Автор: Лун Юэ

Источник: Wall Street News

Чем сильнее растёт рынок, тем сложнее найти причину для падения — но риски никуда не исчезают, они просто скрываются глубже.

14 мая аналитик рынка Bloomberg Джон-Патрик Барнерт отметил в своей статье, что текущий рост на фондовом рынке США явно завышен, но затраты и выбор времени для открытия коротких позиций по-прежнему трудно оценить. Что ещё более проблематично, теперь даже стало неясно, «что должно быть главной причиной для коротких позиций».

Ключевое противоречие этого ралли заключается в следующем: позиции уже чрезвычайно переполнены, но базовый нарратив — особенно связанный с ИИ — по-прежнему поддерживает настроения рынка. Что из этого рухнет первым?

Позиции: рынок близок к состоянию «полной длинной позиции»

Если смотреть на чистую динамику цен, сигналы коррекции уже довольно очевидны.

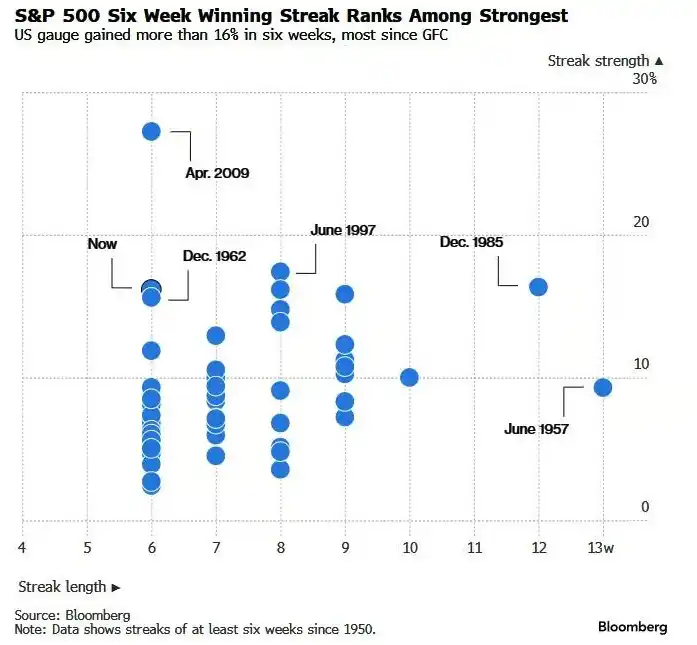

Шестинедельное ралли индекса S&P 500 является не только одним из самых продолжительных периодов роста за последние более чем 70 лет, но и одним из самых сильных по масштабу в истории. Барнерт заявил, что «передышка» для этого рынка — вполне нормальное явление.

Индикатор склонности к риску (Risk Appetite Indicator) Goldman Sachs снова поднялся до 1, что произошло впервые с начала года. Превышение этим индикатором уровня 1 — крайне редкое явление, которое в истории часто предвещало потенциальную коррекцию. В последний раз он превысил этот порог в 2021 году, после чего рынок вошёл в фазу медвежьего тренда.

Что касается самых популярных тематических акций, Барнерт описывает это как рынок, где «всё перекуплено», причём некоторые из самых горячих секторов достигли экстремального уровня перекупленности. В сочетании с механическим притоком средств — который в настоящее время, по-видимому, находится на максимальном уровне или близок к нему — общая картина такова: потенциал роста ограничен, а потенциальное давление для перераспределения позиций огромно.

Однако открывать короткие позиции нелегко. Барнерт отмечает, что корректировка позиций может произойти в течение одного дня, что делает выбор времени для входа и выхода из сделок на понижение чрезвычайно трудным. А если рынок выберет путь «медленного падения», то позиции по волатильности будут незаметно терять эффективность в условиях умеренной среды. Более вероятный сценарий: общие настроения останутся скорее бычьими, и если продавцы будут вынуждены закрывать короткие позиции (short squeeze), это может спровоцировать новую волну роста, которая окажется быстрее, чем кто-либо ожидал.

Потоки средств в некоторых популярных ETF уже начали демонстрировать微妙ные изменения — с тенденцией «фиксировать прибыль», а не «наращивать позиции на пике». Однако Барнерт также признаёт, что эта тенденция сохраняется уже несколько недель и пока не оказала существенного влияния на динамику рынка.

Нарратив: без ИИ рынок — ничто

Если позиции представляют собой техническую уязвимость, то на нарративном уровне ситуация в настоящее время выглядит более стабильной.

Барнерт указывает, что в настоящее время отсутствуют чёткие сигналы, которые могли бы спровоцировать фундаментальный медвежий рынок. Корпоративная прибыль остаётся сильной, инфляционные ожидания несколько выросли, но не достигли экстремального уровня. Рынок уже переварил удар от высоких цен на нефть и ситуации на Ближнем Востоке, а последние данные по занятости в США также ослабили опасения по поводу рецессии. Что касается ожиданий повышения процентных ставок, они уже давно не являются сдерживающим фактором для фондового рынка.

