никто не думал об этом, просто время не пришло. Для платежей AI Agent есть precondition: ИИ должен сначала иметь возможность самостоятельно выполнять целую цепочку задач. Если он может только болтать, не needs вызывать API, покупать вычислительную мощность, нанимать других Agent'ов для работы, то платежи не являются жесткой потребностью.

За последний год это precondition начало slowly выполняться.

OpenClaw позволяет ИИ напрямую操作 компьютер, протокол MCP позволяет ИИ подключаться к внешним сервисам, Agent-способности крупных моделей集中突破 во второй половине 2025 года. ИИ из «инструмента для диалога» превратился в «инструмент для работы», а работа требует денег...

Потребность тратить деньги пришла, но инфраструктура для трат еще не существует.

Вот почему Stripe, Visa, Mastercard, Coinbase одновременно сделали ход. Для традиционных платежных компаний это первое преимущество主场 во всей волне ИИ. Модели они делать не могут, чипы производить не могут, но платежи — это то, чем они занимаются几十年.

Глобальная карточная сеть Visa подключена к миллиардам карт и миллионам merchants, Mastercard покрывает более 200 стран, Stripe в прошлом году обработала транзакции на 1,9 триллиона долларов. Если каждый расход ИИ пойдет через эти管道, то чем способнее ИИ, тем больше они зарабатывают.

Для криптокомпаний логика несколько иная.

Генеральный директор Coinbase Брайан Армстронг ранее сказал очень прямолинейно: «ИИ может иметь криптокошелек, но не может открыть банковский счет».

Каждый шаг традиционной финансовой системы подтверждает «Кто ты»: для открытия банковского счета нужен паспорт, для получения кредитной карты — идентификация по лицу, для каждой транзакции — код из SMS. ИИ — это программное обеспечение, не человек, ни один из этих关卡 он пройти не может.

Но криптокошельки этого не требуют. Один приватный ключ — это один аккаунт. Для AI Agent ончейн-платежи — это путь наименьшего сопротивления.

Вне зависимости от крипто, платежи ИИ станут новым инфраструктурным рынком. Разница лишь в том, чей管道 больше подходит для машин.

Дорогу построили, машин нет

На этом месте история, кажется, полностью готова, пять гигантов заняли свои positions.

Но есть одна цифра, на которую стоит взглянуть.

