Автор: @intern_cc, крипто-KOL

Компиляция: Felix, PANews

Крипто-опционы имеют все шансы стать знаковым финансовым инструментом 2026 года благодаря слиянию трех трендов: сокращению традиционной доходности DeFi из-за «доходного апокалипсиса», появлению нового поколения упрощенных «продуктов для начинающих», которые абстрагируют опционы до интерфейса с одной кнопкой, а также приобретению институционального признания через покупку Coinbase Deribit за $2.9 млрд.

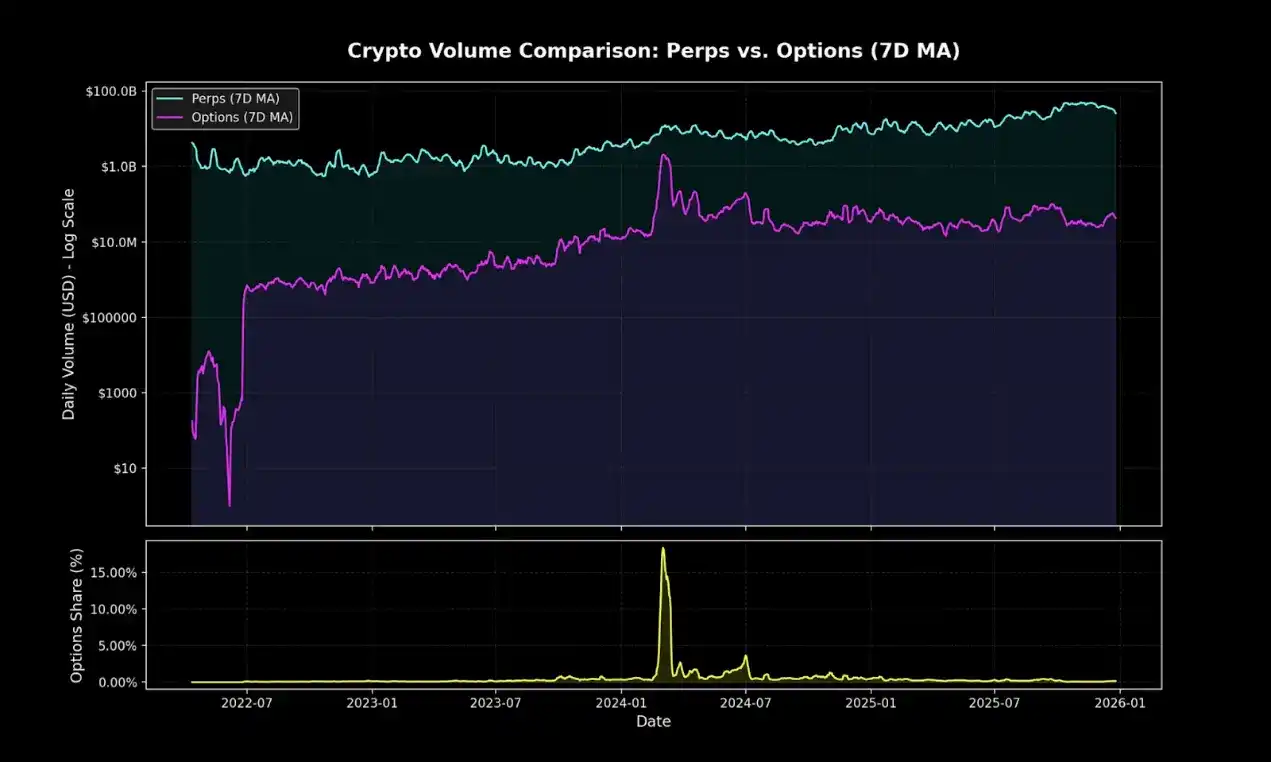

Несмотря на то, что ончейн-опционы в настоящее время составляют лишь небольшую долю объема торгов крипто-деривативами, перпетуальные контракты по-прежнему абсолютно доминируют на рынке. Этот разрыв в точности повторяет ситуацию с опционами в TradFi до их популяризации через Robinhood.

