Настоящее информационное преимущество имеет только одно применение: делать ставки до того, как другие дадут свою оценку.

Последние два года все испытывали тревогу, пытаясь найти ответ на один и тот же вопрос: какой следующий сектор ИИ вырастет?

Хранение данных, оптические модули, акции компаний, занимающихся вычислениями, акции энергетических компаний — нарратив менялся каждые несколько месяцев. Каждый раз кто-то опаздывал, и каждый раз кто-то говорил: «В следующий раз точно успею».

Мало кто задавался другим вопросом: во что делают ставки те, кто больше всех разбирается в ИИ?

Совокупное состояние тех, кто ушёл из OpenAI, уже приближается к 1 триллиону долларов. А их предпринимательская и инвестиционная деятельность знаменует начало следующей эпохи ИИ.

Дарио Амодеи основал Anthropic с потенциальной оценкой в 900 миллиардов. SSI Ильи Суцкевера не имеет продукта, но оценена в 32 миллиарда. Аравинд Шринивас создал Perplexity с оценкой в 21,2 миллиарда. Лаборатория Thinking Machines Lab Миры Мурати оценена в 12 миллиардов.

Так что, возможно, за последние годы OpenAI важнее всего выпустил не GPT-4, а этих уволившихся сотрудников, которых он передал обществу.

И среди них имя Леопольда Ашенбреннера, самого молодого уволенного из OpenAI, стало одним из самых часто упоминаемых в мире капитала за последние два года.

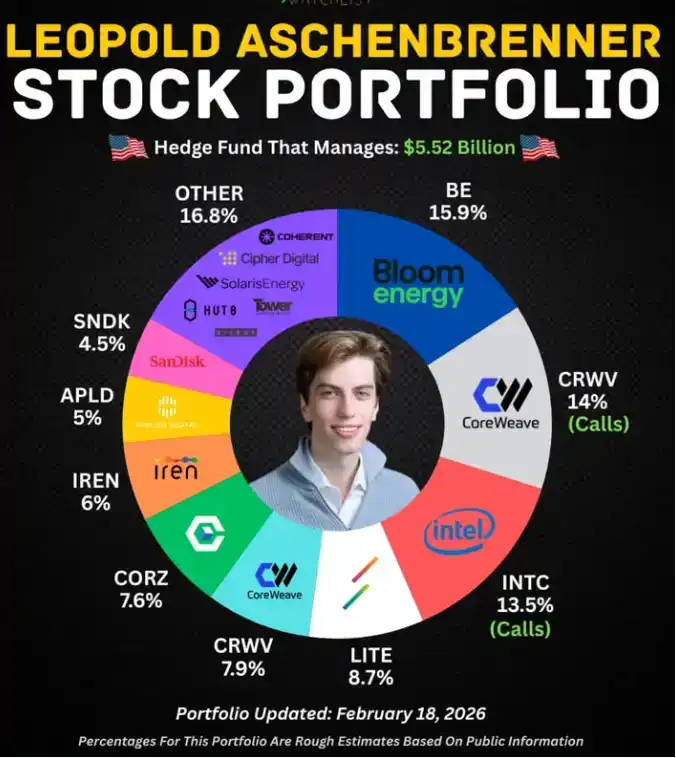

Легендарная история уже сто раз пережёвана медиа: уволенный из OpenAI в 23 года, он написал 165-страничный доклад «Situational Awareness» и за год увеличил объём хедж-фонда с 225 миллионов до 5,5 миллиардов долларов, сделав крупные ставки на ядерную энергетику и топливные элементы, и попал в точку.

История слишком цельная, контраст слишком сильный, результат слишком успешный. Сейчас, когда речь заходит о логике инвестирования в эпоху ИИ, он — практически обязательная фигура.

Но Леопольд — лишь тот, кого увидели первым в этой группе.

Ушедшие из OpenAI пошли двумя путями.

Первый — путь Ильи, Миры, Аравинда: основать компанию, привлечь огромное финансирование, рваться к созданию следующего прорывного продукта. Полная аналогия с тем, как гении уходили из Кремниевой долины.

Второй путь гораздо тише: некоторые выбрали ставки, оставляя исполнение другим, а сами сосредоточились на принятии решений.

Леопольд пошёл по второму пути в его крайней форме.

Он вышел на публичный рынок и с точки зрения оператора в индустрии ИИ нашёл в традиционном энергетическом секторе активы с неверной оценкой, а затем сделал на них крупные ставки. Он не разбирался в энергетике, но знал, сколько электричества «съест» ИИ, и этого было достаточно. Такую осведомлённость нельзя скопировать, читая отчёты или посещая отраслевые конференции; она накапливается только на определённой позиции.

