Jason Jiang|Web3.01

К концу 2025 года выпуск Народным банком Китая «Плана действий по дальнейшему укреплению системы управления цифровым юанем и связанной финансовой инфраструктуры» ознаменовал официальный переход цифрового юаня из эры «цифровой наличности 1.0» в эру «цифровой депозитной валюты 2.0».

Ключевое изменение заключается в том, что с 1 января 2026 года остатки на кошельках цифрового юаня начнут приносить проценты, а его правовой статус изменится с прямого обязательства центрального банка на законное платежное средство с атрибутами обязательств коммерческих банков.

Общие дилеммы глобальных CBDC и прорыв цифрового юаня

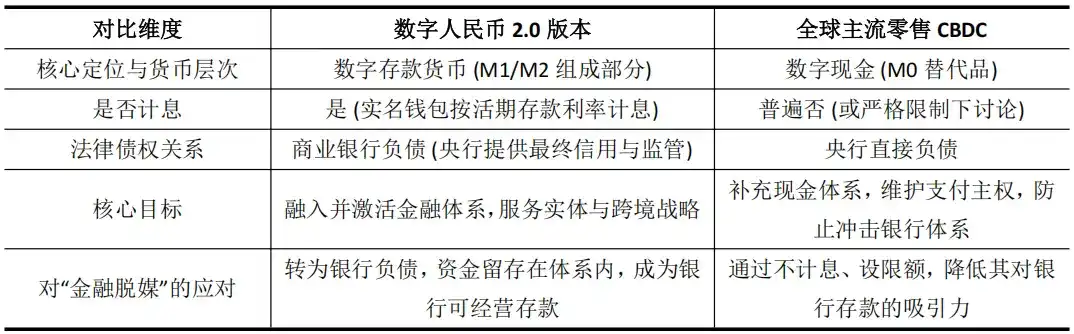

Практика более 130 денежно-кредитных органов, исследующих CBDC,普遍 сталкивается с трудноразрешимым парадоксом: как выпустить цифровую валюту, не подрывая основы традиционной банковской системы? Корень проблемы заключается в опасениях финансового дисбаланса — беспокойстве, что прямое предоставление центральным банком безопасной и удобной цифровой валюты населению может привести к оттоку депозитов из коммерческих банков и ударить по функции кредитования.

Таким образом, будь то дискуссии Европейского центрального банка об установлении лимитов на владение цифровым евро или четкие предупреждения Банка Японии, их основная логика является оборонительной. Они строго ограничивают розничный CBDC статусом беспроцентной цифровой наличности (M0), снижая его привлекательность по сравнению с банковскими депозитами для обеспечения финансовой стабильности. Однако это часто приводит к слабому внедрению CBDC из-за отсутствия стимулов для пользователей и банков, создавая дилемму расхождения между функциональностью и целями.

На этом фоне цифровой юань станет первым в мире CBDC, который будет выплачивать проценты на остатки обычных пользовательских кошельков. Цифровой юань 2.0 путем институциональных инноваций перестраивает отношения денежных обязательств, пытаясь нейтрализовать риски и создать новый импульс внутри банковской системы. Его отличие от других глобальных розничных CBDC заключается в следующем:

Эта модель превращает цифровой юань из инструмента «внешнего обращения», который мог бы ударить по банкам, в «внутреннюю кровь», глубоко интегрированную в балансы банков.

Коммерческие банки обладают правами управления и получения доходов от депозитов в цифровых юанях, и их мотивация к продвижению меняется с «пассивного выполнения обязанностей» на «активное управление», формируя устойчивый рыночный механизм продвижения. Кроме того, четкое страхование депозитов устраняет кредитные опасения на стороне пользователей.

Это не только решает проблему стимулирования, но и означает, что цифровой юань официально включен в традиционные рамки создания и регулирования денежной массы, предоставляя центральному банку новую переменную политики (ставку цифрового юаня), действующую напрямую. Его прослеживаемость также создает условия для реализации точной структурной денежно-кредитной политики.

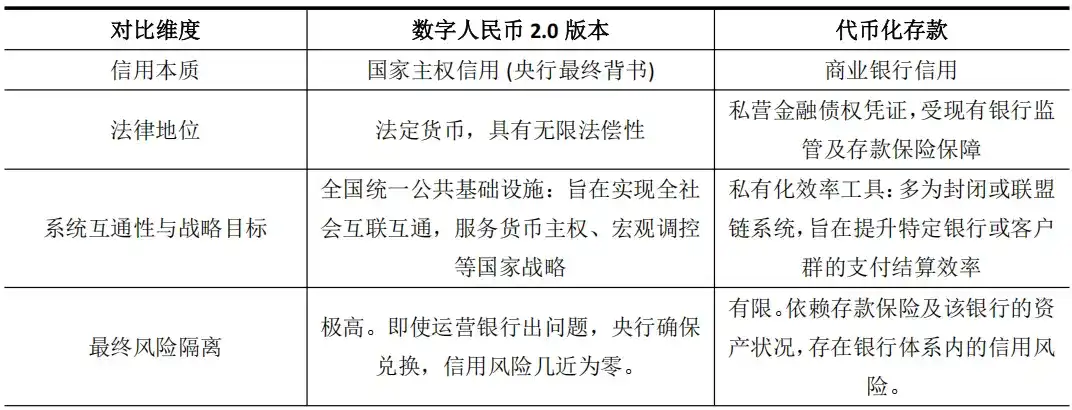

Определение новой формы: «Гибрид» CBDC и токенизированных депозитов

Цифровой юань 2.0 из-за своей особенности начисления процентов и банковского функционирования несколько похож на токенизированные депозиты, продвигаемые коммерческими банками. Последние представляют собой цифровые представления банковских депозитов на блокчейне (например, JPM Coin от JPMorgan Chase), предназначенные для повышения эффективности расчетов между институтами. Но это сходство лишь поверхностно, между ними существует фундаментальное различие в основе доверия и стратегическом уровне.

