Автор оригинала: Чжан Яци

Источник оригинала: Wallstreetcn

NVIDIA опубликует квартальный отчет в среду вечером 20 мая по восточному времени США (20 мая). Это ключевое стресс-тестирование для текущего бычьего цикла в области ИИ. Серьезный технический перекуп на рынке полупроводников, высокая концентрация опционных позиций в пользу роста и редкий сигнал "синхронного роста цены акций и подразумеваемой волатильности" значительно усиливают двусторонние риски в этом окне отчетности.

В понедельник Питер Кэллахан, ведущий эксперт Goldman Sachs по технологическому, медийному и телекоммуникационному секторам (TMT), выпустил брифинг под названием "Желтый свет". В нем отмечается, что на прошлой неделе индекс Nasdaq 100 (NDX) и индекс полупроводников Филадельфии (SOX) впервые за квартал зафиксировали недельное падение; доходность 10-летних казначейских облигаций США выросла примерно до 4,60%, что является самым большим недельным приростом за более чем год; цены на нефть восстановились примерно до 109 долларов за баррель; VIX также синхронно вырос. Он указывает, что основное противоречие, с которым сейчас сталкиваются темы ИИ и полупроводников, заключается в следующем: фундаментальные показатели по-прежнему сильны, но техническое давление продолжает накапливаться.

Аналитическое агентство SpotGamma по опционам в своем недавнем отчете указало, что на рынке наблюдается редкая параллельная картина "рост цен на акции при одновременном росте волатильности" — обычно между ними должна быть обратная зависимость. Этот сигнал указывает на то, что трейдеры, гоняясь за ростом, одновременно оплачивают премию за хеджирование от значительных колебаний. Подразумеваемый диапазон колебаний в отчетности NVIDIA в настоящее время достиг 6%, что свидетельствует о высокой концентрации внимания рынка на этом временном узле.

Результаты отчетности и перспективные ориентиры напрямую проверят обоснованность рыночных прогнозов относительно суперцикла вычислительных мощностей для ИИ. Учитывая высокую корреляцию NVIDIA с сектором полупроводников и более широким технологическим сектором, результаты ее отчета, как положительные, так и отрицательные, вызовут широкий резонанс на рынке.

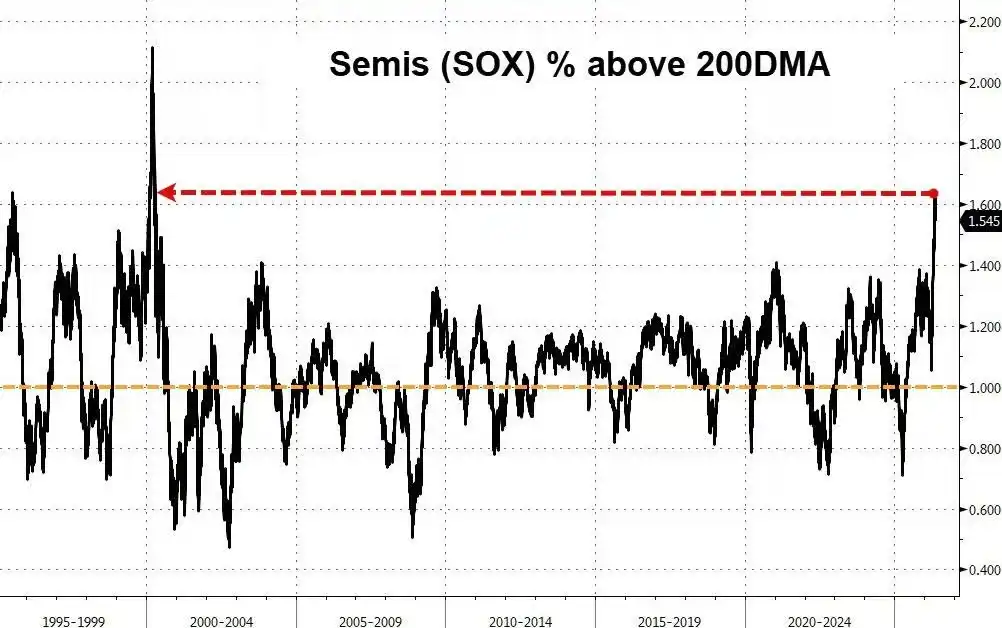

Технический анализ подает самый экстремальный сигнал тревоги с 1999/2000 годов

Масштабы и скорость роста полупроводникового сектора подняли технические показатели до исторически перекупленных уровней.

Данные Goldman Sachs показывают, что индекс SOX с минимумов конца марта вырос примерно на 70%, добавив в пути более 5 триллионов долларов рыночной капитализации. Движущими факторами стали временное ослабление геополитической напряженности, превысившая ожидания корпоративная прибыль — например, AMAT повысил годовые ориентиры больше, чем ожидалось, а заказы на продукты CSCO продемонстрировали рост на 35% в годовом исчислении — а также усиление уверенности инвесторов в спросе на вычислительные мощности для ИИ; прогнозы прибыли в полупроводниковой отрасли с начала года были пересмотрены в сторону повышения более чем на 25%.

