Автор: David, TideResearch

TideResearch Краткое введение:

Управление по управлению благосостоянием J.P. Morgan 1 июня опубликовало промежуточный прогнозный отчет на 2026 год, в котором даются рекомендации своим клиентам с высоким уровнем дохода о том, как инвестировать во второй половине года.

На фоне роста цен на нефть из-за блокады Ормузского пролива, возобновления инфляции и перехода нарратива об ИИ от эйфории к скептицизму, общий тон этого отчета в целом осторожно-оптимистичный, но с необходимостью изменения конкретных инвестиционных конфигураций.

J.P. Morgan считает, что три основных глобальных риска (фрагментация, инфляция, разрушительный потенциал ИИ) в настоящее время оценены рынком излишне пессимистично, и текущая волатильность как раз и является окном возможностей для входа.

Общий вывод:

Продолжайте делать ставку на суперцикл ИИ и американский фондовый рынок, хеджируйте инфляцию с помощью реальных активов и альтернативных стратегий, сокращайте денежные средства, следите за развивающимися рынками.

Если вы держите позиции в американских технологических акциях или размышляете о наращивании или сокращении позиций во второй половине года, структура и данные этого отчета заслуживают внимания; мы сделали его сжатое изложение и интерпретацию, переставив приоритеты в соответствии с инвестиционной значимостью.

Шесть ключевых выводов:

1 Суперцикл ИИ не закончился, рынок излишне пессимистичен.

Прогнозируемые капитальные затраты пяти «гиперскейлеров» (Microsoft, Meta, Oracle, Google, Amazon) на 2026 год превышают 650 млрд долларов, что на 130 млрд долларов больше, чем было повышено в предыдущем отчетном сезоне. Инвестиции, связанные с ИИ, внесли вклад в рост реального ВВП США в 2025 году на 25 базисных пунктов. Темпы роста ВВП Тайваня превысили 7%, что является самым быстрым показателем с 2010 года, основной движущей силой стал экспорт полупроводников. JPM считает, что рынок закладывает в цены сценарий «пика ИИ», но данные не подтверждают этот нарратив.

