Автор: Dhruvang Choudhari (AMINA Bank)

Компиляция: Deep Tide TechFlow

Введение Deep Tide: Январь 2026 года представил парадокс: криптовалютные цены упали на 25%, но инфраструктура, поддерживающая институциональное внедрение, ускорилась. В то время как биткоин упал до 10-месячного минимума в районе 73 000 долларов, BlackRock назвал цифровые активы определяющей инвестиционной темой 2026 года.

В то время как трейдеры с плечом ликвидировали позиции на 22 миллиарда долларов, Depository Trust and Clearing Company (DTCC) запустила промышленный уровень токенизации для казначейских облигаций и акций США. В то время как индекс настроений достиг крайнего пессимизма, Y Combinator объявил, что начнет финансировать стартапы в USDC.

Анализ AMINA Bank указывает, что это не отказ от цифровых активов, а их переоценка в условиях меняющейся глобальной денежной системы. Расхождение между ценовым поведением и структурным прогрессом определяет текущую фазу цикла.

Полный текст ниже:

Введение

Январь 2026 года представил парадокс: криптовалютные цены упали на 25%, но инфраструктура, поддерживающая институциональное внедрение, ускорилась.

В то время как биткоин упал до 10-месячного минимума в районе 73 000 долларов, BlackRock назвал цифровые активы определяющей инвестиционной темой 2026 года. В то время как трейдеры с плечом ликвидировали позиции на 22 миллиарда долларов, Depository Trust and Clearing Company (DTCC) запустила промышленный уровень токенизации для казначейских облигаций и акций США. В то время как индекс настроений достиг крайнего пессимизма, Y Combinator объявил, что начнет финансировать стартапы в USDC.

Первые два месяца 2026 года ознаменовали решительный сдвиг на рынке цифровых активов. То, что изначально казалось хаотичной распродажей, на самом деле было широкой макроэкономической переоценкой, движимой суверенным риском, изменениями в денежной системе и вынужденным закрытием глобального плеча. В отличие от предыдущих падений криптовалют, это событие не было вызвано самой экосистемой цифровых активов. Оно пришло извне.

Январь и февраль выявили парадокс, который сейчас является ядром институциональной эпохи криптовалют. Рыночные цены резко ухудшились, но нормативная ясность, развертывание инфраструктуры и институциональные обязательства продвигались с беспрецедентной скоростью. Это расхождение между ценовым поведением и структурным прогрессом определяет текущую стадию цикла.

Это обновление анализирует, как макроэкономический шок нарушил структуру крипторынка, почему биткоин как макроактив сталкивается с кризисом идентичности, и как институциональный капитал продолжает строить, а не отступать, несмотря на волатильность.

Институциональная экспансия на фоне слабости рынка

Несмотря на ухудшение спотовых цен, институциональное участие ускоряется, а не замедляется. Это ускорение раскрывает фундаментальный сдвиг в том, как зрелые инвесторы подходят к цифровым активам: зрелость инфраструктуры теперь важнее ценового импульса.

Токенизация как ключевая стратегия

BlackRock официально назвал цифровые активы и токенизацию определяющей инвестиционной темой 2026 года, наряду с искусственным интеллектом, как структурные драйверы рынков капитала.

В Franklin Templeton руководство по инновациям охарактеризовало 2026 год как начало нативной для кошельков финансовой системы, где акции, облигации и фонды хранятся непосредственно в цифровых кошельках, а не через традиционные кастодиальные框架 (фреймворки).

Y Combinator подал ключевой сигнал, объявив, что начиная с весенней когорты 2026 года стартапы могут получать финансирование в USDC в сетях Ethereum, Base и Solana. Расчеты в стейблкоинах теперь обычно清算ляются менее чем за секунду при стоимости ниже 0,01 доллара, предлагая явное преимущество по сравнению с трансграничными фиатными каналами.

Снижение регуляторного трения

Регуляторные разработки тихо устранили давние структурные препятствия. SEC отозвала предыдущие бухгалтерские указания, которые мешали банкам предоставлять услуги кастодиального хранения цифровых активов. В то же время Depository Trust and Clearing Company (DTCC) запустила программу промышленной токенизации для казначейских облигаций США, акций крупных компаний и ETF, подтвердив юридическое равенство токенизированных ценных бумаг и традиционных ценных бумаг.