Однако Питер Кэллахан особо отмечает, что индекс SOX в настоящее время примерно на 60% превышает свой 200-дневный скользящий средний показатель — это уровень отклонения, невиданный со времен пика пузыря доткомов 1999/2000 годов. Он также отмечает, что в этом году в портфеле Goldman Sachs с высоким фактором импульса уже было 12 торговых дней с однодневными колебаниями более ±5%, что составляет почти 15% от всех торговых дней в году; быстрое расширение продуктов, таких как ETF с плечом и опционы, еще больше усиливает эту двустороннюю эластичность.

"Перед окончанием сезона отчетности на этой неделе (NVIDIA 20 мая) и переходом к летней торговле стоит помнить об этой тактической динамике", — пишет Кэллахан. Торговая площадка Goldman Sachs в целом сохраняет умеренно конструктивную позицию по темам ИИ и полупроводников в среднесрочной перспективе, но на тактическом уровне рекомендует инвесторам сохранять осторожность в отношении технических вызовов.

Отчетность NVIDIA: перспективные ориентиры могут быть важнее результатов за квартал

Рынок по-прежнему оптимистично оценивает фундаментальные перспективы NVIDIA, но недавняя динамика цен уже в некоторой степени отразила часть ожиданий.

Согласно отчету Goldman Sachs с прогнозом по отчетности NVIDIA, аналитики в целом ожидают, что выручка компании в этом квартале превысит рыночные прогнозы примерно на 20 миллиардов долларов — исторически компания обычно превышала ожидания на 2–3%. Рынок больше сосредоточен на перспективных ориентирах на следующий квартал, текущий консенсус-прогноз аналитиков составляет около 860 миллиардов долларов, что означает рост примерно на 9% в квартальном исчислении. Другими ключевыми направлениями внимания являются: остается ли потенциал для дальнейшего роста ориентиров по совокупной выручке центра обработки данных NVIDIA, составляющей около 1 триллиона долларов, а также нарратив об ускорении спроса на "агентный" ИИ для логического вывода (inference) — особенно в отношении ее чисто процессорных (CPU) стоечных продуктов, поставки которых, как ожидается, начнутся во второй половине 2026 года.

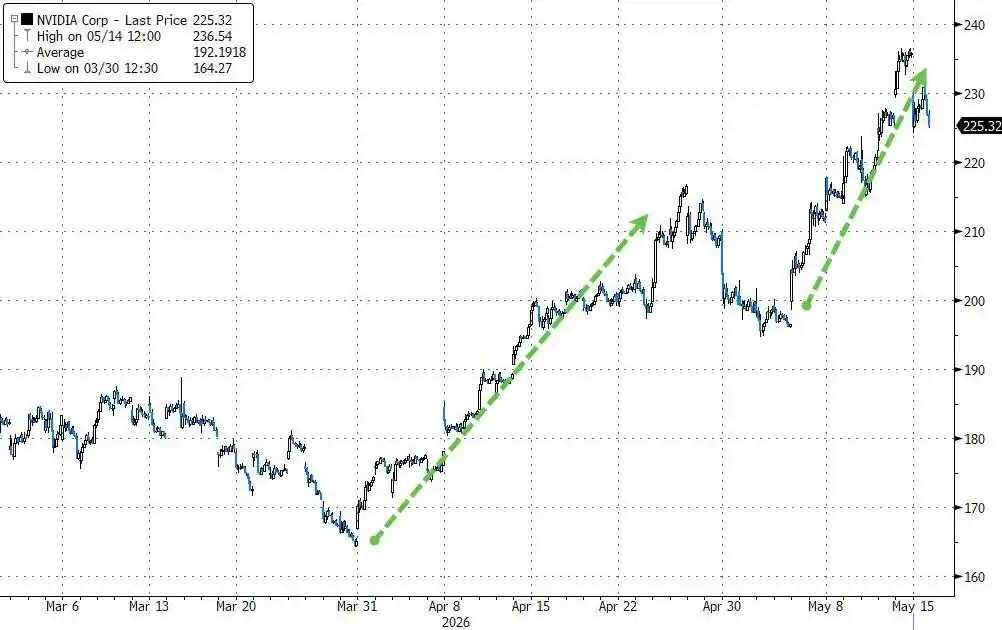

Судя по недавней динамике цен, акции NVIDIA росли в течение 7 торговых дней подряд, прибавив за этот период 20%, что является самым длительным периодом роста за последние два года; с минимумов конца марта совокупная рыночная капитализация выросла примерно на 1,7 триллиона долларов. Однако данные Goldman Sachs также показывают, что в следующий торговый день (T+1) после публикации отчетности в 4 из последних 5 раз акции NVIDIA падали, а с мая 2022 года значительного однодневного роста, вызванного отчетностью, фактически не наблюдалось.

