Автор: Tanay Jaipuria, партнёр Wing

Компиляция: Felix, PANews

Введение: 25 мая на сайте Шанхайской фондовой биржи появилась информация, что IPO Unitree Robotics на рынке STAR Китая (Tech-innovation board) будет рассмотрено 1 июня. Компания планирует привлечь 6,2 миллиарда долларов, стремясь стать первой акцией компании по производству человекоподобных роботов на рынке А.

Проспект эмиссии Unitree Robotics привлекает большое внимание, потому что он хорошо отражает реальное состояние развития текущего рынка роботов.

Будучи компанией с самым большим объёмом продаж человекоподобных роботов в мире, Unitree не только достигла прибыльности, но и сохраняет высокие темпы роста. В этой статье будут рассмотрены:

-

Продукция Unitree Robotics

-

Изменение структуры выручки в сторону человекоподобных роботов

-

Какие предприятия сейчас покупают роботов (и почему)

-

Вертикально интегрированная бизнес-модель

-

Финансовый анализ

-

Цели развития на уровне моделей

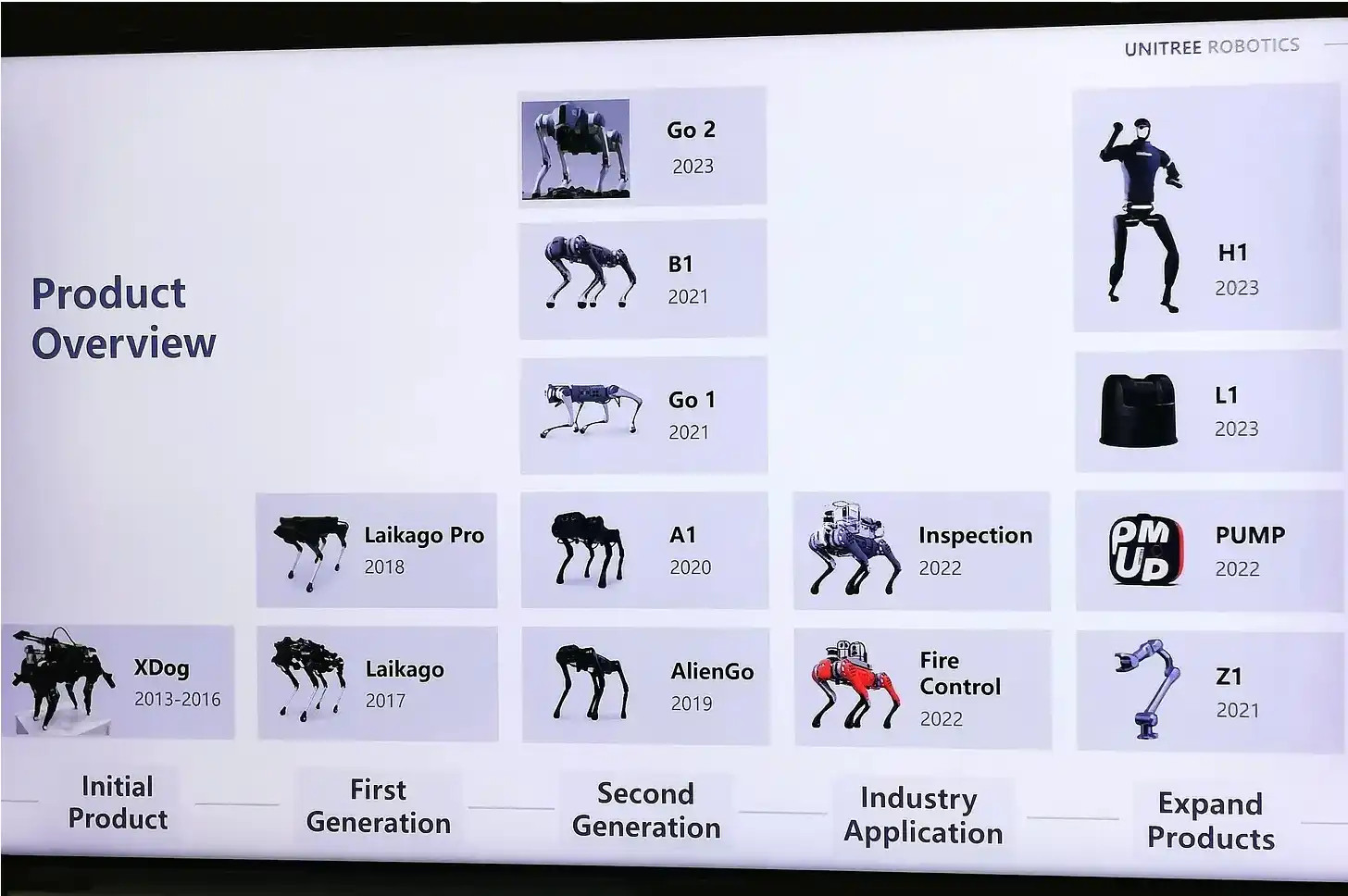

Продукция Unitree Robotics

Unitree Robotics была основана в 2016 году в Ханчжоу. Основатель Ван Синсин — самоучка, эксперт по робототехнике, известный тем, что создал первого четвероногого робота в своей квартире. В компании сейчас работает 480 сотрудников, из которых около 175 — сотрудники R&D.

