Этот отчет подготовлен Tiger Research. Что, если бы заблокированные в мостах активы можно было использовать? Мы глубоко проанализировали Katana — блокчейн, который никогда не спит. Он реинвестирует 100% ончейн- и офчейн-доходов, а также комиссий за транзакции в DeFi.

Ключевые моменты

- Большинство Layer 2 блокируют активы в мостах, не используя их. Katana размещает эти активы в кредитных протоколах Ethereum для получения дохода, а затем перераспределяет этот доход в качестве стимулов для протоколов DeFi.

- Хранение активов в хранилище не приносит никакого дохода. Пользователи должны разместить капитал в протоколах DeFi Katana, чтобы получить дополнительные вознаграждения.

- По состоянию на третий квартал 2025 года, более 95% TVL Katana активно размещено в протоколах DeFi. Это контрастирует с большинством сетей, где уровень утилизации составляет от 50% до 70%.

- Katana реинвестирует 100% чистого дохода от комиссий секвенсора в обеспечение ликвидности, поддерживая стабильные условия для торговли даже в периоды рыночной волатильности.

1. Почему капитал простаивает

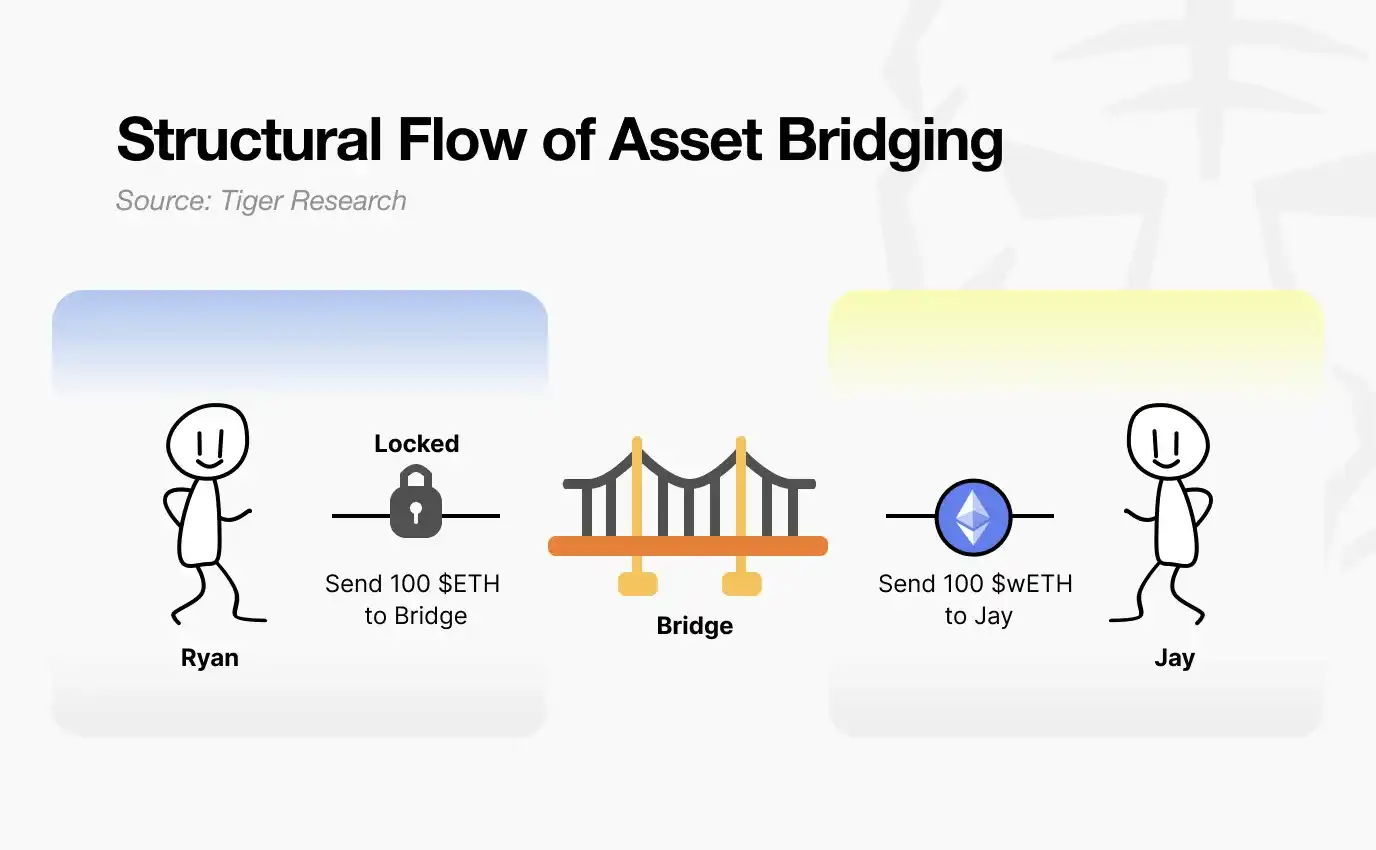

Что происходит с вашими средствами, когда вы переходите с Ethereum на Layer 2?

Источник: Tiger Research

Большинство людей думают, что их активы просто перемещаются. На самом деле, этот процесс больше похож на заморозку. Когда вы вносите активы в контракт моста, он принимает их на хранение. Layer 2 чеканит эквивалентное количество токенов. Вы можете свободно торговать на Layer 2, но ваши исходные активы в мейннете остаются заблокированными и неиспользуемыми.