Но есть одна проблема, которую нельзя игнорировать: концентрация этого ралли уже сама по себе достигла высокой степени.

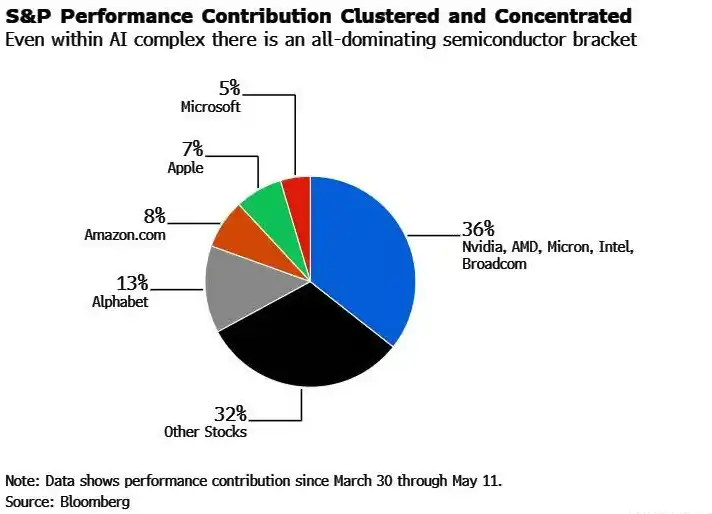

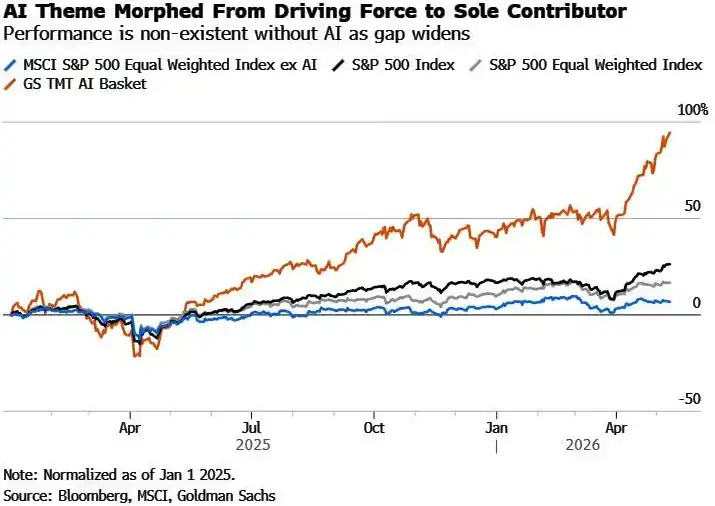

Барнерт отмечает, что независимо от того, сравнивается ли динамика индексов с ИИ и без ИИ, или анализируются источники роста с марта, вывод один и тот же: без ИИ результаты этого рынка можно охарактеризовать только как «посредственные». Более того, важно отметить, что сектор полупроводников в одиночку обеспечил почти 40% роста с марта.

Рыночный нарратив вокруг ИИ снова вошёл в режим «жадности», а не рационального стремления к разумной доходности. Опасения, которые активно обсуждались несколько месяцев назад — покроют ли сэкономленные на увольнениях средства затраты на вычислительные мощности ИИ, узкие места в энергоснабжении дата-центров, ценовая война в сфере ИИ, подрывающая маржу прибыли, новые конкуренты, разрушающие существующие модели с более низкими затратами, значительный рост капитальных затрат при стагнации выкупа акций, проблемы безопасности ИИ — сейчас, кажется, коллективно забыты рынком.

Риск повторения «момента DeepSeek»

Стратег Nomura Securities Чарли МакЭллиготт высказал самое прямое предупреждение по этому поводу.

Он заявил: «Учитывая текущую структуру рынка и высокую степень перекрытия тематик, в случае, если в какой-то день появится ещё один всеобъемлющий катализатор потрясений, подобный ‘DeepSeek’, это может напрямую спровоцировать торговлю по типу ‘лимитного падения’ (limit-down) на Nasdaq».

МакЭллиготт далее указал, что в таком сценарии дневное падение ETF на полупроводники может легко достичь 15% — потому что «гипотетическое обращение рефлексивных механических потоков средств спровоцирует крупномасштабное корректирующее падение с перелётом».

Другими словами, именно те механические потоки средств (такие как стратегии CTA, фонды риск-паритета и т.д.), которые постоянно добавляли покупательскую активность в процессе роста, в случае разворота станут усилителем ускоряющегося падения.

Два основных риска, с которыми сталкивается этот бычий рынок ИИ, — один технический (чрезмерная переполненность позиций), а другой нарративный (способна ли история ИИ продолжаться). Первый может сработать в любой момент, а второй, если рухнет, ударит глубже. Их сочетание создаёт наиболее серьёзную структурную уязвимость, заслуживающую внимания на текущем рынке.