Автор: Сяобин, Shenchao TechFlow

22 мая, после того как Комиссия по ценным бумагам Китая предложила ввести строгие санкции против трех зарубежных брокерских компаний, включая Futu, Tiger и Longbridge, их акции резко упали.

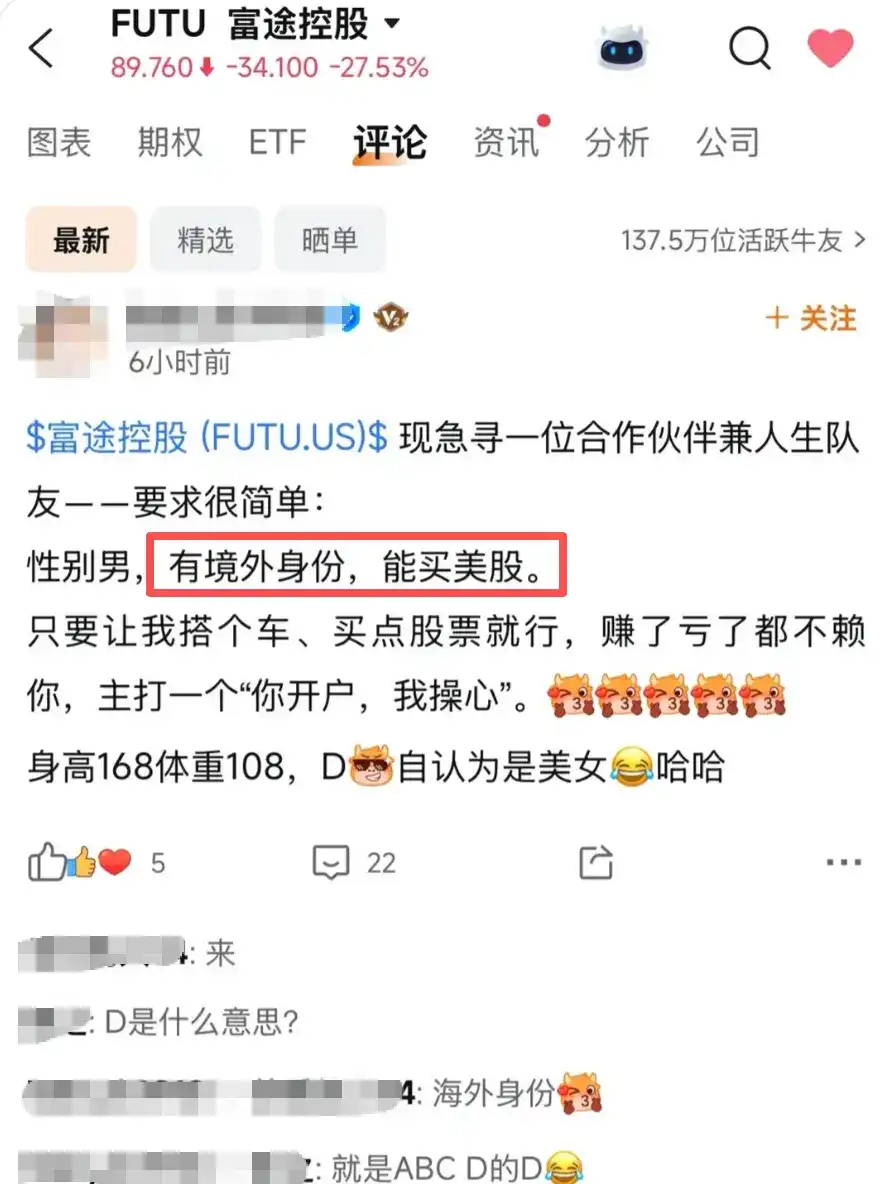

Однако в сообществе приложения Futu произошел неожиданный поворот: здесь не только обсуждают акции, но и буквально за одну ночь платформа превратилась в место для знакомств инвесторов.