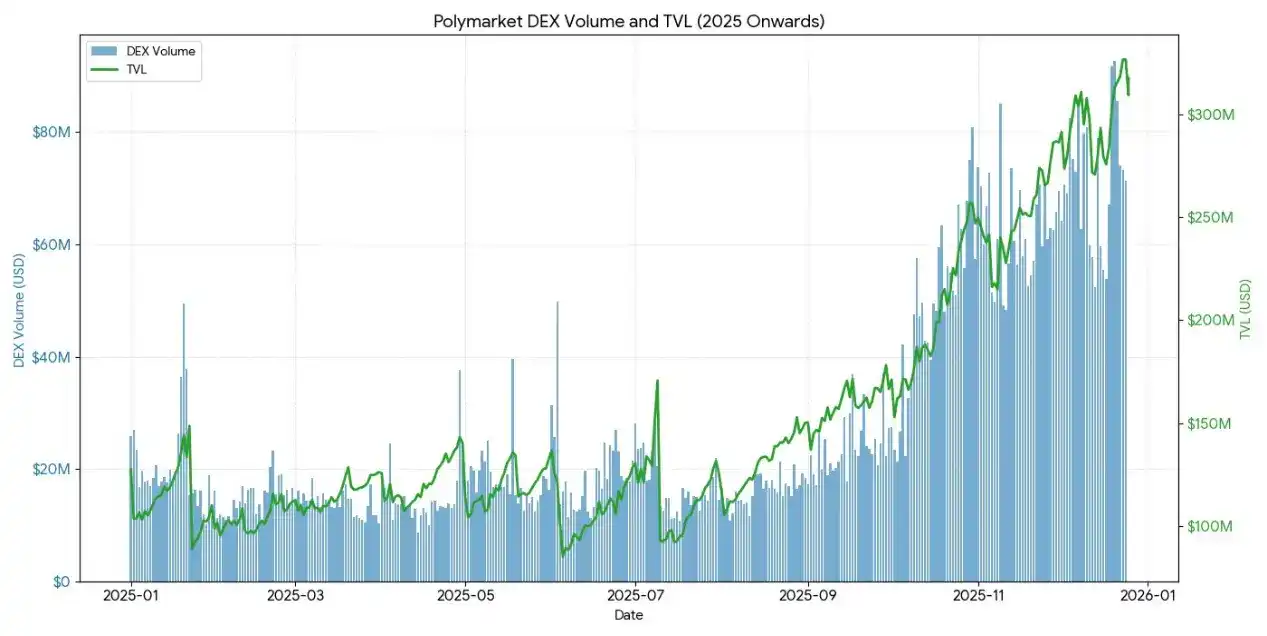

Polymarket, переупаковав бинарные опционы и подкрепив это отличным маркетингом, обработал в 2024 году $90 млрд торгов. Если спрос розничного рынка на вероятностные ставки подтвердится, сможет ли DeFi для опционов совершить такой же структурный сдвиг? Когда инфраструктура и динамика доходности наконец совпадут, исполнение определит, прорвутся ли опционы через барьер или останутся нишевым инструментом.

Конец пассивного дохода

Чтобы понять, почему крипто-опционы могут взорваться в 2026 году, сначала нужно понять: что умирает.

Почти пять лет экосистема криптовалют процветала, и рыночные аналитики ретроспективно называют это золотым веком «ленивой доходности», когда участники могли получать значительную доходность с поправкой на риск при почти полном отсутствии сложных операций или активного управления. Типичными представителями были не сложные опционные стратегии, а такие простые и грубые арбитражные методы, как фарминг выпусков токенов, луповые стратегии и торговля базисом на перпетуальных контрактах.

Торговля базисом была ядром крипто-доходности. Ее механизм кажется простым, но это не так: из-за структурного предпочтения розничных инвесторов длинным позициям, «быки» должны платить «медведям» финансирование для поддержания своих позиций. Покупая спот и продавая перпетуальные контракты, проницательные участники создавали дельта-нейтральные позиции, не подверженные ценовым колебаниям, и при этом получали 20-30% годовых.

Однако, бесплатного сыра не бывает. С одобрением биткоин-ETF на спот, приход традиционных финансовых институтов принес промышленные масштабы эффективности. Уполномоченные участники и хедж-фонды начали исполнять эту торговлю миллиардами долларов, сжимая спреды до уровня ставок по казначейским облигациям плюс скудная премия за риск. К концу 2025 года этот «пузырь» рассеялся.

«Кладбище» протоколов DeFi-опционов

- Hegic запустился в 2020 году с инновацией пул-к-пулу, но дважды закрывался на раннем этапе из-за багов в коде и недостатков в теории игр.

- Рыночная капитализация Ribbon упала с пика в $3 млрд, в основном из-за обвала рынка в 2022 году и последующего стратегического перехода на Aevo, осталось лишь около $2.7 млн, которые были взломаны в 2025 году.

- Dopex внедрил опционы с концентрированной ликвидностью, но в конечном итоге рухнул из-за неконкурентоспособных опционных продуктов, создаваемых моделью, низкой эффективности использования капитала и неустойчивой токеномики в условиях сурового макро-медвежьего рынка.

- Opyn отказался от розницы в пользу инфраструктуры, осознав, что торговля опционами по-прежнему управляется институтами.

Модель провала была高度 последовательной: амбициозные протоколы не могли одновременно запустить ликвидность и упростить пользовательский опыт.

Парадокс сложности

Ирония в том, что опционы, которые теоретически безопаснее и точнее соответствуют намерениям пользователя, менее популярны, чем более рискованные и сложные по механике перпетуальные контракты.

Перпетуальные контракты кажутся простыми, но их механизм чрезвычайно сложен. При каждом обвале рынка люди становятся жертвами ликвидаций или автоматического deleveraging'а, и даже крупные трейдеры не всегда понимают логику работы перпетуальных контрактов.

Опционы, напротив, полностью лишены этих проблем. Покупая колл-опцион, вы рискуете только премией, максимальные убытки известны до входа. Однако перпетуальные контракты доминируют только потому, что «сдвинуть ползунок до 10x» всегда проще, чем «рассчитать дельта-скорректированную экспозицию».

Ловушка мышления перпетуальных контрактов

Перпетуальные контракты заставляют вас платить кросс-спред и дважды за сделку.

Они могут уничтожить вас даже при хеджированной позиции.

Они зависят от пути, вы не можете открыть позицию и «забыть».

Но даже если вы считаете, что краткосрочные розничные направленные потоки все еще будут идти в перпетуальные контракты, опционы все же могут занять доминирующую долю рынка в большинстве нативных ончейн-финансов. Это более гибкий и мощный инструмент для хеджирования рисков и создания дохода.

