Автор: Prathik Desai

Оригинальное название: The Maturity Fingerprint

Компиляция и редактирование: BitpushNews

Все считают, что стейблкоины растут. Всего за два года их оборотное предложение более чем удвоилось, а скорректированный объем торгов вырос более чем в три раза. В прошлом месяце месячный скорректированный объем торгов стейблкоинами достиг рекордного уровня. Некоторые скептически относятся к этим цифрам, а крипто-Твиттер (CT) празднует.

Но одни только цифры плохо объясняют природу роста. Не менее важен контекст, в котором происходит рост: кто использует стейблкоины, для каких целей и меняются ли модели использования. Allium позволил нам ознакомиться с их последним отчетом об инфраструктуре стейблкоинов — «Стейблкоины: восход новых платежных рельсов». Это очень важный отчет, поскольку графики показывают, что использование стейблкоинов смещается с обеспечения низкозатратных кросс-бордерных переводов на поддержку общего коммерческого и поставщического платежного взаимодействия между предприятиями.

Большинство текущих дебатов о стейблкоинах сосредоточено на том, являются ли они финансовыми продуктами (такими как банки, обертки казначейских облигаций, носители дохода) или просто платежной инфраструктурой. Споры на уровне политики о процентах по стейблкоинам исходят из предположения, что стейблкоины в основном являются финансовым инструментом. Но данные в отчете дают другой ответ: недавний состав активности стейблкоинов все больше напоминает платежный рельс, а не сберегательный продукт.

Это точно повторяет модель эволюции, которую мы видели в сети автоматизированной клиринговой палаты (ACH): от первоначальной замены бумажных чеков в выплате зарплат до становления основой для общего коммерческого, B2B-платежного и потребительскогоbill-платежного взаимодействия.

В этой статье, используя данные отчета Allium об инфраструктуре стейблкоинов, мы объясним, почему это меняет наше представление о том, куда движутся стейблкоины.

Дифференциация скорости

С января 2024 года оборотное предложение стейблкоинов (общее предложение за вычетом необоротного предложения) выросло более чем на 100%. За тот же период скорректированный объем торгов (исключающий накрутку, внутренние переводы между субъектами и кольцевые переводы) вырос на 317%.

На этапе накопления любого нового актива рост предложения обычно опережает рост использования. А по мере созревания актива рост использования опережает рост предложения. Это происходит потому, что держатели актива тратят его больше. Здесь, поскольку скорость роста скорректированного объема торгов значительно опережает рост оборотного предложения стейблкоинов, это указывает на то, что стейблкоины созревают из средства сбережения стоимости в более предпочтительное средство обмена или передачи стоимости.

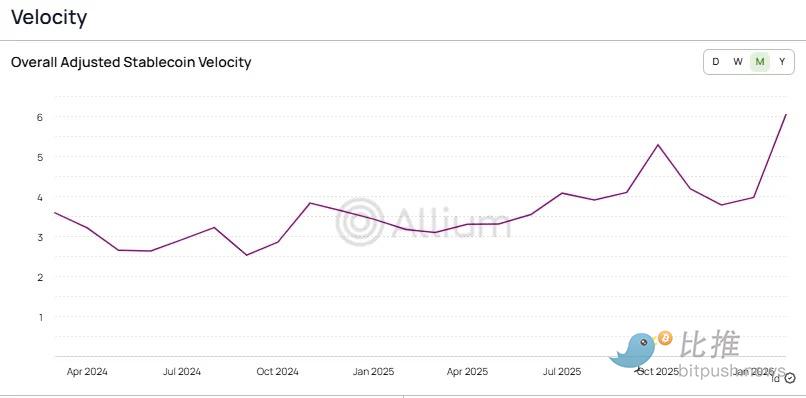

Этот сдвиг отражается в скорости обращения (Velocity) стейблкоинов, рассчитываемой как скорректированный объем торгов, деленный на оборотное предложение.

Allium

Скорость обращения стейблкоинов за последние два года увеличилась с 2.6x до более чем 6x, что отражает, что каждый доллар предложения стейблкоинов теперь оборачивается в 2.3 раза активнее, чем в январе. Если сравнить это с традиционными платежными рельсами, становится ясно, насколько зрелым стало использование стейблкоинов.