Помимо этого пути, есть другая группа людей, делающая то же самое по логике, но в другой форме: небольшие фонды, завершающие за несколько часов due diligence, на которое у других уходят месяцы; их список отказов ценнее списка инвестиций. Они составляют самый незаметный и в то же время самый интересный для изучения слой в этом массовом исходе.

Большинство людей, уходя из компании, уносят с собой резюме. Люди, уходящие из OpenAI, уносят с собой ответы, в которых другие ещё не знают, что нуждаются.

I. Второго Леопольда не будет

Леопольд сделал крупные ставки на ядерную энергетическую компанию Vistra и компанию топливных элементов Bloom Energy.

После того как обе ставки сработали, к концу 2025 года он начал перераспределять активы, продал Vistra и сосредоточил средства на Bloom Energy и инфраструктуре дата-центров.

Традиционные энергетические аналитики, глядя на эти две акции, изучали планы расширения сетей, сравнивали политику углеродных налогов, строили модели роста спроса. Путь Леопольда был совершенно другим.

В OpenAI он видел масштабы серверных комнат, счета за электричество для обучения флагманской модели, слышал, как инженеры обсуждают, почему следующие поколения дата-центров должны располагаться рядом с АЭС. Эти детали не найти ни в каких финансовых отчётах или аналитических исследованиях, но из них складывается вывод о потребностях в энергии, более реальный, чем любая модель.

Такой подход в инвестиционном мире называется «межотраслевой арбитраж знаний»: перевод внутренней информации одной отрасли в недооценённые активы другой отрасли.

Раньше это была привилегия топовых макрохедж-фондов, основанная на глобальном видении мировой экономики.

Леопольд сделал нечто более точное: с позиции оператора в индустрии ИИ он нашёл в традиционном энергетическом публичном рынке уязвимости, связанные с запаздывающей оценкой.

Повторить этот путь очень сложно.

II. Zero Shot: самое ценное — это список отказов

Основатель фонда Zero Shot, Эван Морикава, тоже из OpenAI, с не менее сильным техническим бэкграундом. Он пошёл в венчурный капитал.

Одни и те же выпускники — совершенно разные пути.

Способность Леопольда к оценке проистекает из его конкретного опыта работы на ключевых позициях в ИИ, из прямого понимания затрат на обучение моделей, планирования дата-центров, потребностей в энергии — это накапливается только на этих позициях, перемотать нельзя. Среди ключевых сотрудников OpenAI очень мало тех, кто по-настоящему имеет право решать такую задачу.

В апреле этого года тихо появился новый фонд объёмом 100 миллионов долларов под названием Zero Shot.

Это термин из обучения ИИ, означающий, что модель даёт ответ, не видя никаких примеров.

Три сооснователя — из OpenAI: бывший руководитель инжиниринга приложений DALL-E и ChatGPT Эван Морикава, один из первых инженеров по промптам в OpenAI Эндрю Мейн, а также бывший исследователь и инженер Шон Джайн.

Они уже вложились в три компании: Worktrace (ИИ-оптимизация рабочих процессов на предприятиях), Foundry Robotics (роботы для заводов, усиленные ИИ) и ещё один проект, пока остающийся в тени.

100 миллионов — по нынешним временам, когда ИИ-фонды легко собирают десятки миллиардов, это небольшая сумма.

Но если посмотреть, в какие сектора они отказываются инвестировать, картина становится яснее.

Мейн публично заявлял, что он настроен скептически в отношении большинства инструментов «атмосферного программирования» — продуктов, которые помогают писать код на естественном языке.

Причина довольно прямая: он знает, какие наработки есть внутри OpenAI в области программирования, и знает, насколько быстро конкурентное преимущество таких инструментов будет разрушено базовыми моделями. Морикава же держится на расстоянии от множества компаний в робототехнике, занимающихся «видеоданными, ориентированными на человека» — тех, что собирают данные о движениях людей для обучения роботов. По его мнению, этот технологический путь ведёт в тупик.

Эти два вывода не под силу обычному венчурному инвестору.

Они не были у первоисточника информации, не видели тех внутренних обсуждений, поэтому не могут определить, какой путь ведёт в никуда.

Преимущество Zero Shot скрыто в их списке отказов. На рынке, где все кричат о стартапах в ИИ, знать, где ловушки, ценнее, чем знать, на кого ставить. Для тех, кто уже копал шахту, отчёт о минных полях полезнее карты сокровищ.

Они сознательно ограничили размер фонда 100 миллионами, и на то есть конкретная причина.

Они чётко понимают, на каком этапе их преимущество наиболее ценно: на ранней стадии, когда технологический путь ещё не определился. На этом этапе осведомлённые люди могут с первого взгляда определить, какой путь пройдёт.

Когда проект доходит до раундов C и D, финансовые данные и публичная информация перекрывают информационное преимущество, и эта карта становится бесполезной.