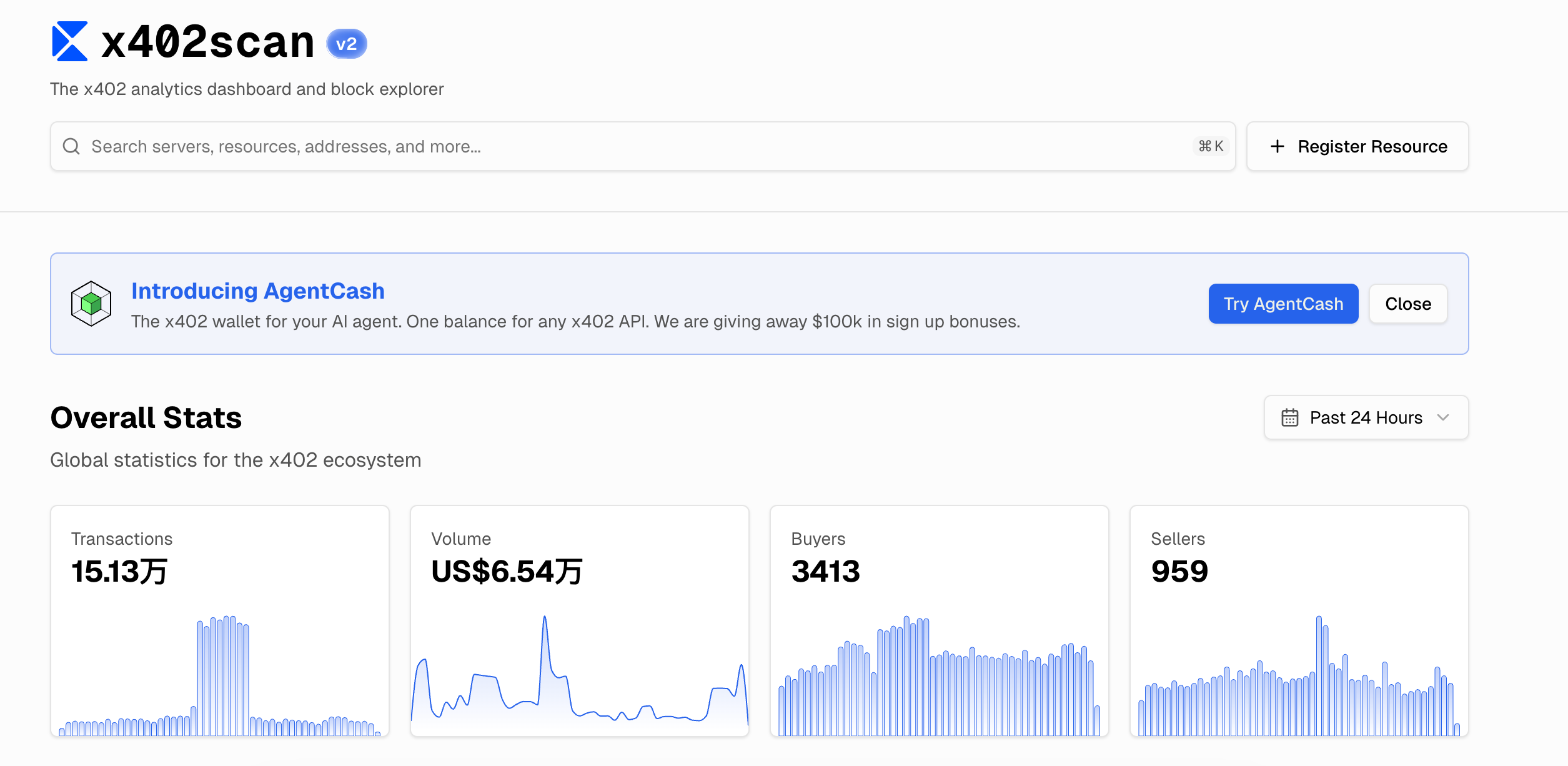

Протокол x402 от Coinbase — это currently самая ранняя и самая широкая по экосистеме платежная система для ИИ. Согласно данным x402scan, за последние 24 часа общий объем транзакций в экосистеме составил 65,4 тысячи долларов. 150 тысяч транзакций, в среднем less 50 центов за транзакцию.

Какой инфраструктуре配 этот数字? Оценка Tempo — 50 миллиардов долларов, Mastercard потратил 1,8 миллиарда на покупку BVNK, Visa专门 создала новое подразделение, Stripe лично下场 написала протокол.

Инфраструктура с оценкой в миллиарды обслуживает рынок с дневным объемом транзакций, comparable с придорожным магазином bubble tea.

Кажется, весь инфраструктурный бизнес таков вначале.

Накануне пузыря доткомов в 2000 году телекоммуникационные компании проложили миллионы километров оптоволокна по дну океана. После прокладки выяснилось, что глобальный интернет-трафик использует only 5% из них. Большинство тех компаний обанкротились, но волокно осталось.

Десять лет спустя视频流媒体 и мобильный интернет заполнили те管道. Те, кто прокладывал дорогу, не заработали денег, но дорога была настоящей.

Платежи ИИ сейчас находятся на этой стадии. Логика спроса обоснована: AI Agent действительно становятся все более способными, действительно need autonomously тратить деньги, действительно need новую финансовую инфраструктуру.

Все вышли на стартовую линию, но после выстрела стартового пистолета обнаружили, что на дорожке пока только они сами.

Что касается того, чья дорога в конечном итоге выиграет, и когда первая настоящая автономная транзакция AI Agent произойдет в вашей жизни, это может случиться быстрее, чем все ожидают, или медленнее, чем все ожидают.

Единственное, что可以肯定, это то, что битва уже началась, а наши с вами кошельки, возможно, узнают об этом последними.