Другой показатель, подтверждающий зрелость использования стейблкоинов, — это количество транзакций. Он наименее подвержен влиянию шума крупных сумм. Следовательно, когда рост количества платежных транзакций опережает рост суммы транзакций, это указывает на то, что средний размер платежа уменьшается. Такое поведение является типичным признаком укоренения платежного рельса, а не экспериментального инструмента для перемещения между биржами.

Это поднимает вопрос: кто совершает эти платежи и за что платит?

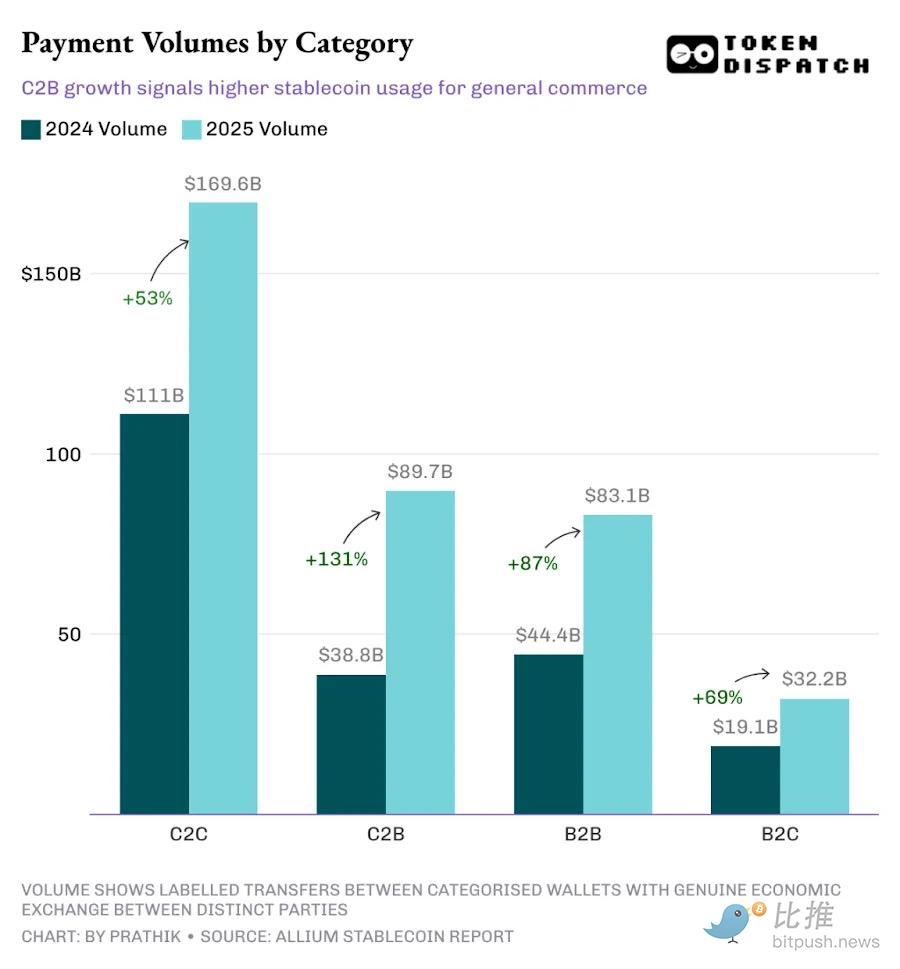

В 2025 году категория «потребитель-потребитель» (C2C) оставалась крупнейшим каналом, опережая «потребитель-бизнес» (C2B), «бизнес-бизнес» (B2B) и «бизнес-потребитель» (B2C). Но ее темпы роста были самыми медленными среди четырех категорий.

Замедление роста C2C further подтверждает зрелость использования стейблкоинов, поскольку переводы между физическими лицами — это самый простой вариант использования. Для них не требуется интеграция с merchants, инструменты для инвойсов, API, и барьеры для внедрения невелики. Это типичная отправная точка для каждой новой платежной технологии.

Когда десять лет назад в Индии запустили Unified Payments Interface (UPI), первыми присоединились розничные пользователи, движимые кэшбэком и другими стратегиями привлечения. Я помню, как использовал Google Pay (изначально запущенный в Индии под названием Tez) для переводов между двумя своими собственными счетами только потому, что это приносило мне кэшбэк в один доллар. Только когда появились коммерческие инструменты, отчетность и специализированные системы аудио-устройств подтверждения платежа (колонки), к системе начали подключаться магазины и учреждения.

