Источник: Fintech Blueprint

Оригинальное название: Analysis: Learning from 2025 to win big in the 2026 machine economy

Компиляция и редактирование: BitpushNews

Структурные проблемы крипторынка

Внедрение финансовых инструментов на блокчейне и тренды машинной экономики активно развиваются.

За последний год мы наблюдали огромное расширение нативных блокчейн-финансов по следующим пяти направлениям: (1) стейблкоины, (2) децентрализованное кредитование и торговля, (3) перпетуальные контракты, (4) прогнозные рынки и (5) хранилища цифровых активов (DATs). Регуляторная среда в США стала чрезвычайно благоприятной, что способствовало росту как количества проектов, так и аппетита к риску.

Если отбросить неопределённость, вызванную пошлинами и структурой рынка, снисходительная макросреда также предоставила плодородную почву для укоренения крипто-инноваций. Эти тренды широко известны, и нет необходимости снова перечислять данные.

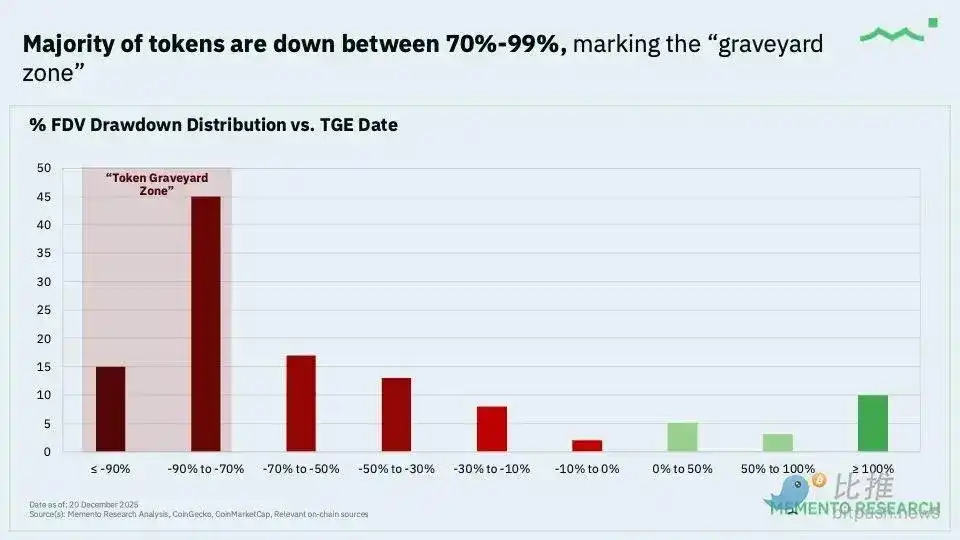

Однако 2025 год оказался чрезвычайно трудным для долгосрочных инвесторов в токены и криптоактивы, за исключением биткоина.

Если вы трейдер или банкир, у вас, возможно, всё было неплохо — мы видели рекордные комиссии за вывод DATs на рынок, а также огромные доходы от комиссий, полученные такими биржами, как Binance, в процессе листинга.

Но для тех из нас, у кого инвестиционный горизонт составляет 3-5 лет, структура рынка была ужасной.

