Автор: Max.s

Оригинальное название: Война, выходные и заблокированная ликвидность: как атака на Иран показывает, как RWA меняет глобальное торговое время

28 февраля 2026 года (суббота) противовоздушная тревога на Ближнем Востоке нарушила глобальную геополитическую тишину. США и Израиль нанесли тщательно спланированный масштабный авиаудар по целям на территории Ирана.

Время проведения этой военной операции было подобно высокоточному хирургическому вмешательству, что проявилось не только в физических координатах тактических ударов, но и в точном расчете «временных координат» глобальных финансовых рынков. Выбор времени для внезапной атаки в выходные дни, когда традиционные западные финансовые рынки закрыты, был глубоко символичным: это в максимальной степени предотвратило мгновенное распространение панических настроений на фондовых и валютных рынках, а также дало правительствам и центральным банкам целых 48 часов буферного периода для вмешательства и управления рыночными ожиданиями.

Однако в этот искусственно созданный «торговый вакуум» глобальный капитал не стал просто ждать. В то время как котировки золота и нефтяных фьючерсов на CME (Чикагской товарной бирже) застыли на уровне цен закрытия пятницы, а кнопки покупки и продажи различных ETF были принудительно заблокированы системой, настоящие подводные течения бурлили в другой сети, которая никогда не спит. Криптовалютные золотые токены, такие как XAUT (Tether Gold) и PAXG (PAX Gold), пережили пик торговой активности в сетях блокчейна, таких как Ethereum.

Это была не только геополитическая игра, но и стресс-тест «привилегии ликвидности». События атаки крайне резко宣告или всем традиционным финансовым从业者: традиционная финансовая инфраструктура, основанная на расчетах T+1 или T+2, ограниченная рабочими днями и фиксированными торговыми периодами, устаревает. Токенизация реальных мировых активов (RWA) и расчеты через цифровые активы круглосуточно уже не являются социальным экспериментом гиков, а становятся неизбежной тенденцией в борьбе глобального капитала за право定价权和 торговый Alpha.

С точки зрения количественной торговли и хедж-фондов, ядро управления рисками заключается в доступности инструментов хеджирования. После атаки 28 февраля рисковая экспозиция макрохедж-фондов мгновенно взлетела. По обычной логике, нефть и золото являются предпочтительными хеджирующими активами. Но в то субботнее утро десятки тысяч финансовых институтов и профессиональных трейдеров стали «пленниками ликвидности».

Инфраструктура традиционных финансовых рынков построена на графике индустриальной эпохи. Хотя электронная торговля普及了几十年, базовые системы клиринга и расчетов (такие как DTCC, Euroclear и сеть SWIFT) по-прежнему极度依赖中心рализованной пакетной обработки и рабочих часов банков. Когда черный лебедь появляется во внебиржевое время, механизм реакции традиционных рынков полностью заморожен. Инвесторы могут лишь наблюдать, как информация распространяется со скоростью света, а поток средств застывает, как насекомое в янтаре, неспособное пошевелиться.

Такая «намеренная атака вне торговых дней» по сути сжимает всю волатильность рынка и риск гэпа (Gap Risk) в短短 несколько минут открытия в понедельник. Для количественных маркет-мейкеров и высокочастотных торговых机构 этот риск гэпа, который невозможно хеджировать непрерывно, является смертельным. На этапе открытия в понедельник, характеризующемся极度信息ционной асимметрией и истощением ликвидности,极易引发 цепную реакцию давки покупателей или взрыва продавцов.