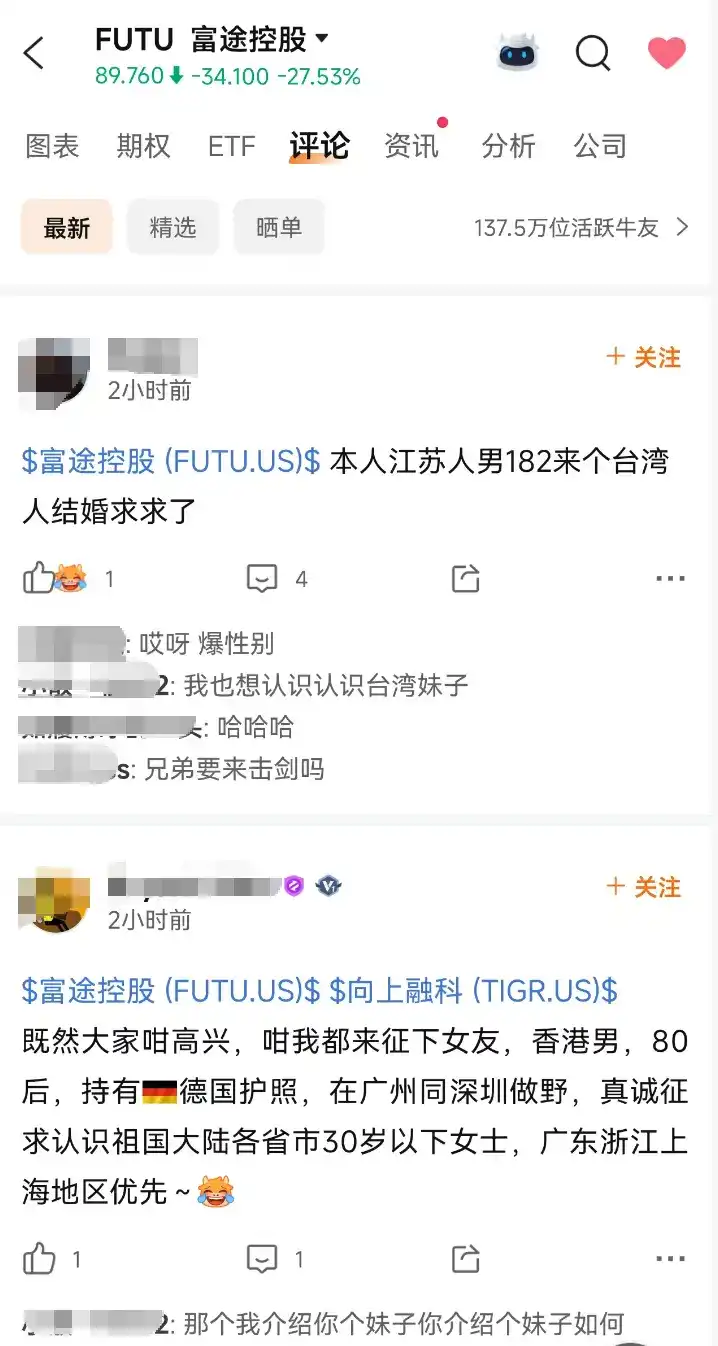

Девушка из материкового Китая, представляющаяся красавицей с размером груди D, ищет мужчину за границей; материковый китаец 90-х годов рождения с доходностью 2046% готов рассмотреть вариант «независимо от пола» в обмен на гражданство; мужчина из Гонконга с немецким паспортом проводит обратный отбор, предпочитая «из Гуандуна, Чжэцзяна и Шанхая»...

Это не просто анекдот, вы наблюдаете за формированием скрытого рынка секьюритизации брачных отношений в реальном времени в сообществе Futu. Сторона спроса, сторона предложения, ценовые предпочтения, географические условия фильтрации... Все формируется спонтанно, это самая честная утечка естественного языка, отражающая настроения группы инвесторов среднего класса Китая в 2026 году.

Регуляторный удар

22 мая Комиссия по ценным бумагам Китая совместно с восемью другими ведомствами выпустила «План комплексного регулирования незаконной трансграничной деятельности с ценными бумагами, фьючерсами и фондами». В тот же день было объявлено о планах ввести строгие санкции против трех зарубежных брокерских компаний: Futu Holdings планируется оштрафовать примерно на 1,85 млрд юаней; Tiger Securities — на 411,2 млн юаней; Longbridge также попал в список. Акции Futu и Tiger упали более чем на 30% в предторговых сделках на американском рынке.

Брокеры ответили сдержанно. Futu заявила, что по состоянию на конец первого квартала 2026 года на клиентов из материкового Китая приходилось около 13% от общего числа пополненных счетов компании; Tiger сообщила, что активы клиентов из материкового Китая составляют около 10% от общих глобальных активов группы. Обе подчеркнули, что «бизнес-операции во всех регионах за пределами материкового Китая продолжаются в нормальном режиме».

Однако для материковых пользователей, у которых уже есть счета в Futu и Tiger с акциями американских компаний, реально болезненной информацией стала лишь одна фраза:

Можно только продавать, нельзя покупать.

Это означает, что в ближайшее время, если вы захотите открыть новый счет для покупки акций Nvidia, Tesla или ETF S&P 500, вам сначала необходимо предоставить документ, подтверждающий статус нерезидента материкового Китая.