Источник: Tiger Research

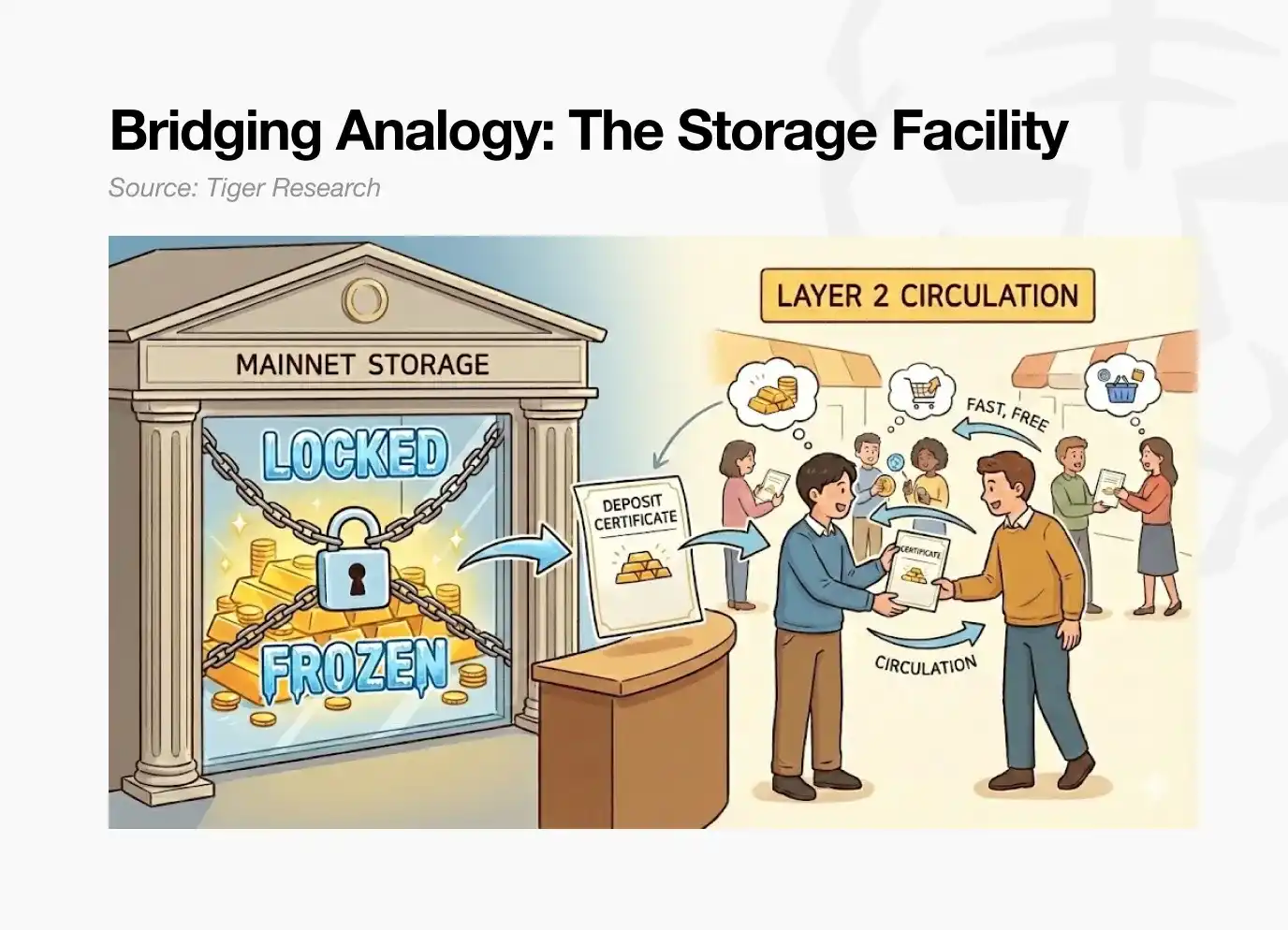

Рассмотрим простую аналогию. Вы оставляете вещи на складском объекте и получаете квитанцию на извлечение. Эту квитанцию можно передать другому человеку. Но сами предметы остаются на складе до тех пор, пока вы их не заберете.

Так работает большинство мостов Layer 2. Активы, находящиеся на хранении в смарт-контрактах Ethereum, не приносят никакого дохода. Они пассивно ждут, пока пользователи не выведут их обратно в мейннет.

А что, если бы депозиты в мостах в мейннете могли приносить доход в DeFi, в то время как вы по-прежнему могли бы совершать быстрые и дешевые транзакции на Layer 2?

Katana прямо отвечает на этот вопрос. Капитал, поступающий в мост, не простаивает. Он используется.

2. Как Katana заставляет капитал работать

Katana активирует капитал с помощью трех механизмов:

- Кроссчейн-активы размещаются на кредитных рынках Ethereum для получения дохода.

- Доход от комиссий за транзакции реинвестируется в пулы ликвидности.

- Нативный стейблкоин AUSD получает доход от казначейских облигаций США.

Работает как внешний капитал, так и капитал, генерируемый внутри сети. Эти три механизма вместе устраняют неиспользуемые активы в Katana.