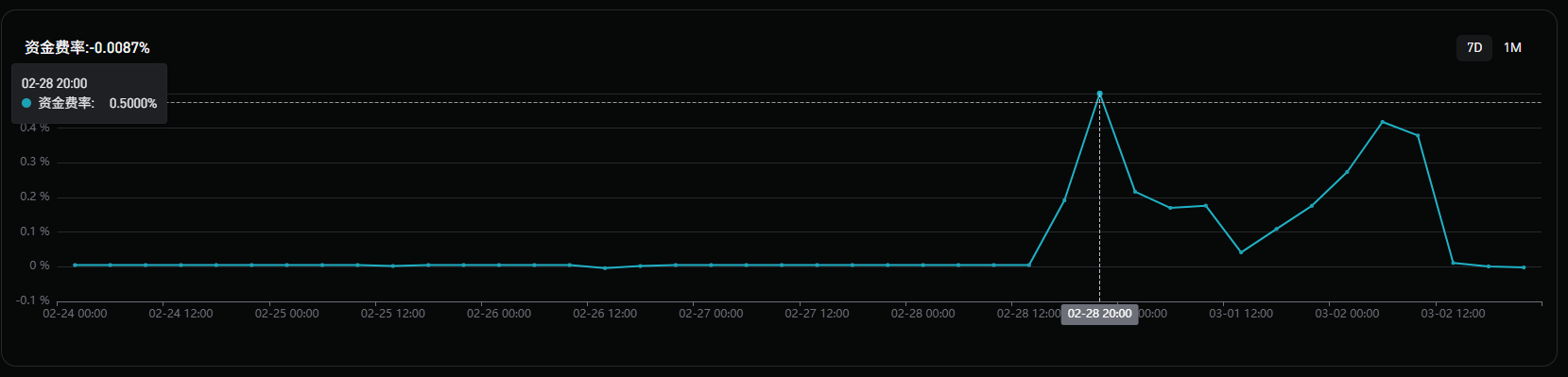

В对比, рынок криптовалют продемонстрировал устойчивость, подобную удару более высокой размерности. В течение нескольких минут после распространения новости об атаке 28 февраля средства хлынули в пулы ликвидности криптосферы. Торговые пары XAUT и PAXG на крупных中心рализованных криптобиржах приняли на себя巨量级别的 спрос на убежище. Как показано на рисунке, финансирование (лонги платят шортам) в тот день достигло 0,5%.

Мы можем четко увидеть эту плавную и крутую кривую роста стоимости в данных on-chain: нет закрытия торгов, нет остановок, нет слепого ящика гэпа на открытии. Цены золотых токенов on-chain следовали за каждым обновлением сводок с фронта, осуществляя непрерывное定价 в миллисекундах. До открытия CME в понедельник цена XAUT on-chain уже завершила адекватное ценовое обнаружение.

Это привело к极具颠覆性的 финансовому явлению: право定价权 традиционных сырьевых товаров впервые в истории во время крупного геополитического кризиса временно перешло к рынку цифровых активов.

Когда 2 марта (понедельник) открылись азиатские торги в ранние часы, традиционные рынки спотого золота и фьючерсов резко выросли. В эти выходные XAUT перестал быть теневым активом для GLD (SPDR Gold ETF) или фьючерсов COMEX. Напротив, токены on-chain в некотором смысле стали «ценовым оракулом» для открытия Уолл-стрит в понедельник. Осторожные арбитражеры использовали эти 48 часов разницы во времени, чтобы создать достаточные позиции on-chain, и в момент открытия традиционного рынка в понедельник сгладили разницу в ценах между двумя мирами за счет арбитража по высокой базе.

Всплеск торговли золотыми токенами в эти выходные揭示了最核心ную ценностную proposition активов RWA: расширение временного измерения ликвидности.

В предыдущих нарративах преимущества RWA часто сводились к снижению порога входа, фрагментации права собственности или повышению прозрачности. Но для профессиональных финансовых从业者最大的 привлекательность RWA заключается в базовой логике «расчеты как клиринг» T+0 и механизме работы 7x24x365 без перерывов.

Представьте, если бы в выходные разразился не авиаудар на Ближнем Востоке, а дефолт по суверенному долгу какой-либо страны, крах крупного банка или внезапное чрезвычайное снижение процентной ставки центрального банка, традиционные институты могли бы лишь пассивно нести巨大的 риск экспозиции до открытия в понедельник. А если бы казначейские облигации, валюта и даже核心ные фондовые индексы были бы токенизированы и на блокчейне были созданы充足的 пулы ликвидности, то институциональные инвесторы могли бы в момент возникновения риска немедленно завершить хеджирование рисков и замену активов через смарт-контракты.

