Автор: Four Pillars

Компиляция: AididaoJP, Foresight News

Ключевые моменты

- Токен ≠ Акция. Для оценки следует использовать Стоимость предприятия / Доход держателей, а не Стоимость предприятия / Доход протокола.

- Коэффициент начисления (доля дохода протокола, которую в конечном итоге получают держатели) — это ключевой диагностический показатель. Среди сравниваемых нами проектов этот коэффициент варьировался от 25% до 100%.

- «Разводнение» тоже бывает разным. Стимулирование команды — это реальная операционная стоимость (должна учитываться в мультипликаторах оценки), а распродажа инвесторами после разблокировки — это рыночное событие (не должно учитываться в мультипликаторах).

- Ценность казначейства зависит от «возможности извлечения». Вопрос не в том, «сколько денег в казначействе», а в том, «смогут ли держатели их получить?»

Я часто вижу распространённую ошибку в оценке криптовалют: кто-то берёт протокол с годовым доходом от комиссий в 500 миллионов долларов, делит рыночную капитализацию на эту цифру, получает однозначный мультипликатор и затем объявляет его «дешёвым». В этом расчёте неверен и знаменатель, и числитель. Инвестор думает, что покупает с мультипликатором 5, но с учётом дохода, который он действительно получит, этот мультипликатор может быть 20.

Коэффициент P/E — хорошая отправная точка, но он игнорирует балансовый отчёт и структуру капитала — именно поэтому в традиционных финансах используются мультипликаторы на основе стоимости предприятия (EV/EBITDA). Однако при попытке применить концепцию EV/EBITDA к токенам возникают три фундаментальные проблемы:

- Активы казначейства: у держателей нет законных прав требования.

- Доход протокола: большая его часть может вообще не дойти до держателей.

- Основная стоимость: отражается не в отчёте о прибылях и убытках, а в форме эмиссии новых токенов.