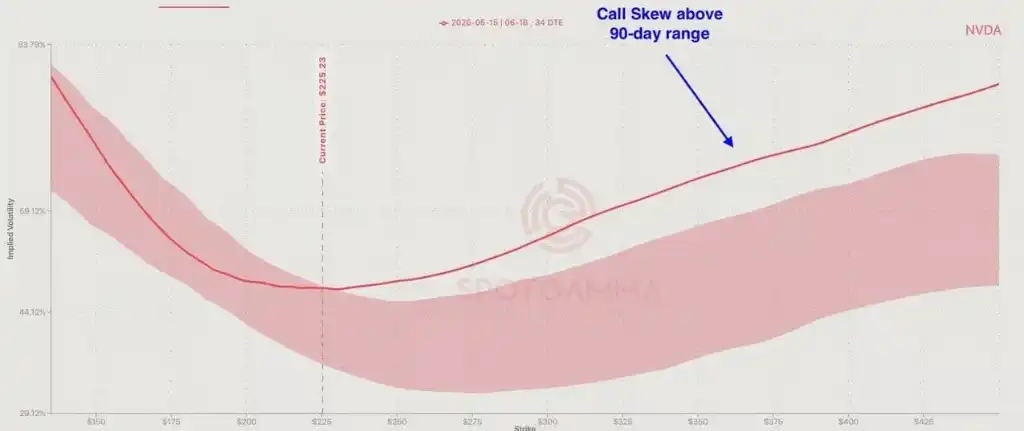

Опционный рынок: экстремальные ставки на рост и хеджирование "хвостовых" рисков размещены одновременно

Структура опционных позиций демонстрирует набор внутренне противоречивых сигналов.

Согласно данным SpotGamma, общее направление позиций по-прежнему крайне смещено в сторону роста, трейдеры продолжают переносить опционы колл на NVIDIA на более высокие страйки, скоу (skew) опционов колл остается в верхней части своего 90-дневного исторического диапазона, в то время как спрос на защиту от падения чрезвычайно ограничен. По данным, на которые ссылается 22V Research, в пятницу номинальный объем сделок по опционам колл на S&P 500 достиг исторического рекорда в 2,6 триллиона долларов, при этом на опционы колл пришлось до 60% от общего объема торгов опционами; индекс относительной силы (RSI) для индекса полупроводников Филадельфии также вырос до самого высокого уровня с марта 2000 года.

В то же время развертывается хеджирование от рисков падения. SpotGamma отмечает, что заметно увеличились крупные структуры опционов пут и их покупка в отношении активов S&P 500 (SPY), ETF на полупроводники (SMH) и связанных с DRAM, причем концентрация идет в диапазоне глубоко вне денег, что указывает на их функцию, скорее как хеджирование "хвостовых" рисков, чем на чисто направленные ставки. "Участники рынка не настроены по-медвежьи в отношении NVIDIA, но подготовка к негативному сценарию не является незначительной", — пишет SpotGamma в отчете. — "Любой сдвиг в направлении почти наверняка быстро затронет более широкий рынок".

SpotGamma добавляет, что акции NVIDIA выросли более чем на 35% с минимумов марта, а текущий масштаб позиций по опционам колл означает, что если отчетность разочарует рынок или вызовет масштабную фиксацию прибыли, это может спровоцировать значительный разворот тренда.

Скрытая угроза ширины рынка: рост поддерживается небольшим количеством акций

На фоне сильных показателей полупроводниковых и крупных технологических акций формируется структурный риск из-за нехватки общего участия в росте американского рынка.

Питер Кэллахан отмечает в отчете, что хотя S&P 500 с начала года вырос примерно на 8%, лишь около 52% компаний, входящих в индекс, показали положительную доходность. Области, заметно отстающие в этом году, включают жилую недвижимость, медицинское оборудование, инжиниринг и строительство без государственных контрактов, федеральные IT-услуги, программное обеспечение и услуги, независимые производители электроэнергии, ресторанные сети, коммерческие брокеры по недвижимости и страховые брокеры, среди прочих.

Кэллахан признается, что, глядя на графики этих секторов, он задается вопросом, отражают ли текущие рыночные показатели общее "здоровье" или же это просто эффект "перераспределения капитала", когда инвесторы вынуждены концентрировать средства на небольшом количестве крупных акций, связанных с ИИ. Команда по производным инструментам на акции Oppenheimer также отмечает, что за последний месяц лишь около пятой части акций, входящих в S&P 500, опережали индекс, индекс дисперсии вырос до самого высокого уровня за более чем год, а подразумеваемая корреляция приближается к минимумам с начала года. Последние данные институционального брокерского подразделения (PB) Goldman Sachs также показывают, что в технологическом секторе в последнее время наблюдаются явные действия по "выводу риска".