Взглянув на следующие пять лет, ончейн-инфраструктура постепенно эволюционирует в бэкенд для уровня распределения, с охватом, более широким, чем в традиционных финансах.

Сегодняшние инновационные хранилища, такие как Rysk и Derive, представляют собой начальную волну этого перехода, предлагая структурированные продукты, выходящие за рамки базового leverage или пулов кредитования. Проницательным аллокаторам активов понадобятся более богатые инструменты для управления рисками, работы с волатильностью и комбинирования доходности, чтобы полностью использовать децентрализованную экосистему.

TradFi доказывает: розница любит опционы

Революция Robinhood

Взрывной рост розничной торговли опционами в TradFi предоставляет дорожную карту. Robinhood запустил беспроцентную торговлю опционами в декабре 2017 года, вызвав отраслевую трансформацию, которая достигла кульминации в октябре 2019 года, когда Charles Schwab, TD Ameritrade и Interactive Broker отменили комиссии в течение нескольких дней.

Влияние было огромным:

- Доля розничной торговли опционами в США взлетела с 34% в конце 2019 года до 45-48% в 2023 году.

- В 2024 году общий годовой объем контрактов на опционы, клирингованных OCC, достиг рекордных 12.2 млрд, пятый год подряд устанавливая рекорд.

- В 2020 году мемные акции составляли 21.4% от общего объема торгов опционами.

Взрывной рост опционов с истечением в ноль дней (0DTE)

0DTE показали интерес розницы к краткосрочным, высоко-выпуклым ставкам. Доля торгов 0DTE в объеме опционов на S&P 500 выросла с 5% в 2016 году до 51% в четвертом квартале 2024 года, при среднем дневном объеме более 1.5 млн контрактов.

Их привлекательность очевидна: меньше капитала, отсутствие overnight-риска, встроенное плечо свыше 50x и дневной цикл обратной связи, который инсайдеры называют «дофаминовой торговлей».

Выпуклость и определенный риск

Нелинейная структура выплат по опционам привлекает направленных трейдеров, ищущих асимметричную доходность. Покупатель колла может рискнуть всего $500 премии при потенциальной прибыли свыше $5000. Спрэды позволяют более точную настройку стратегии: максимальный убыток и прибыль известны до входа.

Продукты для начинающих и инфраструктура

Абстракция как решение

Новое поколение протоколов решает проблему сложности, полностью скрывая опционы за простыми интерфейсами, называемыми в отрасли «дофаминовыми приложениями».