Компания в основном продаёт два типа продуктов:

-

Четвероногие роботы (робособаки): Go2 (потребительского и исследовательского уровня), B2 (промышленного уровня) и A2.

-

Человекоподобные роботы: H1, H2, G1 и R1. Возможно, вы видели G1 в популярных видео в интернете: его рост 1,32 метра, вес 35 килограммов.

Компания начала международную деятельность с 2018 года. Более 35% выручки поступает из-за пределов Китая, включая значительную клиентскую базу в американских академических кругах.

Переход к человекоподобным роботам

Два года назад Unitree Robotics по сути была компанией по производству робособак, в основном продающей четвероногих роботов. В 2023 году человекоподобные роботы составляли лишь 1,9% её выручки.

Однако к первым трём кварталам 2025 года человекоподобные роботы уже составляли более половины её доходов.

Этому переходу способствовали соответствие продукта рынку и агрессивная маркетинговая стратегия. Человекоподобные роботы компании два года подряд появлялись на гала-концерте CCTV в честь Праздника Весны. В 2024 году Дженсен Хуанг также демонстрировал робота Unitree на конференции GTC.

Робот Unitree на гала-концерте CCTV в честь Праздника Весны

Этот брендовый пиар успешно преобразовался в коммерческий и исследовательский спрос — то, чего большинство китайских hardware-компаний никогда по-настоящему не достигали.

