Автор: Кури, Чаосян Яньцзю

Введение: SpaceX назначила цену акций на 11 июня после закрытия торгов, выход на биржу под тикером SPCX на NASDAQ запланирован на 12 июня. Цена размещения составляет 135 долларов США за акцию, оценка компании — около 1,75 триллиона долларов США, объем привлеченных средств — 75 миллиардов долларов США, что делает это крупнейшее IPO в истории.

Однако исторические данные Motley Fool по 30 звездным технологическим IPO показывают: медианная доходность через 6 и 12 месяцев после выхода на биржу составила -9%, медианное максимальное проседание в первый год — 54%, и ни одна компания не избежала падения. Morningstar дает справедливую оценку лишь около 780 миллиардов долларов США, что меньше половины цены размещения.

В эту пятницу (12 июня) SpaceX выйдет на биржу под тикером SPCX на NASDAQ. Согласно сообщению Reuters от 3 июня, цена размещения установлена на уровне 135 долларов США за акцию, будет выпущено около 556 миллионов акций, объем привлеченных средств составит 75 миллиардов долларов США, что соответствует оценке компании примерно в 1,75 триллиона долларов (по некоторым источникам, с учетом послерыночных акций — 1,77 триллиона долларов). В любом случае это крупнейшее по объему IPO в истории фондового рынка. Синдикат андеррайтеров во главе с Goldman Sachs насчитывает 21 инвестиционный банк, окончательная цена будет определена после закрытия торгов на американском рынке 11 июня.

Ажиотаж не вызывает сомнений. SpaceX в документе S-1 заявила, что компания «нашла крупнейший в истории человечества общий целевой рынок с потенциалом реализации», количественная оценка которого составляет 28,5 триллиона долларов. Доля, предназначенная для розничных инвесторов, установлена на уровне 30% от обращающихся акций, что примерно в три раза выше обычного уровня для крупных IPO.

Проблема в том, что для обычных инвесторов, которые решат купить акции в день открытия торгов, исторические данные дают довольно неутешительный ответ.

Медианная картина: небольшая прибыль в первые три месяца, коллективный уход в минус через полгода