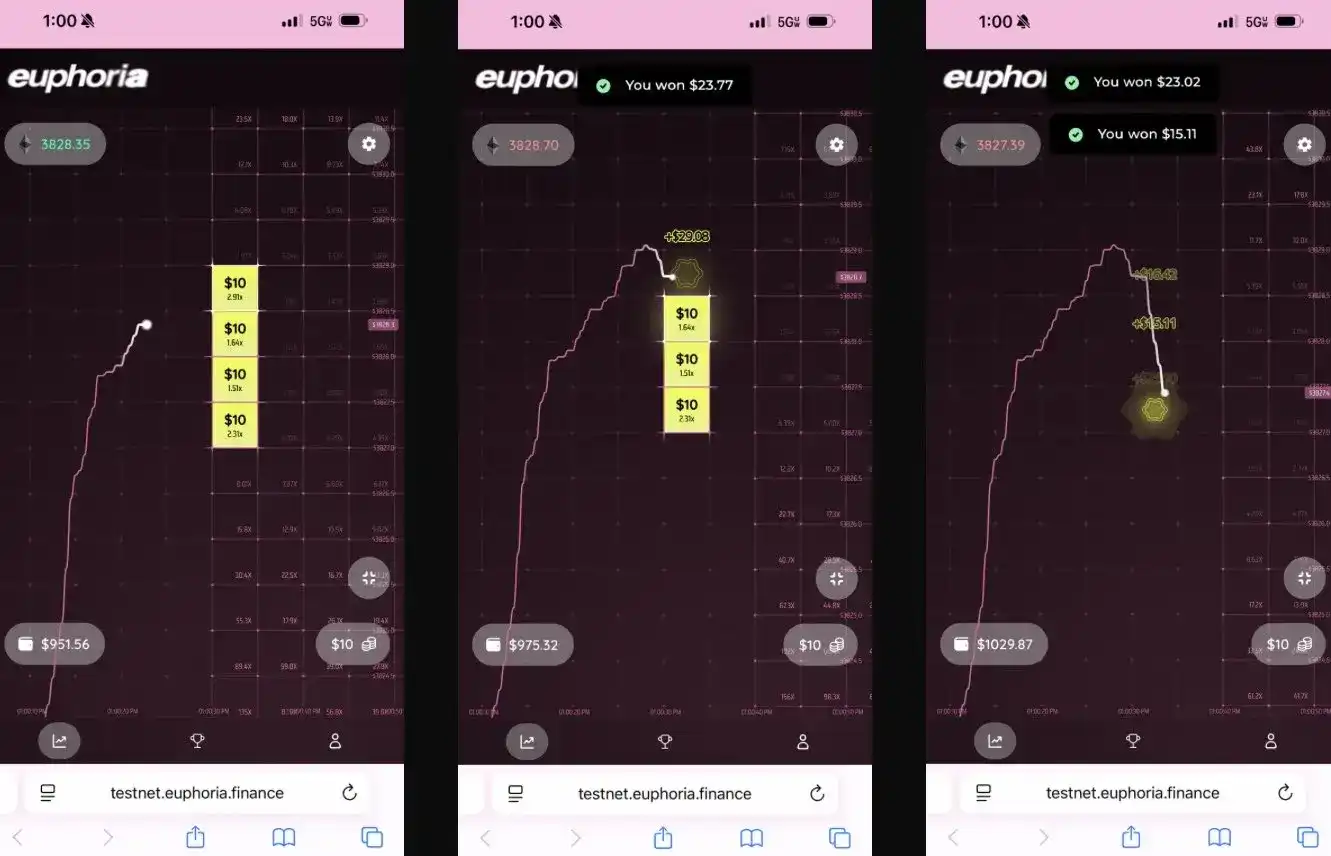

Euphoria привлекла $7.5 млн seed-раунда с радикальной идеей упрощения: «Вы просто смотреть на график, видите движение ценовой линии и кликаете на клетку сетки, куда, по вашему мнению, цена пойдет следующей». Никаких типов ордеров, управления маржой или греков — просто правильная направленная ставка, исполняемая на CLOB.

Построено на суб-миллисекундной инфраструктуре MegaETH.

Взрыв预测 рынков подтвердил концепцию упрощенных стратегий:

- Polymarket обработал свыше $90 млрд торгов в 2024 году, с пиком в 314.5k активных трейдеров в месяц.

- Еженедельный объем торгов на Kalshi стабилизировался на уровне свыше $1 млрд.

Обе платформы структурно идентичны бинарным опционам, но концепция «прогнозирования» превращает стигму азартных игр в коллективный разум.

Как прямо признал Interactive Brokers, их预测 контракты — это «бинарные опционы ‘预测 рынки’».

Урок: розница не хочет сложных финансовых инструментов, она хочет простые, понятные вероятностные ставки с ясным исходом.

Состояние DeFi-опционов в 2025 году

По состоянию на конец 2025 года, экосистема DeFi-опционов переходит от экспериментальных designs к более зрелым, композитным рыночным структурам.

Ранние framework выявили множество проблем: ликвидность, фрагментированная по разным датам экспирации, расчеты через оракулы, добавляющие задержки и риски манипуляций, полностью коллатеризированные хранилища, ограничивающие масштабируемость. Это стимулировало переход к моделям пулов ликвидности, структурам перпетуальных опционов и более эффективным маржинальным системам.

Текущие участники DeFi-опционов в основном представлены розничными инвесторами, ищущими доходность, а не институтами, ищущими хеджирование. Пользователи рассматривают опционы как инструмент пассивного дохода, продавая покрытые коллы для получения премии, а не как инструмент переноса волатильности. Когда волатильность рынка усиливается, хранилища сталкиваясь с риском adverse selection из-за отсутствия инструментов хеджирования, что приводит к постоянной неэффективности и оттоку TVL.

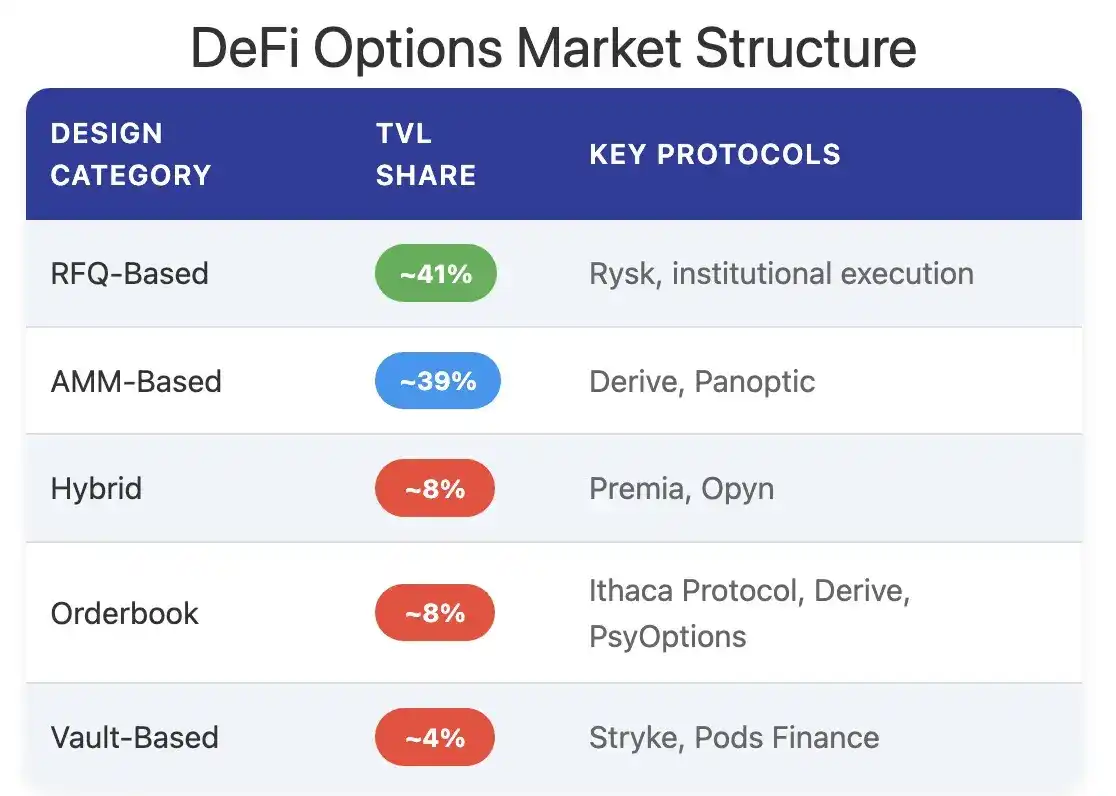

Архитектура протоколов вышла за рамки традиционных моделей с экспирацией, породив новые парадигмы в ценообразовании, ликвидности и т.д.