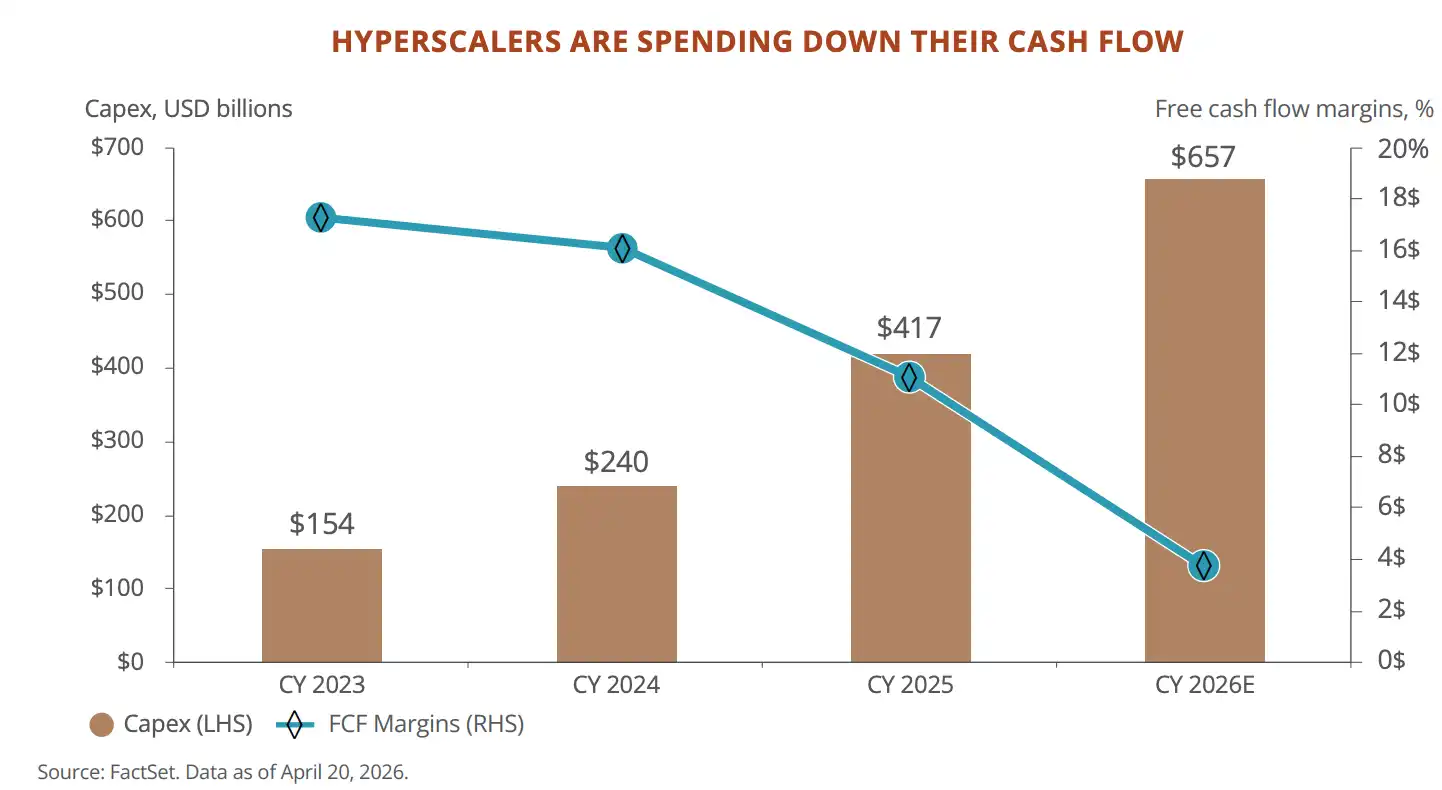

2 Однако финансовые характеристики «гиперскейлеров» меняются.

Свободный денежный поток сократился с 240 млрд долларов в 2024 году до прогнозируемых 73 млрд долларов к концу 2026 года. Forward P/E (форвардное отношение цены к прибыли) Microsoft упал с пика в эпоху ИИ в 35 раз до 22,5 раз. Эти компании трансформируются из моделей «с легкими активами и высокой доходностью» в «с тяжелыми активами и высокими инвестициями», рынок все еще переваривает эту трансформацию.

