Автор: Клод, Deep Tide TechFlow

Вступление от Deep Tide: В то время как Nasdaq обновляет исторические максимумы, а рыночная капитализация NVIDIA приближается к 5,3 трлн долларов, Майкл Берри, прославившийся короткими продажами в ипотечный кризис 2008 года и ставший прототипом фильма «Большой шорт», делает контринтуитивные ставки.

Он не только сохраняет медвежьи позиции по NVIDIA и Palantir, но и расширяет шортовые позиции на ETF полупроводников и ETF индекса Nasdaq, одновременно покупая традиционные софтверные акции, на которые оказало давление повествование об ИИ, формируя таким образом полный портфель «переоценки пузыря ИИ».

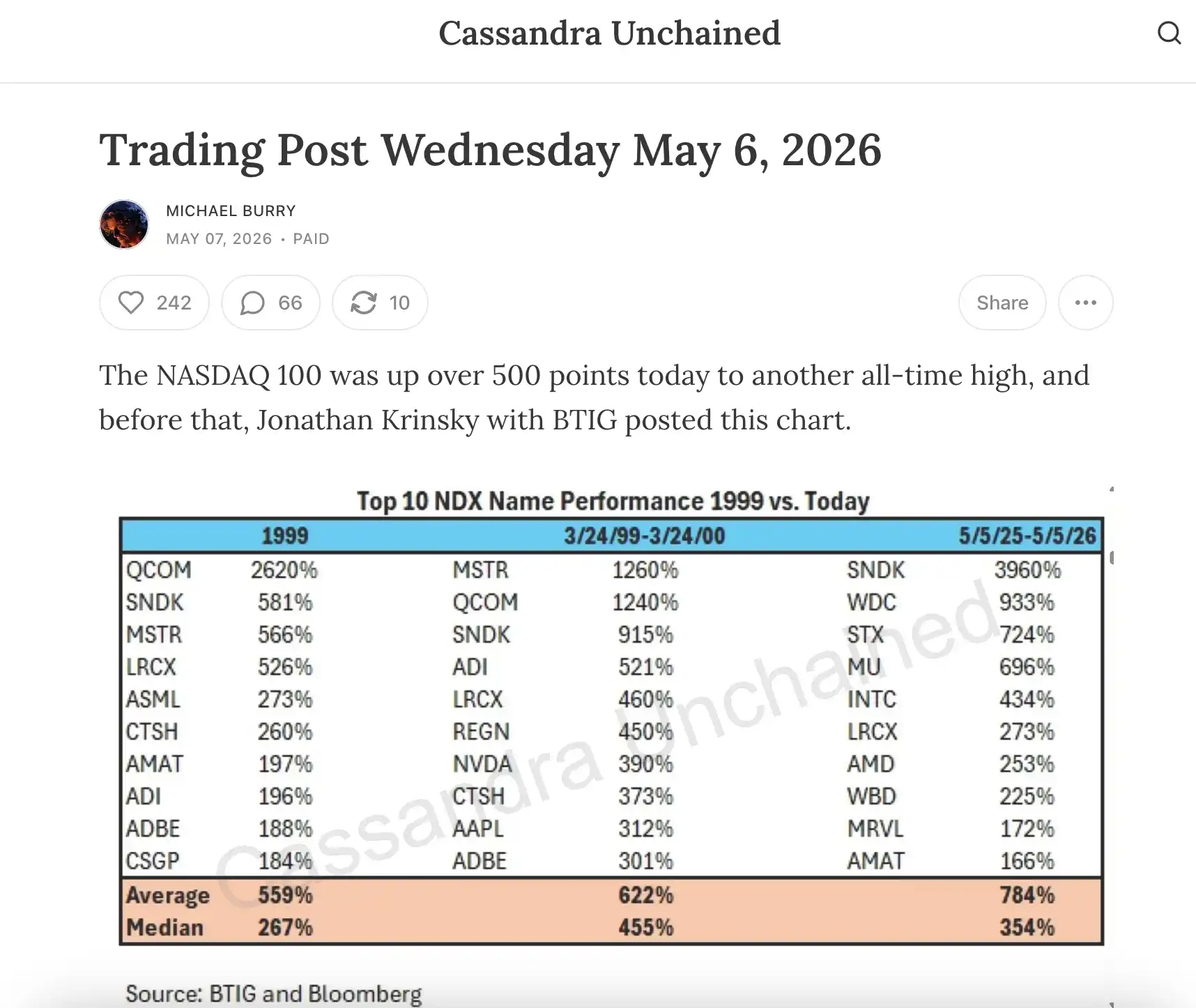

Индекс Nasdaq на этой неделе непрерывно обновляет исторические максимумы, 8 мая закрылся примерно на уровне 26 247 пунктов, индекс S&P 500 в тот же день также достиг рекорда. Индекс полупроводников Филадельфии с начала второго квартала вырос примерно на 55%, акции NVIDIA приближаются к историческому максимуму в 217,80 долларов, рыночная капитализация превысила 5,2 трлн долларов. Технологическое веселье, подпитываемое ИИ, находится на самом горячем этапе.

Но в момент наибольшего рыночного возбуждения инвестор, известный своими контринтуитивными ставками, активно наращивает позиции в противоположном направлении.

Согласно отчету Foreign Policy Journal от 7 мая, Майкл Берри, хедж-фонд менеджер, предсказавший ипотечный кризис 2008 года и ставший прототипом фильма «Большой шорт», на этой неделе в своей колонке на Substack «Cassandra Unchained» раскрыл последние корректировки в портфеле:

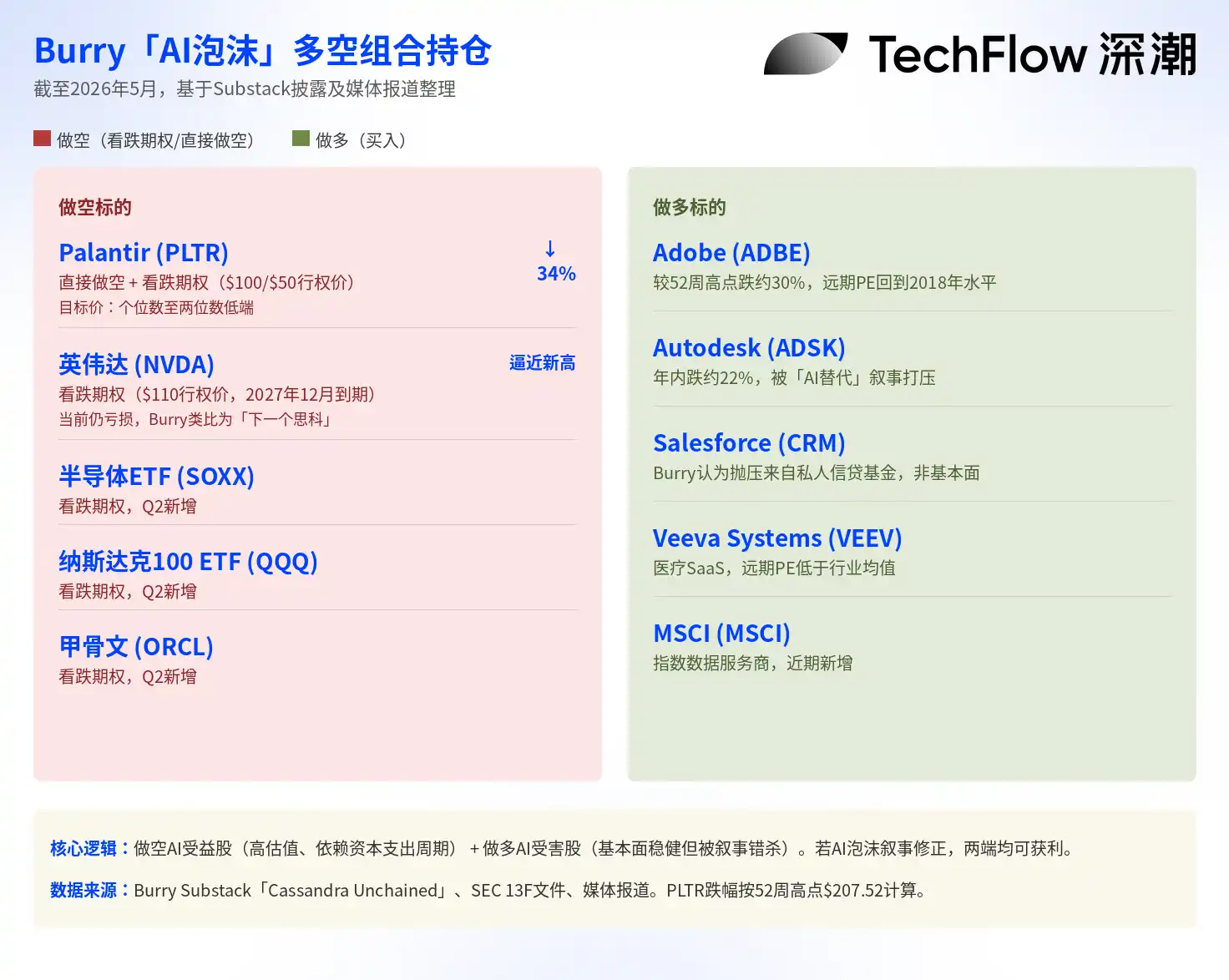

Он не только сохранил медвежьи опционы на NVIDIA и Palantir, но и добавил прямые шортовые позиции по Palantir, а также расширил медвежьи ставки на ETF полупроводников (SOXX), ETF Nasdaq 100 (QQQ) и Oracle.

Одновременно он начал покупать ряд традиционных софтверных компаний, оказавшихся на обочине ажиотажа вокруг ИИ, таких как Adobe, Autodesk, Salesforce и Veeva Systems, аргументируя это тем, что падение их акций вызвано паническими распродажами, а не ухудшением фундаментальных показателей.

Таким образом, сформировался полноценный хеджирующий портфель по типу «Большого шорта», ключевая логика которого — шортить акции, выигрывающие от ИИ, и покупать акции, страдающие от ИИ.

