Автор: Lucas Shin

Компиляция: Deep Tide TechFlow

Введение Deep Tide: Рынок рассматривает Circle как фонд денежного рынка, чувствительный к процентным ставкам, но объем предложения USDC вырос на 72% даже при снижении процентных ставок. Еще более упускается из виду волна коммерции AI-агентов: McKinsey прогнозирует, что к 2030 году объем транзакций агентов достигнет 3-5 триллионов долларов, а из 106 миллионов долларов объема транзакций по стандарту HTTP-платежей x402 99,6% рассчитываются с помощью USDC. Это структурная возможность для спроса на стейблкоины, а не чистая ставка на процентные ставки.

Заключение:

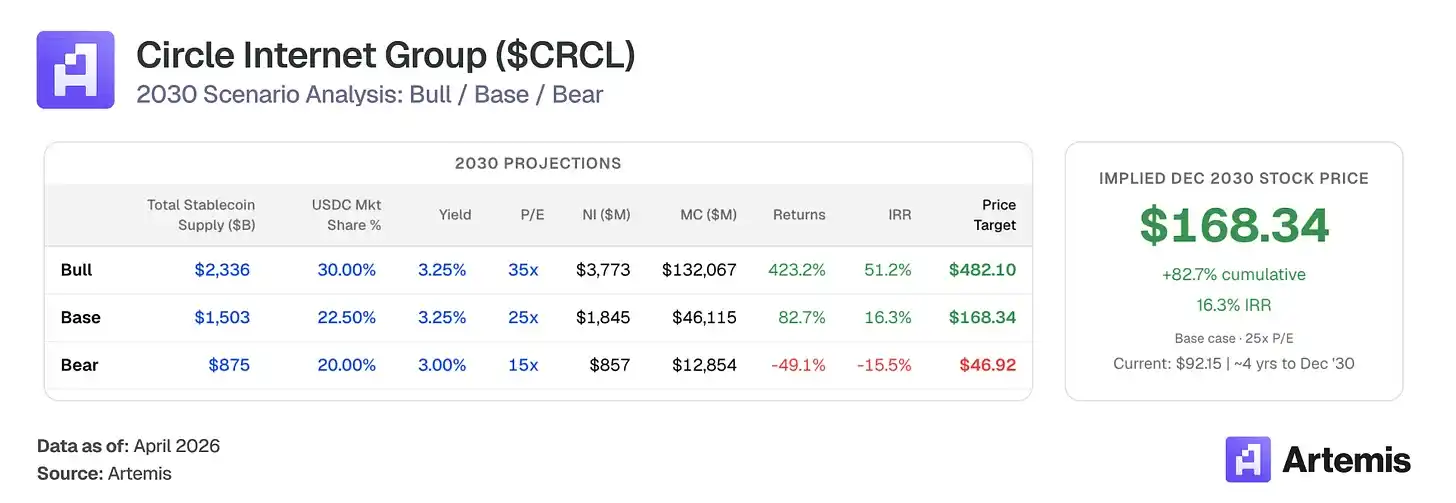

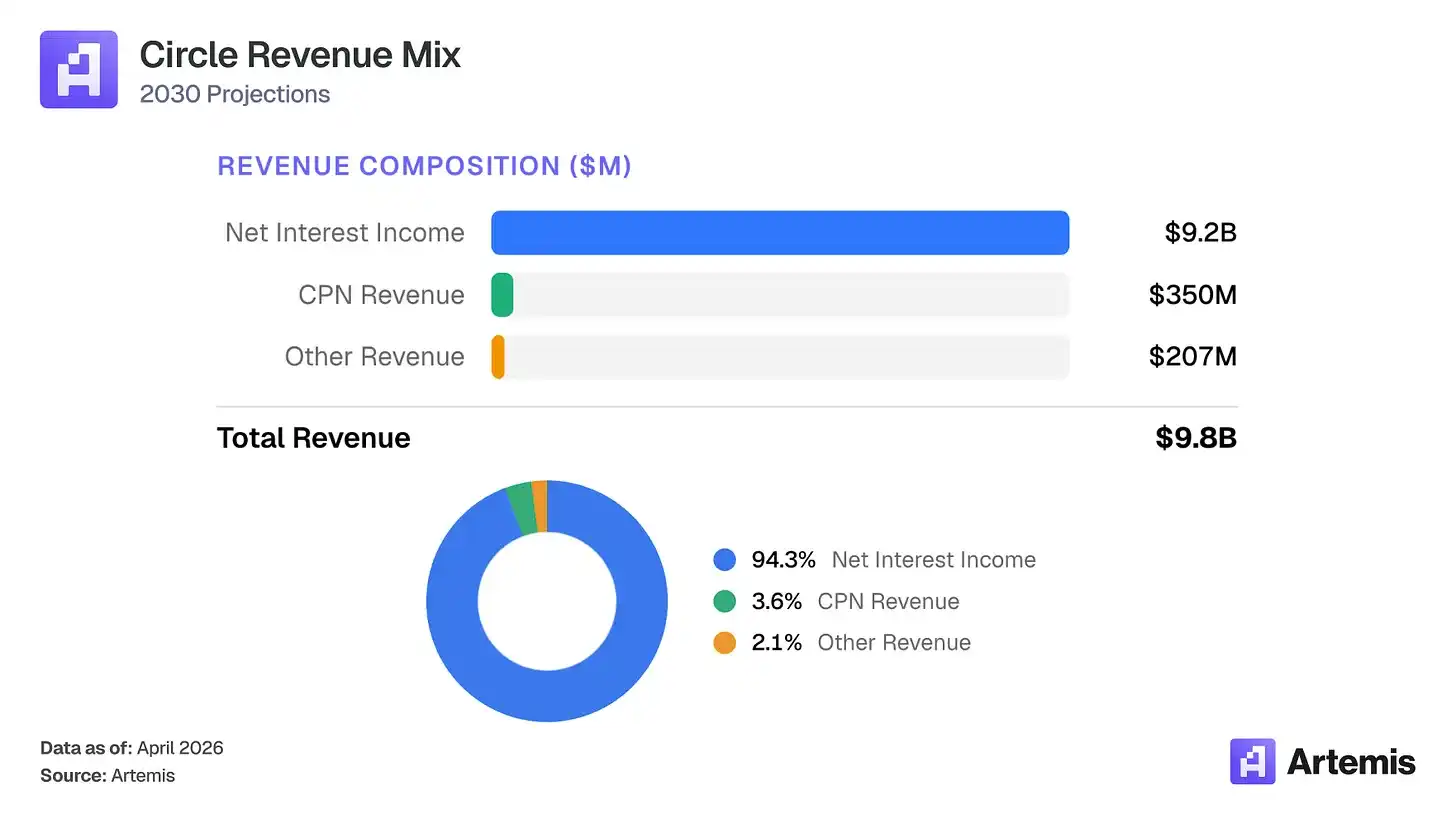

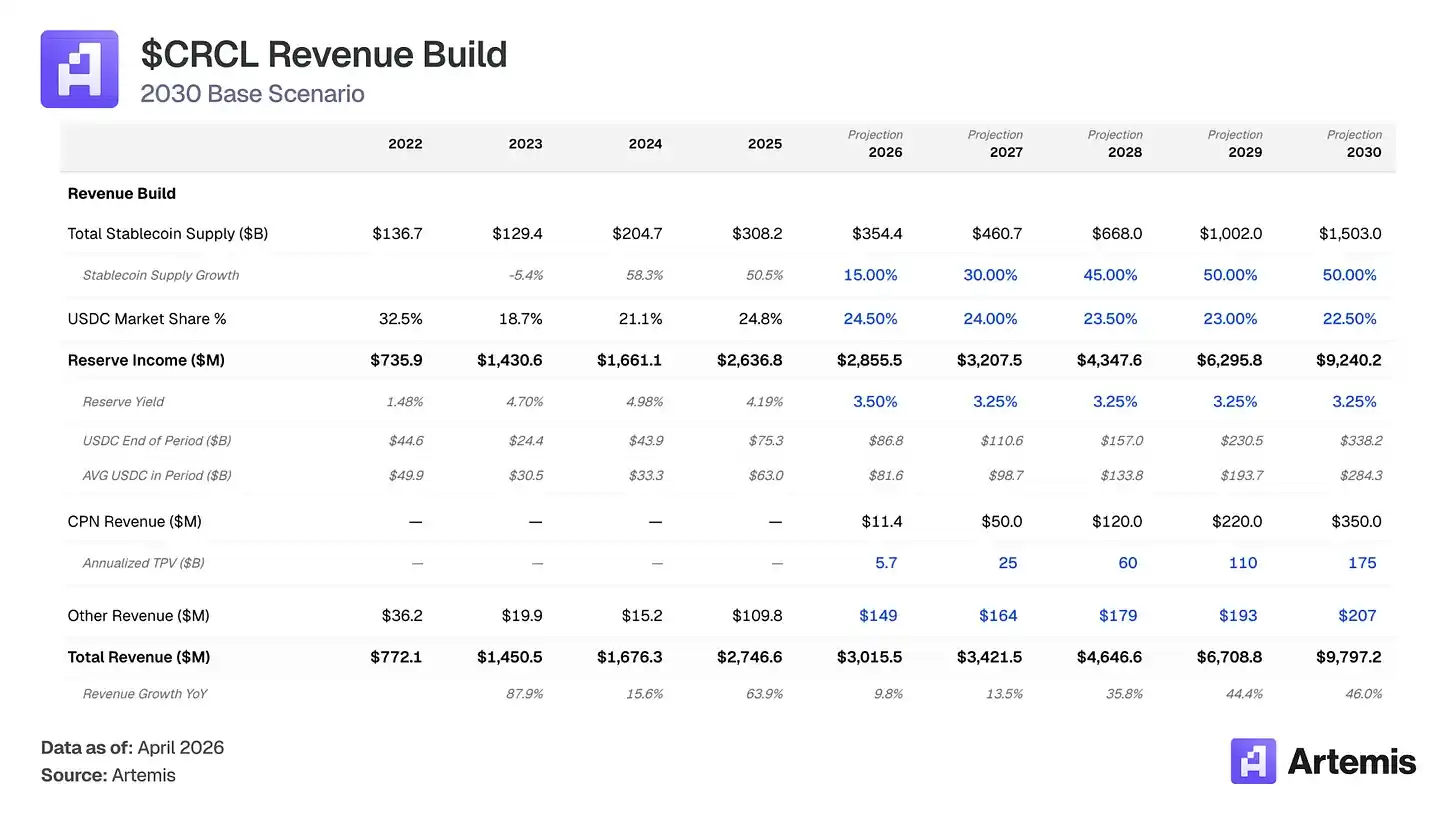

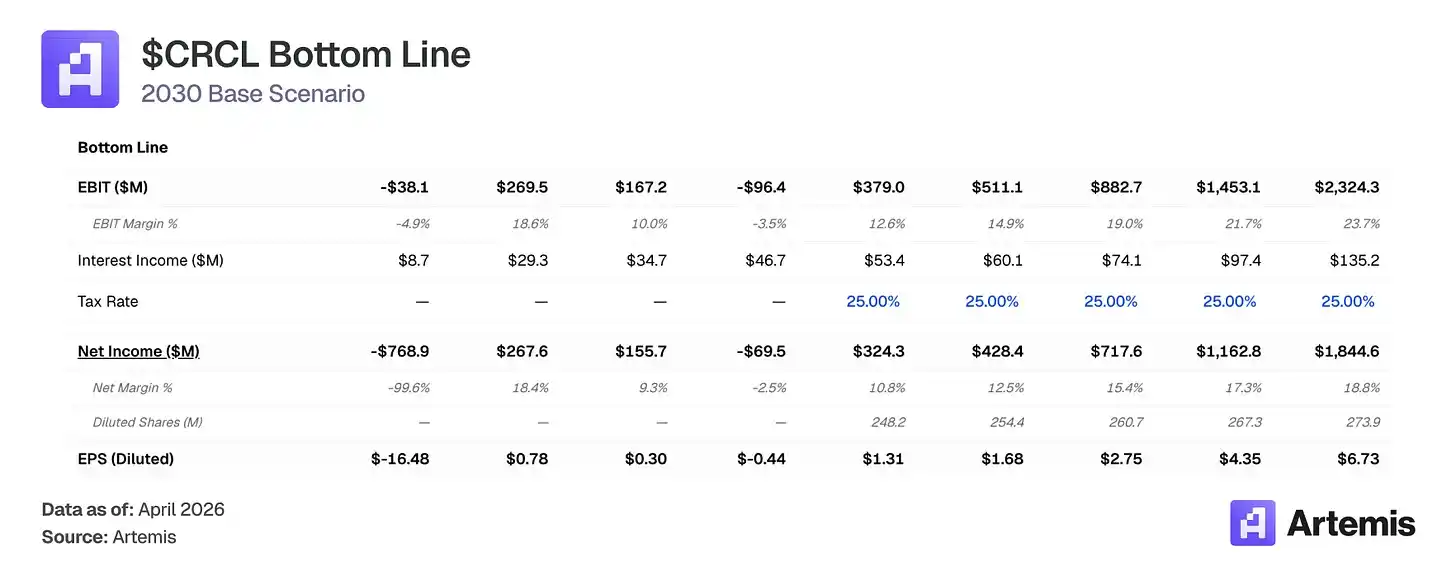