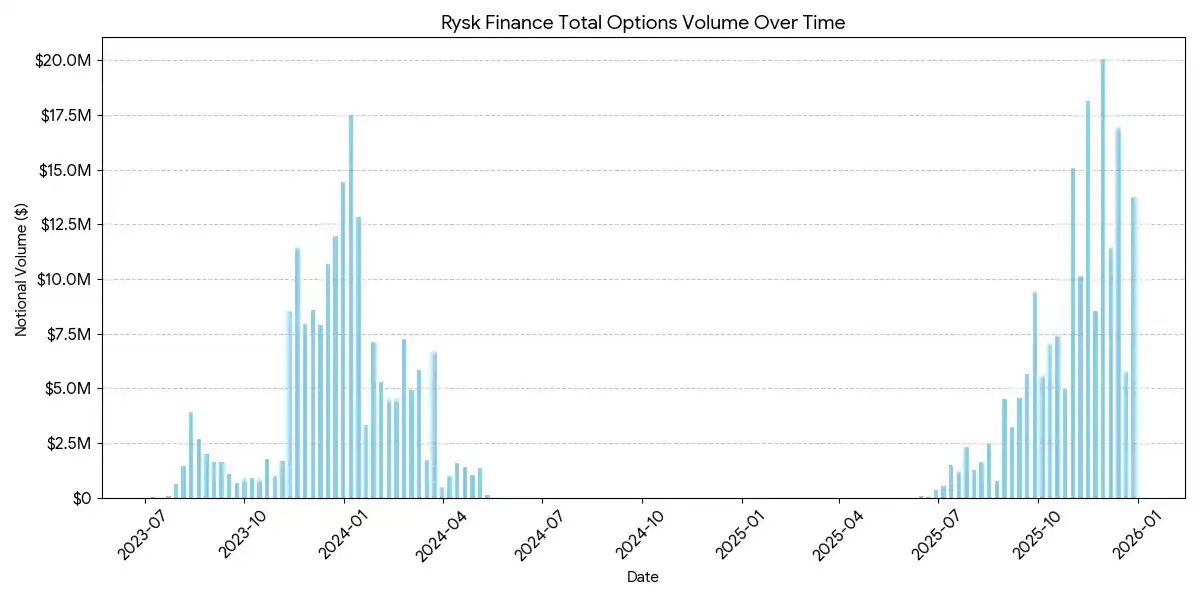

Rysk

Rysk применяет традиционный механизм продажи опционов к DeFi через ончейн-примитивы, поддерживая покрытые коллы и обеспеченные наличными путы. Пользователи могут напрямую вносить коллатераль в смарт-контракты для создания отдельных позиций, настраивая страйк и дату экспирации. Торги исполняются через механизм запроса котировок в реальном времени, где контрагенты предоставляют конкурентные предложения через быстрые ончейн-аукционы, обеспечивая мгновенное подтверждение и авансовое получение премии.

Доходность следует стандартной структуре покрытого колла:

- Если при экспирации цена < страйка: опцион истекает бесполезным, продавец сохраняет коллатераль + премию.

- Если при экспирации цена ≥ страйка: коллатераль физически поставляется по страйку, продавец сохраняет премию, но отказывается от апсайда.

Аналогичная структура применима и к путам, обеспеченным наличными, с автоматической физической поставкой на chain.

Rysk ориентирован на пользователей, ищущих устойчивую, неинфляционную доходность от опционных премий, где каждая позиция полностью коллатеризирована, отсутствует контрагентский риск и используется детерминированный ончейн-расчет. Он поддерживает多种 активы в качестве коллатераля, такие как ETH, BTC, LST и LRT, что делает его применимым для DAO, казначейств, фондов и институтов, управляющих волатильными активами.

Средний размер позиции на платформе Rysk достигает пятизначных цифр, что указывает на институциональный уровень вовлеченных средств.

