Автор: Silvio (@SilvioBusonero)

Оригинальное название: The monetary premium on L1s is fading

Компиляция и редактирование: BitpushNews

Оценка блокчейнов L1 — это совокупность множества факторов: включая культурный нарратив (меметику), сетевые комиссии, безопасность и развитие приложений верхнего уровня. Среди них наиболее недооцененным является так называемый «денежный премиум» (Monetary Premium).

Денежный премиум проистекает из потребности участников рынка использовать актив в качестве средства сбережения (Store of Value, SoV) или средства обмена (Medium of Exchange, MoE).

-

Средство сбережения напрямую связано с надежностью (soundness) и степенью децентрализации актива, поэтому это не самая простая рыночная стратегия для входа.

-

В相比之下, роль средства обмена может быть достигнута проще. Токен может служить основным способом обмена и измерения стоимости в экономике блокчейна.

Это аналогично роли токенов в экономике Web2:

-

Внутриигровая валюта Robux в Roblox обладает сильной обменной стоимостью.

-

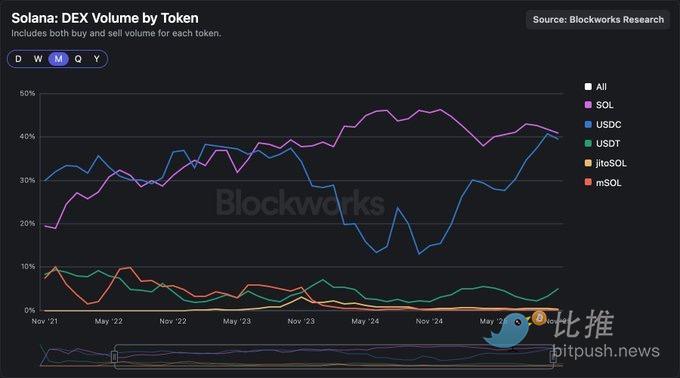

Когда мем-токены начали расти, люди покупали SOL для торговли ими. Поскольку SOL была валютой по умолчанию на платформе Pump, большинство трейдеров не конвертировали активы обратно в доллары, а оставляли часть SOL наготове для «апа» (ape). Подобная ситуация была с ETH во время бума NFT в 2021 году. Множество пользователей начали использовать нативный актив для торговли, эффективно создав полезность средства обмена (MoE).

Сохраняется ли премиум?

Ответ: Нет, этот премиум быстро исчезает. Пользователи все чаще предпочитают использовать стейблкоины для транзакций.

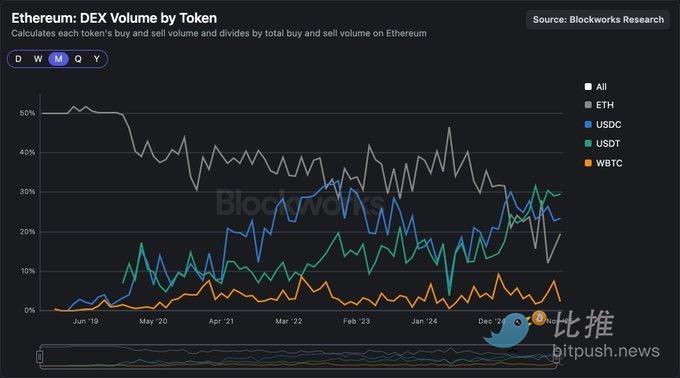

Ethereum — Стейблкоины стали средством обмена

-

Если судить по объему ончейн-транзакций основных токенов, нативный токен ETH больше не является основным средством обмена, как раньше.

-

Доминирование ETH в качестве MoE снижается, в то время как популярность USDC и USDT в графиках объема транзакций и в топе пулов ликвидности Uniswap растет.

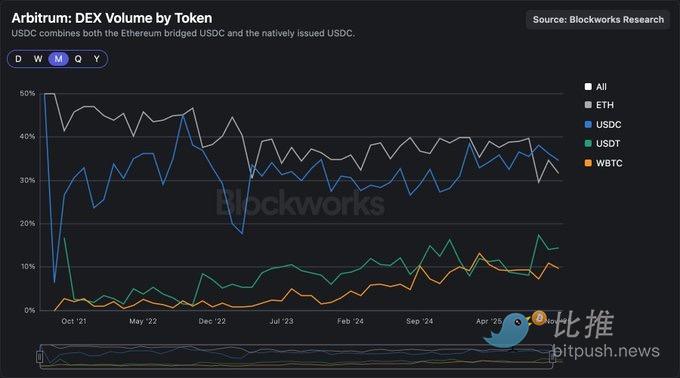

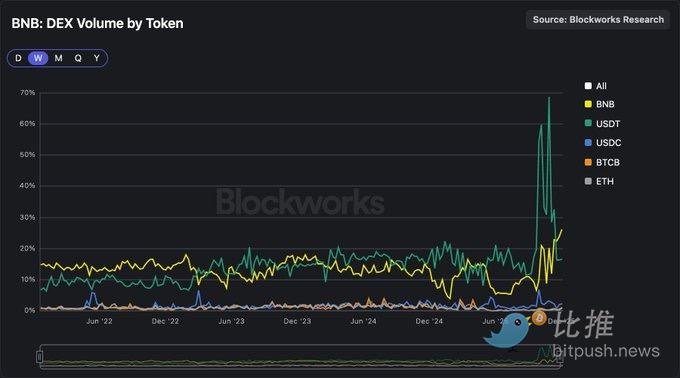

Для L2, таких как Arbitrum, ситуация аналогична.