По мере созревания инфраструктуры коммерческие кейсы начали поглощать долю рынка. И эта трансформация, похоже, происходит.

Высокий рост C2B указывает на то, что все больше пользователей используют стейблкоины для общих коммерческих платежей, подписок и платежей merchants. В то же время рост B2B указывает на то, что коммерческие контрагенты начинают adopt стейблкоины в обработке инвойсов, платежах по цепочке поставок и финансовых операциях. Оба этих темпа роста (131% для C2B и 87% для B2B) превышают общий темп роста платежей в 76%, что указывает на расширение доли коммерческих платежей.

Если совместить растущий объем транзакций C2B со средним чеком (AOV) для C2B, который снизился с 456 долларов до 256 долларов, это намекает на тенденцию использования стейблкоинов для регулярных закупок.

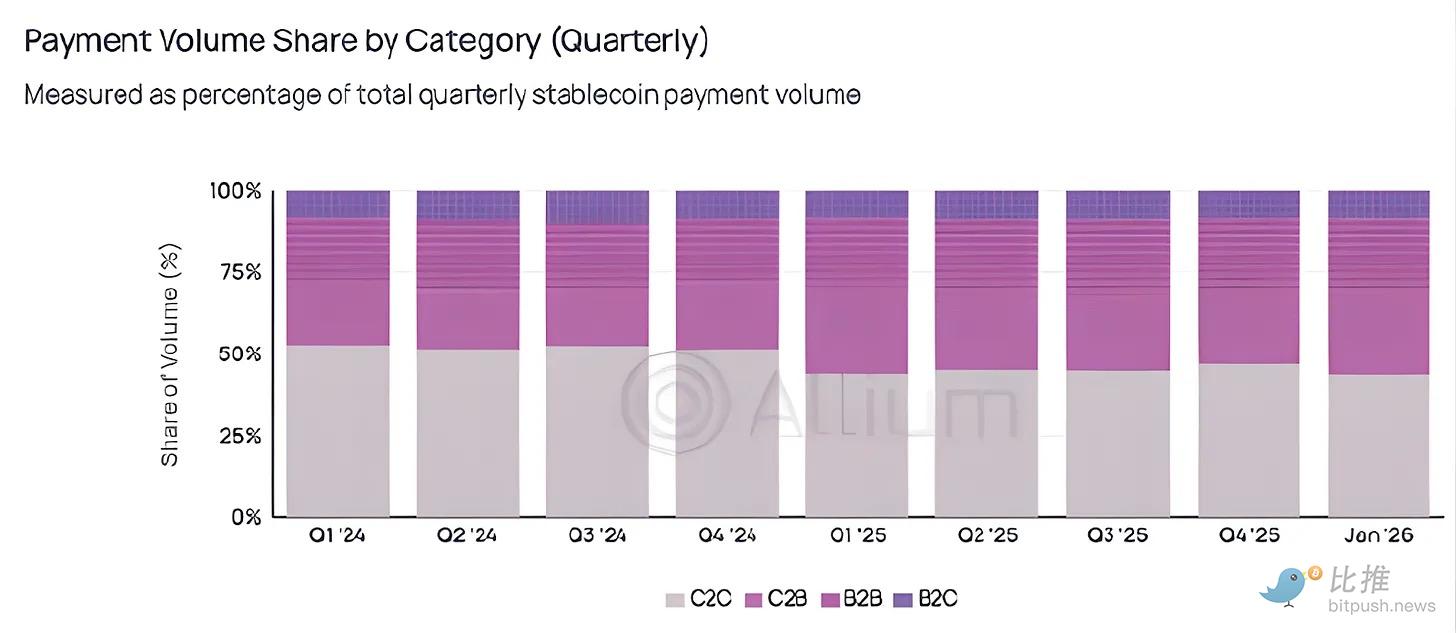

Хотя с точки зрения абсолютных значений категория peer-to-peer (P2P) все еще доминирует, она скоро уступит позиции. Квартальные данные о долях делают эту ротацию еще более очевидной.

Allium

После того как в первом квартале 2025 года доля C2C упала ниже отметки в половину, она никогда больше не превышала 50% от общего объема платежей.