Рынок оценивает Circle как фонд денежного рынка, чувствительный к процентным ставкам — ставку на ставки ФРС, сидящие на блокчейн-треке. Мы считаем, что эта структура неправильно оценивает бизнес. Объем предложения USDC вырос на 72% в 2025 году до 75,3 миллиарда долларов, даже когда ФРС снизила ставки на 75 базисных пунктов во втором полугодии, что указывает на то, что спрос на USDC обусловлен реальным внедрением полезности, а не чисто поиском доходности. Наш базовый сценарий прогнозирует, что общий рынок стейблкоинов достигнет примерно 1,5 триллиона долларов к 2030 году, при среднем объеме предложения USDC в 284 миллиарда долларов. Даже при ожидаемом сжатии доходности резервов, мы прогнозируем, что доход Circle от резервов вырастет до 9,2 миллиарда долларов к 2030 году (примерно в 3,5 раза по сравнению с 2025 годом), поскольку рост предложения перевешивает сжатие ставок. В сочетании с расширением платежной сети Circle (CPN) до 350 миллионов долларов дохода и снижением стоимости дистрибуции с 60% до 55%, наш базовый сценарий прогнозирует общий доход в 9,8 миллиарда долларов и чистый доход около 1,8 миллиарда долларов в 2030 году.

Несколько попутных ветров поддерживают эту траекторию: закон GENIUS создает федеральные рамки для стейблкоинов, благоприятные для合规ных эмитентов; платежная сеть Circle набирает первоначальную популярность, с 55 зарегистрированными финансовыми учреждениями и годовым объемом обрабатываемых транзакций в 5,7 миллиарда долларов, обеспечивая поток дохода на основе транзакций, диверсифицируя от чувствительности к процентным ставкам; внедрение стейблкоинов расширяется в B2B-платежах, трансграничных расчетах и DeFi. Наш базовый сценарий дает прогнозируемую EPS на 2030 год в размере 6,73 доллара, что подразумевает целевую цену около 168 долларов при конечном P/E в 25 раз, с потенциалом роста на 83% относительно текущего уровня.