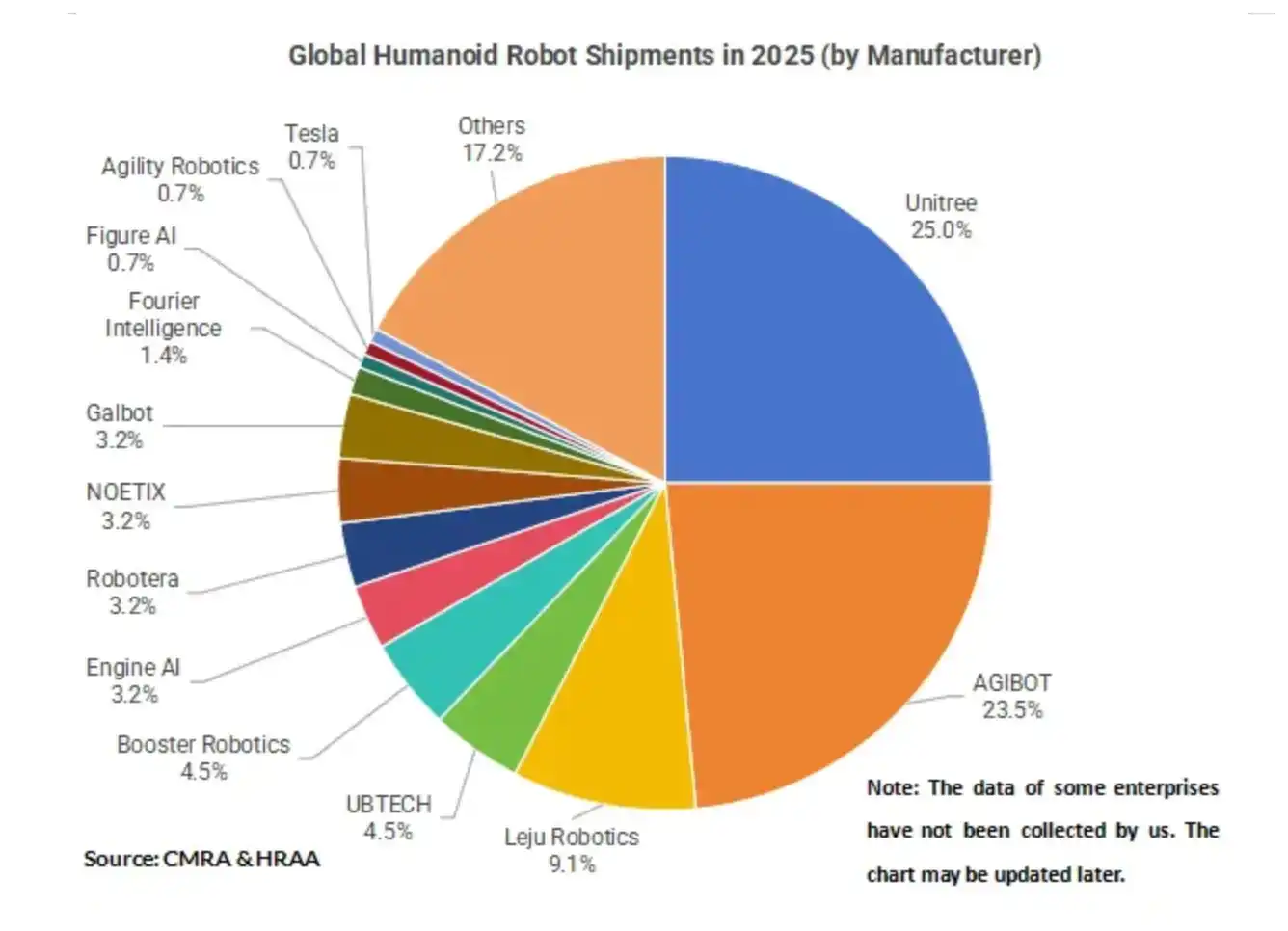

Объём продаж человекоподобных роботов Unitree особенно впечатляет в сравнении с другими компаниями. Unitree продала около 5500 человекоподобных роботов в 2025 году, став крупнейшим в мире производителем двуногих человекоподобных роботов по объёму продаж. Китайская компания AGIBot (Zhìyuán) следует за ней. Для сравнения, известные американские компании, такие как Figure AI и Agility Robotics, вероятно, продали всего несколько сотен единиц (или даже меньше).

В проспекте эмиссии заявлена 5-летняя цель — достичь годового производства 75 000 человекоподобных роботов и 115 000 четвероногих роботов. Это примерно в 14 раз больше, чем объём производства человекоподобных роботов в 2025 году. Цель амбициозна, но также подчёркивает, что отрасль находится на самой ранней стадии.

Кто покупает роботов

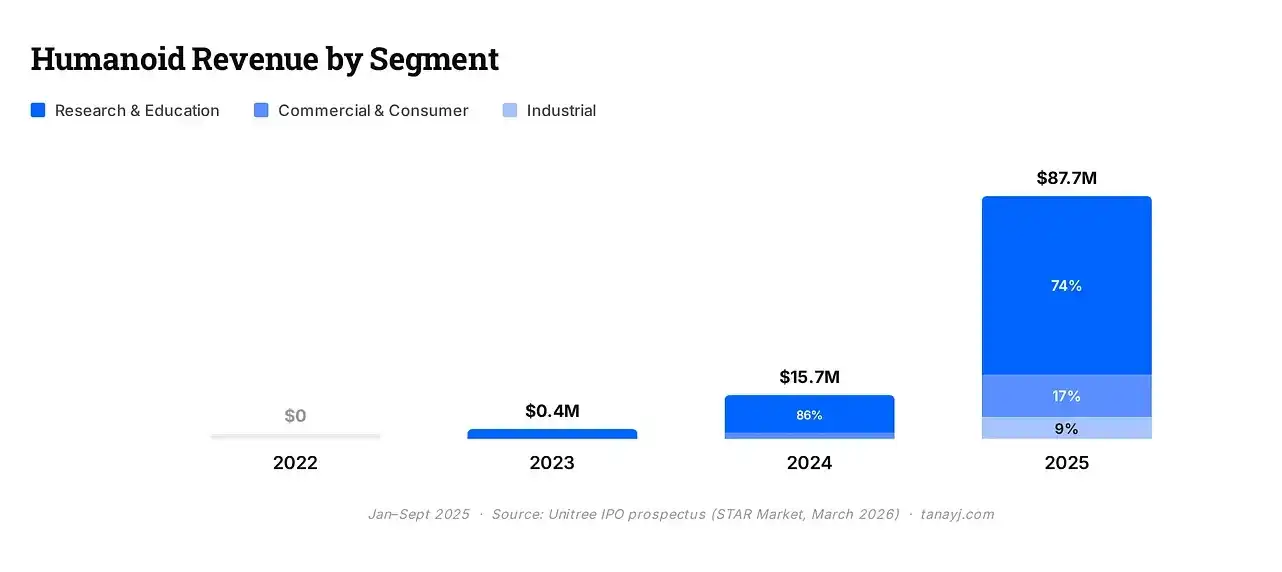

В проспекте эмиссии покупатели делятся на три категории: научные исследования и образование, коммерческое и потребительское применение, а также промышленное применение.

Суровая реальность такова, что в настоящее время большая часть спроса на человекоподобных роботов сосредоточена в сценариях научных исследований и образования.

1. Научные исследования и образование: составляют 74% выручки/объёма продаж человекоподобных роботов. С 2022 года академические покупатели были основной клиентской базой Unitree и до сих пор остаются крупнейшим источником общей выручки компании.