Это знаменует переход от экспериментального внедрения к модернизации внутренней финансовой инфраструктуры.

Региональная конкуренция за криптовалютный капитал

Юрисдикции все чаще используют политику в качестве конкурентного рычага.

Гонконг объявил о нулевых налоговых льготах на квалифицированный доход от цифровых активов для фондов и семейных офисов, позиционируя себя как главный азиатский центр институционального криптовалютного бизнеса. По состоянию на январь 2026 года работают 11 лицензированных платформ для торговли виртуальными активами.

Между тем Дубай продолжает реализацию своей стратегии «blockchain-first» для правительства, целью которой является обработка 50% государственных транзакций на блокчейне к концу 2026 года. Проникновение криптовалют в ОАЭ достигло около 39%, что представляет более 3,7 миллиона пользователей.

Макроэкономический шок, нарушивший спокойствие

Чтобы понять, почему институты продолжают строить, нужно понять, что вызвало распродажи. Относительная стабильность 2025 года породила ожидания, что криптовалюты вступили в фазу низкой волатильности, закрепленную институтами. Эти предположения были разрушены в январе.

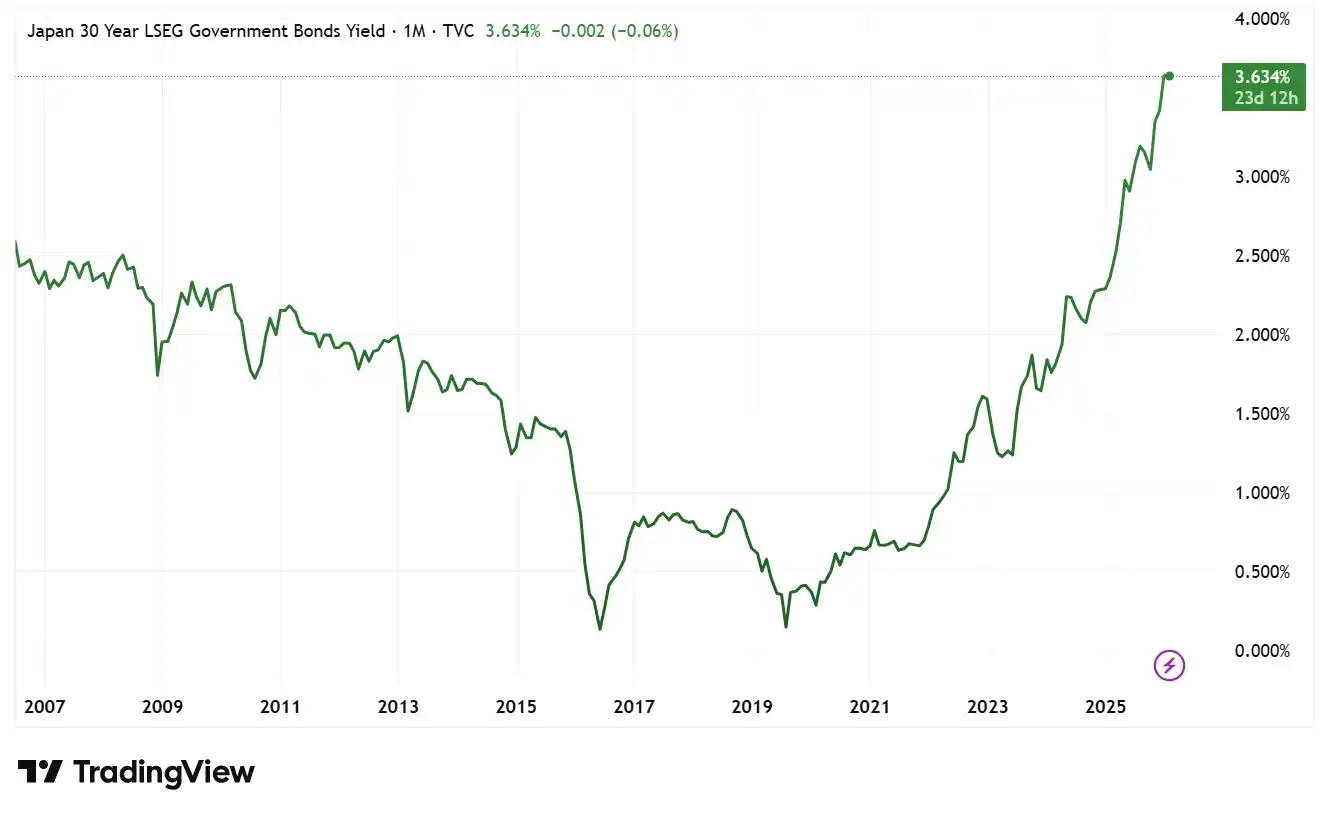

Япония и закрытие глобального плеча

20 января 2026 года рынок государственных облигаций Японии (JGB) вошел в острую стадию стресса. Доходность 30-летних JGB взлетела более чем на 30 базисных пунктов до 3,91%, самого высокого уровня за 27 лет, после того как фискальные заявления премьер-министра Такаити Санаэ обострили опасения по поводу долговой устойчивости. Коэффициент долга к ВВП Японии превысил 250%, что сделало его точкой напряжения на глобальном рынке облигаций.

Рис. 1: Доходность 30-летних государственных облигаций Японии (историческая)