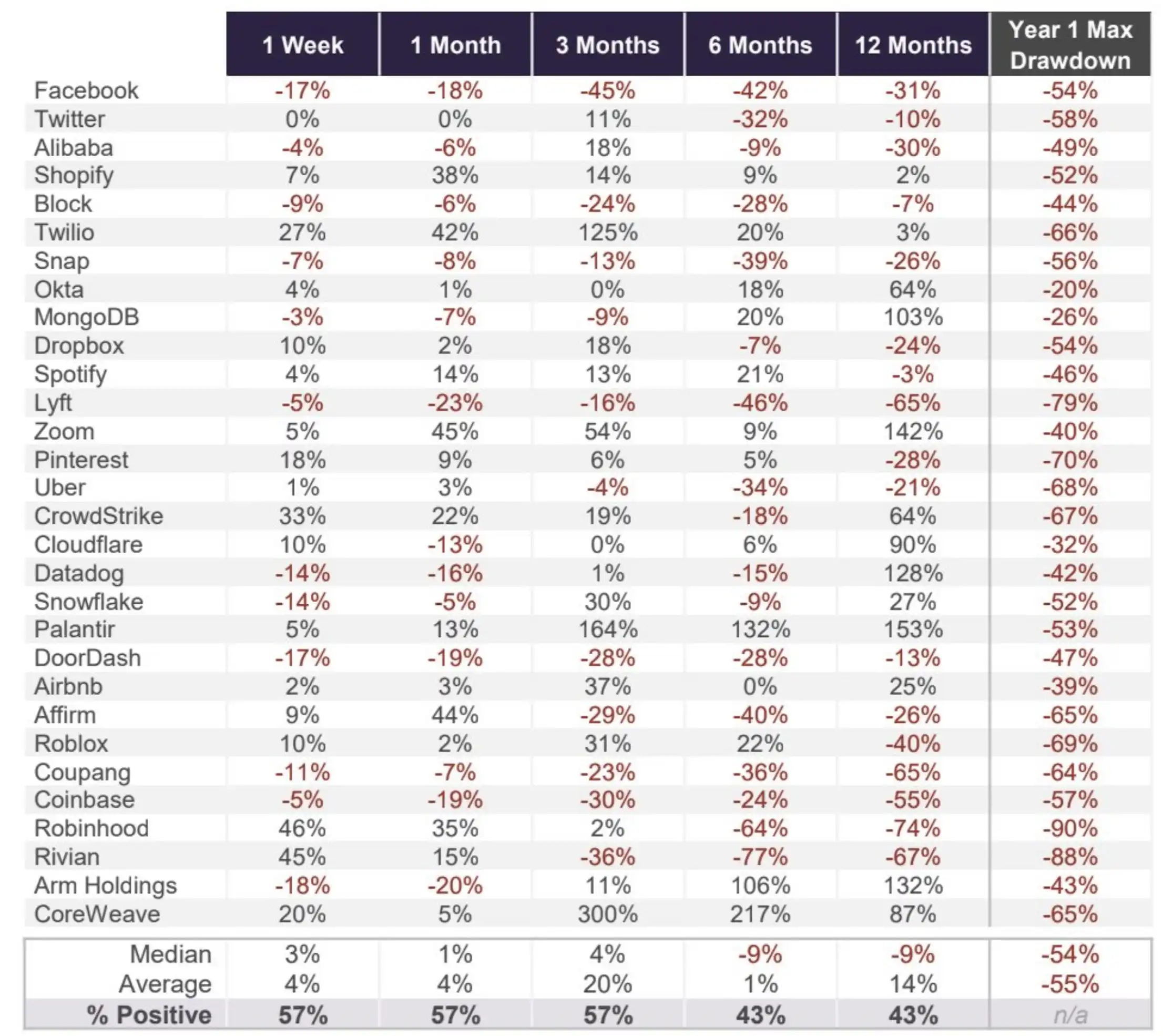

Аналитик Motley Fool Райан Ванзо в статье от 9 июня проанализировал результаты 30 звездных технологических компаний после IPO начиная с 2012 года, выборка включает компании от Facebook и Twitter до Coinbase, Robinhood, Rivian, Arm и CoreWeave.

Форма медианной кривой очень показательна: медианная доходность через 1 неделю после IPO составляет +3%, через 1 месяц +1%, через 3 месяца +4% — до этого момента все выглядит неплохо. Но если взглянуть на период в 6 месяцев, медианная доходность становится -9%; через 12 месяцев — все еще -9%. Доля компаний с положительной доходностью также резко сокращается, в первые три месяца она держится на уровне 57%, а на горизонтах 6 и 12 месяцев падает до 43%. Другими словами, продержавшись год, большинство покупавших по высоким ценам теряют деньги.

На уровне отдельных акций наблюдается огромная диверсификация. Акции CoreWeave выросли на 300% за 3 месяца после IPO, Palantir — на 164% за 3 месяца, Zoom — на 142% за 12 месяцев. Но негативных примеров также предостаточно: Lyft упала на 65% за 12 месяцев, Robinhood — на 74%, Rivian — на 67%, Coupang — на 65%. Между звездным статусом и доходностью после выхода на биржу не наблюдается стабильной связи.

