Автор: Beats

На Уолл-стрит сделка «TACO» устарела, теперь все обсуждают новую торговую модель — «NACHO».

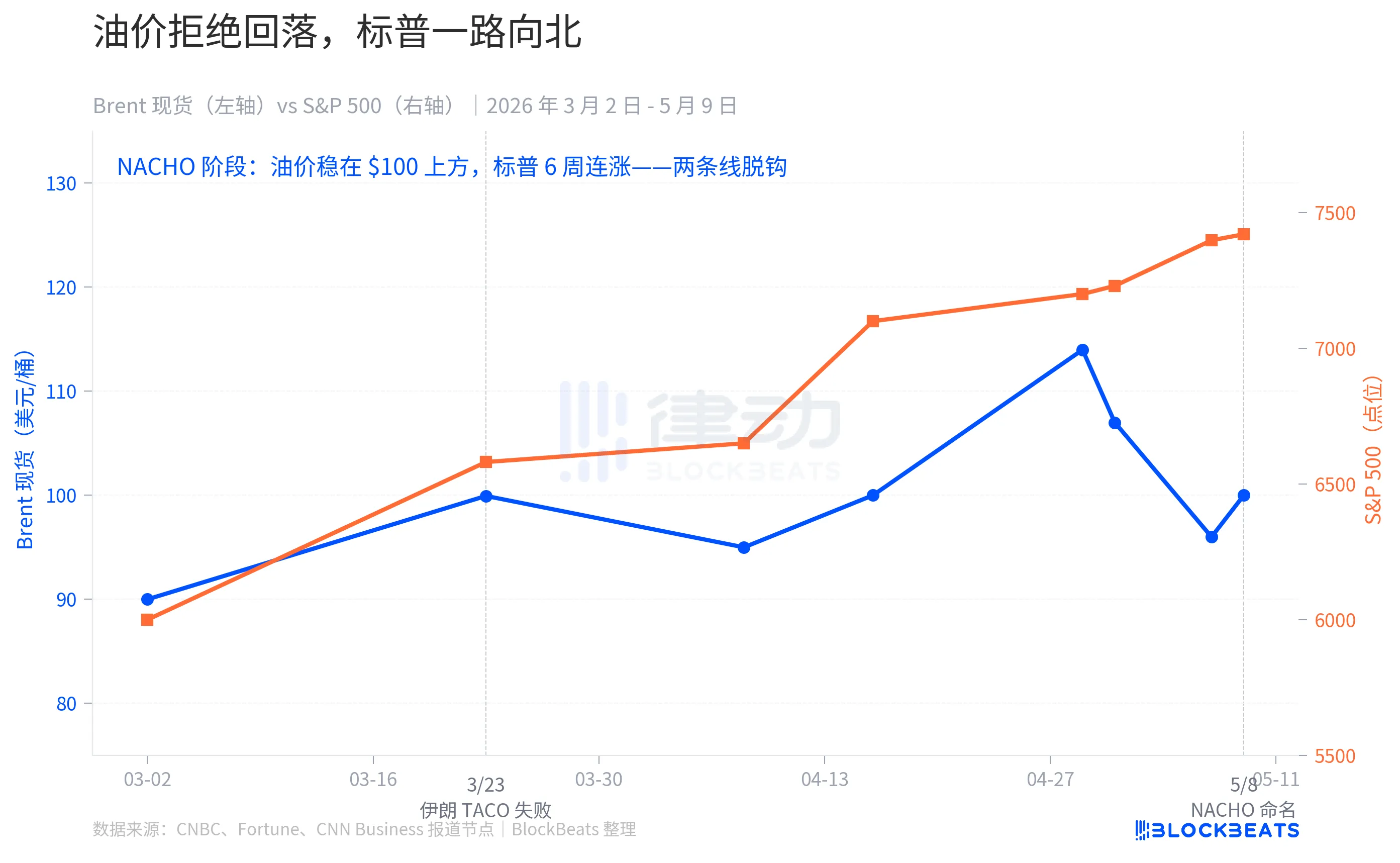

С 28 февраля, после американо-израильских авиаударов по Ирану, Ормузский пролив до сих пор не открыт. Сейчас цены на нефть выросли более чем на 50% по сравнению с довоенным уровнем, ожидания снижения ставки ФРС в 2026 году сжались с 2 раз до войны до текущих 0 раз. Но в то же время S&P 500 обновил исторический максимум, растёт шестую неделю подряд — это самая длинная победная серия с начала 2024 года.

