Автор | Odaily Planet Daily (@OdailyChina)

Автор | Azuma (@azuma_eth)

В прошедшие выходные два ведущих кредитных протокола в экосистеме Solana, Jupiter Lend и Kamino, вступили в открытый конфликт.

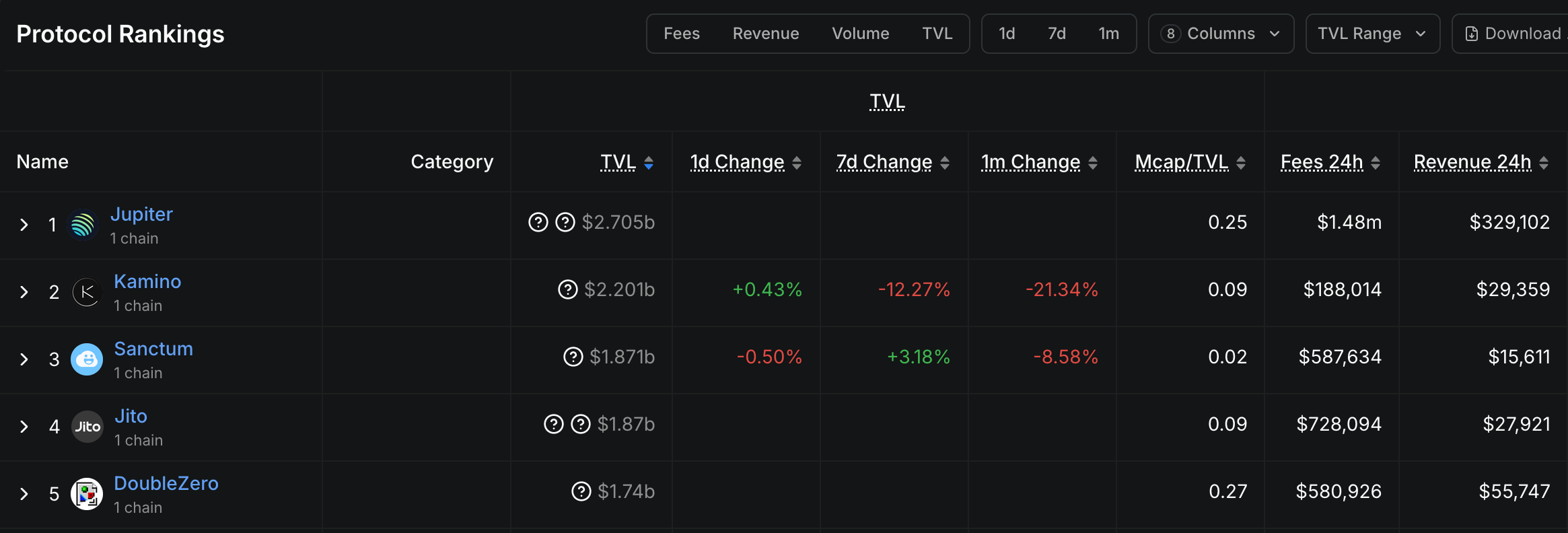

- Примечание Odaily: Согласно данным Defillama, Jupiter и Kamino в настоящее время являются двумя протоколами с наибольшим TVL в экосистеме Solana.

Причина конфликта: удаленный твит Jupiter

Истокидет события можно проследить до августа этого года, когда Jupiter в ходе анонса своего кредитного продукта Jupiter Lend неоднократно подчеркивал его функцию «изоляции рисков» (соответствующие посты были удалены), то есть отсутствие перекрестного заражения рисками между различными пулами.

Однако реализованный дизайн Jupiter Lend не соответствовал общепринятому пониманию модели изоляции рисков. Согласно рыночным представлениям, изолированные пулы в DeFi-кредитовании — это структура, которая разделяет риски разных активов или рынков, предотвращая влияние дефолта по одному активу или краха рынка на весь протокол. Основные характеристики включают:

- Разделение пулов: Разные типы активов (стейблкоины, волатильные активы, NFT как залог и т.д.) размещаются в независимых пулах, каждый со своей ликвидностью, долгом и параметрами риска.

- Изоляция залога: Пользователи могут использовать только активы внутри одного пула в качестве залога для займа других активов, что исключает перекрестное заражение.

Однако на деле дизайн Jupiter Lend поддерживает репост (повторное использование уже внесенного залога в других частях протокола) для повышения капиталоэффективности, что означает, что внесенный залог не полностью изолирован. Соучредитель Jupiter Сямяк Джайн пояснил, что пулы Jupiter Lend «в некотором смысле» изолированы, поскольку каждый пул имеет свои настройки, лимиты, пороги ликвидации, штрафы и т.д., а механизм репоста нужен лишь для оптимизации использования капитала.