2. Коммерческое и потребительское применение: составляют 17% объёма продаж человекоподобных роботов. Большинство неакадемических потребителей, покупающих этих роботов, используют их для «демонстрации»: в качестве привлекающих внимание промоутеров в розничных точках, туристических достопримечательностях, на шоу и выставках. В первые девять месяцев 2025 года выручка от потребительского сегмента выросла почти вчетверо в годовом исчислении, что звучит впечатляюще, но исходная база была очень маленькой. Похоже, самое реальное применение для человекоподобного робота стоимостью 25 000 долларов сегодня — это стоять у входа в какой-нибудь магазин в Шэньчжэне и привлекать клиентов.

3. Промышленное применение: составляет лишь 9% объёма продаж человекоподобных роботов. Unitree также признаёт, что промышленное внедрение относительно ограничено из-за незрелости технологий, что отражает текущее состояние техники. В этих 9% объёма продаж около 50%-70% приходится на сценарии корпоративного приёма и экскурсионного сопровождения, поэтому в целом реальный объём продаж человекоподобных роботов, используемых для таких задач, как корпоративный приём, инспектирование и т.д., составляет лишь 3%-4%.

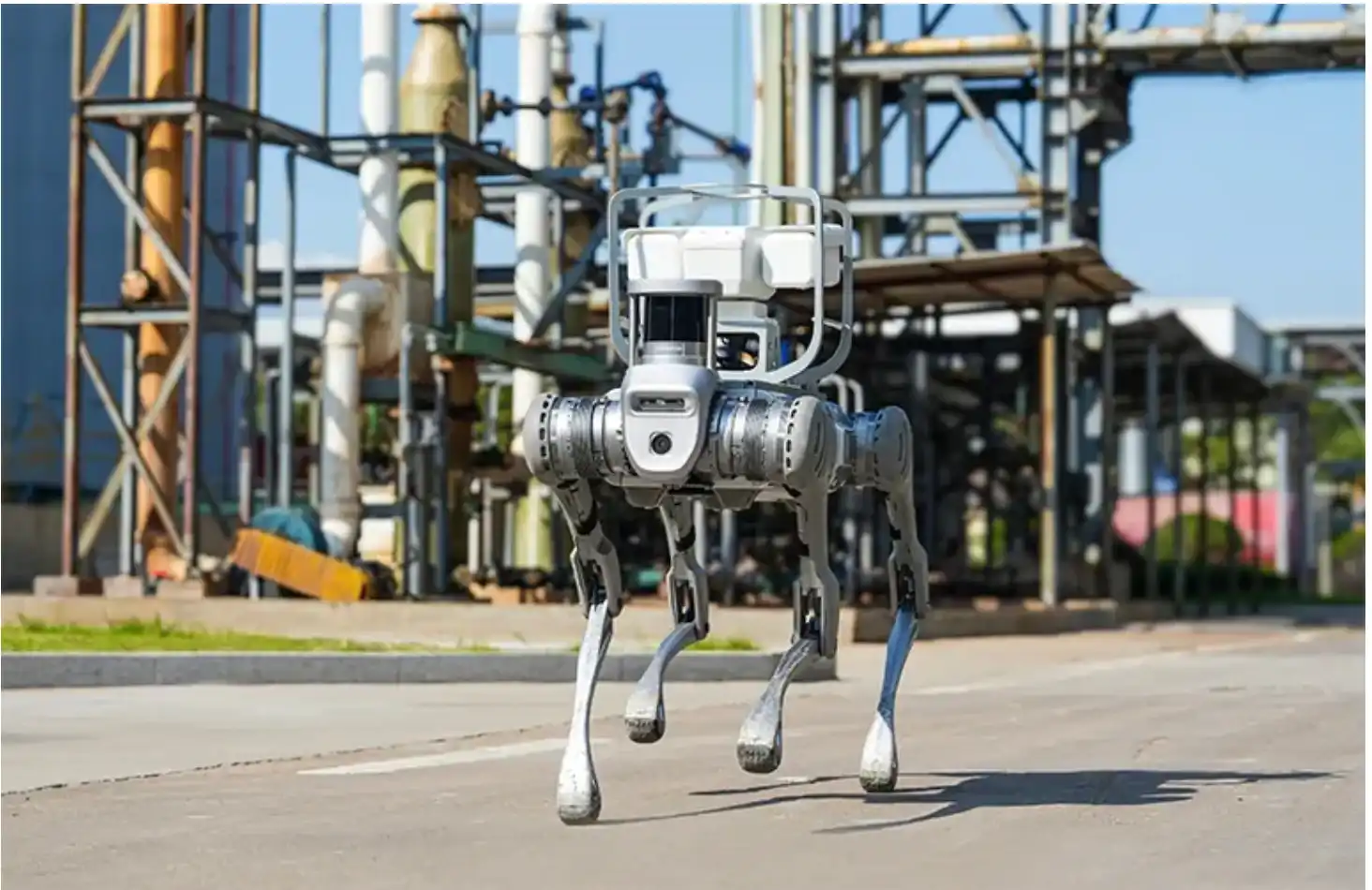

Что касается четвероногих роботов (робособак), перспективы здесь более ясные: только около трети продаж приходится на научные исследования, более 40% — на коммерческое использование, а остальное — на промышленное применение. В этой области сценарии производственного применения уже более зрелые. Клиенты включают State Grid, China Southern Power Grid, PetroChina, Sinopec, Baowu Group и JD.com (JD.com является крупнейшим клиентом Unitree). Эти компании используют четвероногих роботов для реального ежедневного инспектирования химических заводов, подстанций, шахт, трубопроводов и т.д.