Уолл-стрит дала этому кажущемуся противоречивым состоянию рынка имя — NACHO, что означает «Not A Chance Hormuz Opens» (Ормузский пролив не имеет шансов открыться). Это антоним TACO (Trump Always Chickens Out, Трамп всегда отступает). TACO ставила на то, что «человек струсит» — Трамп отступит в ключевой момент. NACHO ставит на то, что «ситуация зайдёт в тупик» — на этот раз Ормуз нельзя будет открыть одним постом в Truth Social.

Аналитик рынков eToro Завьер Вонг так описывает этот переход: «В течение большей части кризиса каждый заголовок о прекращении огня вызывал резкое падение цен на нефть, трейдеры постоянно делали ставки на решение, которое никогда не наступало. NACHO означает, что рынок признаёт: высокие цены на нефть — не разовый шок, а сама текущая рыночная среда».

Начало апреля: две линии

23 марта стало переломным моментом, когда модель TACO перестала работать. В то утро Трамп объявил в Truth Social о «очень хорошем конструктивном диалоге» с Ираном и приказал Пентагону приостановить удары по иранским энергообъектам на 5 дней. Фьючерсы на S&P 500 отскочили почти на 4% от минимума за считанные минуты, рыночная капитализация мгновенно выросла на 1,7 трлн долларов. Brent упал со 109 долларов внутри дня до 92 долларов.

Затем иранские власти опровергли факт диалога. По сообщению иранских государственных СМИ, «высокопоставленный сотрудник службы безопасности» назвал это манипуляцией рынком, заявив, что диалога никогда не было. Рост был сокращен вдвое в течение двух часов, S&P закрылся с ростом всего на 1,15%, Brent отскочил до 99,94 доллара.

Это был первый раз за последние 14 месяцев, когда «отступление» Трампа перестало влиять на рынок. Причина проста: отступление в модели TACO было односторонним, его можно было осуществить одним постом. Отступление 23 марта требовало сотрудничества Ирана. Когда оппонент не сотрудничает, отступление превращается в ложь.

С того дня рыночное поведение изменилось коренным образом. Brent в течение следующих 6 недель так и не вернулся к довоенному уровню в 67 долларов, средняя цена в мае сохраняется на уровне 109,57 доллара. В промежутке произошли соглашения о прекращении огня между США и Ираном 7 и 8 апреля, 17 апреля цены на нефть временно вернулись к «уровню начала войны», 7 мая появились сообщения о приближении к соглашению между США и Ираном — ни один из этих «заголовков о прекращении огня» не смог вернуть цены на нефть к базовому уровню.

Но S&P 500 упорно шёл на север. Рост в апреле составил 10% — сильнейший месяц с ноября 2020 года, за это время было обновлено 7 внутридневных исторических максимумов. 1 мая цена внутри дня пробила уровень 7230 пунктов, 7 мая закрытие на уровне 7398 пунктов.

Две линии полностью разошлись в начале апреля. В эпоху TACO они двигались в одном направлении: угроза — нефть падает, S&P падает; отступление — нефть отскакивает, S&P отскакивает. В эпоху NACHO они говорят на двух разных языках: нефть говорит «Ормуз закрыт наглухо», а S&P говорит «это меня не касается».