Хотя в документации Jupiter Lend есть более подробные объяснения, объективно говоря, ранние заявления об «изоляции рисков» действительно расходятся с общепринятым пониманием и могут вводить в заблуждение.

Эскалация: Kamino переходит в атаку

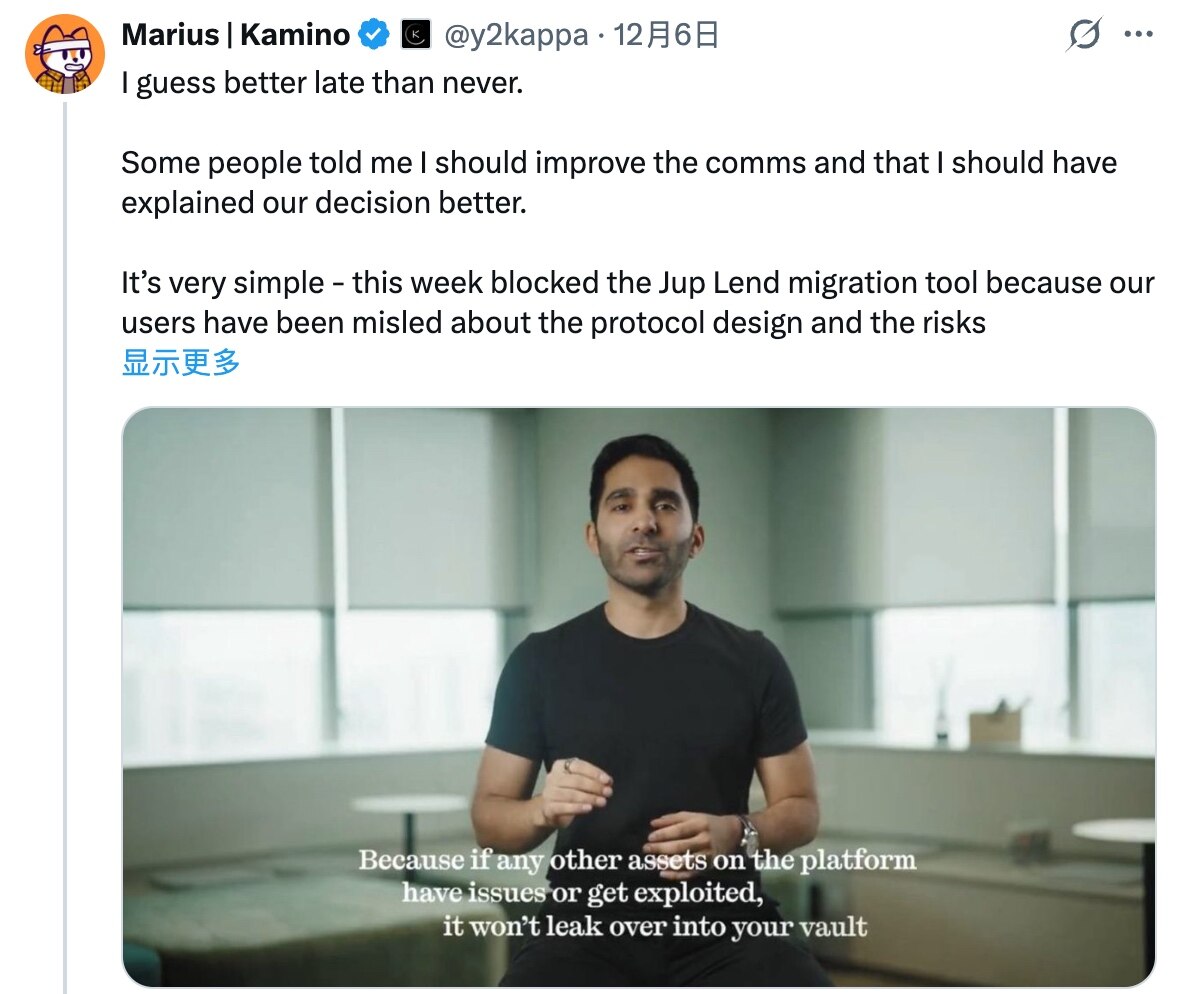

6 декабря соучредитель Kamino Мариус Чуботариу воспользовался этим поводом, чтобы раскритиковать Jupiter Lend, и заблокировал инструмент миграции из Kamino в Jupiter Lend.