2.1. Vault Bridge (Мост-Хранилище)

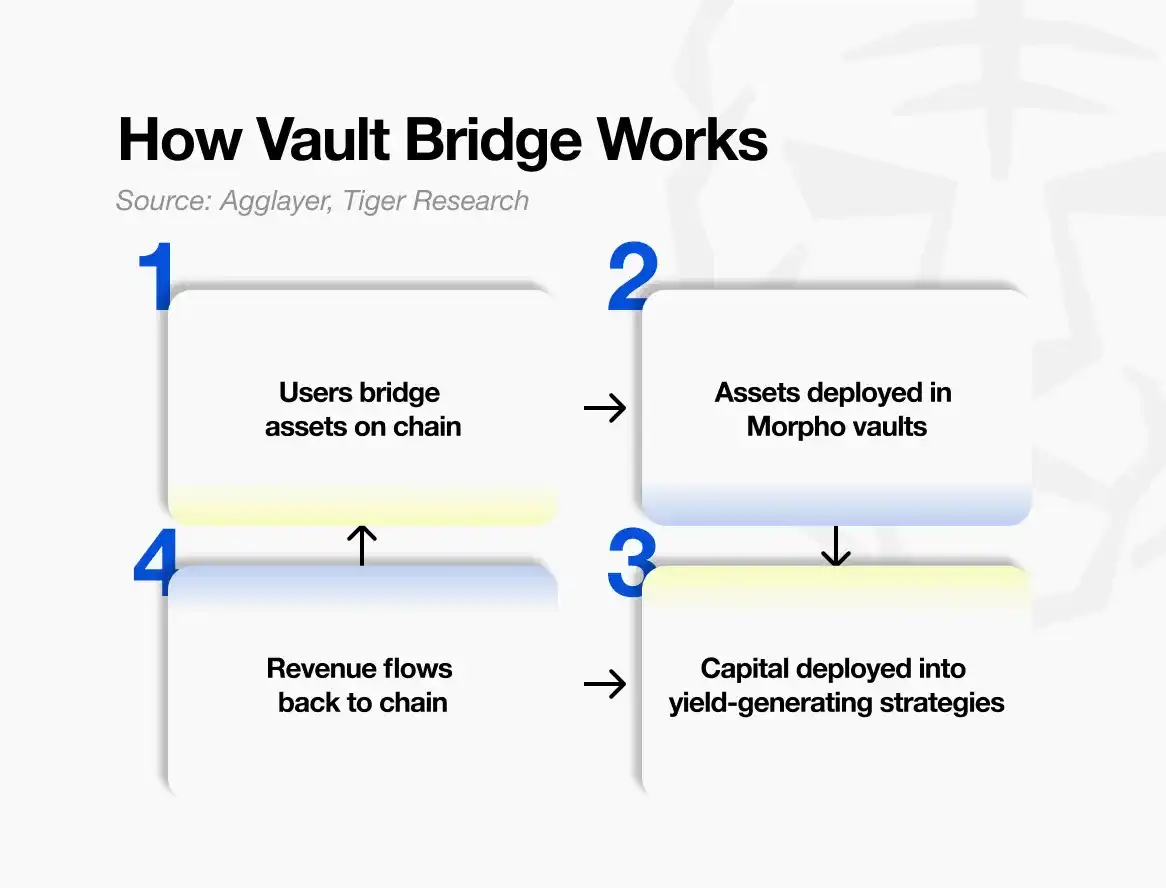

Первый механизм — это Vault Bridge. Когда пользователь отправляет активы в Katana, исходные активы, оставшиеся в мейннете Ethereum, размещаются на кредитных рынках для получения процентов.

Источник: Agglayer, Tiger Research

Когда вы переводите USDC из Ethereum в Katana, эти активы не просто блокируются. В мейннете Ethereum они размещаются в проверенных стратегиях хранилищ (vault strategies) Morpho (популярного кредитного протокола). Генерируемый доход не распределяется напрямую между отдельными пользователями, а собирается на уровне сети и затем перераспределяется в качестве вознаграждений для ключевых рынков DeFi в Katana.

В Katana пользователь получает соответствующий vbToken, например, vbUSDC. Этот токен можно свободно использовать в экосистеме DeFi Katana.