Источник: TradingView

Непосредственным последствием стало быстрое закрытие иеновых сделок carry trade, крупнейшего источника дешевого глобального плеча. По мере роста стоимости финансирования в иенах инвесторы были вынуждены ликвидировать рисковые активы для выполнения маржинальных требований. Биткоин упал ниже 91 000 долларов не из-за специфической слабости крипторынка, а потому что выступил ликвидным прокси для восстановления балансов.

Номинация Уорша и денежная переоценка

Это напряжение усилилось 30 января с номинацией Кевина Уорша на пост следующего председателя ФРС. Долговременное предпочтение Уоршем более высоких реальных процентных ставок и значительного сокращения баланса ФРС было воспринято как явный сдвиг в сторону от мягкой денежно-кредитной политики.

За 24 часа общая рыночная капитализация криптовалют упала примерно на 430 миллиардов долларов. Биткоин упал примерно на 7% за одну торговую сессию, в то время как Ethereum и высокобета-альткойны испытали двузначные процентные откаты. Это движение отражало переоценку ожиданий глобальной долларовой ликвидности, а не спекулятивную панику.

Ценовые движения и кризис идентичности биткоина

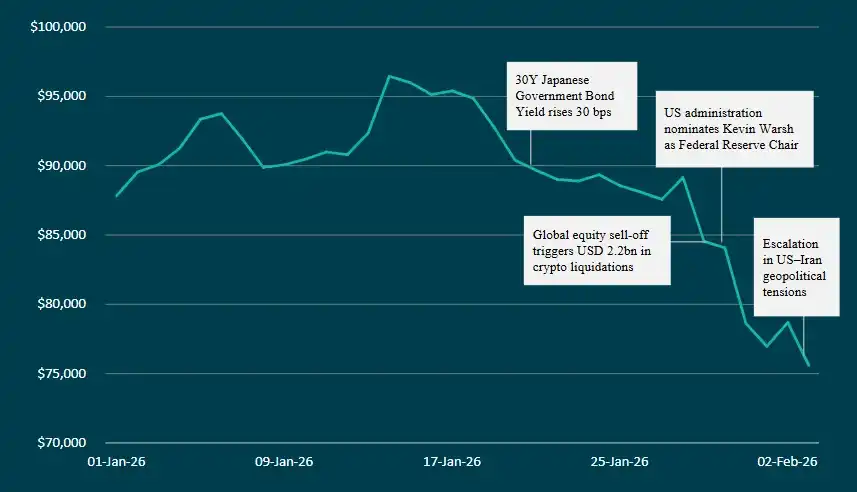

Макрошок выявил неприятную правду об эволюции биткоина как институционального актива. Последняя неделя января породила один из самых серьезных однодневных разрывов в институциональную эпоху.

29 января биткоин упал с 96 000 долларов до 80 000 долларов, потеряв около 15% за один день. На рынке криптодериватов было ликвидировано более 22 миллиардов долларов leveraged позиций. Важность этого движения заключалась не в его величине, а в его корреляционных характеристиках.