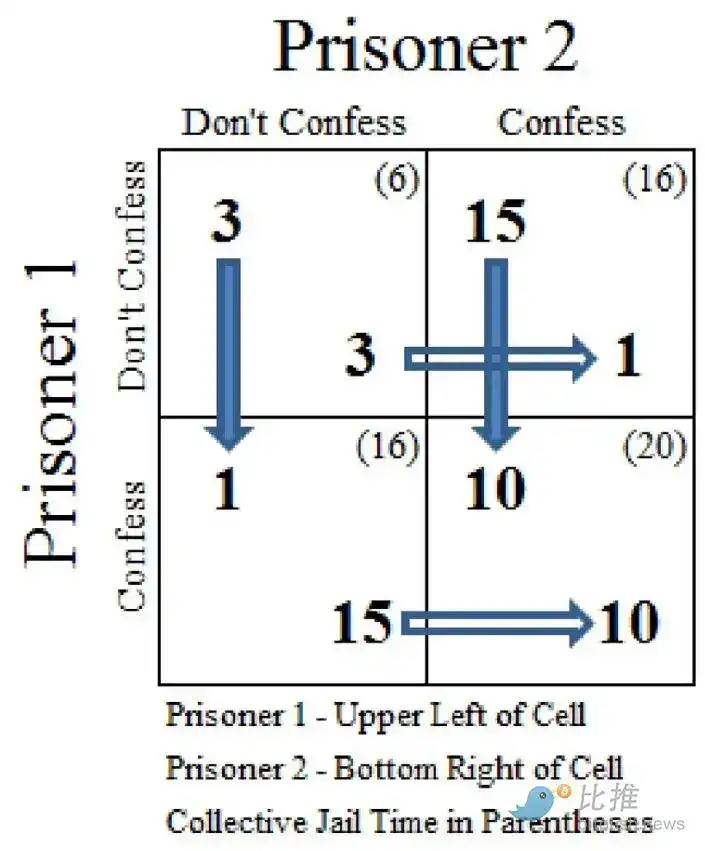

Мы полностью погрузились в «негативную дилемму заключённого»: держатели токенов ожидают будущего давления продаж и поэтому продают любые и все активы; а маркет-мейкеры и биржи, поддерживающие всю криптоэкономику, занимают спекулятивные позиции, ориентированные только на краткосрочную выгоду. Механизмы разблокировки токенов и цены эмиссии часто тянут проекты на дно ещё до того, как они достигнут прибыльности или найдут продукт-маркет fit.

Кроме того, структурный сбой рынка 10 октября 2025 года явно нанёс удар по нескольким крупным игрокам на рынке, и хотя потери ещё не обнародованы, волны ликвидаций продолжаются. Корреляция между всеми криптоактивами возросла почти до 1, что указывает на отраслевую делевереджинг-активность, несмотря на их сильно различающуюся фундаментальную логику.

Сейчас легко отступить и стать циничным.

Но мы предпочитаем провести «переоценку к рыночной стоимости» (Mark-to-market) как можно более чётко, чтобы планировать будущие позиции.

Падение в сфере криптоинвестиций в 2025 году — это информация, но не окончательный вердикт. Вполне вероятно, что в 2026 году на вторичном рынке частных компаний мы увидим масштабные распродажи, и тогда мы проанализируем, как в период крипто-бума было выпущено так много инструментов специального назначения (SPV) по высоким оценкам.

Тем временем, видение программируемых финансов и «рободенег» (Robot Money) продолжает реализовываться, и мы должны продолжать усердно работать, чтобы найти оптимальные позиции в процессе их неизбежного подъёма.