Три рынка, три реакции

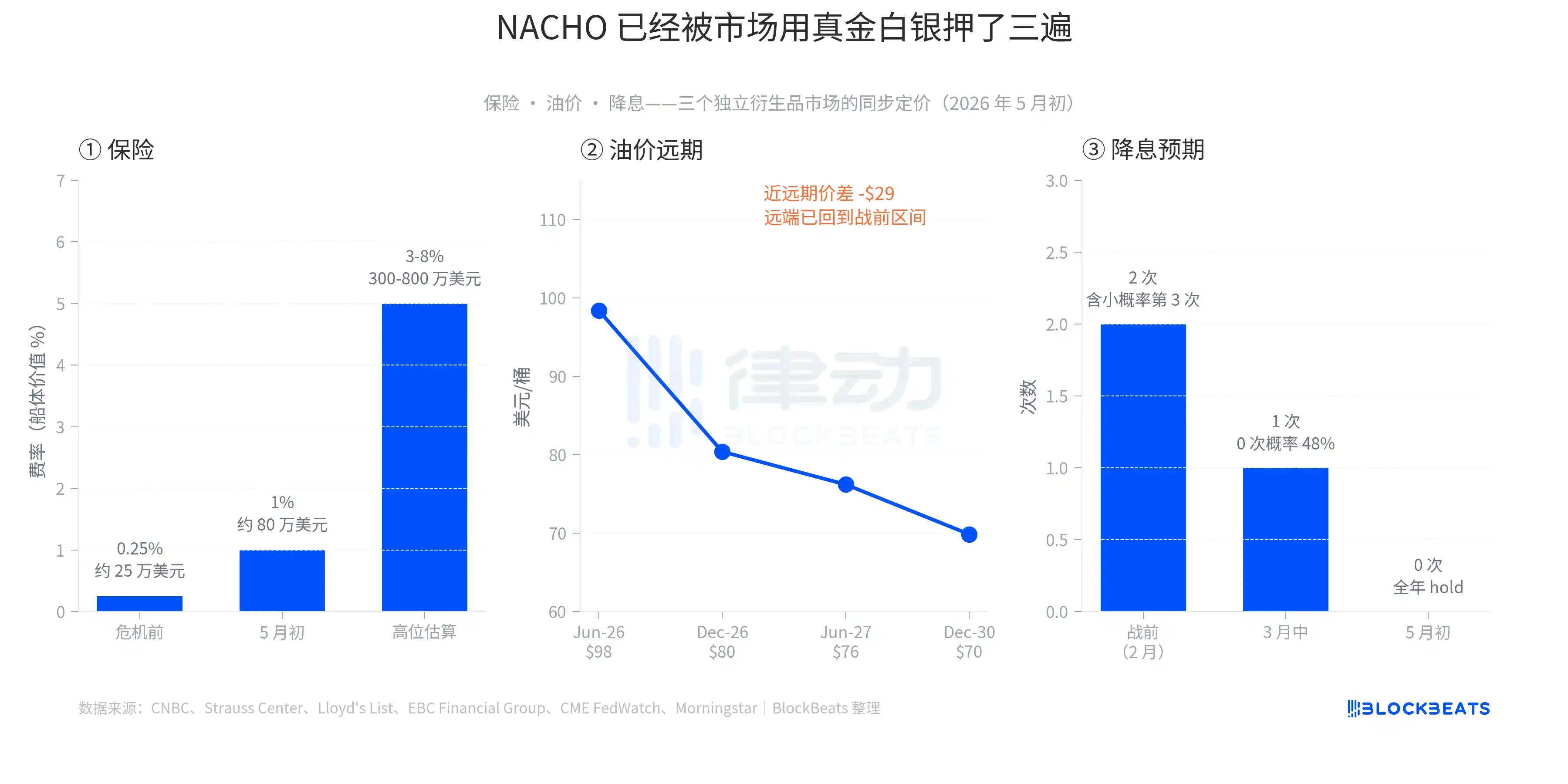

NACHO — это не пустые слова, а одинаковая ставка, сделанная тремя независимыми рынками производных инструментов на реальные деньги.

Первый уровень — страхование. Согласно историческим данным Strauss Center, ставки военного страхования в Ормузском проливе во время вторжения США в Ирак в 2003 году взлетели до 3,5% от стоимости судна, а на пике «танкерной войны» в 1984 году, после атаки на танкер Yanbu Pride, достигли 7,5%. Базовый уровень до этого кризиса составлял от 0,125% до 0,25%. К началу мая эта ставка достигла диапазона 1%, а по некоторым видам страхования взлетела до 3-8%.

Если перевести в стоимость страхования для одного супертанкера (VLCC) за один переход, расходы выросли с примерно 250 тысяч долларов до войны до текущих 800 тысяч — 8 миллионов долларов. Работа страховых компаний — оценивать риски. Реалистичный смысл этого уровня в том, что если страховые компании просто откажутся страховать, судовладельцы не будут брать на себя риск беспроходного перехода. «Физическое открытие» пролива и «фактическое судоходство» — это разные вещи.