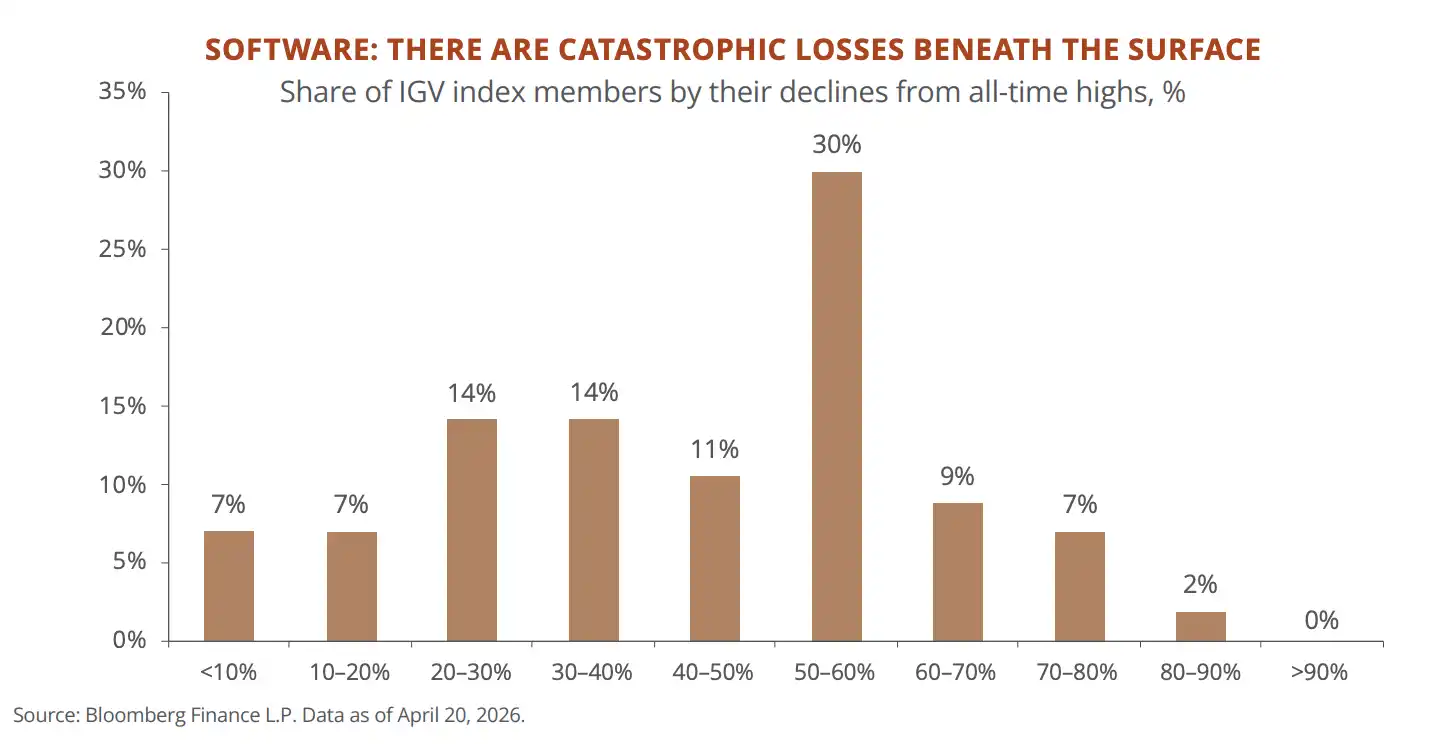

3 В секторе SaaS происходит скрытая бойня.

Около половины компонентов индекса программного обеспечения S&P (IGV) упали более чем на 50% от исторических максимумов. Корзина «уязвимых к ИИ объектов», отслеживаемая JPM, упала почти на 20% в этом году. На рынке частного кредитования 21% экспозиции приходится на компании-разработчики ПО, а вместе с технологиями и бизнес-услугами эта цифра возрастает до 40%. Влияние ИИ на бизнес-модели подписочного программного обеспечения уже происходит.