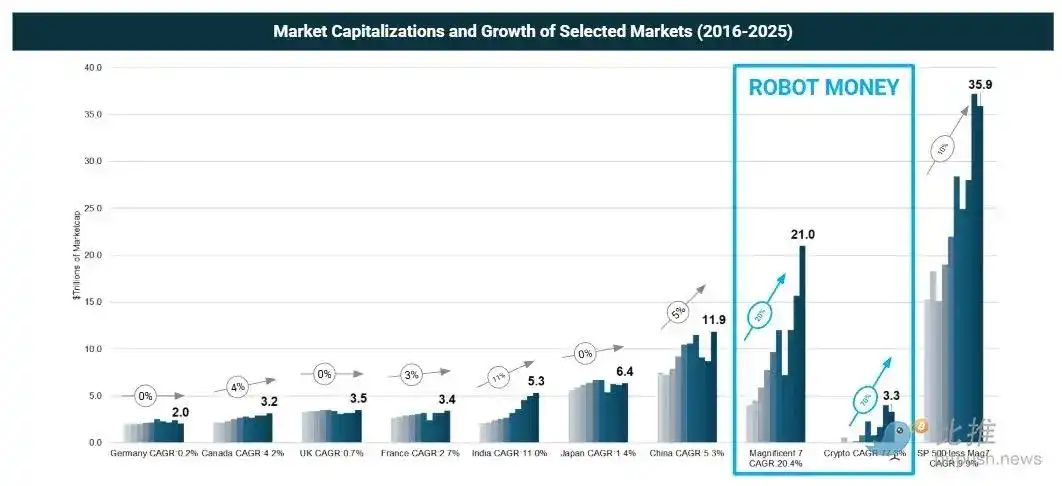

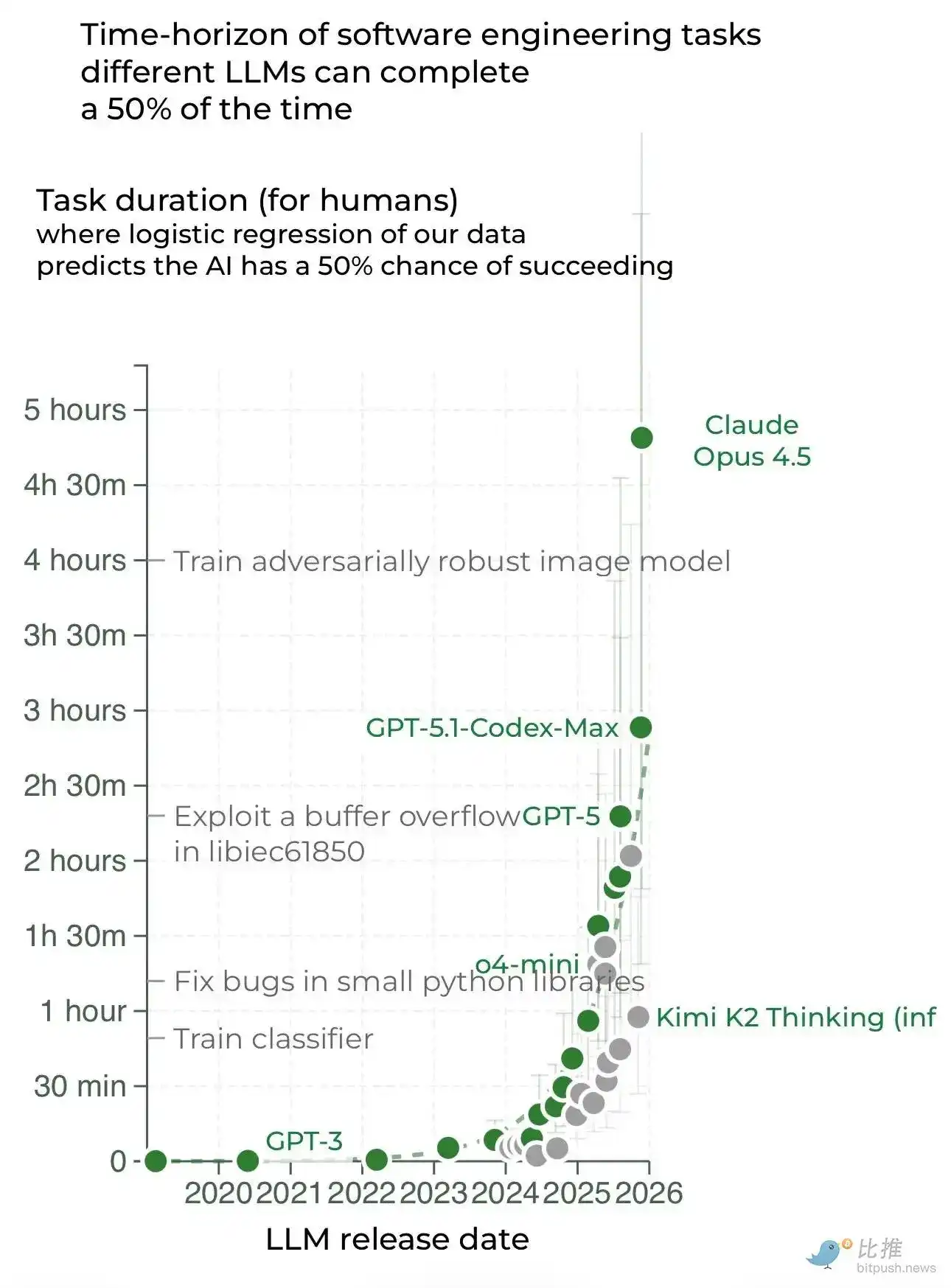

Для контекста взгляните на график ниже. Он охватывает последнее десятилетие и показывает создание рыночной капитализации в нескольких регионах и отраслях.

Когда мы смотрим на эту историю, создание стоимости в сферах криптовалют и ИИ ошеломляет по сравнению с остальным миром.

Европейские рынки капитала (около 2-3 трлн долларов по странам) практически ничего не создали, просто поддерживая статус-кво. Вы могли бы просто инвестировать в гособлигации и получать 3% годовых, создавая, возможно, большую стоимость. В правой части графика Индия и Китай показывают复合年均增长率 (CAGR) в 5-10%, с чистым ростом рыночной капитализации примерно на 3 трлн и 5 трлн долларов соответственно за тот же период.

Поняв этот масштаб, взгляните на то, что мы определяем как «рободеньги»:

«Великолепная семёрка» (Magnificent 7) акций технологических компаний и ИИ в США увеличила рыночную капитализацию примерно на 17 трлн долларов со скоростью 20% в год;

Рынок криптоактивов, представляющий современные финансовые рельсы, добавил за тот же период 3 трлн долларов с复合年均增长率 (CAGR) в 70%.

Это будущий финансовый центр.

Но просто быть логически правым недостаточно. Мы должны тщательно и детально определить те части цепочки создания стоимости, которые ещё не осознаны миром. Вспомните разговоры о роботах-советниках в 2009 году, о необанках (Neobanks) в 2011 или о DeFi в 2017 — тогда словарь и ассоциации ещё не сформировались, и только через 2-5 лет эти результаты затвердели в чёткие бизнес-возможности.

Захват стоимости в машинной экономике

В качестве «мазохистского» упражнения мы собрали сводный отчёт на 158 страницах, охватывающий наиболее relevant участников машинной экономики 2025 года.

