Конкуренция между блокчейнами перешла на уровень «сортировки транзакций», которая напрямую влияет на спреды и глубину стакана маркет-мейкеров 🧐🧐

Потребность в «универсальных блокчейнах» оказалась мифом. Сейчас конкуренция между блокчейнами сосредоточена на двух уровнях:

1) Создание «аппчейнов» на основе существующего зрелого бизнеса, где блокчейн дополняет существующие процессы, такие как расчеты;

2) Конкуренция на уровне «сортировки транзакций».

Данная статья focuses на втором аспекте.

Сортировка напрямую влияет на поведение маркет-мейкеров. Это ключевой вопрос.

Что такое сортировка транзакций?

В блокчейне транзакции пользователей не сразу записываются в блок, а сначала попадают в «зону ожидания» (Mempool). В один момент времени там могут находиться тысячи транзакций, и именно сортировщик (Sequencer), валидатор или майнер решает:

1) Какие транзакции будут включены в следующий блок?

2) В каком порядке эти транзакции будут расположены?

Процесс «определения порядка» и есть сортировка транзакций, которая напрямую влияет на стоимость транзакций для пользователей, ситуацию с MEV, процент успешных транзакций и справедливость.

Например, при загруженности сети сортировка определяет, будет ли транзакция быстро добавлена в блок или будет бесконечно ждать в мемпуле.

Для высокочастотных трейдеров, таких как маркет-мейкеры, отмена ордера важнее, чем его успешное размещение. Приоритет обработки запросов на отмену напрямую влияет на готовность маркет-мейкеров предоставлять глубокую ликвидность.

В прошлом цикле все стремились к высокому TPS, полагая, что одной лишь скорости достаточно для улучшения расчетов в блокчейне. Но практика показала, что для маркет-мейкеров не менее важна оценка рисков.

На централизованных биржах matching строго следует принципу «приоритет цены — времени». В этой среде с высокой определенностью маркет-мейлеры могут обеспечивать глубокую ликвидность в стакане с очень узким спредом.

В блокчейне, после попадания транзакции в Mempool, ноды выбирают транзакции на основе комиссии Gas, что создает возможность для «снайпинга» существующих ордеров путем увеличения Gas.

Предположим, цена TRUMP составляет 4.5 доллара. Маркет-мейкер выставляет ордер на покупку по 4.4 доллара и на продажу по 4.6 доллара, чтобы обеспечить глубину. Но цена TRUMP внезапно обваливается до 4 долларов.

В этот момент маркет-мейкер в блокчейне хочет отменить ордер на покупку по 4.4 доллара, но высокочастотный трейдер увеличивает Gas и «снайпит» его — покупает по 4 доллара, а затем продает маркет-мейлеру по 4.4 доллара.

Следовательно, маркет-мейкер вынужден расширять спреды для снижения рисков.

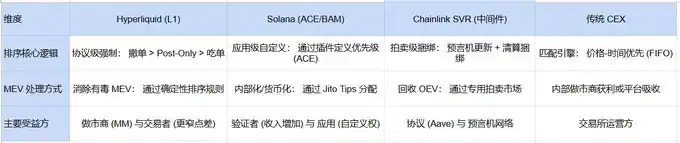

Новое поколение инноваций в сортировке aims перейти от «универсальной сортировки» к «сортировке с учетом приложений» (Application-Aware Sequencing).

Слой сортировки способен понимать намерения транзакций и сортировать их согласно предустановленным правилам справедливости, а не только на основе комиссии Gas.

1) Определение способа сортировки на уровне консенсуса

Яркий пример — Hyperliquid. На уровне консенсуса установлено, что отмена ордеров и Post-Only транзакции имеют приоритет, нарушая принцип приоритета Gas.

Для маркет-мейкера главное — успеть выйти. При резких колебаниях цены запрос на отмену всегда выполняется раньше, чем чей-либо ордер на исполнение.

Маркет-мейкеры больше всего боятся снайпинга. Hyperliquid как раз гарантирует, что отмена всегда в приоритете — при падении цены маркет-мейкер отменяет ордер, система принудительно обрабатывает отмену первой, и маркет-мейкер успешно избегает рисков.

В день обвала 10.11 маркет-мейкеры Hyperliquid оставались онлайн, спред составлял 0.01–0.05%. Причина в том, что маркет-мейкеры знали, что смогут уйти.

2) Добавление новых способов сортировки на уровне сортировки

Например, Application Controlled Execution (ACE) в Solana. BAM (Block Assembly Marketplace), разработанный Jito Labs,引入了 специализированные ноды BAM, отвечающие за сбор, фильтрацию и сортировку транзакций.

Ноды работают в доверенной среде выполнения (TEE), обеспечивая конфиденциальность данных транзакций и справедливость сортировки.

С помощью ACE DEX на Solana (такие как Jupiter, Drift, Phoenix) могут регистрировать в нодах BAM пользовательские правила сортировки. Например, приоритет маркет-мейкеров (аналогично Hyperliquid), условная ликвидность и т.д.

Кроме того, Prop AMM, такие как HumidiFi, представляют собой инновацию на уровне сортировки, использующую прямое подключение Nozomi к основным валидаторам для снижения задержек и выполнения транзакций.

При совершении сделки офчейн-сервер HumidiFi отслеживает цены на различных площадках. Оракул связывается с ончейн-контрактом и сообщает ситуацию. Nozomi действует как VIP-канал, позволяя эффективно отменять ордер до его исполнения.

3) Использование инфраструктуры MEV и приватных каналов

Chainlink SVR (Smart Value Recapture, захват стоимости через оракулы) focuses на вопросе принадлежности стоимости (MEV), создаваемой сортировкой.

Глубоко интегрируясь с данными оракулов, он переопределяет права на сортировку и распределение стоимости при ликвидационных сделках. После генерации обновления цены нода Chainlink отправляет его по двум каналам:

1) Публичный канал: отправляется в стандартный ончейн-агрегатор (в качестве резерва, но в режиме SVR будет небольшая задержка для создания аукционного окна).

2) Приватный канал (Flashbots MEV-Share): отправляется на аукционный рынок, поддерживающий MEV-Share.

Таким образом, доход от аукциона по ликвидациям в protocols кредитования, вызванным изменением цены оракула (т.е. сумма, которую готовы заплатить поисковики), больше не достается solely майнерам, а большей частью захватывается протоколом SVR.

Итог

Если TPS — это входной билет, то сейчас одного лишь TPS совершенно недостаточно. Кастомная логика сортировки, возможно, не просто инновация, а необходимый путь для вывода транзакций в блокчейн.

Возможно, это также начало превосходства DEX над CEX.