Мир, кажется, перерастает экспериментальную фазу использования стейблкоинов для низкорисковых, низкочастотных p2p-переводов и переходит к их последовательному использованию для высокочастотных платежей.

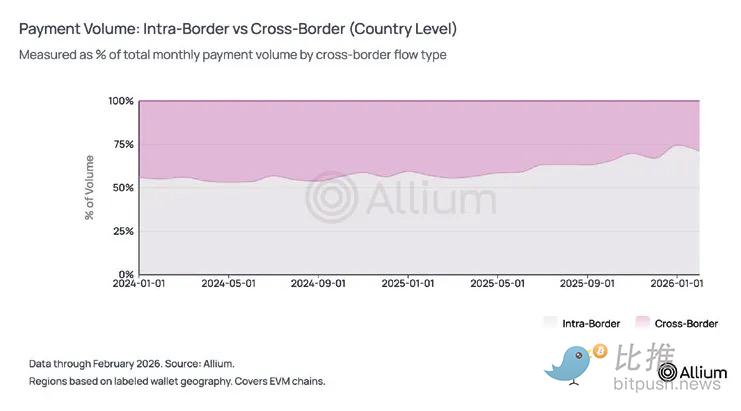

Когда я только начал отслеживать adoption стейблкоинов, одним из основных нарративов в их поддержку было то, как они позволяют осуществлять кросс-бордерные денежные переводы и потенциально могут颠覆 Western Union, позволив работникам из развитых экономик отправлять деньги домой. Но данные говорят об обратном.

В настоящее время около трех четвертей платежей стейблкоинами происходят внутри стран. За последний год доля объема кросс-бордерных платежей на страновом уровне в общем объеме платежей снизилась с 44% до примерно 25-29%. На региональном уровне 84% платежного потока остается в том же географическом регионе.

Allium

Основываясь на всех наших предыдущих графиках, очевидно, что стейблкоины конкурируют не со SWIFT в сфере международных расчетов. Вместо этого, включая 74% доминирования внутренних платежей, снижение среднего размера транзакции, выплату зарплат и растущие кейсы использования инвойсов, показатели B2B указывают на то, что стейблкоины конкурируют с внутренними платежными рельсами, такими как ACH.

Для справки: платежи B2B через ACH в 2025 году выросли примерно на 10%, в то время как платежи B2B стейблкоинами за тот же период выросли на 87%. Я понимаю, что абсолютные масштабы еще несопоставимы, и мы должны учитывать эффект низкой базы стейблкоинов. Тем не менее, этот рост нельзя игнорировать.

Перспективы

Долгое время я считал кросс-бордерные переводы и p2p-транзакции основными драйверами adoption стейблкоинов.

Представление о том, что сын в Индии получает доллары от семьи в Дубае в банковский выходной без того, чтобы посредники забирали 7-8% комиссии, — этот нарратив был очень привлекательным. Эта история до сих пор актуальна, но, возможно, она больше не является основной.

Интересно, что нарратив о внутреннем потребительском использовании незаметно и быстро обогнал все остальное. Доля C2C не возвращалась к 50% уже больше года, и этот показатель, кажется, никогда не был популярен в дискуссиях крипто-сообщества. Но именно этот показатель знаменует переход стейблкоинов от «криптопродукта» к «финансовой инфраструктуре» — делая возможными транзакции между потребителями и businesses или между businesses themselves.

Также стоит отметить, что объем платежных транзакций, отмеченный Allium, основан на анализе кошельков, которые они могут охватить, идентифицировать и пометить. Хотя эти данные показывают, что платежные транзакции составляют всего 2-3% от общего скорректированного объема торгов стейблкоинами, это следует рассматривать как нижнюю границу — несомненно, существует множество кошельков, которые Allium не охватывает.

В дальнейшем я буду внимательно следить за двумя вещами: продолжит ли доля C2B и B2B расти и сможет ли средний размер транзакции оставаться низким в ближайшие кварталы. Если эти тенденции сохранятся даже в условиях спада на крипторынке, это будет означать, что платежная инфраструктура стейблкоинов действительно начала отделяться от спекулятивного цикла крипторынка.

Twitter:https://twitter.com/BitpushNewsCN

Группа общения в TG比推:https://t.me/BitPushCommunity

Подписка в TG比推: https://t.me/bitpush