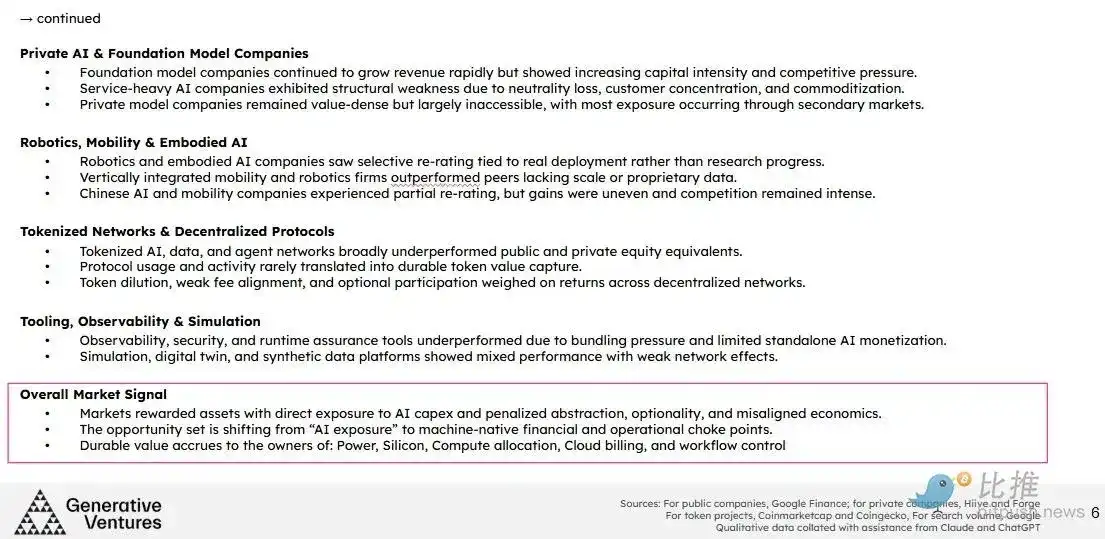

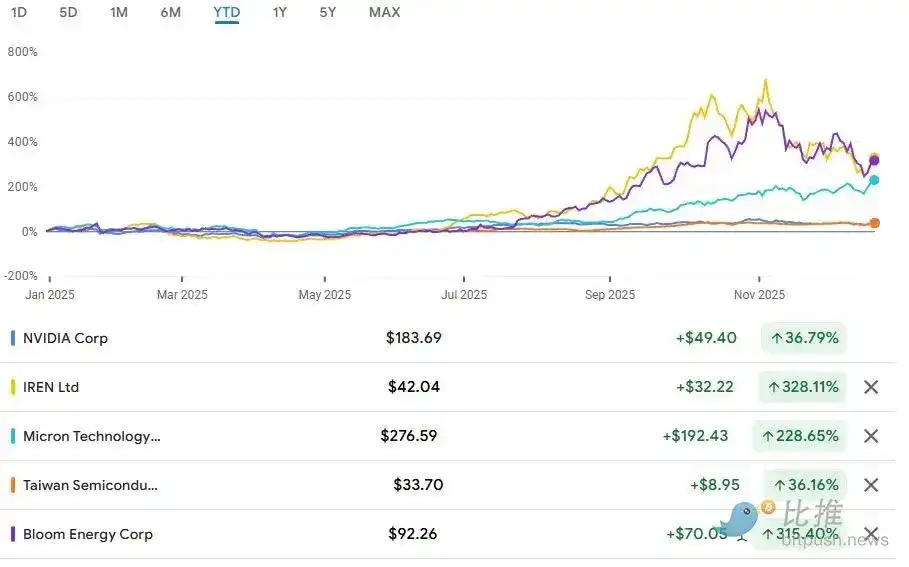

На публичных рынках 2025 год стал годом «усиления сильных и отставания слабых».

Очевидными победителями стали владельцы физических и финансовых узких мест: электроэнергия, полупроводники и дефицитные вычислительные мощности.

Bloom Energy, IREN, Micron, TSMC и NVIDIA показали результаты значительно лучше рынка, поскольку капитал гонится за активами, через которые «должны пройти машины».

Bloom и IREN являются典型ными примерами: они находятся прямо на острие капитальных затрат на ИИ, превращая срочность в доход.

Для сравнения, традиционная инфраструктура, такая как Equinix, показала вялые результаты, что отражает мнение рынка о том, что стоимость универсальных мощностей значительно ниже, чем у гарантированного электропитания, высокоплотных, кастомизированных вычислительных мощностей.