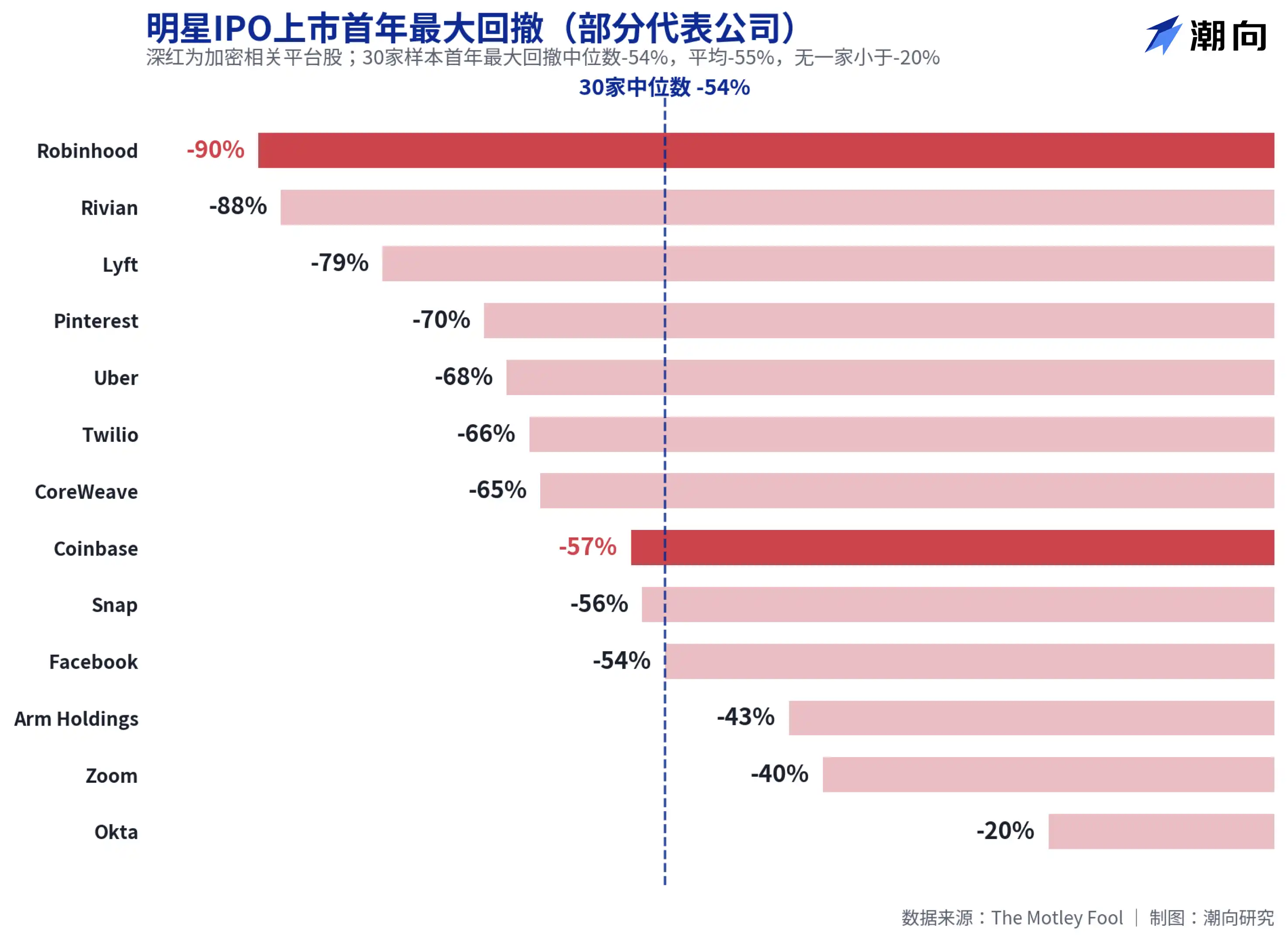

Медианное максимальное проседание в первый год — 54%, акции Robinhood и Coinbase также теряли более половины стоимости

Данные о проседании бросаются в глаза даже больше, чем данные о доходности. Медианное максимальное проседание для 30 компаний в первый год после IPO составило 54%, в среднем — 55%, минимальное проседание у Okta составило 20%, ни одна компания не избежала падения.

Две платформы, знакомые пользователям криптовалют, также находятся в зоне риска. Максимальное проседание акций Robinhood в первый год после IPO составило 90%, что является худшим показателем среди 30 компаний; проседание Coinbase составило 57%. Даже компании, которые впоследствии оказались успешными, не стали исключением: CoreWeave просела на 65% в первый год, Palantir — на 53%, Meta (тогда Facebook) — на 54%. Эти данные указывают на простой вывод: даже если вы выбрали правильную компанию, покупка по цене открытия, скорее всего, сначала приведет к убыткам, сопоставимым с потерей половины стоимости.

Академические исследования рисуют схожую картину. Джей Риттер, директор исследовательского проекта по IPO Университета Флориды, отследил 1479 IPO с 2012 по 2021 год, средняя доходность в первый день составила 23,6%, но средняя общая доходность за последующие три года составила лишь 10,6%. The Wall Street Journal, ссылаясь на данные Риттера, сообщает, что инвесторы, купившие акции в первый день листинга и державшие их три года, получили доходность примерно на 21% ниже, чем если бы они просто купили взвешенный по рыночной капитализации индекс. Ажиотаж в первый день в основном исчерпывает последующий рост.

Отчетность SpaceX: выручка в 18,7 миллиарда долларов США поддерживает оценку в 1,75 триллиона долларов США

Возвращаясь к самой SpaceX, споры об оценке более конкретны, чем исторические закономерности.

Согласно финансовым данным, на которые ссылается The Motley Fool, выручка SpaceX в 2025 году составила 18,7 миллиарда долларов США, что на 33% больше, чем в предыдущем году, но чистый убыток составил 4,9 миллиарда долларов США, что стало разворотом по сравнению с прибылью около 790 миллионов долларов США в 2024 году. Согласно данным документа S-1, собранным BitMEX, чистый убыток за первый квартал 2026 года составил 4,28 миллиарда долларов США, накопленный убыток — 41,3 миллиарда долларов США, причем бизнес в области ИИ (после слияния с xAI) сжигает около 2,5 миллиарда долларов США в квартал. При оценке в 1,75 триллиона долларов США соотношение цены к выручке превышает 90.

Позиция Morningstar наиболее прямолинейна. Аналитики агентства назвали SpaceX «сильно переоцененной», считая, что у долгосрочных инвесторов после IPO появится возможность купить акции с лучшим запасом прочности, и установили справедливую оценку примерно в 780 миллиардов долларов США, что меньше половины оценочной стоимости при размещении. Референс: оценка SpaceX при предложении о выкупе акций вне биржи в декабре 2025 года составляла около 800 миллиардов долларов США, то есть за полгода цена выросла более чем вдвое.

Логика быков также существует. На долю бизнеса по запуску ракет приходится более 80% рынка США, у Starlink более 12 миллионов подписчиков, и он уже прибылен, что является основой этой оценки. Сам Ванзо считает, что акции SpaceX, скорее всего, покажут хорошие результаты в первый день листинга, но с учетом уровня оценки и исторических данных, неудивительно, если в течение следующих 12 месяцев цена акций будет испытывать трудности.

Для тех, кто планирует разместить заявки в пятницу, по крайней мере стоит взглянуть на данные этих 30 компаний: история не гарантирует повторения, но сначала потерять половину стоимости в первый год было нормой для этой игры за последние четырнадцать лет.