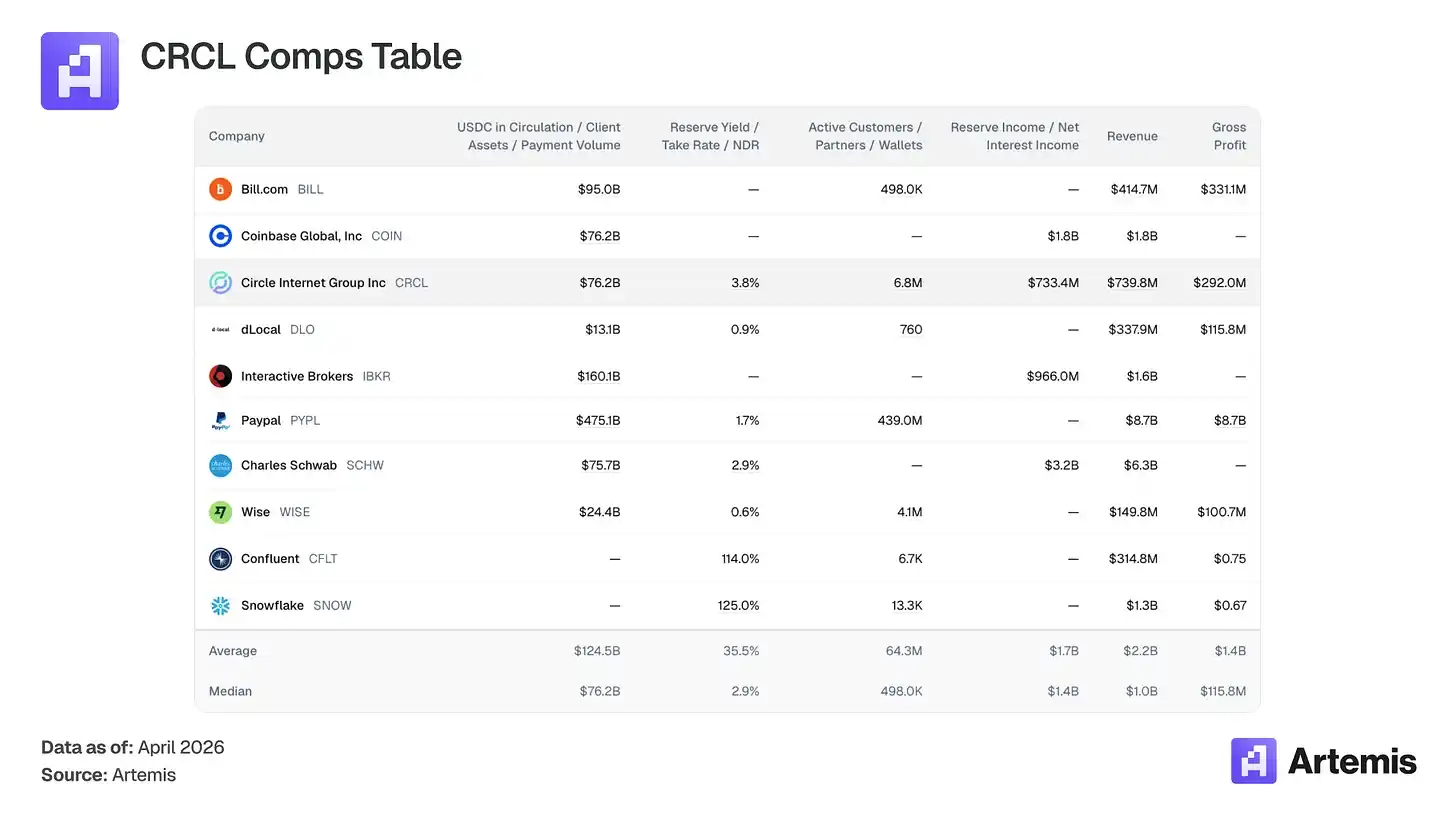

Таблица сопоставимых компаний:

Нет прямых публичных компаний-аналогов в качестве эмитентов стейблкоинов, монетизирующих через резервный флоат. Наш набор аналогов охватывает компании, разделяющие ключевые атрибуты бизнеса Circle: модель дохода на основе флоата (Charles Schwab, Interactive Brokers), инфраструктура цифровых платежей (PayPal, Wise, dLocal, Bill.com), нативные криптоплатформы (Coinbase), а также высокорослая инфраструктура с экономикой, основанной на использовании (Snowflake, Confluent).

Что делает Circle?

Circle является эмитентом USDC, стейблкоина, привязанного к доллару США в соотношении 1:1. Когда пользователи вносят доллары, USDC выпускается; когда они погашают, он уничтожается. Доходность, генерируемая резервами (примерно 43% обратного РЕПО, 43% казначейских векселей и 14% банковских депозитов, находящихся под хранением в Bank of New York Mellon и управляемых через фонд BlackRock USDXX), составляет основной доход Circle.

Ключевые детали структуры затрат: Coinbase作为主要分销ционный партнер USDC, получает 100% дохода от резервов USDC, хранящихся на ее платформе, и 50% от USDC вне платформы. В 2025 году Coinbase получила 1,35 миллиарда долларов, что составило 51% общего дохода от резервов Circle. Включая не-Coinbase дистрибуцию (12,7%), общие дистрибьюторские затраты поглотили около 61% дохода от резервов, оставив 39% валовой прибыли. Мы прогнозируем, что к 2030 году дистрибьюторские затраты снизятся с 60% до 55%, поскольку растет не-Coinbase дистрибуция, новые финансовые учреждения, банки и партнеры по хранению договариваются о более выгодных сделках, чем текущее соглашение Circle с Coinbase. Это увеличит валовую прибыль с 39% до 54%.

Помимо дохода от резервов,最重要的 рычаг роста Circle — это платежная сеть Circle (CPN), трансграничная B2B-расчетная сеть, построенная на USDC. CPN, запущенная в мае 2025 года, зарегистрировала 55 финансовых учреждений, с годовым объемом обрабатываемых транзакций в 5,7 миллиарда долларов, и имеет pipeline из 500 финансовых учреждений. Мы прогнозируем, что к 2030 году CPN расширится до объема обработки транзакций в 175 миллиардов долларов, с комиссией 0,2% (соответствует смешанной трансграничной ставке в 20 базисных пунктов), генерируя 350 миллионов долларов дохода на основе транзакций. Этот доход не чувствителен к процентным ставкам, диверсифицируя Circle от чистой зависимости от доходности резервов. Дополнительные линии дохода (в нашей модели называемые "прочий доход") включают CCTP (47-50% объема транзакций межсетевого моста) и инфраструктуру расчетов Arc, которые мы прогнозируем в совокупности на сумму 207 миллионов долларов к 2030 году.

Тезис №1: Рост предложения перевешивает сжатие ставок

Общий рынок стейблкоинов вырос с примерно 1370 миллиардов долларов в 2022 году до примерно 3080 миллиардов долларов в 2025 году. Наша модель прогнозирует около 1,5 триллиона долларов к 2030 году, с совокупным годовым темпом роста (CAGR) около 37%. Сегодня общее количество стейблкоинов в обращении (около 3,16 триллиона долларов) представляет собой примерно 1,4% от денежной массы M2 США в 227 триллионов долларов. Наш базовый сценарий подразумевает около 6%, что все еще является умеренной долей долларовой ликвидности.