Оглядываясь на последние три года, порог открытия счетов для материковых пользователей зарубежными брокерами постепенно повышался:

- В конце 2022 года Комиссия по ценным бумагам впервые назвала их имена;

- В мае 2023 года приложения были удалены из магазинов приложений материкового Китая;

- С 2024 года они принимают только материковых резидентов, «фактически работающих или проживающих за границей», требуя предоставить счета за коммунальные услуги, кредитные карты, налоговые накладные и т.д.;

- В сентябре 2025 года порог был повышен до «документа, подтверждающего право на постоянное проживание за границей»;

- В конце 2025 года они принимают только «документы, удостоверяющие личность, выданные не в материковом Китае»;

- В мае 2026 года были наложены штрафы непосредственно на самих брокеров.

Порог открытия счета от счета за коммунальные услуги постепенно поднялся до заграничного паспорта или карты постоянного жителя. Обратная сторона этой кривой — это процесс, в котором статус постоянно переоценивается на инвестиционном рынке.

Зарубежное гражданство — новая твердая валюта среднего класса

Для среднего класса материкового Китая в 2026 году зарубежное гражданство стало скрытым классом активов. Оно не продается и не покупается, как недвижимость, и не имеет публичной котировки, как акции, но обладает всеми основными свойствами «твердой валюты».

Во-первых, дефицитность. Примерно 140 тысяч человек получили одобрение по программе привлечения талантов в Гонконге в 2024 году, подавляющее большинство из них — из материкового Китая. Звучит много, но при населении в 1,4 миллиарда человек проникновение составляет менее одной тысячной процента.

В отличие от жилья, зарубежное гражданство не обесценивается из-за оттока населения, регулирования политики или роста процентных ставок. В любой момент времени оно соответствует одному и тому же набору четких прав, и его доходность чрезвычайно высока. Оно открывает доступ не к какой-то одной акции, а к целому измерению распределения активов: акции США, зарубежная недвижимость, оффшорное страхование, депозиты в иностранной валюте, легальные каналы для криптоактивов.

Самое соблазнительное — его нельзя передать. Такой актив, как гражданство, нельзя использовать для арбитража на вторичном рынке, как акции. Его можно только держать лично или передать через брак, рождение детей или наследование — три древних способа.

Недвижимость в хороших школьных районах когда-то создала целую серую индустрию: посредники, компании по передаче прав, фиктивная прописка, фиктивные браки и разводы. Индустрия зарубежного гражданства повторяет все это: посредники по программе привлечения талантов в Гонконге, золотая виза Португалии, Singapore EP, паспорт Мальты, быстрое гражданство в небольших странах Карибского бассейна. У каждого продукта есть четкий прайс-лист и сроки оформления.

Форма актива изменилась с «свидетельства о собственности» на «карту вида на жительство», с «диплома» на «право открыть счет».

Последние двадцать лет средний класс закреплял свой статус с помощью недвижимости в хороших школьных районах; следующие десять лет они будут закреплять свои активы с помощью зарубежного гражданства.

Учеба за границей равна покупке страховки?

Если взглянуть шире, логика покупки зарубежных ресурсов китайским средним классом за последние двадцать лет переопределялась трижды.

С 2000 по 2010 год это были ставки на возможности развития за рубежом. Отправка детей на учебу за границу, переезд семьи за рубеж основывались на наступательном суждении: возможности за границей больше, это инвестиция, цель — доход.

С 2010 по 2020 год это была диверсификация. После быстрого накопления богатства внутри страны зарубежная недвижимость, страхование и образование были включены в географическую диверсификацию семейных активов. Это была защита, цель — контроль рисков.

С 2020 года по настоящее время это «покупка страховки». Зарубежное гражданство больше не является частью портфеля, оно само стало пропуском. Даже если оно не приносит дохода, без него у вас нет даже права входа на некоторые инвестиционные рынки. Это страховой взнос для хеджирования неопределенности, цена которого растет по мере увеличения неопределенности.

Регуляторный удар 22 мая — это еще один скачок на этой кривой «цены страховки».

Когда поколение понимает, что уже упустило окно возможностей для получения зарубежного гражданства, они переносят надежду на следующее поколение. В следующий раз действительно подорожают, возможно, не услуги посредников по привлечению талантов, а места в международных школах, подготовительные курсы в зарубежных университетах, услуги по сопровождению детей на учебу за границей в раннем возрасте. «Страховка гражданства» будет передаваться вниз по поколениям семьи.

Я не знаю, какой путь в итоге выбрал тот самый 90-х годов с доходностью 2046%.

Потратив год на то, чтобы доказать на рынках акций США и криптовалют, что он лучший из 1%, оставив после себя доказательства, которые должны были стать ярким моментом в резюме.

Но после 22 мая это стало приложением к резюме для знакомств.

Кривая, которая могла бы заставить глаз менеджера фонда покраснеть, в итоге используется именно так.

Таков 2026 год.