Мариус заявил: «Jupiter Lend постоянно утверждает, что между активами нет перекрестного заражения, что является полной чушью. На самом деле, в Jupiter Lend, если вы вносите SOL и занимаете USDC, ваш SOL будет передан другим пользователям, использующим JupSOL, INF для рекурсивного кредитования, и вы будете нести все риски краха таких схем или провала активов. Здесь нет изоляции, существует полное перекрестное заражение, что противоречит рекламе и тому, что людям говорят...... Как в традиционных финансах (TradFi), так и в децентрализованных финансах (DeFi) информация о том, репостится ли залог, существуют ли риски заражения, является важной и должна раскрываться четко, никто не должен давать расплывчатых объяснений.»

После атаки со стороны Kamino дискуссия вокруг дизайна Jupiter Lend быстро взорвала сообщество. Некоторые согласились, что Jupiter занимается вводящим в заблуждение маркетингом — например, генеральный директор Penis Ventures 8bitpenis.sol яростно критиковал Jupiter за откровенную ложь с самого начала; другие считали, что модель Jupiter Lend сочетает безопасность и эффективность, а атака Kamino была продиктована рыночной конкуренцией и нечистыми намерениями — например, зарубежный KOL letsgetonchain заявил: «Дизайн Jupiter Lend позволяет достичь капиталоэффективности модели пулов, сохраняя при этом некоторые возможности управления рисками модульных кредитных протоколов...... Kamino не может помешать людям мигрировать к лучшей технологии.»

Под давлением Jupiter тихо удалил ранние посты, что вызвало еще большую волну FUD. Позже операционный директор Jupiter Каш Дханда также признал, что формулировка команды в соцсетях о «нулевом риске заражения» для Jupiter Lend была неточной, и извинился, заявив, что следовало сразу опубликовать исправление после удаления постов.

Ключевое противоречие: определение «изоляции рисков»

Обобщая противоположные мнения в сообществе, кажется, что корень разногласий лежит в разных определениях термина «изоляция рисков».

С точки зрения Jupiter и его сторонников, «изоляция рисков» — не полностью статичное понятие, в нем может быть пространство для маневра в дизайне. Jupiter Lend, хотя и не является общепринятой моделью изоляции, но и не относится к полностью открытой модели пулов; хотя используется общий слой ликвидности с репостом, каждый кредитный пул можно настраивать независимо, с собственными лимитами активов, порогами ликвидации, штрафами.

С точки зрения Kamino и его сторонников, любое разрешение на репост является полным отрицанием «изоляции рисков», и проекты не должны вводить пользователей в заблуждение расплывчатыми раскрытиями и ложной рекламой.

Позиция вышестоящих игроков: одни подливают масло в огонь, другие примиряют

Помимо спора между сторонами и сообществом, другой примечательный аспект этого конфликта — отношение ключевых игроков экосистемы Solana.

