18 апреля мост Kelp DAO подвергся атаке, в результате которой злоумышленник сгенерировал 116,5 тыс. токенов rsETH без реального обеспечения, которые были немедленно внесены в Aave для займа WETH. Хранитель Aave активировал экстренную заморозку в течение нескольких часов. По оценкам Lookonchain, потенциальные убытки для Aave V3 и V4 составляют около 195 млн долларов.

В то же время кредитный протокол SparkLend экосистемы MakerDAO (Sky) не понес потерь.

Это произошло не потому, что команда Spark умнее команды Aave, и не потому, что они заранее обнаружили уязвимость моста. Причина выхода Spark из rsETH была изложена в посте на governance-форуме три месяца назад и не имеет никакого отношения к безопасности контракта моста.

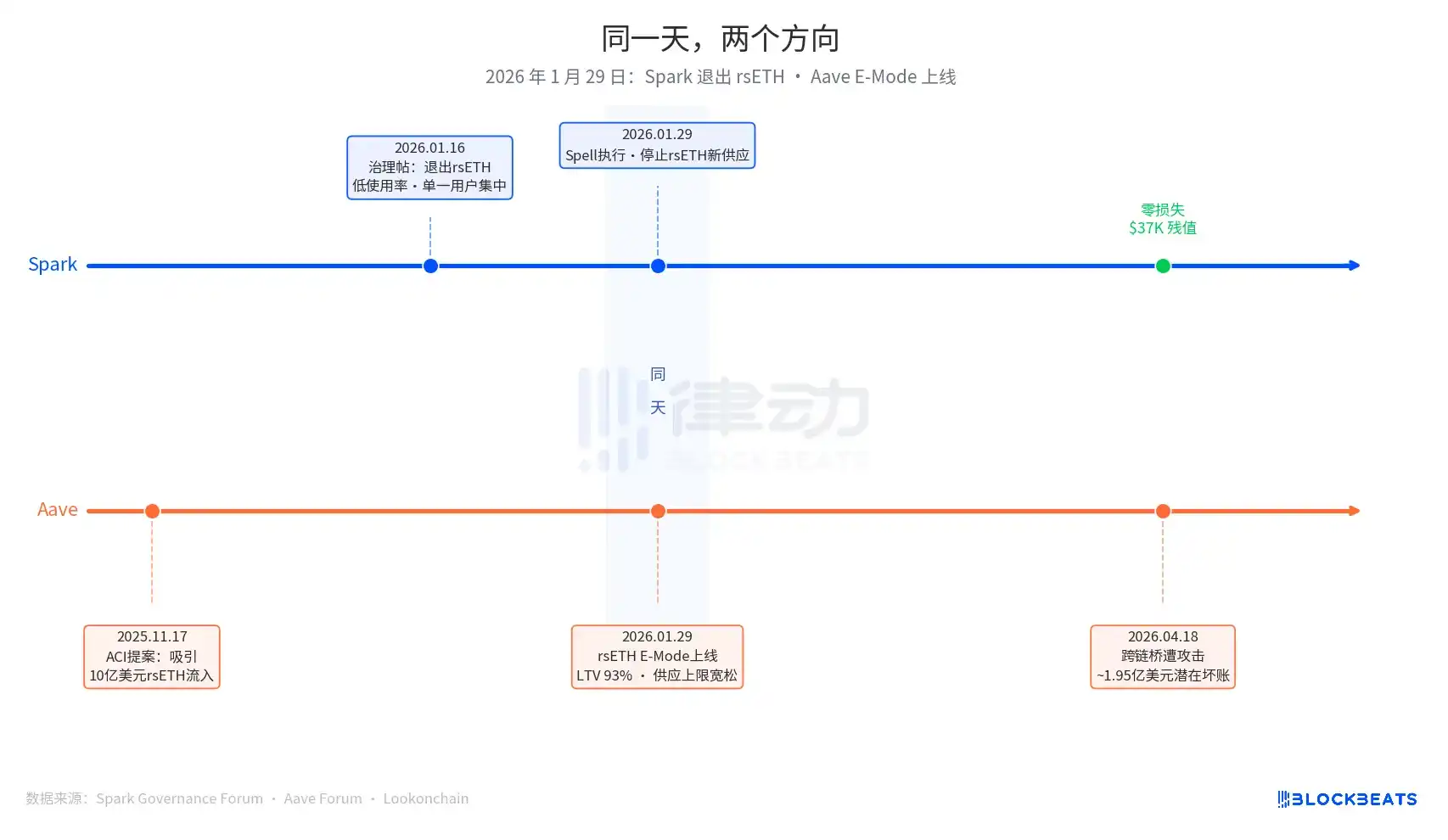

29 января 2026 года — ключевая дата в этой статье. В этот день Spark выполнил governance-операцию под названием Spell, прекратив прием новых поставок rsETH. В тот же день в Aave официально запустился режим E-Mode для rsETH, позволяющий пользователям использовать rsETH в качестве залога для займа WETH с максимальным коэффициентом кредитования (LTV) до 93%.