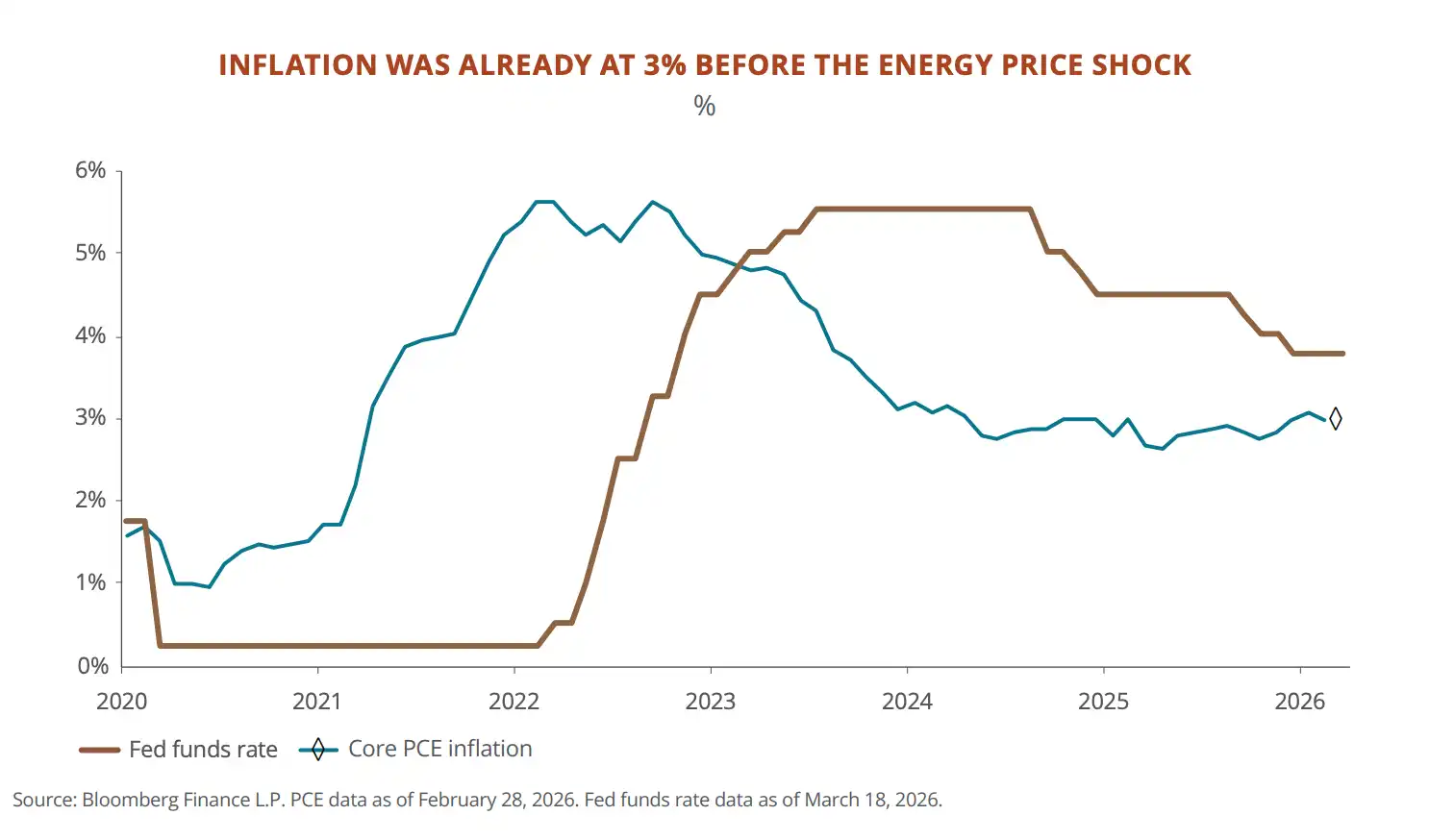

4 Дно инфляции стало выше, чем до пандемии, денежные средства медленно обесцениваются.

Базовый индекс PCE в США до энергетического шока уже застрял на уровне 3%. С начала 2020-х годов потребительские цены в совокупности выросли на 25%, а основные облигации заработали лишь 6%. У клиентов JPM почти 20% активов находятся в денежных средствах и краткосрочных облигациях. Смысл отчета ясен: вы думаете, что избегаете риска, но на самом деле теряете деньги.

5 Блокада Ормузского пролива является крупнейшим с времен Второй мировой войны шоком для поставок нефти, но JPM считает, что следует покупать на падении.

Цены на нефть почти удвоились, американский фондовый рынок испытал коррекцию примерно на 10%, P/E индекса S&P 500 в какой-то момент упал ниже 20. Исторические данные JPM показывают, что после прорыва индекса VIX выше 30 вероятность положительной доходности в течение 6 месяцев составляет от 70% до 83%, со средней доходностью 12,4%.

6 Развивающиеся рынки могут стать возможностью во второй половине года.

Ожидается рост прибыли компаний развивающихся рынков на 46%, при P/E всего 11,8. Тайвань и Южная Корея являются ключевыми узлами цепочки поставок аппаратного обеспечения для ИИ. Латинская Америка обладает более 40% мировых запасов меди и почти 60% лития. Дисконт китайских акций к другим азиатским рынкам достиг максимума за 20 лет, отношение JP «становится осторожно более теплым».