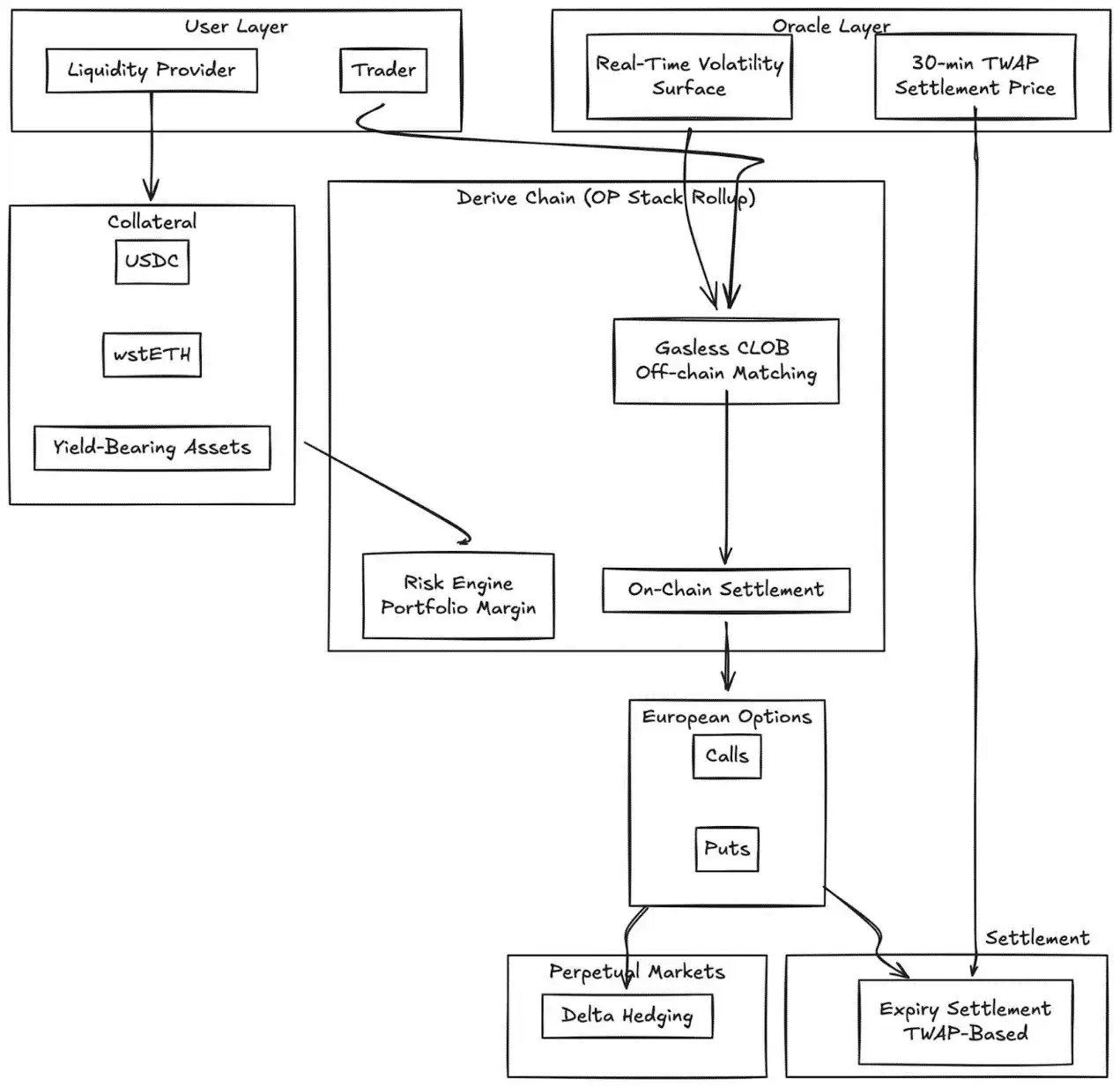

Derive.xyz

Derive (ранее Lyra) перешла от своей pioneering AMM-архитектуры к бесгазовой централизованной стакану заявок (CLOB) с ончейн-расчетом. Протокол предлагает полностью коллатеризированные европейские опционы с динамической volatility surface и расчетом на основе 30-минутного TWAP.

Ключевые инновации:

- Ценообразование в реальном времени через внешние feed'ы volatility surface

- 30-минутный TWAP-оракул снижает риск манипуляций при экспирации

- Интеграция с перпетуальными рынками для непрерывного дельта-хеджирования

- Поддержка доходного коллатераля (wstETH и т.д.) и портфельной маржи для повышения эффективности капитала

- Качество исполнения: конкурентоспособно по сравнению с небольшими CeFi-площадками