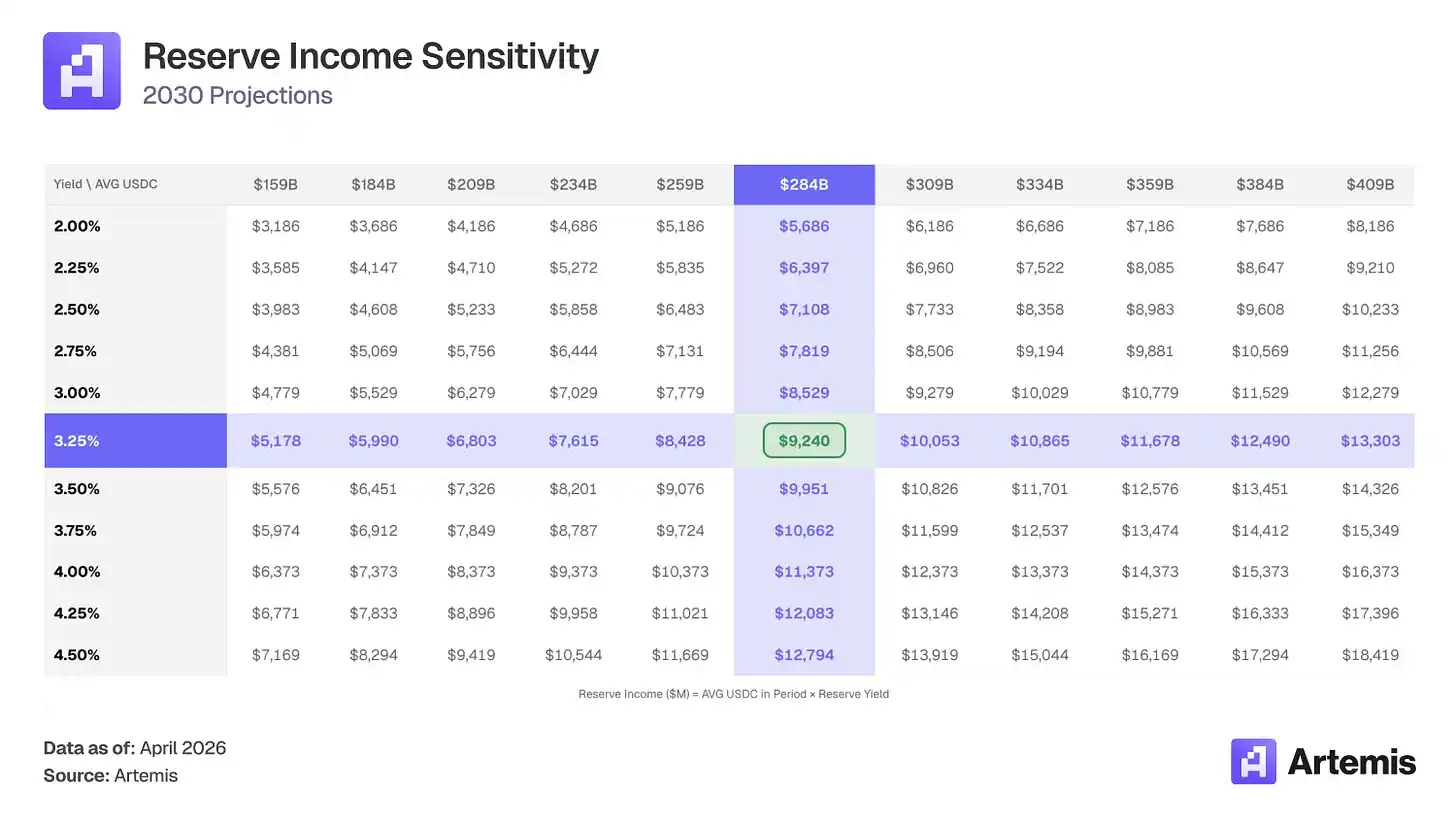

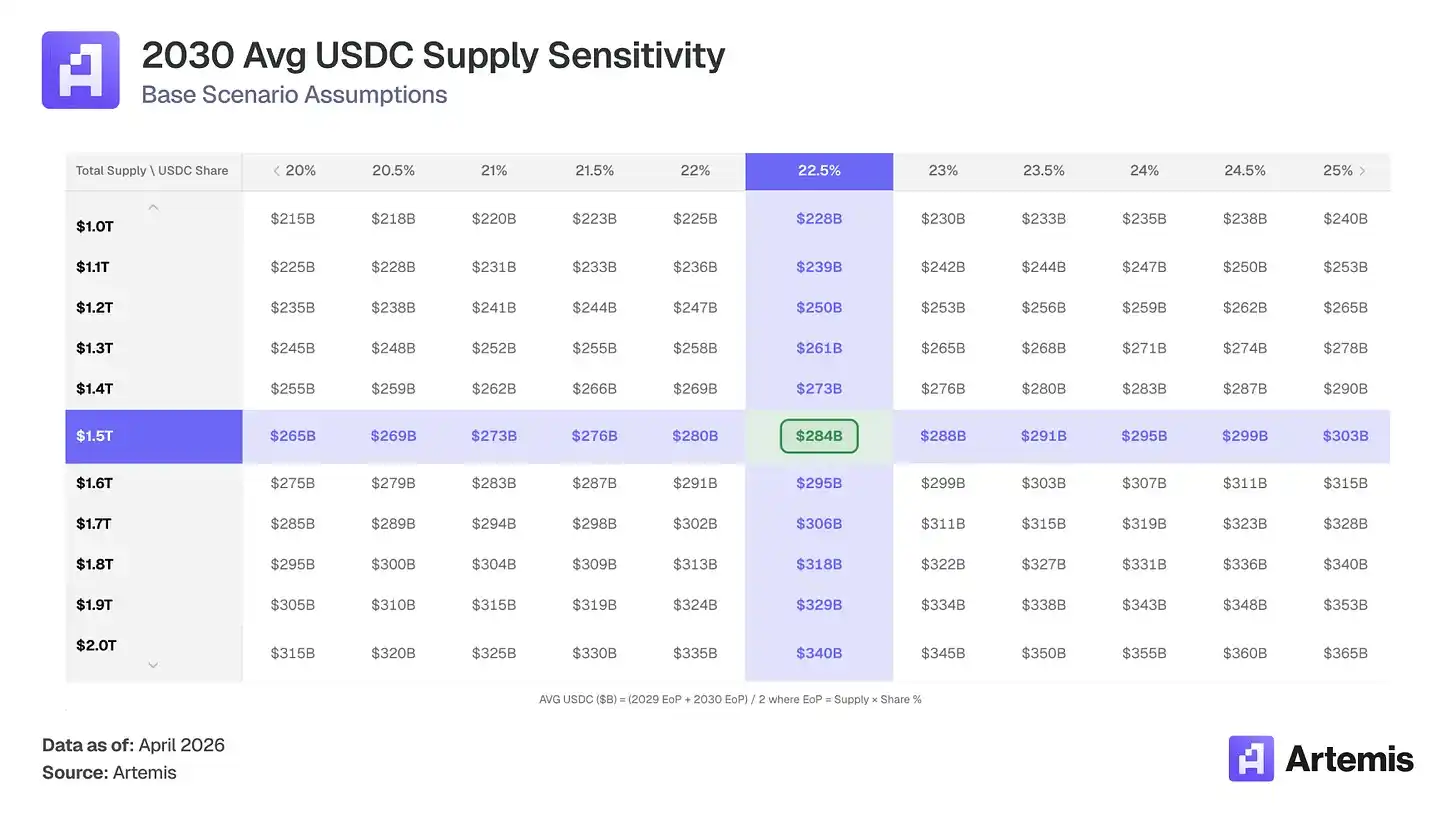

Мы прогнозируем, что USDC сохранит долю рынка в 22-25% (умеренное снижение с 24,8%, поскольку white-label и банковские стейблкоины разделяют пространство), что к 2030 году даст объем предложения USDC в 338 миллиардов долларов (рост примерно в 4,5 раза по сравнению с сегодняшним днем). Проще говоря, даже если эффективная доходность резервов Circle снизится, чистый рост объема USDC с 63 миллиардов долларов до в среднем 284 миллиардов долларов достаточен для компенсации. В результате доход от резервов вырастает в 3,5 раза, с 2,64 миллиарда долларов до 9,24 миллиарда долларов.

Тезис №2: Коммерция агентов подстегнет следующую волну спроса на стейблкоины

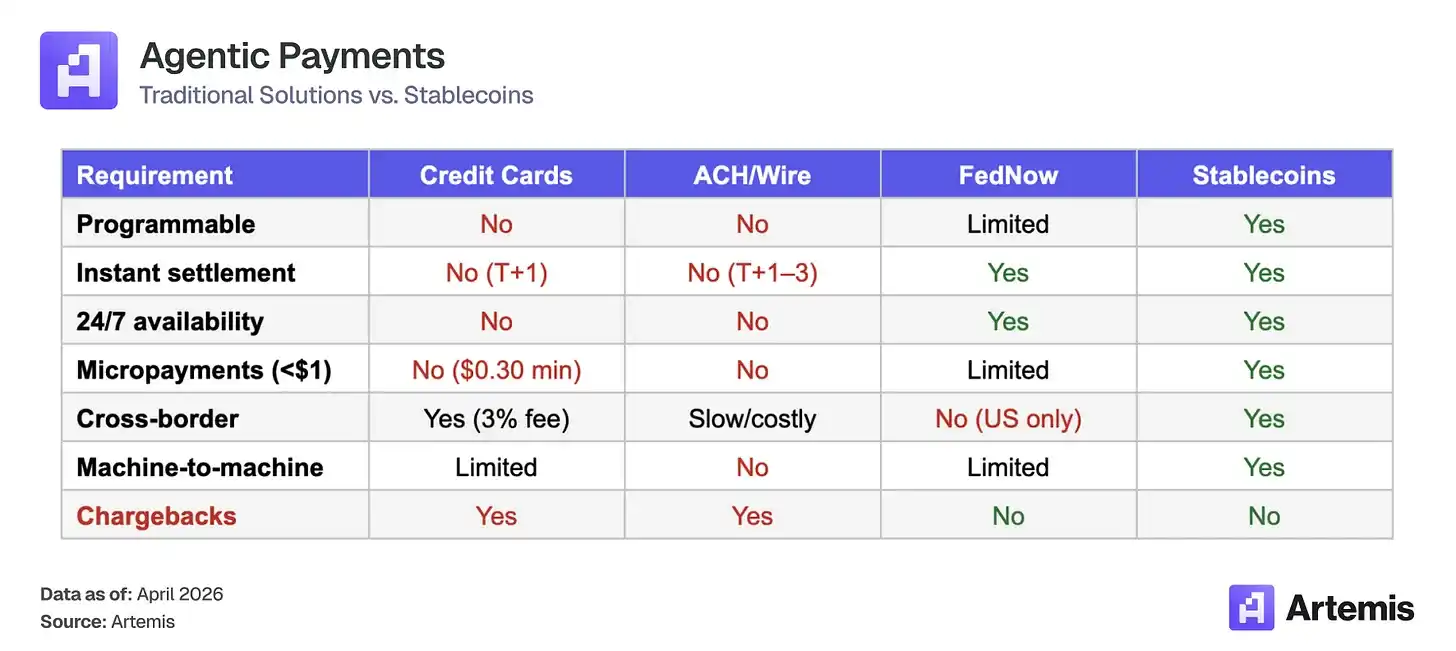

AI-агенты движутся по траектории к автономному выполнению транзакций к 2030 году. McKinsey прогнозирует глобальные продажи коммерции агентов в размере 3-5 триллионов долларов к 2030 году; Gartner оценивает, что к 2028 году AI-агенты будут посредничать в более чем 15 триллионах долларов B2B-закупок. Эти транзакции структурно требуют стейблкоин-треков:

Стейблкоины становятся расчетным слоем для этой emerging экономики агентов, и бизнес-модель Circle масштабируется вместе с ней. Когда агенты держат USDC в кошельках для финансирования автономных транзакций, Circle получает доходность за каждый доллар, сидящий в этих резервах. Чем больше пул USDC, удерживаемый агентами, тем больше база дохода, независимо от частоты транзакций.

USDC уже является стейблкоином по умолчанию для платежей агентов. За шесть месяцев с момента обретения популярности стандарта платежей x402 (нативные HTTP-микроплатежи) было обработано около 17,7 миллионов транзакций на объем около 106 миллионов долларов. Более 99,6% этого объема транзакций рассчитывались с помощью USDC.

Преимущество первопроходца создает маховик: новые разработчики по умолчанию поддерживают USDC, поскольку он имеет самую глубокую интеграцию, что further углубляет интеграцию, затрудняя прорыв альтернативам. Мы не моделируем доход от агентов в базовом сценарии, но спрос агентов встроен в наш бычий сценарий как опцион роста. Если 1-2% нижнего прогноза McKinsey в 3 триллиона долларов рассчитываются на треке USDC, это implies дополнительный инкрементный флоат USDC в размере 30-60 миллиардов долларов в кошельках агентов, от которого Circle может получать пассивную доходность.