Об ИИ: рынок закладывает «пик», JP Morgan считает, что еще рано

JPM начинает с заявления, что Уолл-стрит уже «слишком пессимистична» в отношении нарратива о суперцикле ИИ.

Ключевые данные, подтверждающие этот вывод:

- Пять гигантов облачных вычислений — Microsoft, Meta, Oracle, Google, Amazon — их совокупные ожидаемые капитальные затраты на 2026 год превышают 650 млрд долларов. Арендные ставки на GPU (ключевые чипы для обучения моделей ИИ) в облаке с прошлого октября выросли на 40%, предложение по-прежнему не поспевает за спросом. Акции Nvidia торгуются с дисконтом в 40% к среднему P/E за последние десять лет, рынок оценивает сценарий «пика продаж чипов», но доходы от облачного бизнеса продолжают ускоряться.

В то же время финансовые характеристики этих пяти компаний меняются. Свободный денежный поток сокращается с 240 млрд долларов в 2024 году до прогнозируемых 73 млрд долларов к концу 2026 года, P/E Microsoft упал с пика в эпоху ИИ в 35 раз до 22,5 раз. Модель с легкими активами, привлекавшая инвесторов в последнее десятилетие, переписывается в сторону тяжелых капитальных вложений. JPM считает, что на данном этапе следует смотреть на темпы роста выручки, а не на денежный поток, но это также означает, что как только спрос замедлится, эти вложения могут превратиться в обузу.