Второй уровень — цены на нефть. Данные на начало мая показывают: контракт Brent Jun-26 торгуется на уровне 98,41 доллара, Dec-26 — 80,39 доллара, Jun-27 — 76,20 доллара, Dec-30 — 69,85 доллара. Спред между ближайшим месяцем и Dec-30 составляет около 28,5 доллара — это одна из самых крутых инвертированных (ближние выше, дальние ниже) структур за последние 5 лет. Эта кривая рассказывает очень конкретную историю: рынок считает, что спотовый рынок напряжён, но в конечном итоге ситуация улучшится, а дальние цены вернутся к довоенному диапазону 60-70 долларов. Другими словами, высокие цены на нефть — не конец истории, а ограниченный по времени промежуток. Но этот промежуток достаточно длинный, чтобы трейдеры не стали ставить на его внезапное завершение.

Третий уровень — снижение ставок. В начале февраля 2026 года рынок ожидал, что ФРС снизит ставку 2 раза в течение года, с небольшой вероятностью на 3-й раз. В середине марта, после взлёта цен на нефть, ожидания сжались до 1 раза, вероятность 0 снижений достигла 48%. 29 апреля ФРС оставила ставку на уровне 3,50%-3,75% без изменений, 6 мая данные CME FedWatch показали 70% вероятность сохранения ставки на июньском заседании. На весь 2026 год рынок уже заложил 0 снижений ставки. Легендарный хедж-фондовый управляющий Пол Тюдор Джонс даже заявил 7 мая в интервью CNBC: «Даже Уолшу не удастся заставить ФРС снизить ставки».

Все три уровня уже оставили след на рынке деривативов — это не нарратив, а реальные деньги.