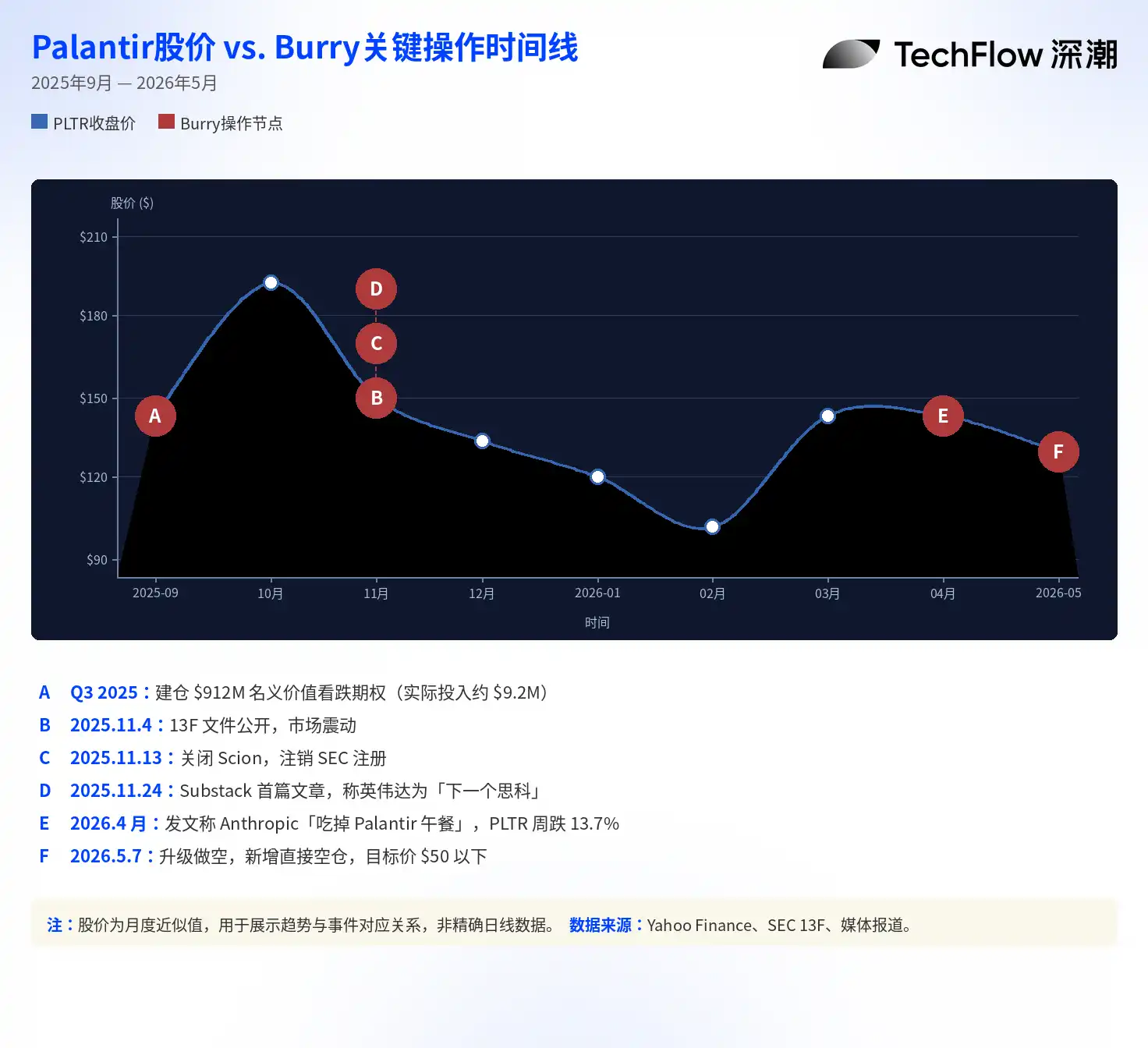

Начиная со ставки в 1,1 млрд долларов в ноябре прошлого года

Медвежьи позиции Берри на сектор ИИ начались в третьем квартале 2025 года.

Тогда файлы 13F его хедж-фонда Scion Asset Management показали, что он купил медвежьи опционы на Palantir номинальной стоимостью около 912 млн долларов и медвежьи опционы на NVIDIA номинальной стоимостью около 187 млн долларов. Это сообщение, опубликованное в ноябре прошлого года, вызвало волну на рынке, акции Palantir и NVIDIA временно оказались под давлением.

Однако позже Берри уточнил на платформе X, что его реальные вложения составили около 9,2 млн долларов, а не широко распространенные в СМИ 912 млн долларов — последняя сумма представляет собой номинальную стоимость опционных контрактов, разница почти в сто раз. Эта деталь крайне важна: номинальная стоимость в файлах 13F часто ошибочно интерпретируется как реально вложенные средства, тем самым преувеличивая масштабы сделки.

Вскоре после раскрытия информации Берри объявил о закрытии Scion Asset Management и аннулировании регистрации в SEC, завершив карьеру по управлению внешним капиталом.

Затем он перешел в статус частного инвестора и открыл колонку под названием «Cassandra Unchained» на Substack (Кассандра — пророчица из греческой мифологии, предсказывавшая правду, которой никто не верил), продолжая публиковать рыночный анализ.

Шорт по Palantir уже приносит результаты, Берри говорит: «Еще не упали достаточно»