Биткоину не удалось decouple (разделиться) с акциями, вместо этого он торговался синхронно с высокобета-технологическими акциями. Во время глобального события делевериджа он вел себя не как защитный актив, а как инструмент, чувствительный к ликвидности.

К началу февраля индикаторы настроений отражали крайний пессимизм. Индекс страха и жадности для криптовалют упал до 19, а ключевые технические уровни, включая уровень 0,786 Фибоначчи в 85 400 долларов, были решительно пробиты. Высокий диапазон 70 000 долларов стал основной зоной структурной поддержки рынка.

Рис. 2: Падение цены биткоина, вызванное глобальными макрособытиями (январь-февраль 2026 г.)

Источник: AMINA Bank

Корреляционные характеристики подняли фундаментальные вопросы о роли биткоина в институциональных портфелях. Если во время стресса он ведет себя как высокобета-технологический прокси, а не как защитный хедж, инвестиционный тезис должен быть соответствующим образом скорректирован. Тем не менее, институциональные обязательства продолжались несмотря ни на что, что позволяет предположить, что зрелые инвесторы оценивают долгосрочную структурную роль биткоина, а не его краткосрочное корреляционное поведение.

Эволюция протоколов и конкурентная дифференциация

Несмотря на падение цен и ухудшение макроусловий, разработка на базовом уровне продолжалась без перерыва. Это демонстрирует ключевую особенность текущего цикла: разработка инфраструктуры отвязалась от ценового импульса.

Ethereum остается сфокусированным на масштабировании через повышение эффективности исполнения, устойчивости к цензуре и смягчении MEV. Предстоящее обновление Glamsterdam aims увеличить лимит газа до 200 миллионов, теоретическая пропускная способность приблизится к 10 000 TPS.

Solana pursues агрессивное повышение производительности. Ее обновление Alpenglow aims сократить время финализации транзакций с 12,8 секунд до примерно 100-150 миллисекунд, позиционируя ее как один из самых быстрых settlement слоев в production.

Эти технологические усовершенствования продолжаются независимо от рыночных настроений, отражая долгосрочные капитальные обязательства и инженерное развитие, не зависящее от ценового поведения.

Потери из-за взломов подчеркивают операционные риски

Даже по мере созревания институциональной инфраструктуры инциденты безопасности подчеркивают сохраняющуюся операционную уязвимость. В январе 2026 года было зарегистрировано более 370 миллионов долларов украденных средств, что стало самым высоким месячным показателем почти за год. Более 311 миллионов долларов убытков произошло из-за фишинговых атак и атак с помощью социальной инженерии, а не из-за сбоев смарт-контрактов.

Крупнейшее отдельное событие, превышающее 280 миллионов долларов, involved атаку с использованием AI-генерированного голосового мошенничества (voice impersonation) на пользователей аппаратных кошельков. Эти инциденты подчеркивают структурный сдвиг в рисках. Человеческая и операционная уязвимость теперь представляют основную поверхность атаки для институциональных участников крипторынка.

Эта модель усиливает, почему кастодиальные框架 (фреймворки), работающие под regulatory oversight, предлагают конкурентные преимущества, выходящие за рамки compliance. Протоколы операционной безопасности, институциональный ключевой менеджмент и страховые框架 стали обязательными условиями.

Заключение

Откат января-февраля 2026 года — это не отказ от цифровых активов, а их переоценка в условиях меняющейся глобальной денежной системы. Криптовалюты теперь напрямую реагируют на рынки суверенных облигаций, руководство центральных банков и геополитическую эскалацию. Эта чувствительность привносит волатильность, но она также подтверждает интеграцию.

В то же время институциональное внедрение, нормативная ясность и разработка протоколов продвигались вперед во время распродаж. Токенизация перешла от нарратива к развернутой инфраструктуре, финансовая система, нативная для кошельков, — от теории к реализации.

Начало 2026 года не ознаменовало крах крипторынка. Оно ознаменовало его первое настоящее стресс-тестирование институциональной зрелости. Хотя цены не прошли тест, базовая инфраструктура прошла его с отличием.

Расхождение между ценовым поведением и структурным прогрессом не может продолжаться бесконечно, поскольку институциональное развертывание, регуляторные разъяснения и зрелость инфраструктуры в конечном итоге отразятся на рыночных оценках.