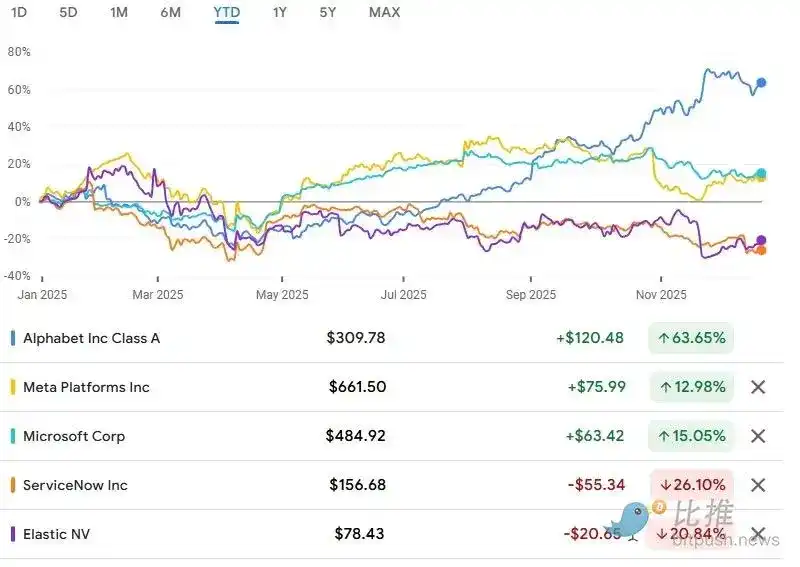

В сфере программного обеспечения и данных производительность分化ровалась по другому измерению: (1) обязательность против (2) опциональности. Встраиваемые в рабочие процессы и имеющие обязательные продления корпоративные системы платформенного типа (такие как Alphabet, Meta) продолжали复合ный рост, показав рост с начала года, поскольку расходы на ИИ укрепили их существующие рвы дистрибуции. ServiceNow и Datadog, несмотря на сильные продукты, столкнулись с давлением на valuation, давлением со стороны гиперскейлеров облачных услуг в виде бундлинга и более медленной монетизацией ИИ, что сказалось на их доходности. Elastic иллюстрирует неблагоприятный сценарий: сильные технические возможности, но давление со стороны cloud-native альтернатив, и unit-экономика ухудшается.

На приватном рынке наблюдается similarный механизм отбора.

Компании с базовыми моделями (foundation models) — главные герои истории, но хрупкость растёт. OpenAI и Anthropic быстро растут в доходах, но их нейтральность, капиталоёмкость и сжатие маржинальности теперь стали явными рисками. Scale AI — это предостерегающий случай года: частичное поглощение со стороны Meta разрушило её статус «нейтральной» и вызвало отток клиентов, что доказывает, как быстро может рухнуть сервисно-ориентированная бизнес-модель,一旦 доверие нарушено. Для сравнения, компании, контролирующие стоимость (Applied Intuition, Anduril, Samsara и emerging операционные системы для автопарков), выглядят better positioned, даже если реализация стоимости в основном остаётся в непубличном состоянии.

Токенизированные сети были самым слабым сегментом.

За исключением极少数 проектов, децентрализованные протоколы для данных, хранения, агентов (Agent) и автоматизации показали плохие результаты, поскольку использование не преобразовывалось в захват стоимости токена.

Chainlink сохраняет стратегическую важность, но испытывает трудности с согласованием доходов протокола и токеномики; Bittensor — крупнейшая ставка в крипто-ИИ сфере, но пока не представляет существенной угрозы для Web2 лабораторных компаний; Giza и similarные протоколы для агентов показали реальную активность, но всё ещё страдают от dilution и мизерных комиссий. Рынок больше не вознаграждает «коллаборативные нарративы» без механизмов принудительного сбора платы.

Стоимость накапливается в тех областях, за которые машины уже платят — электроэнергия, кремний, вычислительные контракты, облачные счета и регулируемые балансы, — а не в тех, которые они могут выбрать someday в будущем.

В 2025 году рынок награждал владение «узкими горлышками» и наказывал проекты с одними лишь идеалами, но без контроля над денежными потоками или вычислительной мощностью. Будущее заключается в идентификации мест, где экономическая сила уже существует, и в ставках на активы, которые машины не могут обойти.

Ключевые выводы:

- Реализация стоимости ИИ происходит на «уровень глубже», чем предполагало большинство.

- Нейтральность теперь является активом первого порядка (см. Scale AI).

- «Платформа» работает только в сочетании с точками контроля, а не просто как функция.

- ИИ-ПО дефляционно (давление на цены); инфраструктура ИИ — инфляционна.

- Вертикальная интеграция важна только если позволяет зафиксировать данные или экономические эффекты.

- Токен-сети repeatedly проходят одни и те же испытания структурой рынка.

- Просто иметь экспозицию на ИИ недостаточно, всё решает качество позиционирования.

