Автор: Jeff Park

Компиляция: Chopper, Foresight News

В финансовом мире каждое поколение изобретает новый инструмент, который оборачивает наихудшие инстинкты в оболочку кажущейся благоразумности.

В 80-е это были мусорные облигации, замаскированные под «демократизацию капитала»; в 90-е — долги развивающихся рынков, представленные как благородное дело помощи странам в интеграции в глобальную экономику; в 2000-е — структурированное кредитование, настолько сложное, что даже его создатели не понимали его до коллапса.

У этих «инноваций» есть общая черта: они создают искусственные решения (например, трансформацию ликвидности) для реальных проблем (например, недостаточного роста), которые в конечном итоге приводят к катастрофе из-за чрезмерного распространения.

Частное кредитование — это последняя версия этой истории и, возможно, самая коварная. Потому что, в отличие от своих предшественников, оно изначально разработано так, чтобы сделать ликвидацию до взрыва рисков полностью невидимой, и к моменту обнаружения последствия уже будут необратимы.

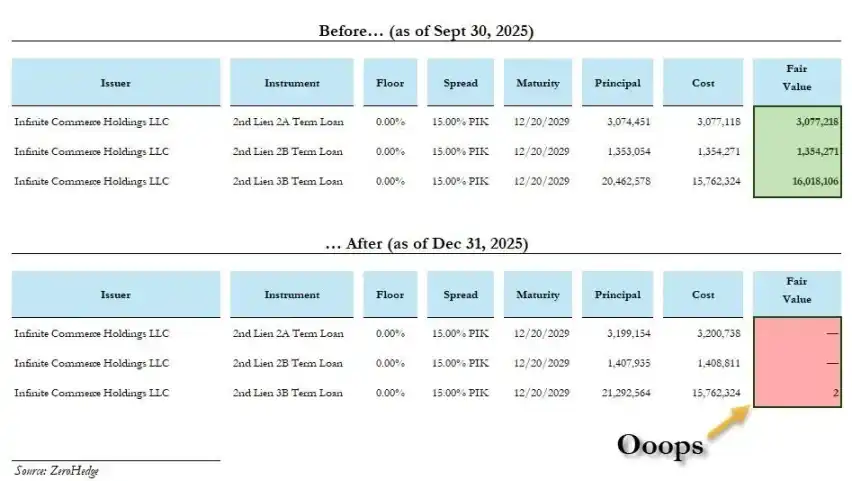

Недавно BlackRock единовременно списала две частные кредитные ссуды с 100% до 0, причем одна из них — менее чем за месяц. Это выглядит не как техническая ошибка в методах оценки, а скорее как признание ошибок в стимулах.

Как мы до этого дошли?

Кризис не корень, его создает сокрытие правды

Основная нарративная линия индустрии такова: после финансового кризиса 2008 года банки, ограниченные Базелем III, перестали рисковать кредитованием, и небанковские учреждения выступили, чтобы заполнить пустоту, обслуживая малый и средний бизнес — это был неизбежный рыночный выбор.

Более реальная ситуация: регуляторная архитектура после 2008 года не устранила риски, а активно породила теневую систему, которая берет на себя те же базовые риски, но уклоняется от регулирования, предназначенного для их сдерживания.

Рынок частного кредитования вырос с 46 миллиардов долларов в 2000 году до примерно 2 триллионов долларов сегодня. Эти деньги не появились из ниоткуда и не случайно попали в пенсионные фонды и страховые компании. Они были целенаправленно направлены учреждениям с большим объемом капитала, способным к долгосрочной блокировке и готовым принять непрозрачную оценку.

Его структура точно такая же, как во время кризиса 2008 года, с одним существенным отличием. Когда в 2008 году рухнули субстандартные кредиты, потери в основном легли на безрассудные заемные семьи и кредитующие банки; а когда рухнет частное кредитование, потери не будут иметь границ, деньги поступят от страхователей жизни, бенефициаров пенсионных фондов, то есть от обычных людей.

Такая социализация потерь, которая вызывала общественное возмущение в 2008 году, по крайней мере, предварялась периодом частной прибыли. А в частном кредитовании: прибыль идет в карман управляющих фондами, убытки социализируются и направляются на пенсионные счета учителей, медсестер, госслужащих, которые никогда не соглашались их покрывать.

style="text-align: start;">Хуже того, индустрия не удовлетворяется сбором урожая только с учреждений, теперь она нацелилась на розничных инвесторов. С 2025 года частные кредитные ETF стали очень популярны, но проблема только усугубилась: неликвидные активы, помещенные в ETF, не становятся ликвидными. Это просто переносит бомбу «наплыва погашений при невозможности продать активы» с профессиональных учреждений на брокерские счета обычных инвесторов.Это реальность, которая происходит прямо сейчас.