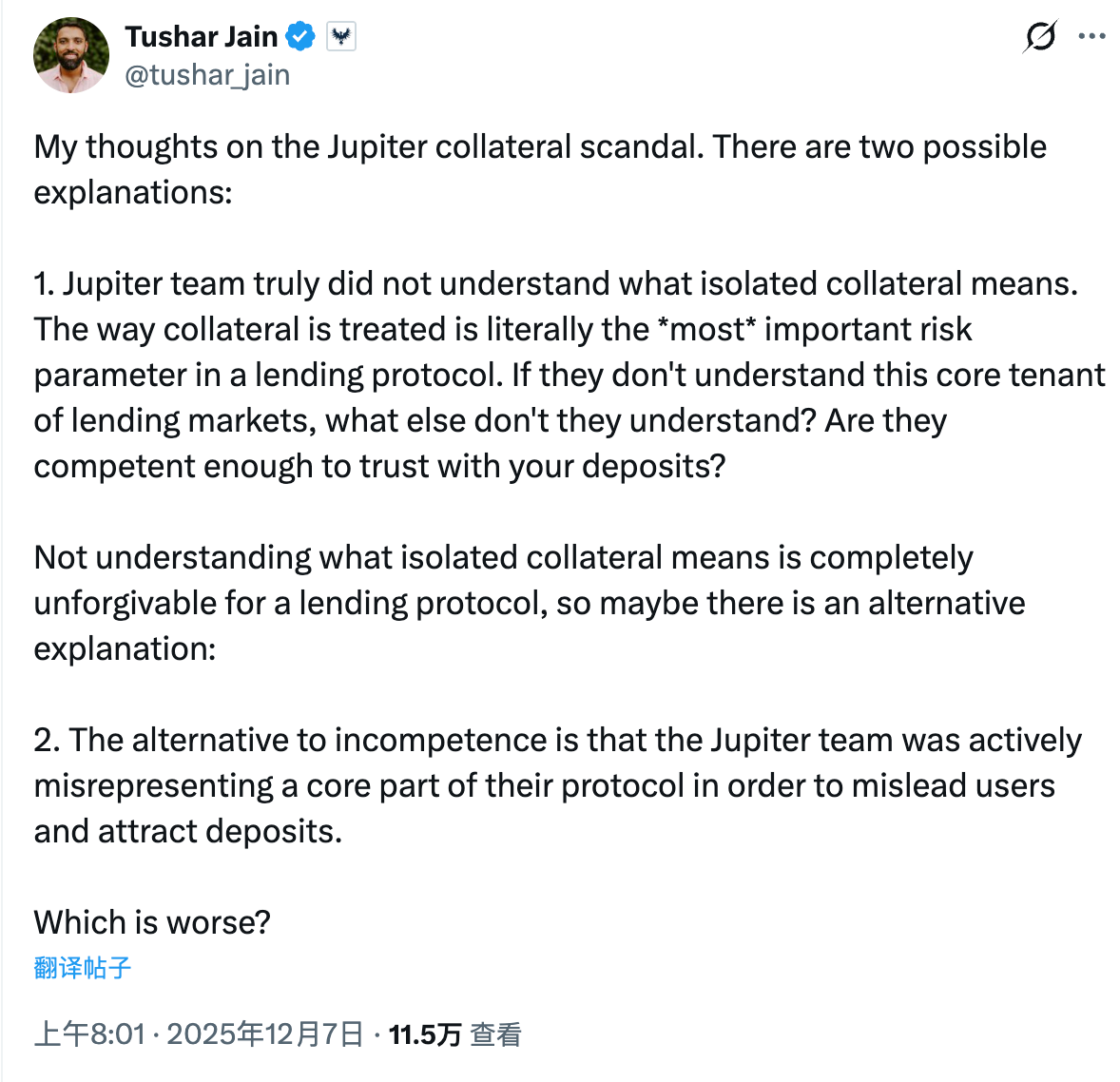

Во-первых, венчурный фонд Multicoin, обладающий наибольшим влиянием в экосистеме Solana. Будучи инвестором Kamino, партнер Multicoin Ташар Джайн прямо заявил, что Jupiter «либо глуп, либо плох, и ни то, ни другое непростительно» — объективно говоря, его заявление во многом усугубило конфликт.

Ташар сказал: «Есть два возможных объяснения спора вокруг Jupiter Lend. Первое: команда Jupiter действительно не понимает, что означает изолированный залог. Обработка залога — самый важный параметр риска в кредитном протоколе. Если они не понимают этот核心原则 кредитных рынков, что еще они упускают? Достаточно ли их профессионализма, чтобы можно было спокойно вносить средства? Для кредитного протокола непонимание значения изолированного залога совершенно непростительно. Другая возможность: команда Jupiter не некомпетентна, а намеренно искажает核心部分 своего протокола, чтобы ввести пользователей в заблуждение и привлечь депозиты.»

Очевидно, мотивация Ташара была ясна — использовать эту возможность, чтобы помочь Kamino нанести удар по конкуренту.

Другое важное заявление поступило от Фонда Solana. Как материнская экосистема, Solana явно не хочет видеть, как два ее ключевых проекта погружаются в чрезмерное противостояние, ведущее к внутренним распрям во всей экосистеме.

Вчера днем президент Фонда Solana Лили Лю обратилась на платформе X к обоим проектам с призывом к примирению: «Люблю вас. В целом, размер нашего рынка кредитования в настоящее время составляет около 5 миллиардов долларов, в то время как в экосистеме Ethereum он примерно в 10 раз больше. Что касается рынка залога в традиционных финансах, то он несравнимо больше. Мы можем выбрать атаковать друг друга, но также можем выбрать взгляд в будущее — сначала объединить усилия, чтобы отвоевать долю у всего крипторынка, а затем вместе двинуться на广阔просторы традиционных финансов.

Короче говоря — хватит спорить, а то Ethereum получит преимущество!

Фоновая логика: Битва кредитных лидеров Solana

Учитывая данные развития Jupiter Lend и Kamino, а также рыночную环境, этот конфликт, хотя и вспыхнул внезапно, кажется неизбежным столкновением, вопрос был лишь во времени.