Цифровой юань 2.0 фактически создает новую гибридную форму: он заимствует внешнюю эффективность токенизированных депозитов, но его ядро — это полный кредит национальной sovereign валюты.

Это различие крайне важно. Кредит токенизированных депозитов тесно связан с балансом банка-эмитента, и по своей сути они являются инструментами повышения эффективности существующих финансовых посредников. В то время как фундамент доверия цифрового юаня 2.0 по-прежнему — национальный суверенитет, а его цель — построение базовой финансовой инфраструктуры для поддержки будущей цифровой экономики.

Отчет Института финансовых технологий Университета Цинхуа также указывает, что эта обеспеченная государственным кредитом, программируемая цифровая валюта предоставляет ключевую опору для построения двухплатформенной модели «блокчейн + цифровые активы».

Таким образом, обновление цифрового юаня 2.0 — это не просто эволюция платежного инструмента, но и заблаговременная прокладка «расчетного рельса» с наивысшим кредитным рейтингом для грядущей эры массовой токенизации активов.

Расширение возможностей цифровой финансовой экосистемы Гонконга за счет цифрового юаня с процентами

Стратегическое повышение уровня цифрового юаня наиболее прямо и глубоко затрагивает Гонконг с его уникальным геополитическим и институциональным положением.

Ключевая переменная — начисление процентов — кардинально меняет природу цифрового юаня в трансграничных и финансовых сценариях, превращая его из «платежного канала» в «стратегический актив», тем самым предоставляя существенные возможности на многих уровнях для строительства Гонконгом «Международного центра цифровых активов».

Во-первых, проценты решают проблему мотивации задержки трансграничных средств, напрямую усиливая функцию пула офшорных юаневых средств Гонконга.

В трансграничных платежных сетях на основе моста CBDC (mBridge) беспроцентные цифровые валюты являются лишь средством обращения, и у предприятий есть стимул быстро проводить расчеты, чтобы сократить стоимость占用 средств. После введения процентов цифровой юань приобрел свойства, конкурирующие с офшорными юаневыми депозитами в Гонконге. Казначейские центры транснациональных корпораций могут использовать его как приносящий проценты инструмент управления ликвидностью, оставаясь дольше в регулируемой системе Гонконга.

В настоящее время доля цифрового юаня в транзакциях mBridge превышает 95%, и политика начисления процентов может превратить это преимущество в объеме в преимущество в存量х, способствуя расширению и углублению пула офшорных юаневых средств Гонконга и укреплению его статуса хаба.

Во-вторых, проценты усиливают кредитную привлекательность цифрового юаня как валюты для выпуска и расчетов токенизированных активов в Гонконге.

Гонконг активно продвигает токенизацию активов, таких как облигации. В расчетах по принципу «поставка против платежа» (DvP) кредитный рейтинг расчетной валюты напрямую влияет на ценообразование риска и принятие рынком продукта. Цифровой юань с процентами и поддержкой государственного кредита имеет кредитный рейтинг, значительно превышающий токенизированные депозиты любого отдельного банка.

Проект Гонконгского валютного управления Ensemble уже исследует взаимодействие токенизированных депозитов, и цифровой юань 2.0 может быть подключен к этой экосистеме как актив для расчетов более высокого уровня. Используя программируемость цифрового юаня, можно автоматизировать процесс выплаты купонов по облигациям или условия торгового финансирования, значительно повысив эффективность и снизив операционные риски.

Это предоставляет Гонконгу потенциально более совершенный вариант базовой финансовой инфраструктуры для выпуска высококлассных продуктов, таких как токенизированные государственные зеленые облигации.

В-третьих, проценты активизируют пространство для инноваций в финансовых услугах вокруг цифрового юаня, создавая синергетические возможности для финтеха Гонконга.

Когда цифровой юань становится управляемым и приносящим проценты обязательством банка, вокруг него появятся услуги по депозитам, управлению капиталом, финансированию и управлению смарт-контрактами.

Гонконг, с его соответствующей международным стандартам системой общего права и активным финансовым рынком, является идеальной «песочницей» для тестирования подобных инновационных услуг. Например, можно разработать соответствующие шлюзы, соединяющие кошельки цифрового юаня с платформами виртуальных активов, или создать структурированные финансовые продукты на основе его процентных特性.

Этот синергетический эффект инноваций позволит Гонконгу захватить инициативу в разработке продуктов и установлении правил в области цифровых финансов.

В-четвертых, проценты углубляют стратегию дифференцированной синергии между цифровым юанем и гонконгским «цифровым гонконгским долларом» (e-HKD).

Гонконг четко определил приоритетное развитие оптового «цифрового гонконгского доллара», ориентированного на крупные сделки между финансовыми институтами и применение на рынках капитала. Цифровой юань 2.0 с процентами, в свою очередь, может быть сосредоточен на обслуживании трансграничных розничных платежей, расчетов по торговле и связанных с ними производных финансовых услуг, тесно связанных с реальной экономикой материкового Китая.

Они не являются заменой, а формируют четкую картину взаимодополняемости: цифровой гонконгский доллар оптимизирует эффективность местных оптовых финансов, а цифровой юань углубляет трансграничные экономические связи. Такая синергия позволяет Гонконгу одновременно укреплять местную финансовую инфраструктуру и функции трансграничного моста.