Оценка и сценарии

Мы оцениваем CRCL с использованием terminal P/E от прогнозируемой EPS на 2030 год. Наш базовый сценарий генерирует чистый доход в 1,84 миллиарда долларов при 273,9 миллионах разводненных акций, что дает EPS в 6,73 доллара. 25-кратный terminal P/E — выше средневзвешенного значения comparable, отражая структурную траекторию роста Circle, диверсификацию дохода за счет CPN и regulatory moat — подразумевает около 168 долларов за акцию в 2030 году, с потенциалом роста на 83% относительно текущего уровня.

25-кратная multiple находится между примерно 15-кратной JPMorgan (JPM) и примерно 38-кратной Coinbase, что подходит для бизнеса высокорослой инфраструктуры, переходящего к recurring, нечувствительному к ставкам доходу.

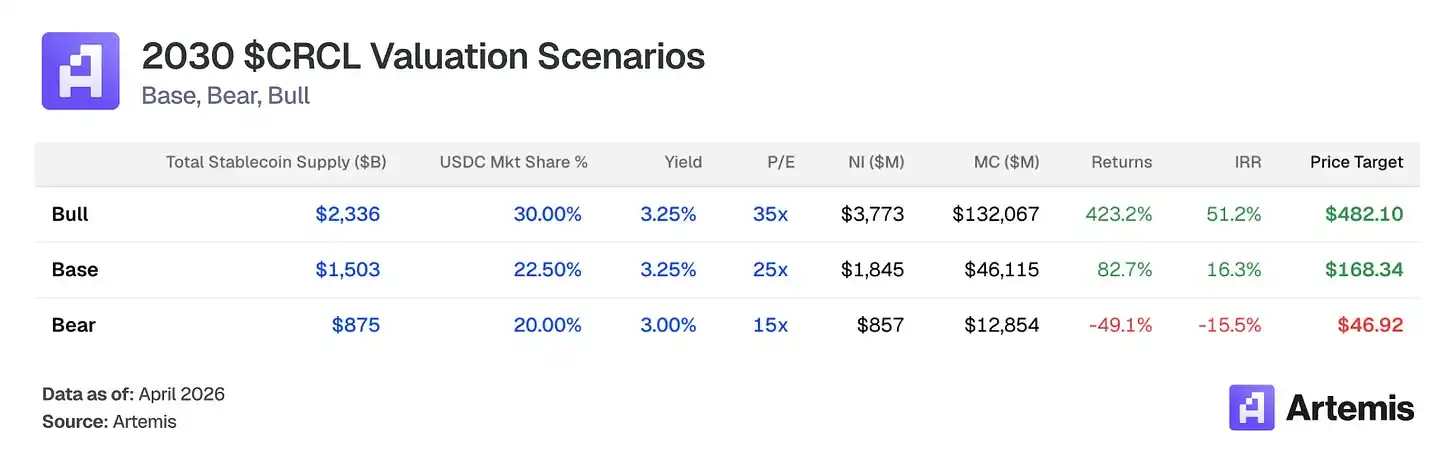

Базовый сценарий: Предполагает continued выполнение роста предложения и расширения CPN, рынок стейблкоинов достигает 1,5 триллиона долларов, USDC сохраняет долю в 22,5%. Дистрибьюторские затраты умеренно снижаются до 55%, поскольку новые партнеры-финансовые учреждения договариваются о более низкой доле дохода. Выход с 25-кратным terminal P/E от прогнозируемой прибыли на 2030 год подразумевает целевую цену в 168,34 доллара — потенциал роста 82,7%, внутренняя норма доходности (IRR) 16,3%.

Бычий сценарий: Предполагает ускоренное внедрение стейблкоинов, движимое благоприятным регулированием, сетевыми эффектами CPN и широким доступом к традиционным финансам. Общий рынок стейблкоинов достигает 2,3 триллиона долларов, USDC получает 30% долю. Дистрибьюторские затраты сжимаются до 50% по мере расширения происхождения не от Coinbase. Выход с 35-кратным terminal P/E от прогнозируемой прибыли на 2030 год подразумевает целевую цену в 482,10 доллара — потенциал роста свыше 423%, IRR 51,2%.

Медвежий сценарий: Предполагает замедление внедрения стейблкоинов, white-label стейблкоины размывают долю рынка USDC до 20%, снижение ставок сжимает доходность резервов до 2,75%. Привлекательность CPN разочаровывает. Выход с 15-кратным terminal P/E от прогнозируемой прибыли на 2030 год подразумевает целевую цену в 46,92 доллара — падение примерно на 49%, IRR -15,5%.

Мы считаем, что качество менеджмента выше среднего в области криптоинфраструктуры, с особыми преимуществами в навигации по регулированию (лицензии денежного перевода (MTL) в 49 штатах, первый compliant с MiCA).

Джереми Аллер (Jeremy Allaire) co-основал Circle в 2013 году и является председателем и CEO. Серийный предприниматель (бывший CTO Macromedia, основатель/CEO Brightcove, IPO в 2012), Аллер перевел Circle от потребительского платежного приложения к инфраструктуре стейблкоинов, запустив USDC с Coinbase в 2018 году, после неудачи SPAC в 2022 году, завершил традиционное IPO на NYSE в июне 2025 года.

Хит Тарберт (Heath Tarbert) занимает должность президента, повышен с главного юрисконсульта в январе 2025 года. Тарберт является бывшим председателем и CEO CFTC (2019-2021), бывшим помощником министра финансов США и бывшим главным юрисконсультом Citadel Securities.

Джереми Фокс-Гин (Jeremy Fox-Geen) является CFO с января 2021 года. Бывший CFO iStar/Safehold (публичные REITs на NYSE) и CFO североамериканского бизнеса McKinsey & Company. Он курировал IPO Circle и управляет архитектурой резервов, поддерживающей обращение USDC на сумму свыше 70 миллиардов долларов.

Данте Диспарте (Dante Disparte) занимает должность главного стратегического директора и главы глобальной политики и операций. Бывший основатель-исполнитель и заместитель председателя ассоциации Diem (стейблкоин-проект Meta), он руководит глобальной регуляторной стратегией, государственной политикой, расширением рынка и международными операциями.