Четвероногий робот Unitree используется для инспекционных работ

Вертикально интегрированная бизнес-модель

Одна из уникальных особенностей Unitree Robotics заключается в том, что она может самостоятельно проектировать и производить большинство ключевых компонентов: высокомоментные двигатели, прецизионные редукторы, энкодеры, модули приводов («суставы»), интеллектуальные контроллеры, высокоточные датчики, ловкие манипуляторы, лидары и камеры. Согласно данным McKinsey, приводные механизмы (двигатели, редукторы и системы приводов, которые приводят робота в движение) обычно составляют 40%-60% от общей стоимости материалов (BOM) человекоподобного робота.

Большинство компаний в этой области полагаются на внешние закупки, тогда как Unitree производит сама. Закупленные у сторонних производителей компоненты составляют всего около 14%-18% от её общих затрат. Она передаёт на аутсорсинг только такие универсальные компоненты, как аккумуляторные элементы, флэш-память, а также дифференцированные компоненты, такие как основные вычислительные платы.

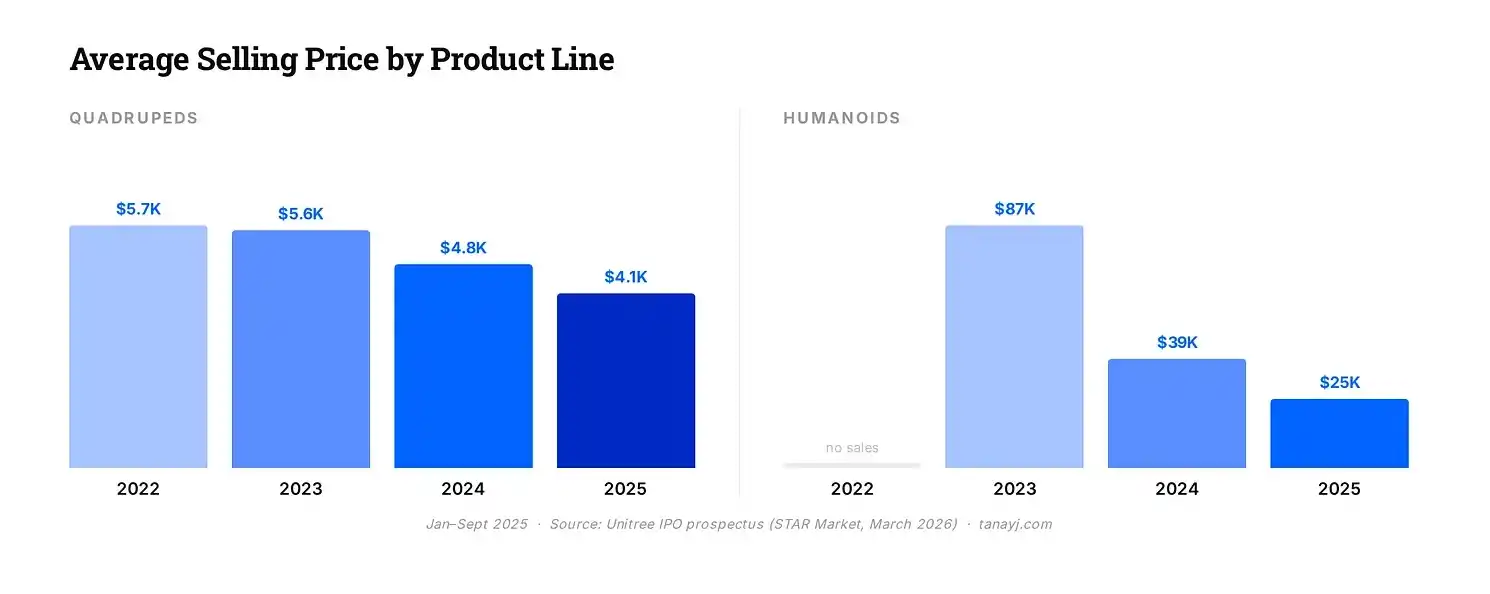

Благодаря этому себестоимость производства одного четвероногого робота снизилась примерно с 3300 долларов в 2022 году до примерно 1800 долларов к середине 2025 года — снижение на 46%. В тот же период себестоимость человекоподобного робота также снизилась с примерно 10 800 долларов до 9200 долларов.