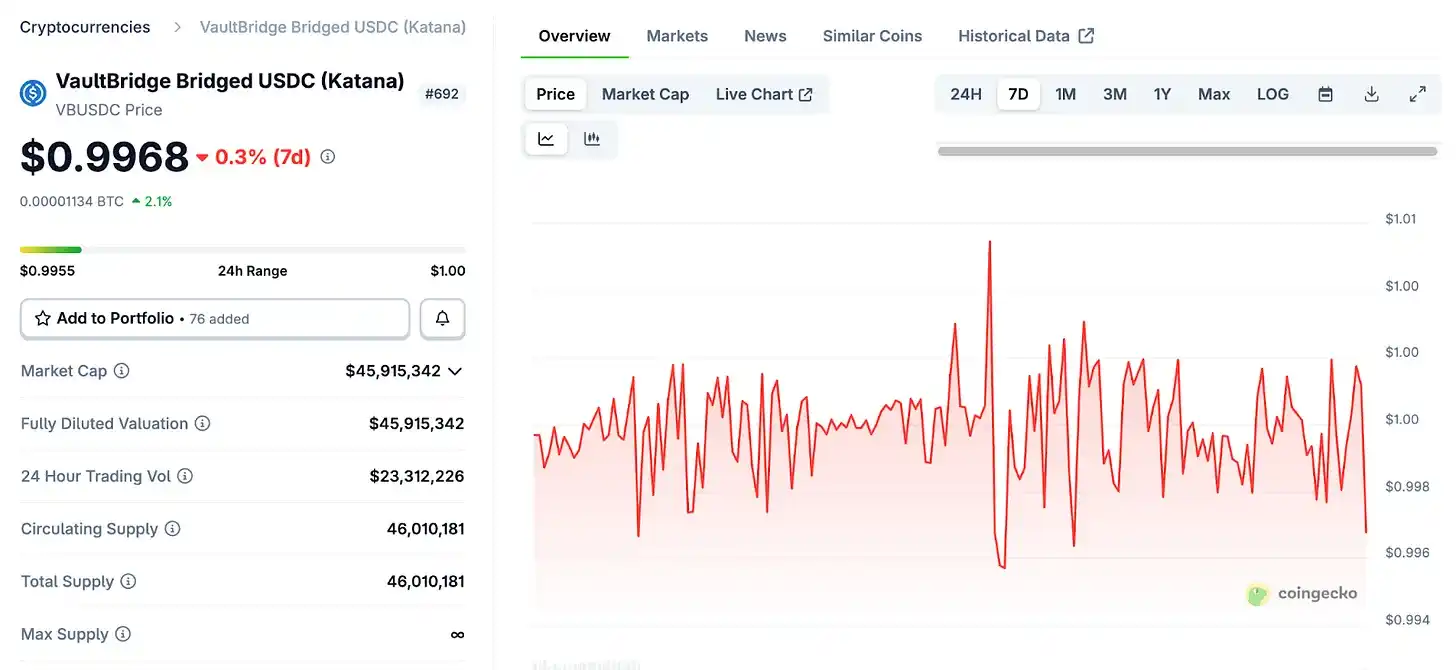

Здесь важно прояснить распространенное заблуждение. vbToken нельзя приравнивать к стейкинг-деривативам, таким как stETH от Lido. stETH автоматически увеличивается в стоимости по мере накопления стейкинг-вознаграждений.

Источник: Coingecko

Механизм vbToken совершенно иной. При хранении vbUSDC в кошельке его количество и цена не увеличиваются. Доход, генерируемый Vault Bridge в Ethereum, не поступает к отдельным держателям vbToken, а направляется в пулы DeFi Katana. Эти средства периодически распределяются по сети для усиления стимулов в пулах ликвидности Sushi и на кредитных рынках Morpho.

Пользователи получают выгоду, только активно размещая свои vbToken. Внося vbToken в пулы ликвидности Sushi или в кредитные стратегии, предлагаемые такими платформами, как Yearn, пользователи могут зарабатывать базовый доход плюс дополнительные вознаграждения от Vault Bridge. Простое хранение vbToken не приносит никакого дохода.

Katana вознаграждает активное использование активов, а не пассивное хранение. Капитал, который находится в движении, получает награду, а бездействующий капитал — нет.

2.2. Собственная ликвидность цепи (Chain-owned Liquidity, CoL)

Второй механизм — это собственная ликвидность цепи (CoL). Katana получает 100% чистого дохода от комиссий секвенсора (т.е. платы за обработку транзакций за вычетом затрат на settlement в Ethereum).

Фонд использует эти средства, чтобы напрямую стать поставщиком ликвидности, предоставляя активы в пулы для торговли на Sushi и на кредитные рынки Morpho. Этой ликвидностью владеет и управляет сама сеть.

Это создает самоподкрепляющийся цикл. По мере того как пользователи совершают сделки в Katana, комиссии секвенсора накапливаются. Эти комиссии преобразуются в собственную ликвидность цепи, что further углубляет пулы. Спреды уменьшаются, кредитные ставки стабилизируются, пользовательский опыт улучшается. Лучший опыт привлекает больше пользователей, что генерирует больше комиссий. Цикл повторяется.

Теоретически, такая структура особенно эффективна в условиях рыночного спада. Внешняя ликвидность обладает высокой мобильностью и часто быстро уходит в периоды рыночного стресса. В contrast, собственная ликвидность цепи предназначена для постоянного нахождения на месте, позволяя пулам продолжать функционировать и более эффективно поглощать рыночные потрясения.

На практике это резко контрастирует с большинством систем DeFi, которые полагаются на эмиссию токенов для стимулирования внешнего капитала. Непосредственно поддерживая свою собственную ликвидность, сеть стремится к более стабильной и устойчивой работе.