Основной риск менеджмента — концентрация основателя и высокая доля стимулирования акционерным капиталом после IPO (свыше 500 миллионов долларов в 2025 году, включая ускорение RSU на 424 миллиона долларов, связанное с IPO), которое в настоящее время нормализуется (стимулирование акционерным капиталом в третьем и четвертом кварталах 2025 года составило 59 и 48 миллионов долларов соответственно, стремясь к годовому run-rate ниже 200 миллионов долларов).

White-label и нативные стейблкоины платформ

Наиболее недооцененный риск доли рынка USDC — это запуск платформами, основными приложениями и финансовыми учреждениями стейблкоинов под собственным брендом. Например, Hyperliquid имеет USDH, PayPal имеет PYUSD, Fidelity имеет FIDD, JPMorgan имеет JPMD. Недавно Polymarket запустил "Polymarket USD", который в настоящее время является оберткой USDC, но может быть шагом к независимому расчету. Если эта стратегия расширится в рамках закона GENIUS, USDC может постепенно потерять статус расчетного трека по умолчанию. Наш базовый сценарий прогнозирует снижение доли рынка USDC до 22,5% к 2030 году, чтобы отразить эту фрагментацию.

Смягчающие факторы: White-label стейблкоины все еще требуют инфраструктуры резервов, compliance и — что наиболее важно — глубокой ликвидности. Учитывая, что USDC интегрирован на каждой крупной бирже, в кошельке, DeFi-протоколе и мосте, новые брендовые стейблкоины должны воспроизвести эту сеть ликвидности, чтобы функционировать как независимые расчетные токены. Глубокие пулы ликвидности, tight спреды и мгновенная погашаемость нелегко запустить, фрагментированные стейблкоины со слабой ликвидностью создают худшее исполнение для пользователей. Затраты на переход к запуску полностью независимых резервов достаточно высоки, и большинство платформ, возможно, никогда не завершат переход.

Чувствительность к ставке ФРС

Доход от резервов напрямую привязан к процентным ставкам. Прогнозируемый средний объем USDC в 284 миллиарда долларов в 2030 году, каждое снижение ставки на 100 базисных пунктов эквивалентно потере около 2,8 миллиарда долларов общего дохода от резервов. Если ФРС снизит ставки до 2,0%, прогнозируемый доход от резервов в 2030 году упадет на 25-30% по сравнению с нашим базовым сценарием. Рынок прогнозов Kalshi в настоящее время оценивает вероятность дальнейшего снижения ставок к 2027 году в 63%.

Смягчающие факторы: Даже при доходности в 2,5%, средний объем USDC в 284 миллиарда долларов генерирует 7,1 миллиарда долларов дохода от резервов, что все еще в 2,7 раза больше, чем 2,64 миллиарда долларов, заработанных при доходности 4,19% в 2025 году. Рост предложения перевешивает все, кроме самых экстремальных сценариев ставок.

Концентрация на одном продукте и зависимость от Coinbase

Доход от резервов USDC составляет более 96% дохода в 2025 году. Coinbase контролирует около 67% доли американской криптобиржи, получая 51% дохода от резервов. Как упоминалось ранее, если Coinbase запустит собственный стейблкоин, агрессивно пересмотрит условия или если регуляторное сопротивление замедлит рост предложения USDC, вся база дохода подвергнется риску.

Смягчающий фактор 1: Учитывая, что Coinbase зарабатывает 1,35 миллиарда долларов в год по соглашению с Circle при практически нулевом риске баланса, маловероятно, что они выберут запуск конкурирующего стейблкоина. Если они это сделают, это потребует от Coinbase построить регуляторную инфраструктуру и ликвидность, на создание которой Circle потратила годы.

Смягчающий фактор 2: Рынок годами высказывал аналогичную критику в адрес Visa (называя ее бизнесом одного продукта), но дополнительные услуги Visa в 2025 году принесли более 10,9 миллиарда долларов (рост на 24% г/г), показав ее reduced зависимость от interchange fees. Мы считаем CPN ключевым рычагом диверсификации для Circle. К концу 2030 года мы прогнозируем, что CPN будет генерировать 350 миллионов долларов дохода на основе транзакций (около 4% от общего дохода), который既 нечувствителен к процентным ставкам, так и независим от отношений с Coinbase. Со временем, происхождение USDC от институциональных и B2B-клиентов, обходящее Coinbase, также должно органически снизить смешанные дистрибьюторские затраты.

Устойчивость Tether и конкурентный ландшафт

Текущее предложение USDT приближается к 2,5-кратному объему USDC, и Tether активно сокращает regulatory gap, используемый USDC. В январе 2026 года Tether запустил USAT, стейблкоин, соответствующий закону GENIUS, выпущенный через Anchorage Digital Bank (регулируемый OCC), что открывает Tether доступ к ранее заблокированному американскому институциональному рынку. Если Tether успешно проведет двойную стратегию (USDT для глобальной ликвидности, USAT для американского compliance), regulatory moat USDC значительно сузится.

Смягчающие факторы: Конкурентный ландшафт тонкий. USDT доминирует в торговле на централизованных биржах за пределами США и в трансграничных переводах на развивающихся рынках, в то время как USDC доминирует в качестве залога в DeFi (выбор по умолчанию для Aave, Compound, Uniswap), институциональном внедрении в США, межсетевом мосте (CCTP составляет 47-50% объема транзакций моста) и B2B-платежах (235 миллиардов долларов в 2025 году, рост на 733% г/г, USDC занимает около 65%). Это, по сути, разные продукты, обслуживающие разные TAM. Тем не менее, наш тезис построен на расширении общего рынка стейблкоинов, а не на росте доли рынка за счет Tether. Оба стейблкоина значительно вырастут.

Раскрытие информации: Данный материал предназначен только для информационных целей и не constitutes инвестиционную консультацию, финансовую консультацию, торговую консультацию или任何 другую форму совета. Высказанные мнения являются мнениями автора и не должны рассматриваться как рекомендация покупать, продавать или удерживать任何 активы. Автор или связанные实体 могут иметь позиции в обсуждаемых активах. Вы должны провести собственное исследование и проконсультироваться с соответствующими финансовыми профессионалами перед принятием任何 инвестиционных решений.