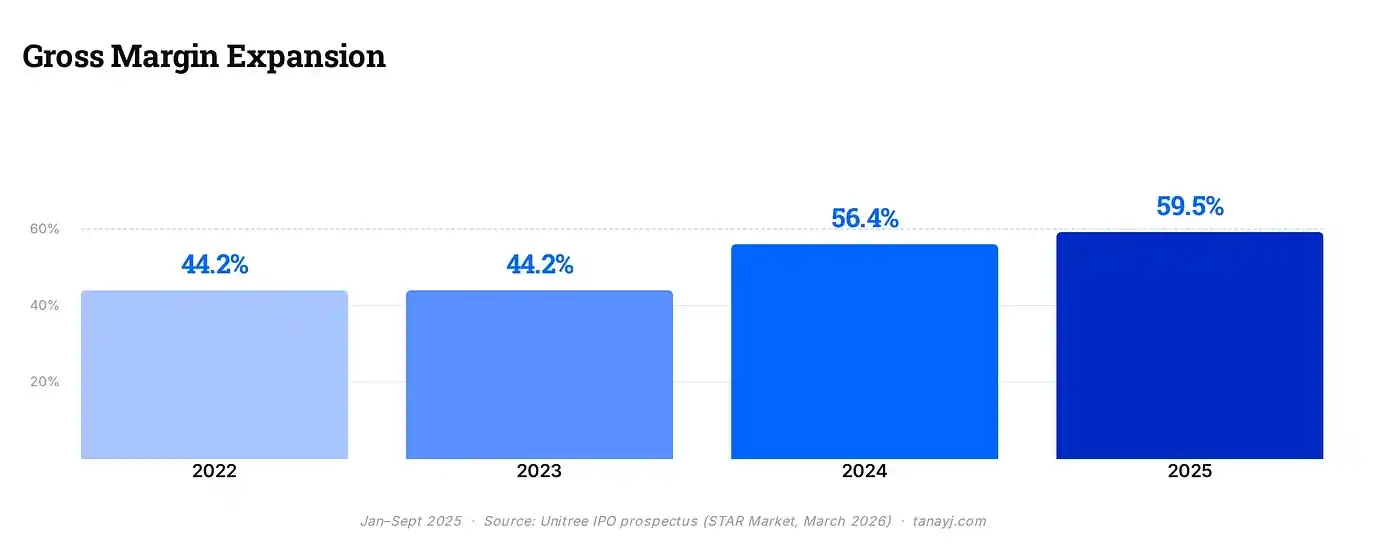

Интересно, что, как показано на графике ниже, хотя средняя цена продажи четвероногих и человекоподобных роботов с годами снижалась, благодаря их высоко вертикально интегрированной стратегии их валовая прибыль (gross margin) в течение всего периода не только не снизилась, а выросла: с примерно 45% в 2022-2023 годах до почти 60% в 2025 году.

Примечание: в 2023 году Unitree продала всего 5 человекоподобных роботов, поэтому средняя цена продажи за этот год не является репрезентативной.