В этом事件 не только золото, но и сеть обмена между стейблкоинами и нативными криптоактивами выступила в роли супермагистрали для убежища средств. В традиционной финансовой системе跨国ные и меж机构ные переводы средств требуют сложных подтверждений корреспондентских банков и множественных проверок соответствия, занимая甚至 дни. В on-chain, хеджирующие позиции на миллиарды долларов могут быть обменены атомарно в течение времени одного блока (12 секунд в Ethereum) без какого-либо риска контрагента.

Для Уолл-стрит выходные в конце февраля 2026 года стали глубоким уроком для исследований и инвестиций. Ранее многие традиционные институты занимали выжидательную позицию в отношении запуска BlackRock фонда токенизированных казначейских облигаций BUIDL, роста протоколов RWA, таких как Ondo Finance, считая это merely трюком для привлечения存量 средств криптосферы. Но события атаки доказали, что перед лицом экстремального черного лебедя, премия ликвидности, предоставляемая токенизированными активами, является硬核ным Alpha, который не может заменить ни одна优秀的 количественная модель.

Количественные фонды больше не будут удовлетворяться торговыми интерфейсами, предоставляемыми CME или Nasdaq, они будут массово подключать API к DEX on-chain и пулам торговли RWA с институциональным уровнем соответствия. Чтобы捕捉 торговые возможности «несинхронного времени» в выходные и праздничные дни, создание跨界ных арбитражных моделей, охватывающих TradFi и DeFi, станет стандартной конфигурацией для ведущих хедж-фондов.

Когда брокеры и маркет-мейкеры осознают, что巨量交易需求和 комиссионные прибыли утекают в сеть блокчейна по выходным, движимые прибылью, они主动 станут поставщиками ликвидности для активов on-chain. В будущем крупные маркет-мейкеры, такие как Jane Street, Jump Trading, будут не только обеспечивать ликвидность для ETF в рабочие дни, но и注入 ликвидность в круглосуточные пулы активов RWA по выходным.

Начиная с высокостандартизированных товаров, таких как золото и нефть, постепенно распространяясь на краткосрочные казначейские обязательства,优质 корпоративные облигации и даже индексы акций США. Носитель финансовых активов彻底 переместится с бухгалтерских книг трастовых компаний и клиринговых палат на распределенные реестры. Не будет占用 средств по T+2, не будеттревоги выходных из-за продаж в避险 в пятницу днем, глобальный капитал真正实现无缝ное流通ование в физическом времени и пространстве.

«Деньги никогда не спят» был одним из самых известных лозунгов Уолл-стрит, но реальность такова, что традиционная Уолл-стрит не только спит, но и имеет выходные и государственные праздники. Пушечный огонь 28 февраля 2026 года жестоко доказал, что перед лицом все более сложной и непредсказуемой глобальной макросреды, разорванное торговое время и заблокированная ликвидность сами по себе являются最大的系统性风险.

Процесс ценового обнаружения,主导ованный цифровыми активами, такими как XAUT, в эти выходные, возвестил о кончине традиционной клиринговой системы. RWA — это не просто перенос активов реального мира в блокчейн, это перестройка временных законов финансового运转 с помощью кода. Для количественных аналитиков, трейдеров и финансовых инженеров будущее поле битвы больше не ограничивается 5 днями в неделю и 8 часами в день. Тот, кто率先 овладеет инфраструктурой торговли и расчетов с круглосуточными цифровыми активами, сможет в следующую внезапную ночь черного лебедя схватить глобальный рынок за горло.

Twitter:https://twitter.com/BitpushNewsCN

Группа общения比推 TG:https://t.me/BitPushCommunity

Подписка比推 TG: https://t.me/bitpush