Один уходит, другой расширяется — в один и тот же день.

Решение Spark выйти началось с governance-поста, представленного PhoenixLabs (операционным органом экосистемы Spark) 16 января 2026 года. Причина была straightforward: низкая утилизация rsETH, почти весь объем использования приходился на один кошелек (адрес 0xb99a), и владелец этого кошелька уже выразил готовность использовать альтернативное обеспечение, такое как wstETH или weETH. В оригинальном посте говорится: «Отказ от rsETH может улучшить запас прочности SparkLend, повысив доходность с учетом рисков». Это была плановая очистка активов; в той же партии были выведены tBTC, ezETH и весь рынок Gnosis Chain по единой причине — «низкая утилизация».

Решение Aave о расширении было принято раньше, на основе предложения, инициированного ACI (Aave Chan Initiative, организация по governance-предложениям под руководством Marc Zeller) 17 ноября 2025 года. Мотивация предложения была четкой: «восстановить утилизацию WETH, ожидается привлечение 1 млрд долларов притока rsETH». Chaos Labs в январе подтвердил параметры риска, установив LTV для E-Mode на уровне 93% и порог ликвидации на уровне 95%. В принятии решения участвовали ACI, Chaos Labs, LlamaRisk и сообщество Aave, голосовавшее по предложению. Это было решение о расширении, продвигаемое множеством сторон, а не ошибка одного учреждения.

Три месяца спустя рынок вынес вердикт.

В текущем страховом механизме Umbrella от Aave доступные средства составляют около 50 млн долларов, что покрывает лишь 25% от потенциальных убытков в ~195 млн долларов. Порядок поглощения убытков следующий: сначала несут убытки стейкеры aWETH, затем вкладчики WETH пропорционально, далее stkAAVE и казначейство DAO. TVL Aave упал с 26,4 млрд долларов до 19,8 млрд долларов, включая панические изъятия. Утилизация рынка USDT достигла 100% за несколько часов, объем новых займов составил около 300 млн долларов.

На рынке rsETH в SparkLend от Spark текущая замороженная остаточная стоимость составляет 37,3 тыс. долларов, то есть 15,32 токена rsETH. Кошелек 0xb99a после запрета на новые поставки 29 января почти полностью перевел средства в wstETH и weETH, что полностью соответствует прогнозу в governance-посте.

Соучредитель Spark Сэм Макферсон (@hexonaut) 19 апреля отметил: утверждения протоколов об отсутствии exposure к rsETH не означают его реального отсутствия; если у пользователей есть залог на затронутых кредитных рынках, косвенное exposure все же присутствует. У Spark нет прямых потерь, но косвенные риски все еще оцениваются.

Два протокола в один день приняли противоположные решения. Дело не в том, что Spark или Aave приняли правильное решение, а в том, что исходные точки двух систем совершенно разные.

Логика управления рисками Spark запускается вопросом «превышают ли предельные издержки предельную выгоду». Если утилизация ниже порога, концентрация у единственного пользователя превышает норму, скорректированная на риск доходность не достигает цели — при выполнении любого из этих условий актив попадает в список кандидатов на вывод. Это активный, ориентированный на эффективность механизм ужесточения, не зависящий от того, есть ли у самого актива риски безопасности.

Логика Aave запускается «возможностями роста рынка». Утилизация WETH偏低, объем рынка rsETH достаточно велик, E-Mode может привлечь дополнительные средства. С этой отправной точки параметры направлены на расширение: LTV 93%, либеральный лимит поставок, продвижение несколькими governance-субъектами.

Эти два протокола отвечают на совершенно разные вопросы: «Стоит ли продолжать держать этот актив?» или «Сколько прироста может принести этот актив?». Обе эти логики до triggering рискового события являются разумной бизнес-логикой. Судья появляется только после срабатывания.

Результат безопасности Spark имеет еще один уровень поддержки.