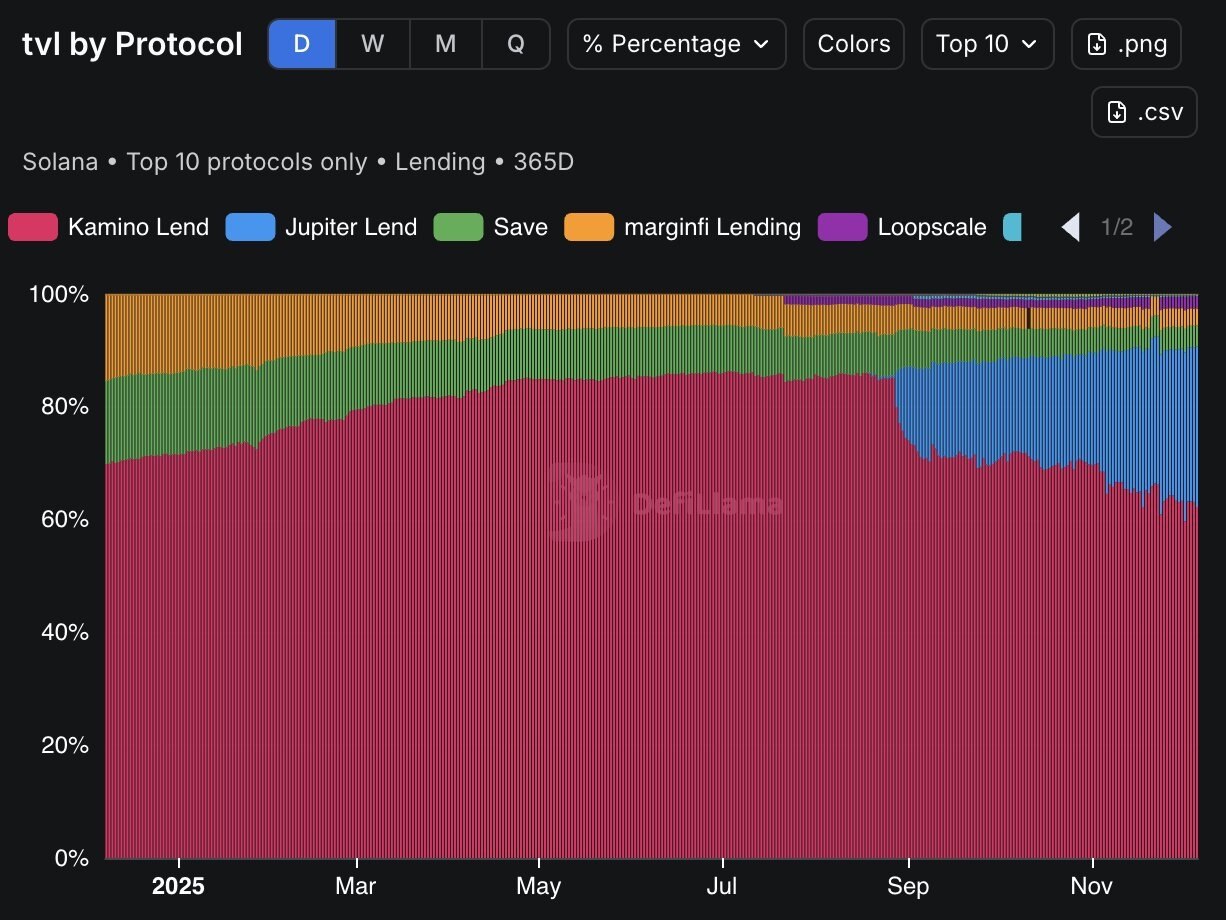

С одной стороны, Kamino (красный на графике) долгое время занимал лидирующую позицию в кредитовании в экосистеме Solana, но Jupiter Lend (синий на графике) с момента запуска захватил значительную долю рынка, став единственным challenger для Kamino в экосистеме.

С другой стороны, посе кровавой бани 11 октября рыночная ликвидность значительно сократилась, общий TVL экосистемы Solana продолжает снижаться; вдобавок череда провалов проектов сделала рынок DeFi крайне чувствительным к «безопасности».

В условиях хорошего рынка и притока средств Jupiter Lend и Kamino相对мирно сосуществовали, ведь все зарабатывали, и, казалось, будут зарабатывать еще больше... Но когда рынок перешел в режим игры с нулевой суммой, конкурентные отношения между ними стали более напряженными, а вопросы безопасности оказались самым эффективным поводом для атаки — даже если у Jupiter Lend не было сбоев, одного лишь подозрения в дизайне достаточно, чтобы вызвать警惕пользователей.

Вероятно, с точки зрения Kamino, сейчас идеальный момент, чтобы нанести серьезный удар по конкуренту.