2.3. Доход AUSD от казначейских облигаций

Третий механизм — это AUSD, нативный стейблкоин Katana. AUSD обеспечен казначейскими облигациями США, и офчейн-доход от этих активов поступает в экосистему Katana.

Источник: Agora

AUSD выпускается Agora. Обеспечение, поддерживающее AUSD, инвестировано в физические казначейские облигации США. Проценты, полученные от этих облигаций, накапливаются офчейн, а затем периодически передаются в сеть Katana для усиления стимулирования пулов, номинированных в AUSD.

Если Vault Bridge приносит ончейн-доход, то AUSD приносит офчейн-доход. Эти два источника дохода fundamentally различны. Доход от Vault Bridge колеблется в зависимости от состояния рынка DeFi в Ethereum, в то время как доход от AUSD привязан к ставкам по казначейским облигациям США и относительно стабилен.

Это диверсифицирует структуру доходов Katana. Когда ончейн-рынки волатильны, офчейн-доход обеспечивает буфер; когда ончейн-доходы низки, доходность от казначейских облигаций поддерживает общий доход. Эта структура охватывает как крипторынок, так и традиционные финансы.

3. Блокировка капитала vs Заставление капитала работать

Как упоминалось ранее, большинство существующих кроссчейн-мостов выбирают простую блокировку активов по причине — безопасности. Когда активы не двигаются, дизайн системы остается простым, а поверхность атаки ограничена. Большинство сетей Layer 2 используют этот подход. Хотя это безопасно, капитал простаивает.

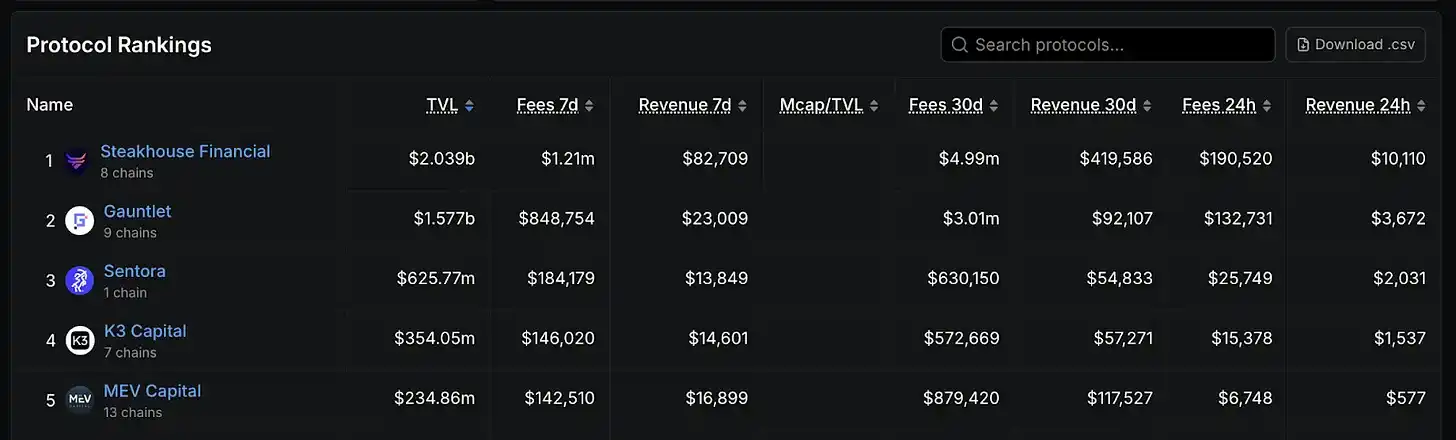

Katana занимает противоположную позицию. Активация бездействующих активов introduces дополнительный риск, и Katana очень откровенна в отношении этого компромисса. Сеть не избегает риска, а сотрудничает с опытными экспертами по управлению рисками в сфере DeFi, включая такие компании, как Gauntlet и Steakhouse Financial.

Источник: DefiLlama

Gauntlet и Steakhouse Financial — это опытные управляющие рисками в сфере DeFi с большим опытом установки параметров для основных кредитных протоколов и консультирования ведущих DeFi-проектов. Их роль аналогична роли профессиональных asset management компаний в традиционных финансах: они оценивают, в какие протоколы следует размещать капитал, определяют разумный размер позиций и постоянно monitor риски.

