Оригинальное название: Wall Street Pulls Back From Bitcoin』s Money-Spinning Basis Trade

Оригинальный автор: Sidhartha Shukla, Bloomberg

Оригинальная компиляция: Peggy, BlockBeats

Примечание редактора: Арбитраж биткоин-базиса, некогда считавшийся «безрисковым и прибыльным», незаметно теряет привлекательность: открытые позиции на CME и Binance меняются местами, спреды сузились до уровня, едва покрывающего стоимость финансирования и исполнения.

На поверхности это сжатие арбитражных возможностей; на более глубоком уровне это свидетельствует о созревании рынка криптодеривативов. Институциональным игрокам больше не нужно зарабатывать на «арбитраже», трейдеры переходят от кредитного плеча к опционам и хеджированию. Эпоха высоких доходов с помощью простых стратегий уходит, новая конкуренция будет разворачиваться в более сложных и изощренных стратегиях.

Ниже оригинальный текст:

На рынке криптодеривативов происходит тихая, но значимая перемена: один из самых стабильных и прибыльных торговых стратегий начинает показывать признаки сбоя.

Часто используемая институциями стратегия «кэрри-трейд» (покупка биткоина спот с одновременной продажей фьючерсов для заработка на спреде) рушится. Это не только предвещает быстрое сжатие арбитражных возможностей, но и посылает более глубокий сигнал: структура крипторынка меняется. Открытый интерес (open interest) к фьючерсам на биткоин на Чикагской товарной бирже (CME) впервые с 2023 года упал ниже показателя Binance, что further illustrates, как по мере сужения спредов и повышения эффективности доступа на рынок, те прибыльные арбитражные возможности, что были в прошлом, быстро исчезают.

После запуска спотовых Биткоин-ETF в начале 2024 года, CME一度 стала предпочтительной площадкой для исполнения этих стратегий трейдинговыми десками Уолл-стрит. Эта логика операций очень похожа на «арбитраж базиса» (basis trade) на традиционных рынках: покупка биткоина спот через ETF с одновременной продажей фьючерсных контрактов и заработок на спреде между ними.

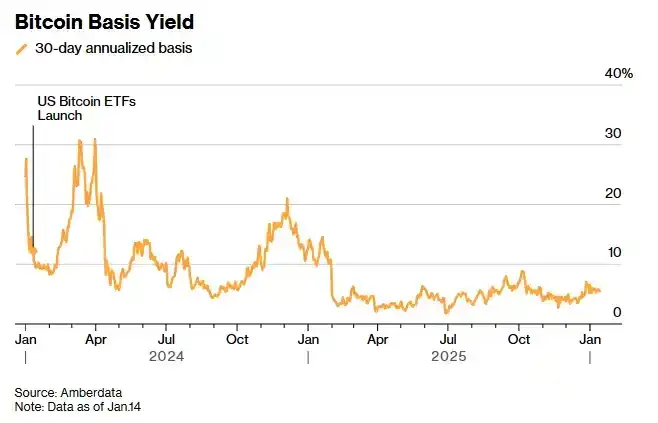

А в месяцы после одобрения ETF годовая доходность этой так называемой «Дельта-нейтральной стратегии» часто достигала двузначных цифр, привлекая миллиарды долларов — эти деньги не интересовало направление движения цены биткоина, только возможность получить доход. Но именно ETF, которые способствовали быстрому расширению этой торговли, заложили основу для ее завершения: по мере того как все больше трейдинговых десков устремлялись на рынок, арбитражный спред быстро сокращался. Сегодня доход от этой сделки едва покрывает стоимость финансирования.

Согласно aggregated данным Amberdata, текущая годовая доходность для месячного горизонта колеблется около 5%, находясь на многолетних минимумах. Глава отдела деривативов Amberdata Грег Магадини отметил, что годом ранее базис был близок к 17%, а сейчас снизился примерно до 4.7%, чего едва хватает для покрытия порога стоимости финансирования и исполнения. Между тем, доходность годовых казначейских облигаций США составляет около 3.5%, что быстро снижает привлекательность этой сделки.

На фоне продолжающегося сужения базиса, согласно aggregated данным Coinglass, объем открытых позиций по фьючерсам на биткоин на CME упал с пика в более чем $21 млрд до менее чем $10 млрд; в то время как открытый интерес на Binance оставался относительно стабильным, около $11 млрд. Генеральный директор цифровой asset management компании Tesseract Джеймс Харрис заявил, что это изменение в большей степени отражает отток хедж-фондов и крупных американских счетов, а не полный отход от криптоактивов после того, как цена биткоина достигла пика в октябре.

Такие криптобиржи, как Binance, являются основными площадками для торговли бессрочными контрактами (перпетами). Эти контракты рассчитываются, оцениваются и по ним вычисляется маржа непрерывно, часто несколько раз в день. Бессрочные контракты, часто сокращенно называемые «perps», занимают наибольшую долю объема торгов на крипторынке. В прошлом году CME также запустила фьючерсные контракты с меньшим номиналом и более длительными сроками, охватывающие криптоактивы и рынки индексов акций, предлагая фьючерсные позиции, близкие к спотовому рынку, что позволяет инвесторам удерживать контракты до пяти лет без частого ролловера.

Харрис из Tesseract отметил, что исторически CME была предпочтительной площадкой для институциональных средств и стратегии «кэрри-трейд». Он добавил, что превышение открытого интереса на Binance над CME «является важным сигналом того, что структура участия на рынке смещается». Он охарактеризовал текущую ситуацию как «тактическую перезагрузку», вызванную снижением доходности и истончением ликвидности, а не потерей доверия к рынку.

Согласно заявлению CME Group, 2025 год стал ключевым переломным моментом для рынка: по мере прояснения регуляторных рамок и улучшения ожиданий инвесторов в отношении этой сферы, институциональный капитал также начал расширяться от ставок исключительно на биткоин до таких токенов, как Ethereum, XRP от Ripple и Solana.

CME Group заявила: «В 2024 году среднедневной номинальный открытый интерес по фьючерсам на Ethereum составлял около $1 млрд, а к 2025 году этот показатель вырос почти до $5 млрд.»

Хотя снижение процентных ставок ФРС снизило стоимость финансирования, это не привело к устойчивому восстановлению на крипторынке после того, как 10 октября цены различных токенов集体 обрушились. Текущий спрос на заимствования ослаб, доходность в децентрализованных финансах (DeFi) находится на низком уровне, и трейдеры чаще倾向于 использовать опционы и инструменты хеджирования,而不是 напрямую использовать кредитное плечо для directional ставок.

Управляющий директор Auros в Гонконге Ле Ши заявил, что по мере созревания рынка у традиционных участников теперь есть больше каналов для выражения directional views, от ETF до прямого доступа к биржам. Это увеличение выбора сокращает ценовые разрывы между различными торговыми площадками, что, естественно, сжимает арбитражное пространство, которое ранее раздувало открытый интерес на CME.

Ле сказал: «Здесь существует эффект саморегулирования». Он считает, что когда участники рынка стекаются на торговые площадки с самыми низкими costs, базис сужается, а incentive для занятия кэрри-трейдом ослабевает.

В среду биткоин временно упал на 2.4%, до $87,188, затем частично отыграл потери. Это падение временно стерло все gains с начала года.

Главный инвестиционный директор 319 Capital Bohumil Vosalik заявил, что эпоха получения высоких доходов практически без риска, возможно, закончилась, что заставит трейдеров перейти к более сложным стратегиям на децентрализованных рынках. Для высокочастотных и арбитражных институций это означает, что им придется искать opportunities в других местах.

Оригинальная ссылка