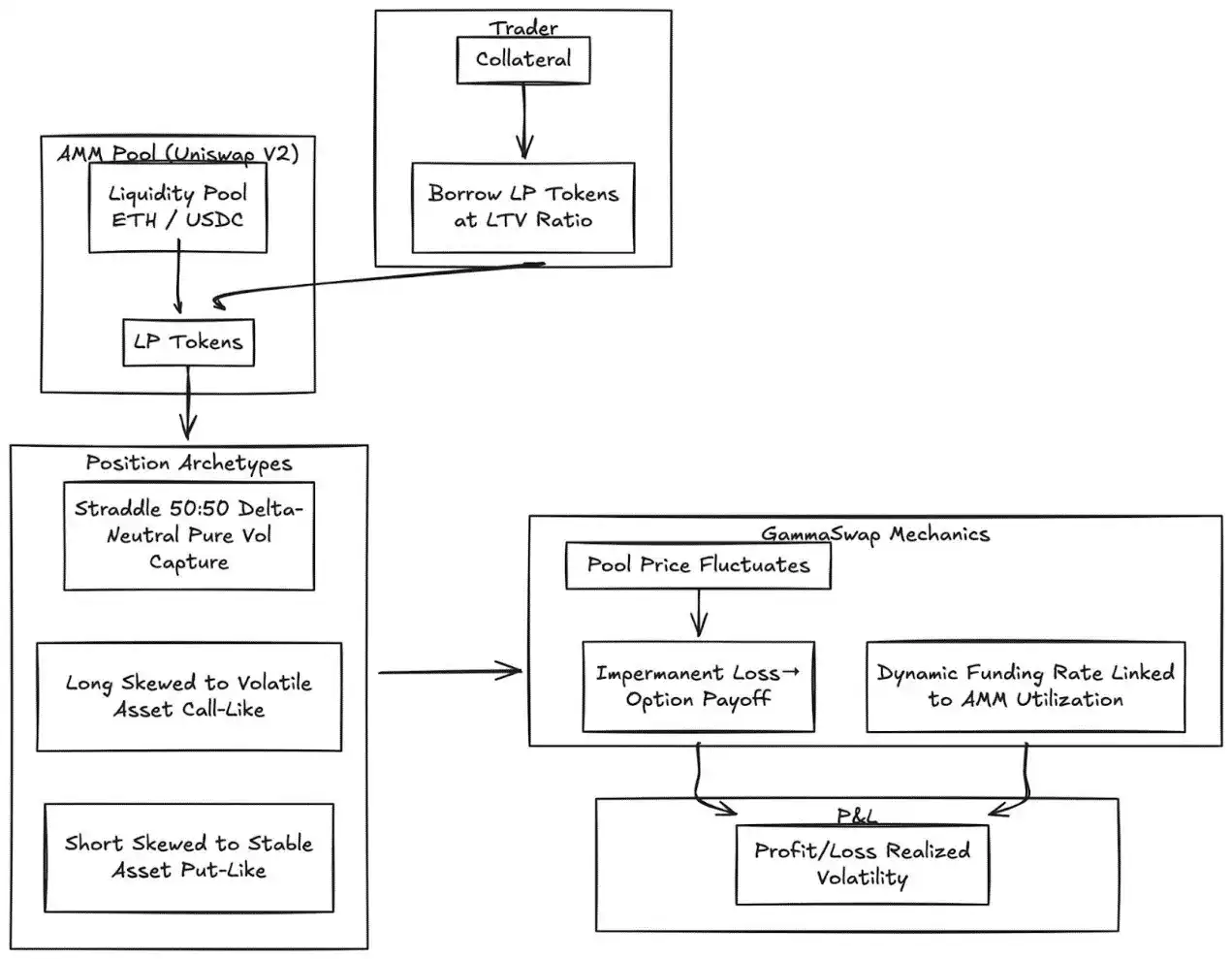

GammaSwap

GammaSwap представляет собой несинтетические перпетуальные опционы, построенные на основе ликвидности AMM.

Он не полагается на оракулы или фиксированные даты экспирации, а вместо этого генерирует постоянную экспозицию к волатильности, занимая ликвидность у AMM, таких как Uniswap V2.

Этот механизм превращает impermanent loss в торгуемую опционную доходность:

- Трейдеры занимают LP-токены по указанному loan-to-value ratio

- По мере колебания цены пула, стоимость коллатераля изменяется относительно занятой суммы

- Прибыли/убытки пропорциональны реализованной волатильности

- Динамическая ставка финансирования привязана к утилизации AMM

Типы позиций:

- Стрэддл: Дельта-нейтральный (50:50), чистая capture волатильности

- Лонг-опцион: Коллатераль смещен в сторону более волатильного актива (аналогично коллу)

- Шорт-опцион: Коллатераль смещен в сторону более стабильного актива (аналогично путу)

Этот механизм полностью устраняет зависимость от оракулов, выводя все цены из эндогенного состояния AMM.

Panoptic

Перпетуальные опционы без оракулов на Uniswap.

Panoptic представляет собой фундаментальный сдвиг: перпетуальные опционы без оракулов, построенные на основе концентрированной ликвидности Uniswap v3. Любая LP-позиция в Uniswap может быть интерпретирована как комбинация длинных и коротких опционов, а комиссии существуют в виде непрерывного потока опционных премий.

Ключевое прозрение: позиция Uniswap v3 в определенном ценовом диапазоне ведет себя подобно комбинации коротких опционов, чья дельта меняется с ценой. Panoptic формализует эту концепцию, позволяя трейдерам вносить коллатераль и выбирать диапазоны ликвидности для создания перпетуальных опционных позиций.

Ключевые характеристики:

- Оценка без оракулов: все позиции оцениваются с использованием внутренних котировок и данных о ликвидности Uniswap

- Перпетуальная экспозиция: опционы удерживаются бессрочно, поток премий непрерывен, а не дискретные даты экспирации

- Композитность: построен на Uniswap, интегрирован с протоколами кредитования, структурированной доходности и хеджирования

Сравнение с CeFi:

Разрыв с централизованными биржами все еще значителен. Deribit доминирует глобально с ежедневным открытым интересом свыше $3 млрд.

Эту разницу объясняют несколько структурных факторов:

Глубина и ликвидность

CeFi концентрирует ликвидность в стандартизированных контрактах с тесно расположенными страйками, поддерживая стаканы в десятки миллионов для каждого страйка. Ликвидность DeFi все еще фрагментирована между протоколами, страйками и датами экспирации, каждый протокол запускает отдельные пулы, не способные делиться маржой.