Расшифровка рынка

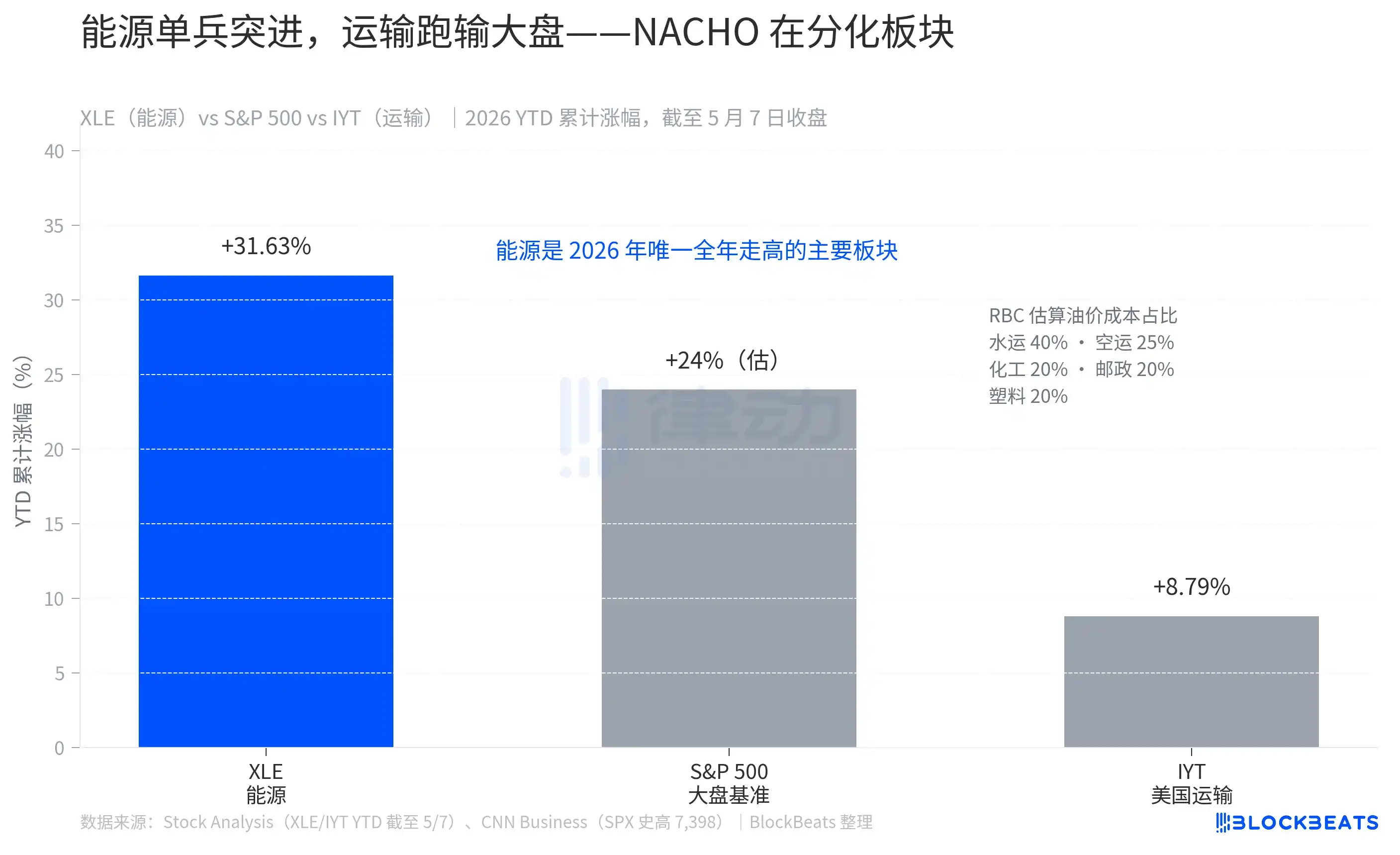

Второй неочевидный аспект NACHO заключается в том, что внутри общего рынка уже произошла дифференцированная оценка.

По состоянию на закрытие 7 мая, ETF энергетического сектора (XLE, фонд State Street Energy Select Sector Fund) с начала года вырос на 31,63% — это единственный крупный сектор, показавший рост за весь 2026 год. За тот же период S&P 500 вырос примерно на 24%. ETF транспортного сектора (IYT, iShares U.S. Transportation ETF) вырос всего на 8,79% с начала года, отстав от общего рынка более чем на 15 процентных пунктов.

Этот разрыв не случаен. По оценкам RBC Capital Markets, на долю топлива приходится 40% операционных затрат в морских перевозках, 25% — в авиаперевозках, по 20% — в химической промышленности, почтовой и курьерской доставке, производстве резины и пластмасс. Если нефть составляет большую часть вашей себестоимости, NACHO бьёт вам прямо в лицо.

Рост XLE на 31,63% — это не краткосрочный отскок, а результат 8 недель устойчивого опережения. Падение IYT на 8,79% — это не слабость, а рост вместе с рынком, но с одновременным снижением прибыли из-за цен на нефть. Рынок уже чётко показал, как рассчитываются шансы NACHO — достаточно взглянуть на величину отставания транспортного ETF от общего рынка.