- Аппаратное и программное обеспечение для роботов станет следующим циклом хайпа, и мы, вероятно, увидим similarную волну инвестиций и избирательных победителей.

Позиционирование на 2026 год

За последние два года мы создали核心овый инвестиционный портфель, охватывающий ключевые темы, обсуждаемые здесь. looking ahead на 2026 год, наше позиционирование и инвестиционное исполнение будут ещё более усилены.

Далее я расскажу о нашей стратегии持仓.

Хотя долгосрочное видение автономных агентов, роботов и machine-native финансов верно по направлению, рынок сейчас находится на стадии чрезвычайно завышенных оценок в частном сегменте ИИ и робототехники. Агрессивная вторичная ликвидность и подразумеваемые оценки свыше 1000 млрд долларов знаменуют переход от «фазы открытия» к «фазе выхода».

Как ранний фонд с финтех-углом (Fintech angle), мы должны瞄准下游ние цели этих расходов:

- Поверхности машинных транзакций (Machine Transaction Surfaces): Уровни, где машины или их операторы уже несут экономическую активность, такие как платежи, биллинг, учёт, маршрутизация, а также оркестрация капитала или вычислительной мощности, compliance, кастодиальные и settlement примитивы. Возврат получается через объём транзакций, поглощения или регуляторный статус, а не через спекулятивные нарративы. Walapay и Nevermined в нашем портфеле являются примерами.

- Прикладная инфраструктура с бюджетами (Applied Infrastructure With Budgets): Инфраструктура, которую предприятия или платформы уже закупают, такая как агрегация и оптимизация вычислительной мощности, сервисы данных, встроенные в рабочие процессы, инструменты с recurring расходами и cost of switching. Акцент на владении бюджетом и глубине интеграции. Например, Yotta Labs и Exabits.

- Высоко-новизнные возможности: Несколько асимметричных возможностей для роста с неопределённым временем: фундаментальные исследования, передовая наука, культурные или IP-платформы, связанные с ИИ. Наша недавняя инвестиция в Netholabs (лаборатория, работающая над симуляцией полного digital мозга мыши) соответствует этому признаку.

Кроме того, до решения проблем структуры токен-рынка, мы будем more активно инвестировать в акции (Equity). Ранее наша экспозиция составляла 40% на токены и 40% на акции, оставшиеся 20% гибко распределялись. Мы считаем, что токен-сектору потребуется 12-24 месяца, чтобы переварить текущие трудности.

Ключевые выводы

Вам не нужно быть венчурным инвестором, чтобы извлечь уроки из этой рыночной динамики и получить выгоду.

Огромные капитальные расходы перетекают от tech-гигантов к поставщикам энергии и компонентов. От нескольких компаний ожидается, что они станут победителями на публичном рынке с триллионными капитализациями, но они choose оставаться приватными, одновременно выделяя SPV. Публичные компании尽力防御. Политическая власть централизует и национализирует эти инициативы — будь то Маск и Трамп, или Китай и DeepSeek — а не поддерживает их децентрализованные альтернативы в Web3. Робототехника переплетается с государственным manufacturing и ВПК.

В креативных индустриях (от игр до кино, музыки) наблюдается сопротивление ИИ, люди, занимающиеся «человеческим ремеслом», отвергают роботов, которые pretend делать то же самое.

А в software, науке и математике ИИ被视为 великое достижение, способное помочь в открытиях и построении эффективных бизнес-архитектур.

Нам нужно перестать верить в эту коллективную иллюзию и вернуться к реальности. С одной стороны, уже есть десятки компаний, достигших годового дохода свыше 100 млн долларов, обслуживая пользователей; с другой стороны, на рынке同样充斥着大量 подделок и мошенничества. Оба этих утверждения верны и сосуществуют параллельно.

Новый год принесёт全面ную перетряску, но также и огромные возможности. Успеха можно достичь, only осторожно продвигаясь по канату возможностей. До встречи на том берегу!