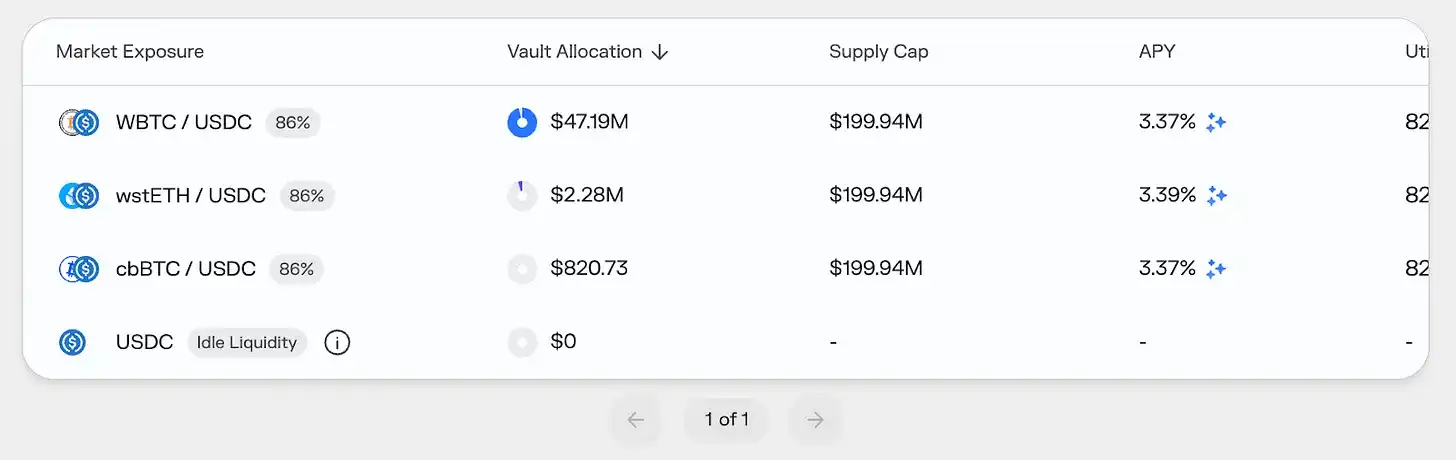

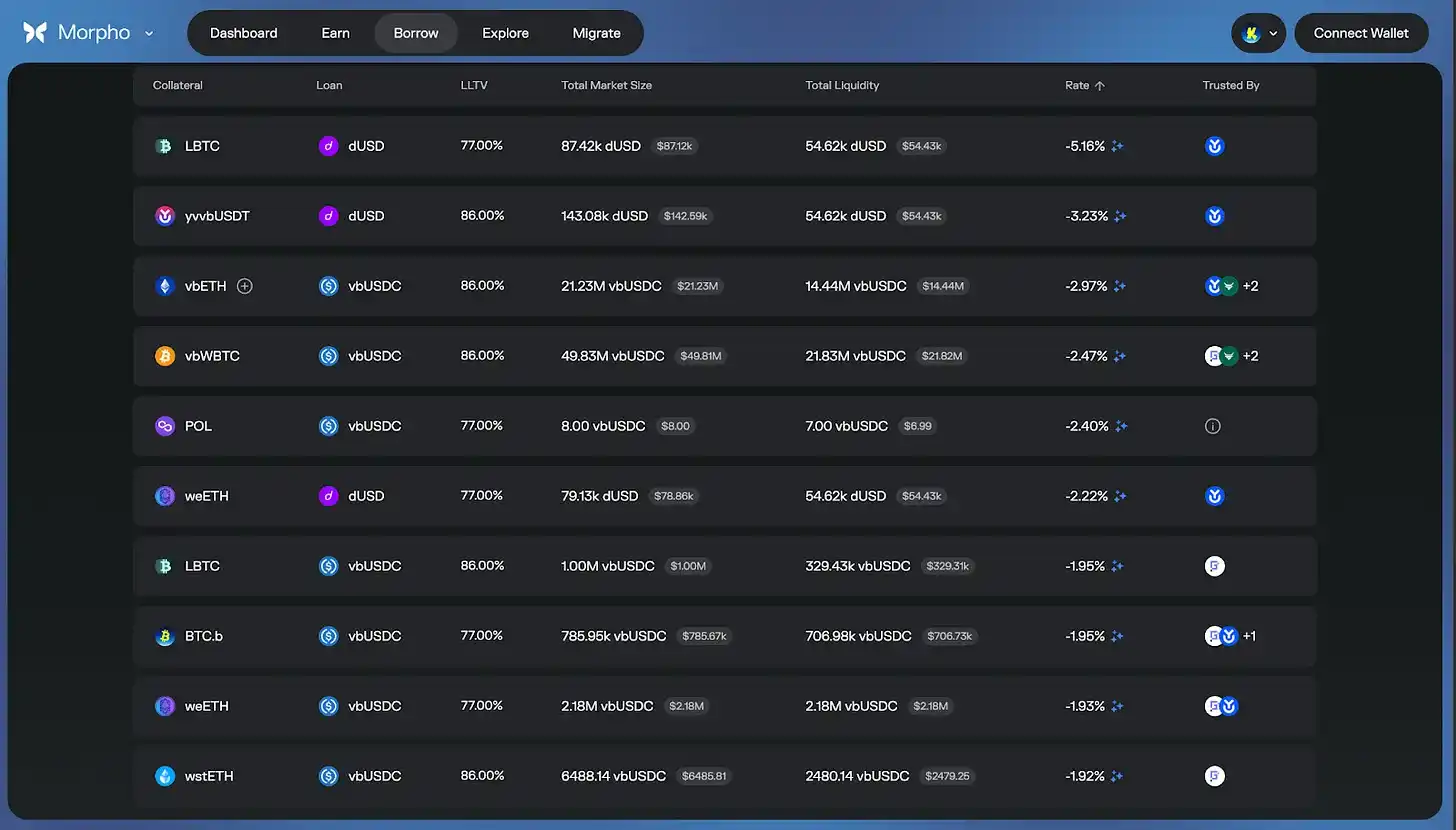

Источник: Morpho

Ни одна финансовая система не может обеспечить 100% гарантию безопасности, поэтому беспокойство по поводу остаточного риска обоснованно.

Тем не менее, Katana сотрудничает с ведущими управляющими рисками и поддерживает консервативную структуру хранилищ. Внутренний комитет по рискам oversees операции. Дополнительные меры безопасности включают в себя такие механизмы защиты, как буфер ликвидности, предоставляемый Cork Protocol.

4. DeFi-утопия, создаваемая Katana

Текущий рынок DeFi сталкивается с проблемой фрагментации ликвидности. Пулы, торгующие одинаковыми активами, разбросаны по разным блокчейнам и протоколам, что снижает эффективность исполнения, увеличивает проскальзывание и снижает утилизацию капитала. Некоторые пользователи извлекают выгоду из этих неэффективностей через арбитраж, но большинство несет более высокие издержки.

Katana решает эту проблему на системном уровне.

Vault Bridge и собственная ликвидность цепи концентрируют ликвидность в ключевых протоколах. Результат: повышение эффективности исполнения сделок, снижение проскальзывания, стабилизация кредитных ставок. Что наиболее важно, доход от бездействующих активов в мейннете Ethereum накладывается на базовую доходность, повышая общую прибыль.

Источник: Morpho

Структура стимулирования Katana также может в определенные моменты значительно снижать фактические затраты на заимствование, даже создавая отрицательные процентные ставки в зависимости от рыночных условий и программ вознаграждений. Это происходит потому, что доходы от Vault Bridge, CoL и AUSD реинвестируются в ключевые рынки. Однако важно отметить, что это стимулирования, зависящие от рыночных условий.

Именно поэтому, по состоянию на третий квартал 2025 года, более 95% TVL Katana было активно размещено в протоколах DeFi. Для сравнения, утилизация капитала в большинстве сетей составляет лишь от 50% до 70%. В конечном счете, Katana создает цепь, где капитал никогда не спит, — систему, которая по-настоящему вознаграждает фактическое использование.

Katana никогда не спит.