Качество исполнения: Deribit и CME предлагают почти мгновенное исполнение по стакану. AMM-модели, такие как Derive, предлагают более узкие спреды для ликвидных, near-the-money опционов, но для крупных ордеров и глубоких out-of-the-money страйков качество исполнения падает.

Эффективность маржи: CeFi-платформы允许 кросс-маржу across инструментов; большинство DeFi-протоколов все еще изолируют коллатераль по стратегиям или пулам.

Однако, DeFi-опционы обладают уникальными преимуществами: permissionless доступ, ончейн-прозрачность и композитность с более широким стеком DeFi. Этот разрыв сократится по мере повышения эффективности капитала и устранения фрагментации протоколами через отказ от экспирации.

Институциональное позиционирование

Супер-стек Coinbase-Deribit:

Покупка Coinbase Deribit за $2.9 млрд обеспечила стратегическую интеграцию всего крипто-капитального стека:

- Вертикальная интеграция: спот-биткоины, хранящиеся пользователями на Coinbase, могут использоваться в качестве коллатераля для опционной торговли на Deribit.

- Кросс-маржа: в фрагментированном DeFi капитал разбросан по протоколам. На Coinbase/Deribit капитал сосредоточен в одном пуле.

- Полный контроль жизненного цикла: через приобретение Echo, Coinbase контролирует выпуск => спот-торговля => торговля деривативами.

Для DAO и крипто-нативных институтов опционы предоставляют эффективные механизмы управления рисками казначейств:

- Покупка путов для хеджирования downside risk, блокировки минимальной стоимости активов казначейства.

- Продажа покрытых коллов для получения дохода от idle assets, создания системного потока доходов.

- Токенизация risk exposure через упаковку опционной экспозиции в ERC-20 токены.

Эти стратегии превращают волатильные холдинги токенов в более стабильные, скорректированные на риск резервы, что критически важно для институционального adoption казначейств DAO.

Оптимизация LP-стратегий

Расширяемый инструментарий для LP, превращающий пассивную ликвидность в активные стратегии хеджирования или усиления доходности:

- Опционы как инструменты динамического хеджирования: LP в Uniswap v3/v4 могут снизить impermanent loss, покупая путы или строя дельта-нейтральные спреды. GammaSwap и Panoptic позволяют использовать ликвидность в качестве коллатераля для непрерывной опционной доходности, компенсируя экспозицию AMM.

- Опционы как overlay дохода: хранилища могут автоматически исполнять стратегии покрытых коллов и обеспеченных наличными путов против LP или спот-позиций.

- Стратегии с таргетированием дельты: перпетуальные опционы Panoptic позволяют выбирать дельта-нейтральную, короткую или длинную экспозицию через настройку страйков и диапазонов.

Композитные структурированные продукты

- Интеграция с хранилищами: автоматизированные хранилища упаковывают краткосрочные волатильные стратегии в токенизированные инструменты дохода, подобные структурированным ончейн-нотам.

- Многоногые опционы: протоколы, такие как Cega, разрабатывают path-dependent выплаты (dual currency notes, autocallables) с ончейн-прозрачностью.

- Кросс-протокольная композитность: комбинирование опционной доходности с кредитованием, рестейкингом или правами выкупа для создания гибридных risk инструментов.

Взгляд вперед

Рынок опционов не превратится в единую категорию. Он эволюционирует в два截然 разных уровня, каждый обслуживает不同类型的 пользователей и предлагает совершенно разные продукты.

Уровень 1: Абстрагированные опционы для массовой розницы

Успех Polymarket доказал, что розница не отвергает опционы, она отвергает сложность. $90 млрд объема пришли не от трейдеров, понимающих implied volatility, а от пользователей, которые видят вопрос, выбирают сторону и нажимают кнопку.

Euphoria и подобные дофаминовые приложения продвинут эту теорию дальше. Механика опционов невидима под интерфейсом click-to-trade. Никаких греков, дат экспирации, расчетов маржи — только ценовые цели на сетке. Продукт — это опцион.

Пользовательский опыт подобен игре.

Этот уровень захватит объем, который сейчас монополизирован перпетуальными контрактами: краткосрочные, высокочастотные, дофаминовые направленные ставки. Конкурентное преимущество — не в финансовой инженерии, а в UX-дизайне, mobile-first интерфейсах и суб-секундной обратной связи. Победители на этом уровне будут больше похожи на потребительские приложения, чем на торговые платформы.

Уровень 2: DeFi-опционы как институциональная инфраструктура

Протоколы like Derive и Rysk не будут бороться за розницу. Они будут обслуживать совершенно другой рынок: DAO, управляющие казначействами с восьмизначными суммами, фонды, ищущие некоррелированную доходность, LP, хеджирующие impermanent loss, и аллокаторы активов, строящие структурированные продукты.

Этот уровень требует технического совершенства. Портфельная маржа, кросс-коллатерализация, системы запросов котировок, динамические volatility surfaces — функции, которые, вероятно, не понадобятся розничному инвестору, но критичны для институционального.

Сегодняшние провайдеры хранилищ — это ранняя инфраструктура институционального уровня.

Ончейн-аллокаторам активов потребуется вся выразительная сила опционов: точные стратегии хеджирования, overlay дохода, дельта-нейтральные стратегии, композитные структурированные продукты.

Ползунки leverage и простые рынки кредитования не справятся.

Связанное чтение: Являются ли预测 рынки расширенной формой бинарных опционов?