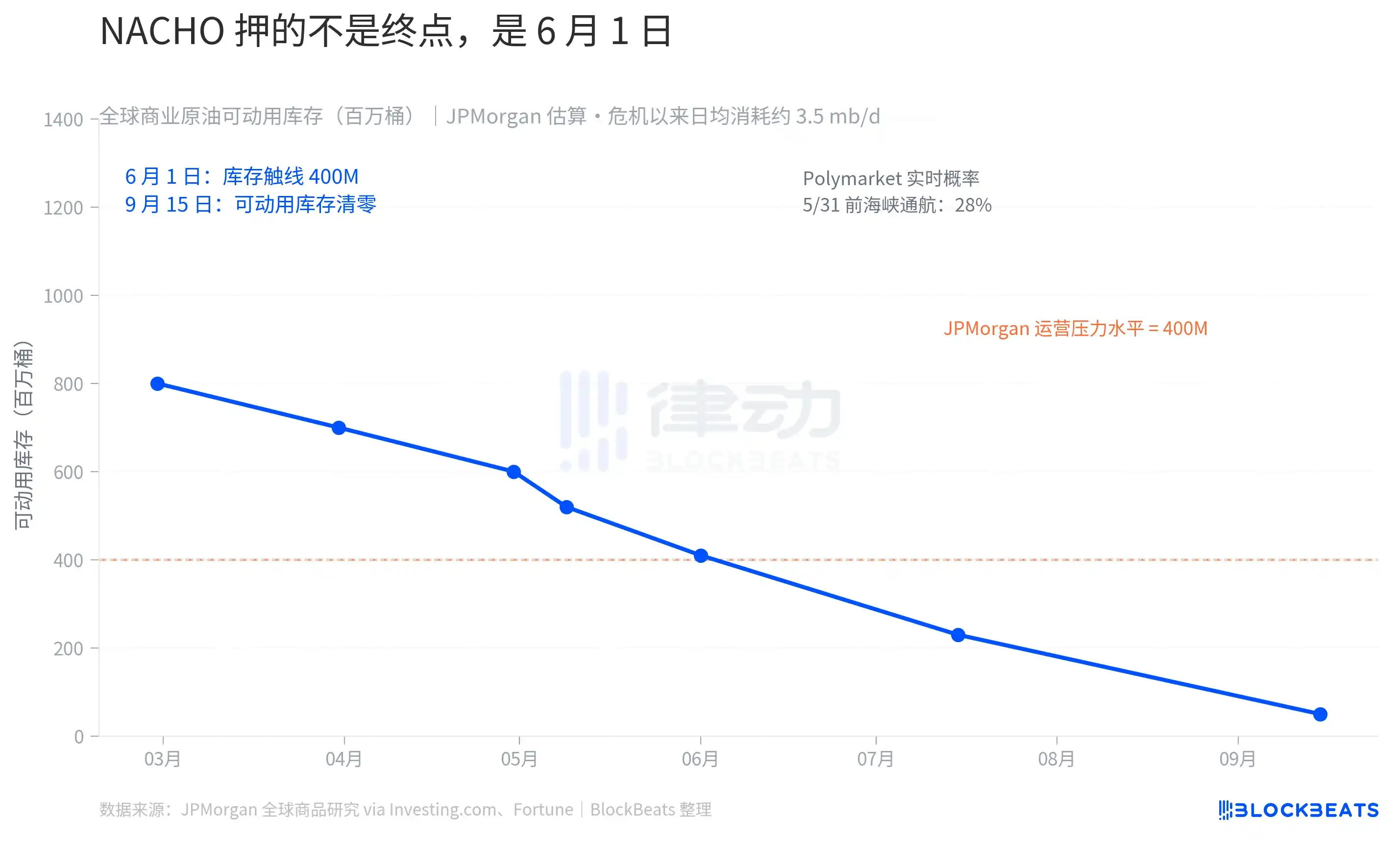

Но NACHO — это не бессрочная ставка, у неё есть очень конкретный срок — 1 июня.

Согласно оценке команды по исследованию сырьевых товаров JPMorgan, в начале 2026 года глобальные коммерческие запасы нефти составляли около 84 млрд баррелей, но только около 8 млрд из них были «фактически доступными», остальные — это заполнение трубопроводов, остатки в резервуарах, минимальные терминальные запасы и т.д., необходимые для поддержания повседневной работы системы. С начала этого кризиса было использовано 2,8 млрд баррелей, текущие остающиеся доступные запасы составляют около 5,2 млрд баррелей. Слова JPMorgan: «Ожидается, что коммерческие запасы приблизятся к уровню операционного давления в начале июня».

«Уровень операционного давления» — это конкретное физическое понятие. Объяснение JPMorgan: «Система не рухнет из-за исчезновения нефти, она рухнет из-за того, что в сети циркуляции не останется достаточного объёма работы». Как только будет пройдена эта линия, у предприятий и правительств останется только два выбора: либо сжать минимальные запасы, которые необходимо поддерживать (это нанесёт ущерб самой инфраструктуре), либо ждать новых поставок. Если Ормузский пролив не откроется до сентября, коммерческие запасы ОЭСР могут упасть до так называемого «operational floor» (операционного дна). По сообщению Fortune, ожидается, что запасы авиатоплива в Европе в июне упадут ниже порога в 23 дня поставок — это критический предупредительный уровень для отрасли.

Шансы прогнозных рынков синхронизированы с физическими часами. Согласно данным Polymarket на 9 мая, вероятность «нормального судоходства в Ормузском проливе до 31 мая» составляет 28%, а вероятность до 15 мая — всего 2%. На этом рынке активные позиции на сумму 9,92 млн долларов делают ставку на то, что NACHO, по крайней мере, до конца мая не перестанет действовать.

Рынок больше не торгует следующим постом Трампа в Truth Social, он начал торговать данными о запасах в Ормузском проливе на начало июня.