Несколько других суждений об ИИ, которые можно считать указаниями на локальные риски в рамках общей тенденции:

Традиционные компании-разработчики ПО стали первыми реальными жертвами ИИ. Около половины компонентов индекса сектора ПО на американском фондовом рынке упали более чем на 50% от максимумов, медианная операционная рентабельность составляет всего 4%. Логика воздействия проста: SaaS (подписочное ПО) взимает плату с человека, ИИ сокращает количество людей. Это уже передалось на рынок кредитования: около 21% средств на рынке прямого кредитования США выдано компаниям-разработчикам ПО, цены на публично торгуемые фонды кредитов технологического сектора упали почти до минимумов прошлого цикла. Стресс-тесты JPM показывают, что в экстремальном сценарии убытки с учетом плеча могут достичь 4%, но пока не представляют системного риска.

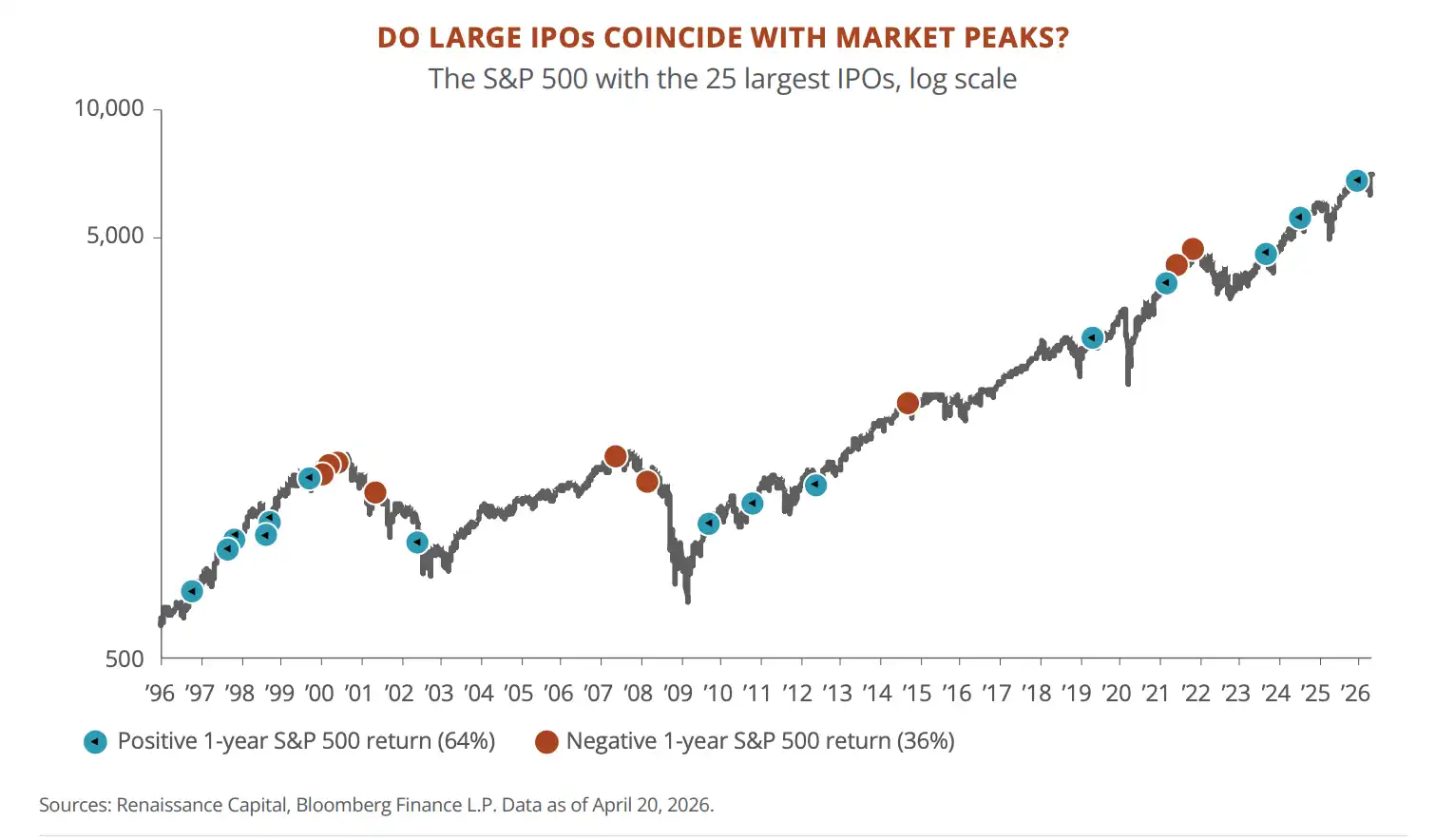

SpaceX, Anthropic, OpenAI могут провести IPO в этом году скопом, что исторически не является хорошим предзнаменованием. После 25 крупнейших IPO за последние годы медианная доходность новых акций в первый год на 30 процентных пунктов отставала от рынка, 12 из 18 акций падали в первый год. В годы с мега-IPO медианная годовая доходность рынка составляла всего 3%, что значительно ниже долгосрочного среднего показателя в 10%. JPM не утверждает, что пик обязательно наступит, но явно рассматривает реакцию рынка на IPO SpaceX как термометр цикла.

Об инфляции: инфляция не вернется к 2%, ваши денежные средства и облигации теряют в стоимости

Ключевой момент этой части не в том, что Ормузский пролив поднял цены на нефть, а в том, что инфляция в США не вернулась к нормальному уровню еще до роста цен на нефть.

В январе 2026 года базовый индекс PCE составил 3,1% в годовом исчислении, особенно устойчиво росли цены на такие категории локальных услуг, как общественное питание, личный уход. Затем цены на нефть удвоились. Модели ФРС показывают, что рост цен на нефть на 10 долларов за баррель повышает инфляцию примерно на 0,3 процентных пункта, на этот раз рост составил 40 долларов.

JPM считает, что вероятность полного повторения 1970-х годов невелика. На рынке труда не наблюдается спирали «зарплаты-цены», уровень добровольных увольнений снижается, инфляция в жилищном секторе снизилась с 5% в конце 2024 года до чуть более 3%, избыточные мощности в Китае также сдерживают глобальные цены на товары. Но дно инфляции стало заметно выше, чем до пандемии, и, вероятно, будет колебаться около 3%.