С точки зрения результатов торгов, ставка Берри на Palantir в настоящее время прибыльна. Акции Palantir упали с примерно 161 доллара на момент его входа до текущих примерно 137 долларов, что примерно на 34% ниже 52-недельного максимума в 207 долларов. Несмотря на то, что компания только что опубликовала блестящую отчетность за первый квартал 2026 года (выручка выросла на 85% в годовом исчислении), после публикации отчетности акции, наоборот, упали.

Берри не стал фиксировать прибыль. Согласно его раскрытию в Substack, в настоящее время он держит медвежьи опционы с истечением в декабре 2026 года и страйком 100 долларов, а также медвежьи опционы с истечением в июне 2027 года и страйком 50 долларов, что означает, что он ожидает падения Palantir более чем на 60% от текущего уровня в течение следующего года. В своем посте он четко заявил, что справедливая оценка Palantir составляет лишь «низкие однозначные или двузначные цифры».

В апреле этого года Берри опубликовал в Substack пост, в котором заявил, что Anthropic «съедает обед у Palantir», указав, что выручка этой компании по безопасности ИИ растет с годовой скоростью, превышающей 300 млрд долларов, и ее более простые в использовании и менее дорогие инструменты интеграции ИИ заменяют сложные корпоративные решения Palantir. После публикации этого поста акции Palantir упали на 13,7% в течение недели, после чего Берри удалил пост. Аналитик Wedbush Дэн Айвз назвал эту точку зрения «выдуманной историей», а генеральный директор Palantir Алекс Карп ранее публично заявлял, что не понимает медвежью позицию Берри.

Шорт по NVIDIA все еще убыточен, но Берри настаивает: «ИИ — это пузырь»

По сравнению с победой на Palantir, положение Берри на NVIDIA совершенно иное.