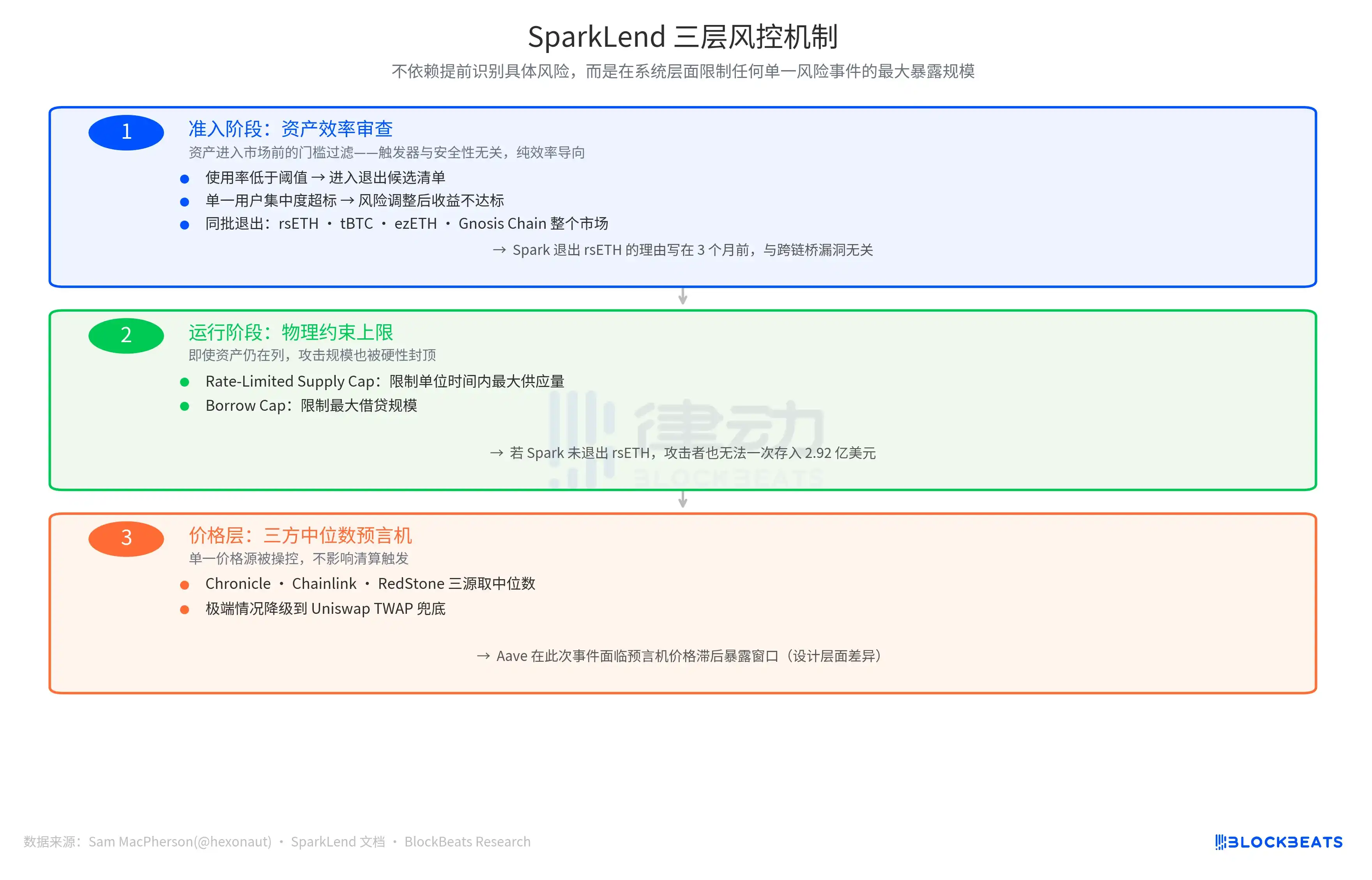

Сэм Макферсон в посте X от 19 апреля об «отказе от rsETH» упомянул: «В SparkLend установлены ограниченные по скорости лимиты на внесение и займ. Его механизм оракула также использует медиану трех источников». Это указывает на еще две линии защиты в системе управления рисками Spark.

Одна — это физические ограничения во время работы. Rate-Limited Supply Cap ограничивает максимальный объем поставок в единицу времени, Borrow Cap ограничивает максимальный объем займов. Значение этих конструкций в том, что даже если бы Spark тогда не отказался от rsETH, злоумышленник не смог бы единовременно внести rsETH на 292 млн долларов, как в Aave — масштаб убытков был бы жестко ограничен.

Другая линия защиты — на уровне ценовой информации: оракул с медианой из 3 источников, берущий медиану из трех независимых источников цен (Chronicle, Chainlink, RedStone), с резервным вариантом на основе TWAP Uniswap в крайних случаях. Компрометация одного источника цен не влияет на triggering ликвидации. Для сравнения, в этом инциденте Aave столкнулся с window of exposure из-за запаздывания цены оракула — это различие на уровне design, а не ошибка исполнения.

Логика design трех линий защиты是一致的: не полагаться на заблаговременное выявление конкретных рисков, а на системном уровне ограничивать максимальный масштаб exposure любого единичного рискового события.

Конечная цифра убытков зависит от плана распределения убытков Kelp DAO. В настоящее время рассматриваются три варианта: социализация убытков среди всех держателей rsETH во всех сетях (масштаб bad debt уменьшается), поглощение убытков только держателями rsETH в L2 (bad debt в Mainnet Aave остается неизменной), откат снапшота (чрезвычайно сложно в реализации). Ответ на этот вопрос появится в ближайшие недели.

Но результат двух философий принятия решений уже можно Quantify: разница составляет около 195 млн долларов. Triggering date одинаков, оно было записано в governance-операциях в один и тот же день.