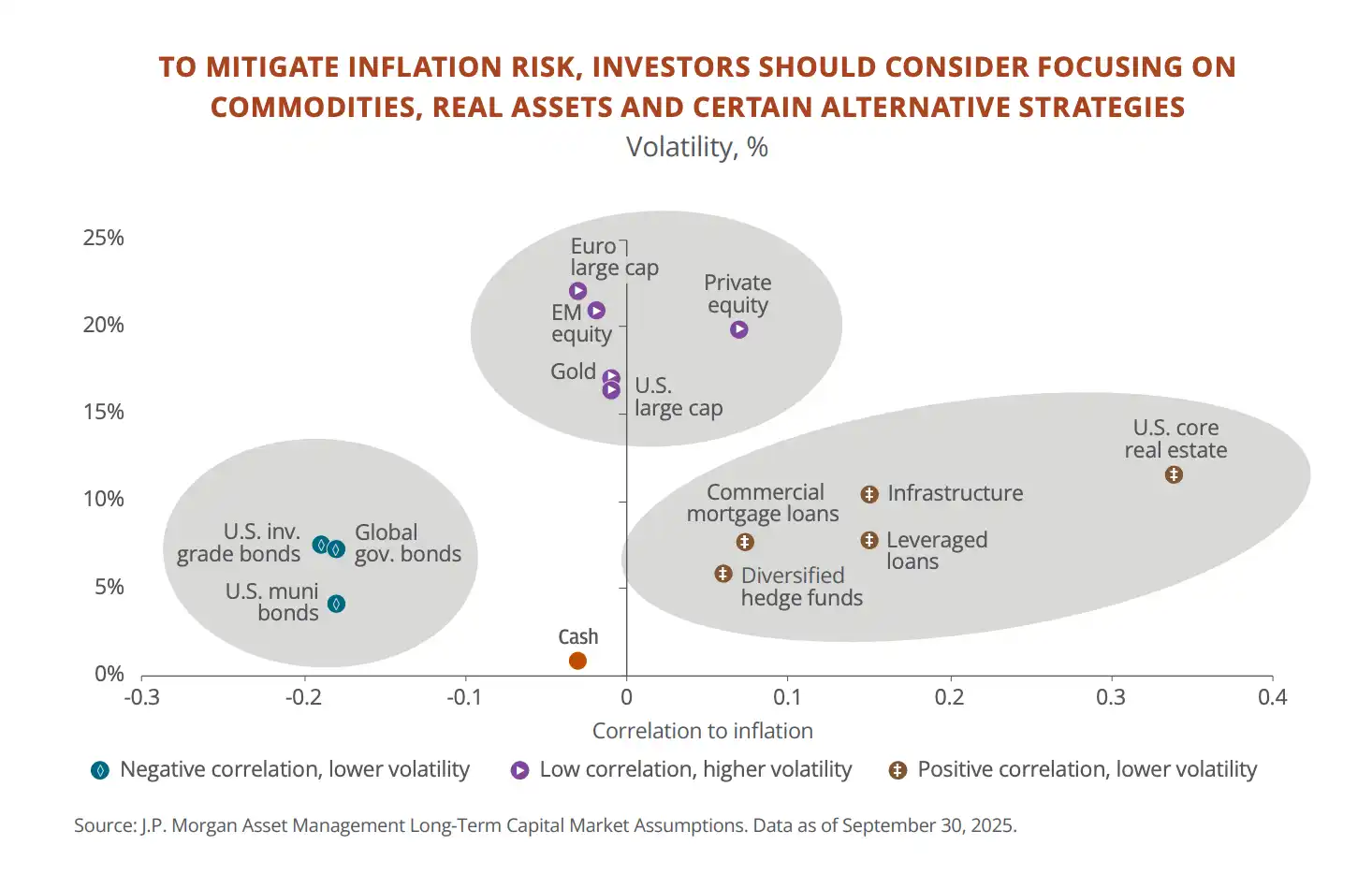

Рекомендация JPM по ответным мерам — увеличить инвестиции в реальные активы.

С начала 2020-х годов цены в США в совокупности выросли на 25%, облигации принесли доход лишь в 6%, денежные средства еще меньше. Вы думаете, что деньги лежат без движения, но на самом деле они ежегодно обесцениваются. У собственных клиентов JPM почти 20% активов все еще находятся в денежных средствах и краткосрочных облигациях.

Поэтому их рекомендация — переместить часть денег в активы, привязанные к инфляции:

- Товарно-сырьевые товары, инфраструктура, недвижимость — вещи, которые будут расти вместе с ценами; рекомендуется совокупно довести их долю в портфеле примерно до 5%.

- Золото отдельно рекомендуется в размере от 3% до 6%.

- Кроме того, хедж-фонды: в 2022 году, когда падали и акции, и облигации, макростратегические хедж-фонды заработали 9%. Но JPM также признает, что 94% их клиентов частных банков вообще никогда не покупали хедж-фонды, 86% не покупали инфраструктурные продукты.

Резюме этой части в одном предложении:

Инфляция может и не выйдет из-под контроля, но и не вернется к 2%. Если ваш портфель по-прежнему представляет собой традиционное соотношение 60/40 акций и облигаций плюс куча денежных средств, JPM считает, что вы готовитесь к миру, которого больше не существует.

О геополитике: фондовый рынок Китая может ожидать структурная переоценка

Эта часть охватывает самый разнообразный контент: от конфликтов на Ближнем Востоке до соперничества между США и Китаем и проблем Европы. Мы коснемся только того, что напрямую связано с инвестиционными решениями.

1. Блокада Ормузского пролива стала крупнейшим рыночным шоком первой половины года. Ежедневно через этот проход проходит около 20 млн баррелей нефти, что составляет пятую часть мирового потребления нефти. После совместных ударов США и Израиля по Ирану цены на нефть за несколько дней почти удвоились, цены на газ в Европе выросли почти на 100% за два дня. Генеральный директор Qatar Energy заявил, что 15% мощностей по производству СПГ могут быть выведены из строя на срок до пяти лет. Катар также поставляет около 30% мирового гелия, необходимого для производства чипов, Южная Корея уже предупредила о возможных простоях на фабриках по производству чипов.

JPM считает, что конфликт движется к деэскалации, но повреждения физической инфраструктуры и премия за риск в энергетике быстро не исчезнут.

Поэтому их рекомендация инвесторам: наращивать позиции на американском фондовом рынке на коррекциях.

В первой половине года американский фондовый рынок упал примерно на 10%, P/E индекса S&P 500 в какой-то момент упал ниже 20. Исторически после прорыва индекса VIX (индекса волатильности) выше 30 вероятность положительной доходности в течение 6 месяцев составляет от 70% до 83%, со средней доходностью 12,4%.