Чем крупнее фонд, тем больше он вынужден гоняться за «определёнными большими направлениями», тем больше он использует чужие методы игры.

100 миллионов — это их честная оценка границ своих преимуществ.

III. Бизнес-ангельство — это другой бизнес

И Мира Мурати, и фонд Zero Shot инвестировали в Worktrace бывшей коллеги по OpenAI Анджелы Цзян — компанию, оптимизирующую рабочие процессы на предприятиях с помощью ИИ.

Но инвестиционная логика прочнее, чем просто «хорошие отношения».

Мира видела, как Анджела принимала решения в условиях высокого давления в OpenAI, видела её оценку границ ИИ-продуктов, видела её исполнительность при реальных ограничениях. Эти вещи невозможно подделать за двухчасовую питч-презентацию основателя, их не восстановить даже самым тщательным due diligence.

Анджеле не нужно было убеждать Миру верить в неё, потому что у Миры уже сформировалось суждение. Информационные затраты для бизнес-ангела близки к нулю, но качество информации намного выше среднерыночного.

Больший маховик раскручивает Сэм Олтман.

По сообщениям, Олтман решает, инвестировать ли ему вслед за бывшим сотрудником, в течение нескольких часов после того, как узнаёт о его стартапе, добавляя к этому средства OpenAI Startup Fund и огромные ресурсы API.

Он лично не владеет акциями OpenAI, но успех каждого выпускника расширяет точки входа данных OpenAI, каналы распространения и политическое влияние. Он использует капитал для поддержания экосистемы, которая ему не принадлежит, но продолжает приносить ему отдачу. Это невидимая доля собственности, но она реально приносит сложные проценты.

Эта экосистема заставляет многих ошибочно полагать, что это просто взаимопомощь бывших коллег.

Если сравнить её с «Мафией PayPal», разница будет очевидна.

Сплочённость «Мафии PayPal» была основана на общих трудностях: вместе пережили платежные войны, поглощение eBay, в те времена, когда компания была на грани смерти, сложились товарищеские отношения окопной жизни. Это доверие было реальным, но их взгляды на будущее были разными. Тиль занялся венчурным капиталом, Маск — ракетами, Хоффман — социальными сетями, пути разошлись.

А выпускников OpenAI объединяет общая ставка на будущее: ОИИ (AGI) придёт, временное окно ограничено, сейчас — уникальный момент для расстановки фигур. Движущая сила веры устойчивее дружеских чувств, потому что она напрямую связана с выгодой: если направление ставок каждого окажется верным, выиграет вся сеть.

Это также делает порог входа в этот круг довольно тонким.

Если продукт достаточно хорош, привлечь деньги этих людей не проблема. Но если вы сомневаетесь в будущем ИИ или логика вашего стартапа строится на предпосылке «ОИИ ещё далеко», то даже при отличном продукте получить от них чек будет крайне сложно.

Разногласия в мировоззрении заканчивают разговор ещё до рукопожатия.

IV. От Создателей к Инвесторам

Направления, выбранные выпускниками OpenAI, можно разделить на три категории.

Илья, Аравинд, Мира выбрали путь предпринимательства.

Но при том, что все они основали компании, они занимаются совершенно разными вещами. Аравинд ведёт конкурентный потребительский бизнес, Мира создаёт инструментальную платформу, у SSI Ильи нет даже продукта, но она получила оценку в 32 миллиарда, делая ставку на само слово «безопасность».

Леопольд и Zero Shot выбрали инвестиции.

Леопольд пошёл на публичный рынок, Zero Shot занялся ранним венчурным капиталом — оба пути заключаются в превращении суждений в капитал, а не в личном исполнении. Среди выпускников OpenAI это меньшинство, но это меньшинство стоит рассмотреть отдельно: когда человек готов делать ставки, но не делать сам, это обычно означает, что его понимание результата уже настолько ясно, что не требует проверки действиями.

Принято считать, что высшей формой выражения гения является творение. Но эта группа даёт другой ответ: когда суждение достаточно ясно, распределить это понимание, поставив на несколько направлений, и позволить исполнительным людям строить — это более эффективный выбор.

Доклад Леопольда называется «Situational Awareness» («Осведомлённость о ситуации») — военный термин, означающий способность пилота в реальном времени воспринимать общую картину на поле боя.

Осведомлённость пилота о ситуации определяет его действия через две секунды, потеря её означает смерть. То, что эти люди вынесли из OpenAI, — это и есть осведомлённость о ситуации на поле боя ИИ. Они знают, куда движется битва, знают, где высоты, знают, какой окоп ведёт в тупик.

То, что они делают сейчас, — это расстановка сил на основе этого.

Когда умнейшие люди эпохи начинают ставить всё на кон, это значит, что, по их мнению, ответ уже достаточно ясен — настолько ясен, что не требует проверки собственными руками.