Финансовый обзор

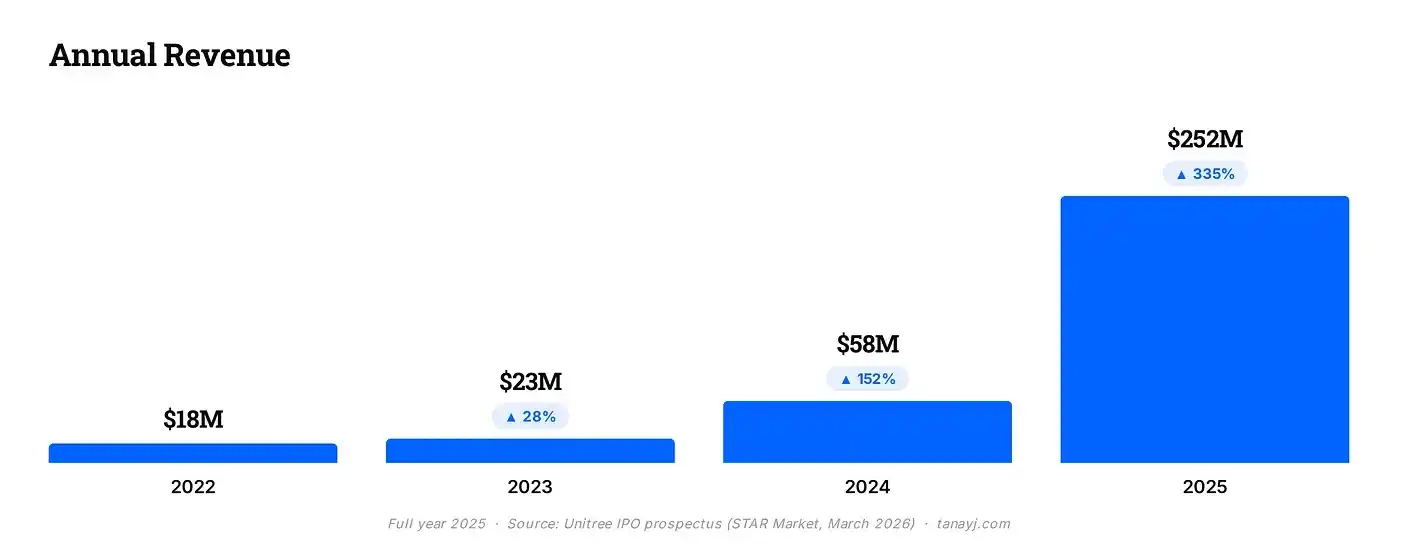

Благодаря сильному росту бизнеса по человекоподобным роботам, выручка компании резко выросла с 58 миллионов долларов в 2024 году до примерно 252 миллионов долларов в 2025 году — рост на 335%. На протяжении большей части истории компании международные продажи составляли более 55% выручки. В 2025 году внутренняя выручка Китая впервые превысила экспорт, однако абсолютный показатель экспортной выручки за рубежом все ещё удвоился в годовом исчислении.

Валовая прибыль (gross margin) приближается к 60% и в последние годы продолжает расти, как показано ниже.

Для сравнения: валовая прибыль большинства hardware-компаний составляет 30%-40%, у software-компаний она обычно достигает 70%-80%. Для компании, продающей физических роботов, валовая прибыль Unitree находится на довольно высоком уровне, что полностью объясняется их вертикально интегрированной моделью и сильной дифференциацией текущих продуктов.

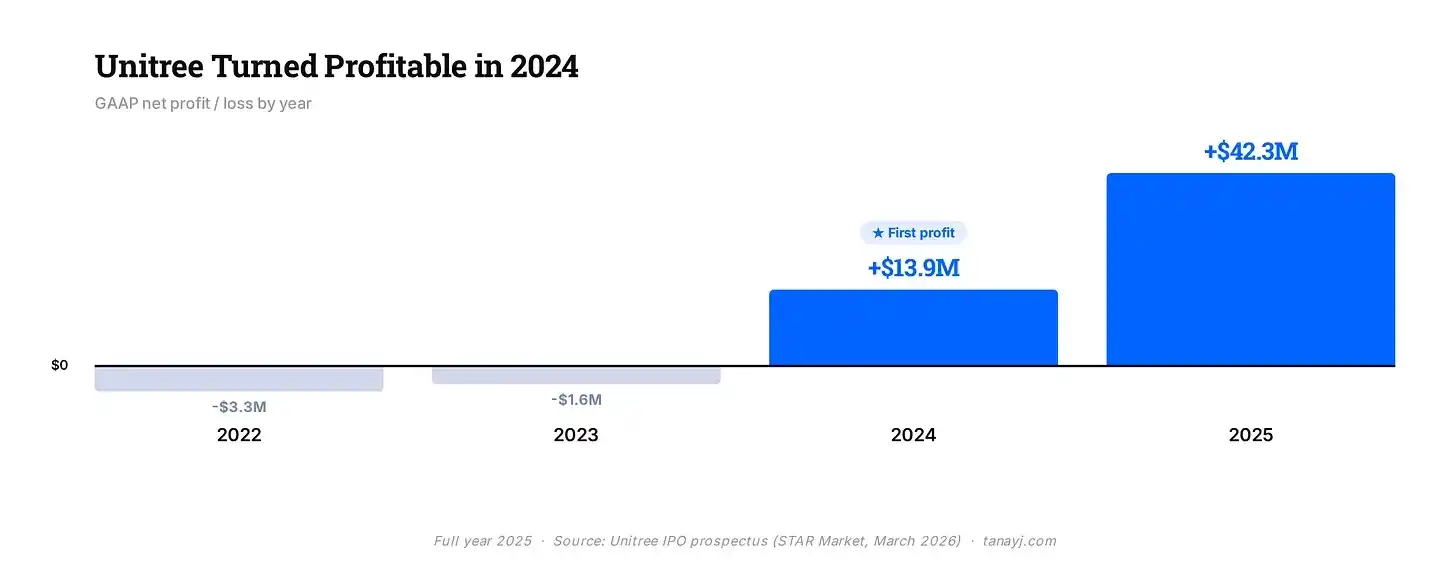

Компания стала прибыльной в 2024 году (по GAAP) с маржой прибыли около 18%, скорректированная маржа приближается к 35%.

Целевая оценка Unitree Robotics в ходе данного IPO составляет примерно 6-7 миллиардов долларов США.

Видение на уровне моделей

Unitree планирует направить почти половину средств, привлечённых в ходе IPO, на разработку программного обеспечения. Из привлечённых 6,2 миллиарда долларов около 3 миллиардов долларов выделено на обучение моделей ИИ в течение следующих трёх лет, что эквивалентно инвестициям примерно в 1 миллиард долларов в год на разработку «больших моделей для воплощённого интеллекта».