Ненавидящие биткоин управляющие активами все暴露или

Последние несколько лет я повсюду рекомендовал биткоин учреждениям и обнаружил удивительную закономерность: те, кто отвергает биткоин, часто狂热но продвигают частное кредитование. Это не два разных взгляда на вещи, а одно и то же мышление.

Их аргументы против биткоина звучат «благоразумно»: слишком высокая волатильность, необъяснимые просадки, невозможно оценить из-за отсутствия денежного потока.

Но подтекст таков: цена биткоина слишком честная. Она публична в реальном времени,所有人都可见, ошибка就是错误, ее не скрыть.

А частное кредитование — полная противоположность:

- Оценка меняется очень медленно, «сглаживается» управляющими фондами ежеквартально

- Нет ликвидного рынка, чтобы разоблачить ложь

- Период блокировки достаточно длинный, чтобы лица, принимавшие решения, успели повыситься, сменить работу, выйти на пенсию

Так называемые «эксклюзивные каналы проектов» — не более чем оправдание отсутствия эффективной ценовой конкуренции.

Настоящий доверительный управляющий стремится к истине, а эти управляющие активами стремятся избежать ее. Это не управление рисками, а его противоположность, замаскированная под профессионализм и полностью игнорирующая интересы бенефициаров.

Ажиотаж вокруг ИИ превращает это в системный риск

По оценкам Morgan Stanley, в 2025-2028 годах глобальные центры обработки данных потребуют капитальных затрат в размере 2,9 триллионов долларов, из которых около 800 миллиардов должны быть решены за счет частного кредитования. Это уже превратило частное кредитование из рынка займов в ключевую инфраструктуру для最重要的 технологической трансформации ближайших десятилетий.

Типичный случай: в октябре 2025 года Meta и Blue Owl завершили финансирование центра обработки данных на 270 миллиардов долларов, это крупнейшая в истории сделка частного кредитования. Деньги поступили от PIMCO, BlackRock, а в конечном итоге — от пенсионных фондов и страховых компаний.

Жестокость этого цикла: пенсионные накопления обычных трудящихся используются для финансирования автоматизации и ИИ, которые, в свою очередь, заменяют их собственную работу. Частное кредитование искажает стоимость капитала, занижает стоимость труда. Сейчас почти 500 миллиардов долларов частного кредитования ежеквартально устремляются в сферу ИИ.

Финансирование инфраструктуры ИИ и замещение питающих ее работников образуют замкнутый круг: левая рука рубит правую.

Трансформация ликвидности — это кража времени

Я не говорю, что кредитование само по себе преступно, и не говорю, что все учреждения частного кредитования плохи. Кредитование всегда было игрой вероятностей, плохие долги, дисбаланс были в каждую эпоху.

Ключевое отличие: кто真正承担损失?

- Если банк выдал плохой кредит, он находится в его собственном балансе, регулируется, сталкивается с набегами вкладчиков и обнулением капитала, несет реальные риски;

- Управляющий частным кредитованием зарабатывает на performance fee (вознаграждение за результат), это стимул «подталкивать вас делать ставки», а не «подталкивать вас ответственно выигрывать».

К тому времени, как кредит обнулится, управляющий уже заработает достаточно денег.

Каждый финансовый инжиниринг в конечном итоге сводится к一个问题: кто承担没人想要的成本?

«Гениальность» частного кредитования заключается в том, что оно отвечает на этот вопрос невероятно «элегантно»:

Доходы текут вверх и назад: к тем, кто старше, уже на пенсии, бенефициарам долгосрочного капитала

Издержки текут вниз и вперед:压低工资、冻结招聘、延缓投资, искажая стоимость капитала для всей экономики

Частное кредитование — это кража времени.

Это давно известная в финансовой сфере трансформация ликвидности, только лишенная маскировки.

Они через инструменты, которые не могут выбрать, по ценам, которые не могут предвидеть,承担着自己无需承担的风险。

Период блокировки гарантирует, что они не могут выйти, отсутствие публичной оценки гарантирует, что они не могут протестовать, а механизм квартального сглаживания оценки гарантирует, что когда окончательный счет будет предъявлен, ответственных уже не найти.

Это выглядит не как грабеж, а как «стабильный доход», их почти невозможно отличить до момента краха. Хотя эта история стара, новизна заключается в ее масштабе, низкой прозрачности и ошеломляющем успехе этого класса активов, построенного на иллюзии безопасности, который заставил поверить даже самых осторожных управляющих капиталом в мире.

В мире нет ни одного класса активов, который мог бы три месяца подряд оцениваться в 100%, а затем в одночасье обнулиться.

Если это не кража, то я не знаю, что тогда кража.