Акции NVIDIA 8 мая закрылись примерно на 215 долларов, приближаясь к историческому максимуму в 217,80 долларов, рыночная капитализация составила около 5,3 трлн долларов. По сообщениям, медвежьи опционы Берри на NVIDIA имеют страйк 110 долларов и истекают в декабре 2027 года, в настоящее время они находятся в глубоком минусе. Но он не сократил позиции, а, наоборот, в последних корректировках портфеля продолжил наращивать их.

Ключевая логика Берри в шорте NVIDIA — «чрезмерное строительство инфраструктуры ИИ». В своей первой статье на Substack в ноябре прошлого года он сравнил нынешний бум инвестиций в ИИ с пузырем доткомов конца 1990-х, сравнив NVIDIA с Cisco того времени. Акции Cisco в период с 1995 по 2000 год выросли на 3800%, на короткое время став самой дорогой компанией в мире по рыночной капитализации, а затем рухнули более чем на 80% после лопнувшего пузыря доткомов.

Ключевые аргументы Берри включают: гипермасштабные клиенты, такие как Microsoft, Google, Meta, Amazon и Oracle, увеличивают сроки амортизации GPU для улучшения отчетности; по его оценкам, в период с 2026 по 2028 год такая бухгалтерская обработка позволит в совокупности недоначислить около 176 млрд долларов амортизационных расходов, завышая прибыль всей отрасли. Кроме того, он считает, что крупные капитальные затраты на текущую инфраструктуру ИИ основаны на чрезмерно оптимистичных прогнозах спроса, что аналогично ситуации с безумной прокладкой оптоволоконных кабелей телекоммуникационными компаниями около 2000 года.

Эта точка зрения вызвала прямую реакцию NVIDIA. По сообщению CNBC, NVIDIA в частном порядке распространяла среди уолл-стритовских продающих аналитиков семистраничный меморандум, в котором по пунктам отвечала на обвинения Берри, в частности упоминая его посты на платформе X как источник информации, требующий опровержения. NVIDIA в меморандуме заявила, что ее клиенты устанавливают срок амортизации GPU в четыре-шесть лет на основе реального срока службы, и что ранние продукты (например, A100, выпущенный в 2020 году) по-прежнему сохраняют высокий уровень использования. Берри ответил: «Я не говорю, что NVIDIA — это Enron», но настаивает на своем анализе.

Покупка пострадавших от ИИ софтверных акций: полный хеджирующий портфель против пузыря

Возможно, в корректировках портфеля Берри стоит обратить внимание не столько на шорты, сколько на его «лонговые» направления.

Недавно он купил акции Adobe, Autodesk, Salesforce, Veeva Systems и MSCI. Общая черта этих компаний: их бизнес-фундаменталы по-прежнему стабильны, но акции значительно упали из-за рыночного нарратива «подверженности риску от ИИ» и вынужденных распродаж фондами частного кредитования.

Adobe в настоящее время упала примерно на 30% по сравнению с 52-недельным максимумом, Autodesk потеряла около 22% с начала года, а их форвардный P/E вернулся к уровням 2018-2019 годов.

Берри объяснил в Substack, что он «не считает, что техническое давление со стороны продаж, вызванное частным кредитованием и софтверным долгом, достаточно, чтобы долгосрочно повлиять на эти акции». Другими словами, он считает, что рынок чрезмерно наказал компании, на которых наклеили ярлык «проигравшие от ИИ», и чрезмерно поддержал компании с ярлыком «победители от ИИ» — и он ставит на исправление этой ошибочной цены.

Если рассматривать вместе короткую и длинную стороны, Берри формирует типичный длинно-короткий хеджирующий портфель: если нарратив пузыря ИИ лопнет, высокооцененные акции-победители, такие как NVIDIA и Palantir, окажутся на передовой, а несправедливо наказанные традиционные софтверные акции, вероятно, получат переоценку. Даже если рынок в целом упадет, такая структура потенциально может принести положительную доходность.

Берри признался в письме инвесторам при закрытии Scion: «Мои суждения о стоимости ценных бумаг уже долгое время не совпадают с рыночными». Эта фраза — и самоанализ, и своего рода его постоянный манифест.

В самый разгар безумия вокруг ИИ он выбрал сторону, противоположную толпе.