В проспекте эмиссии описаны две параллельные архитектуры моделей:

-

Первая — модель VLA (визуально-языково-действенная): Эта модель непосредственно преобразует визуальные и языковые входные данные в двигательные команды, позволяя роботу обобщать и обрабатывать незнакомые задачи без ручного написания кода.

-

Вторая — модель WMA (мировая модель + действие): Unitree рассматривает её как более перспективный вариант. Модель WMA способна строить внутреннюю симуляцию физической реальности. Робот предсказывает, что произойдёт, перед тем как действовать, вместо того чтобы учиться исключительно методом проб и ошибок.

Unitree уже выпустила начальные версии этих двух моделей. В сентябре 2025 года Unitree открыла исходный код UnifoLM-WMA-0; в январе 2026 года открыла исходный код UnifoLM-VLA-0.

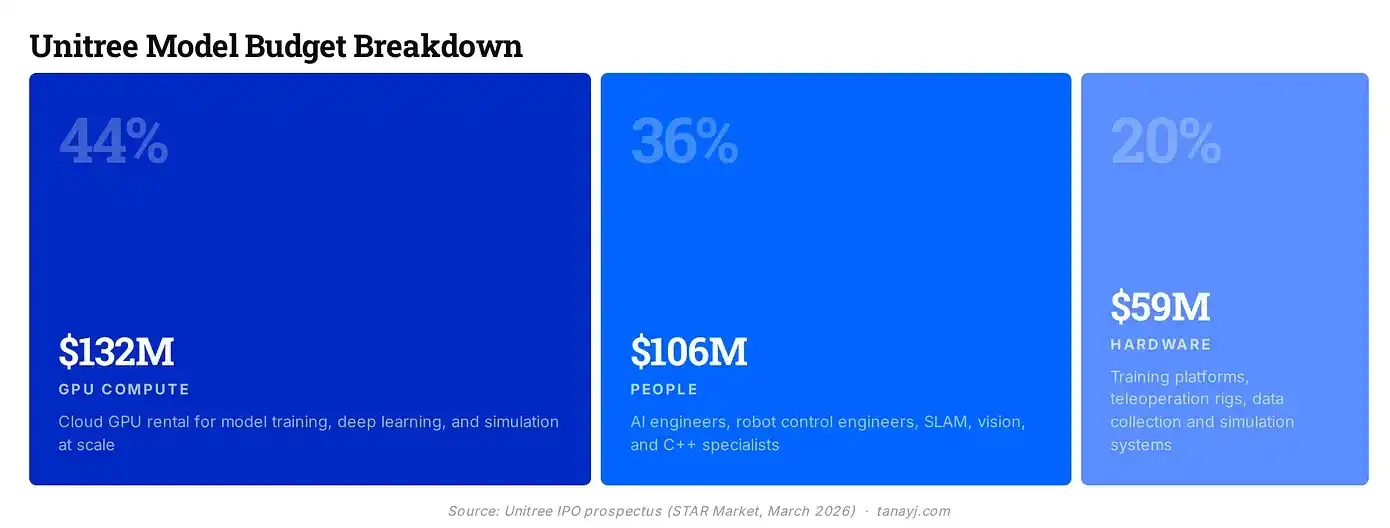

Unitree также подробно изложила примерную разбивку расходов на эту модель, как показано ниже:

Текущее лидерство Unitree в hardware неоспоримо, но компания понимает, что для поддержания устойчивого конкурентного преимущества в области робототехники, возможно, необходимо одновременно контролировать и уровень моделей: систему «мозга», которая определяет, что делает робот и как он движется. Кроме того, амбиции в области программного обеспечения также служат хеджированием против возможной товаризации (конкуренции по низким ценам) hardware. Unitree построила свой защитный ров в hardware-производстве.

Однако если приводные механизмы и модули приводов в конечном итоге станут стандартизированными компонентами, как аккумуляторы для электромобилей, то линии обороны и конкурентные барьеры в отрасли неизбежно сместятся на уровень моделей.

Заключение

Unitree Robotics обладает прибыльным hardware-бизнесом, надёжным защитным рвом в производстве и большим количеством человекоподобных роботов, чем у любой другой компании, причём по весьма конкурентоспособным ценам. Однако, как показывает реальное использование человекоподобных роботов, широкое коммерческое внедрение все ещё находится в зачаточном состоянии. «Демонстрационные» приложения доминируют в потребительском спросе, в то время как промышленное развёртывание относительно ограничено.

Unitree Robotics позволяет заглянуть в текущее состояние рынка роботов, и в будущем можно ожидать больше прорывов в области моделей, hardware и сценариев применения.

Рекомендуем прочитать: Обзор более 30 компаний по производству человекоподобных роботов: кто сможет победить в 2026 году?