2. США и Китай строят свои экосистемы, рынки могут ускорить разделение на два лагеря. США ограничивают экспорт чипов в Китай, привлекая Нидерланды и Японию к ограничениям на поставки полупроводникового оборудования. Китай расширяет экспорт на рынки, не входящие в США, объем инвестиций в рамках инициативы «Один пояс, один путь» в 2025 году достиг рекордного уровня, в Бразилию за год инвестировано 53 млрд долларов, общий объем торговли с Латинской Америкой уже превысил показатели США. Вывод JPM: будущая доходность инвестиций может все больше зависеть от того, к какому лагерю принадлежат ваши активы, а не только от роста самой компании.

Но фрагментация также создает возможности, особенно на развивающихся рынках.

JPM перечисляет несколько направлений:

- Латинская Америка обладает более 40% мировых запасов меди и почти 60% лития, а также богата никелем, редкоземельными элементами и сельскохозяйственными ресурсами. Прямые иностранные инвестиции за последние двадцать лет удвоились, центральные банки контролируют инфляцию лучше, чем в развитых странах, в политике наблюдается переход к более прагматичным прорыночным правительствам.

- Страны Персидского залива на Ближнем Востоке используют доходы от нефти для строительства центров обработки данных для ИИ, Саудовская Аравия сотрудничает с Blackstone в проекте центра обработки данных на 3 млрд долларов, стоимость которого на 30% ниже, чем в США.

- Восточная Азия (Тайвань, Южная Корея) контролирует ключевые узлы цепочки поставок аппаратного обеспечения для ИИ. Если капитальные затраты на ИИ продолжат ускоряться, экспорт и ценовая власть этих экономик продолжат усиливаться.

- Дисконт китайских акций к другим азиатским рынкам достиг максимума за 20 лет, 80% китайских потребителей испытывают энтузиазм в отношении продуктов ИИ (в США — 38%), стоимость электроэнергии примерно вдвое ниже, чем в США. Отношение JPM «становится осторожно более теплым», если в политике появятся более четкие прорыночные сигналы, фондовый рынок Китая может ожидать структурная переоценка.

Для сравнения, Европа — самый консервативный с точки зрения отношения JPM рынок. Стоимость электроэнергии в два-четыре раза выше, чем в США, расходы на НИОКР составляют лишь 2,2% ВВП (США — 3,6%, Южная Корея — 5,2%), объем венчурного капитала составляет одну десятую от американского.

Энергетический шок также вынуждает ЕЦБ, возможно, снова повышать процентные ставки. JPM в Европе рекомендует покупать только акции, связанные с обороной и инфраструктурой, избегая автомобильного и потребительского секторов.

На что ставит JPM, на что не ставит

Сжать 60-страничный отчет до одного предложения: Волатильность — это возможность для входа, но способ входа нужно менять.

На что следует делать ставку:

- Цепочка создания стоимости инфраструктуры ИИ (чипы, оптические модули, электроэнергия), акции и облигации развивающихся рынков, реальные активы (товарно-сырьевые товары, инфраструктура, золото), акции, связанные с обороной, концепции ИИ в Китае (осторожное наращивание позиций).

На что не следует делать ставку:

- Денежные средства, традиционные компании подписочного ПО, европейский автомобильный и потребительский секторы, а также чистая стратегия распределения активов 60/40 акций и облигаций для второй половины этого года.

Ссылка на оригинальный отчет:

https://www.jpmorgan.com/content/dam/jpmorgan/documents/wealth-management/mid-year-outlook-2026.pdf

Данная статья представляет собой обзор и интерпретацию промежуточного прогнозного отчета на 2026 год управления по управлению благосостоянием J.P. Morgan, подготовленные TideResearch. Приведенные в статье суждения и рекомендации являются точкой зрения JPM и не отражают позицию TideResearch, а также не представляют собой каких-либо инвестиционных рекомендаций.

Отчеты продавцов по своей природе склонны к оптимизму, JPM одновременно является поставщиком инвестиционно-банковских услуг для ряда упомянутых компаний. Ценность отчета заключается в его структуре и данных, а не в каком-то одном выводе. Смотрите на логику, а не только на направление.

Рынки связаны с рисками, решения должны быть независимыми.

Источники данных: J.P. Morgan Wealth Management Mid-Year Outlook 2026 · Bloomberg · FactSet · U.S. Bureau of Labor Statistics · IEA · METR · Renaissance Capital

TideResearch · 4 июня 2026 г.