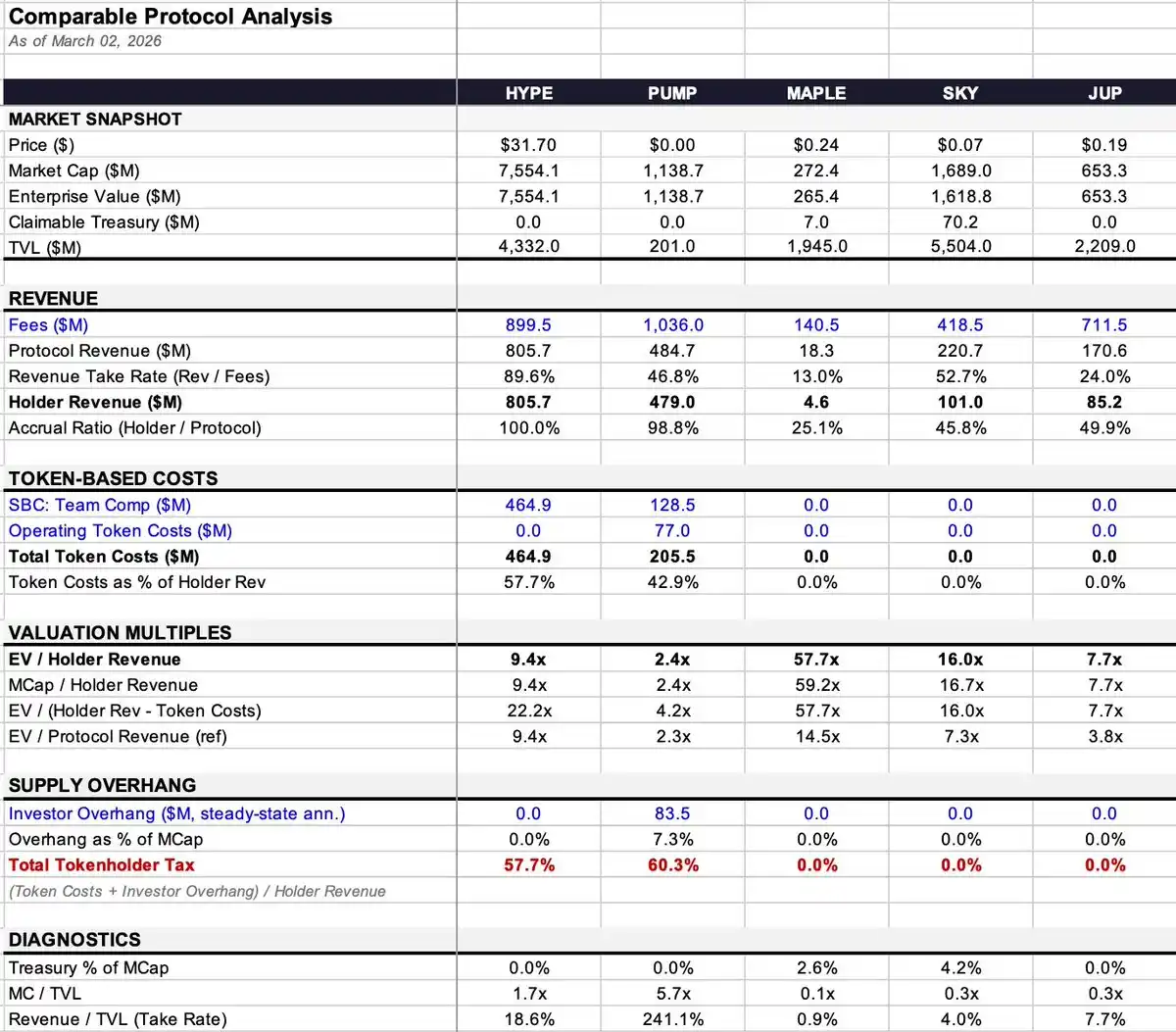

Данная статья aims to построить framework оценки, адаптированный к особенностям токенов. Ключевым показателем является Стоимость предприятия / Доход держателей — то есть цена, которую вы платите за каждый доллар дохода, который в конечном итоге попадёт в ваш карман (как держателя токенов), с одновременным учётом влияния балансового отчёта и реальных операционных затрат. Я буду использовать пять протоколов (HYPE, PUMP, MAPLE, JUP, SKY) в качестве примеров для иллюстрации; это не инвестиционная рекомендация, а лишь демонстрация метода.

1. Как рассчитать «Стоимость предприятия» для токена?

Первая ошибка во многих оценках токенов — это отправная точка: прямое использование рыночной капитализации, но рыночная капитализация не равна стоимости предприятия.

В традиционных финансах логика ясна:

Стоимость предприятия = Рыночная капитализация + Долг - Денежные средства

Потому что если вы покупаете всю компанию, вы берёте на себя долг, но также забираете денежные средства. Вычитание денежных средств оправдано, потому что эти деньги по закону ваши.

Но в криптомире всё сложнее. От автоматического сжигания (поступление USDC, токены безвозвратно уничтожаются, никто не получает эти USDC) до кошельков фондов (лежат миллиарды долларов, но нет ни прав управления, ни механизмов распределения) — ситуации бывают разными. Ключевой вопрос не в том, «что в казначействе», а в том, «смогут ли держатели это извлечь?» (Конечно, если кто-то приобретёт весь протокол, дисконт на право требования исчезает, как и в традиционных финансах. Здесь «дисконт на право требования» в основном относится к нам, держателям миноритарных долей.)

Я использую термин «Стоимость предприятия», потому что логика схожа: вы рассчитываете, сколько нужно заплатить за получение основного бизнеса, одновременно исключая части баланса, которые вам не принадлежат. Формула следующая:

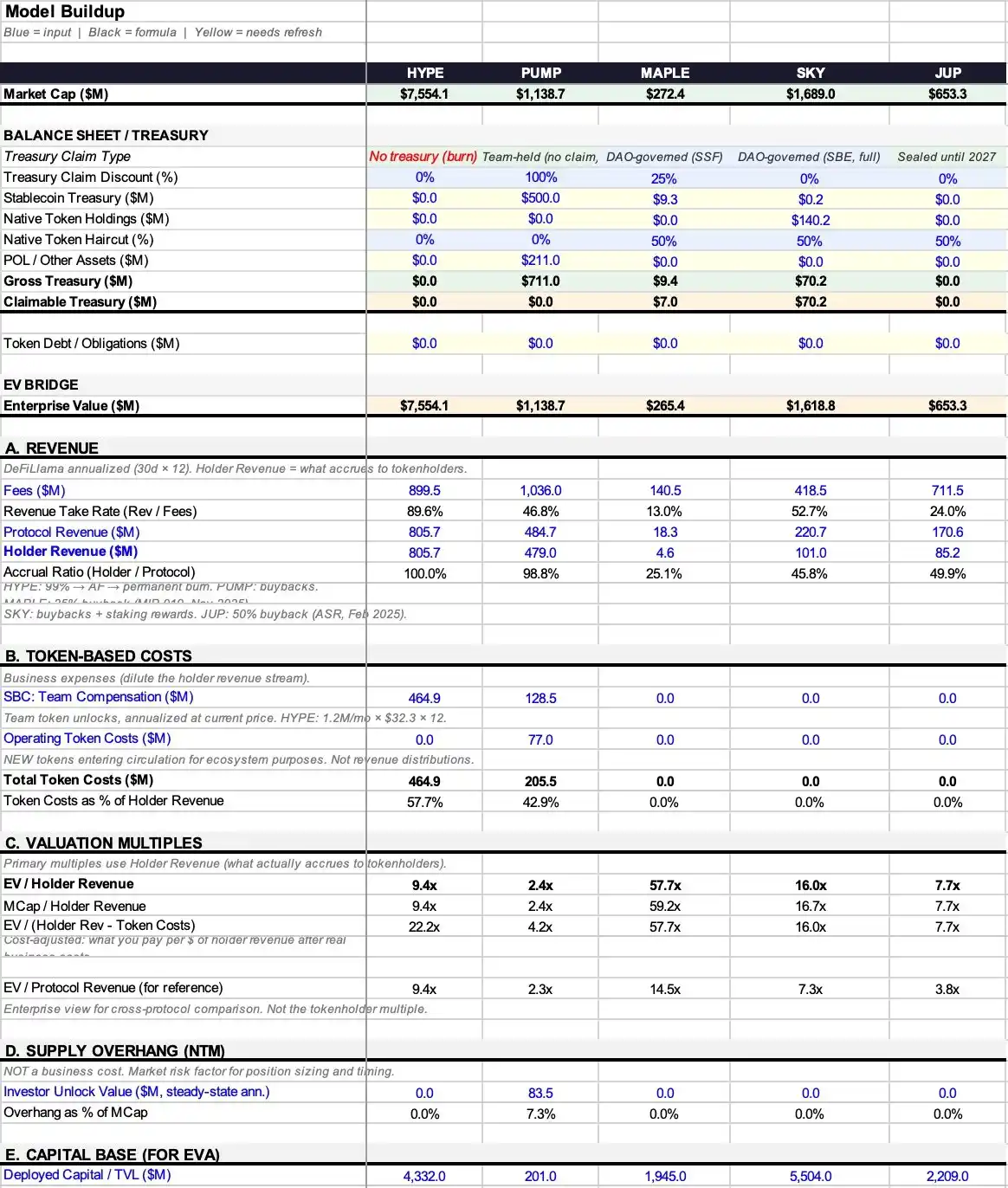

Стоимость предприятия токена = Рыночная капитализация + Токенизированный долг - Извлекаемые активы казначейства

В настоящее время у большинства протоколов ещё нет «токенизированного долга», поэтому акцент обычно делается на активах казначейства.

Сначала разберём, что находится в казначействе. Казначейство протокола обычно хранит три типа активов:

- Стейблкоины: реальные деньги, в принципе, могут быть полностью извлечены.

- Собственные токены: свои собственные токены. Вычитание этой части эквивалентно «вычитанию самого себя», обычно требует дисконта как минимум 50%.

- Локвидность, принадлежащая протоколу (POL), и другие активы.

Общие активы казначейства = Стейблкоины + Собственные токены × (1 - Подходящий вам коэффициент дисконта) + POL

Но общие активы ≠ Извлекаемые активы, и это именно та ключевая проблема, которую решает этот framework.

У некоторых протоколов даже нет казначейства, которое можно дисконтировать. Например, механизм чистого сжигания (поступление USDC, используется для выкупа и сжигания токенов) не формирует активы баланса, которые кто-либо может получить. В этом случае Извлекаемые активы казначейства = 0, Стоимость предприятия = Рыночная капитализация. Это самый ясный случай, не требующий субъективных суждений.

Для казначейств, которые действительно держат реальные активы, я ввожу framework «Дисконта на право требования», принимая значение от 0% до 100% в зависимости от степени фактического контроля со стороны держателей:

- Дисконт 0%: Автоматический выкуп и сжигание, не требующие голосования по управлению; или использование средств полностью определяется держателями токенов.

- Дисконт 25%: Существует активное DAO и реальная история распределения.

- Дисконт 50%: Права управления есть, но только на бумаге, никогда реально не осуществлялись.

- Дисконт 75%: Казначейство контролируется командой, управление слабое.

- Дисконт 100%: Средства контролируются фондом, у держателей нет никаких прав требования.

Эти проценты — самая субъективная и уязвимая часть всего framework, я признаю. Но спор двух аналитиков о том, 25% это или 50%, гораздо значимее, чем если бы они оба игнорировали казначейство и говорили только о P/E.

Рассмотрим практические примеры:

- Maple: В казначействе 9,36 млн долларов (99,7% — стейблкоины), сумма небольшая. Стоимость предприятия скорректирована с 272 млн долларов до 265 млн долларов, влияние незначительное.

- SKY: В казначействе 140,3 млн долларов, но 99,9% — это собственные токены. Применив дисконт 50%, я считаю извлекаемую стоимость равной 70,2 млн долларов, стоимость предприятия снизилась с 1,69 млрд долларов до 1,62 млрд долларов.

- PUMP: По сообщениям, holds около 700 млн долларов стейблкоинов, но нет механизма управления и каналов распределения, держатели просто не могут их получить. Следовательно, Извлекаемые активы = 0, Стоимость предприятия = Рыночная капитализация.

- HYPE и JUP: Аналогично, чистое сжигание или закрытое казначейство, не требуют суждений, Стоимость предприятия = Рыночная капитализация.

2. Доход и стоимость токена: сколько на самом деле достанется мне?

Разрыв между деньгами, которые зарабатывает протокол, и деньгами, которые получают держатели, — это место, где терпят неудачу большинство frameworks оценки, и это ключ, который действительно влияет на мультипликаторы оценки.

Можно представить доход как трёхуровневый водопад:

- Комиссии: Общая сумма, уплаченная пользователями.

- Доход протокола: Часть, которую протокол оставляет себе после выплат LP, валидаторам и другим «поставщикам».

- Доход держателей: Часть, которая в конечном итоге доходит до держателей токенов через выкуп, сжигание или прямое распределение.

Между ними есть два ключевых коэффициента конверсии:

- Коэффициент удержания = Доход протокола ÷ Комиссии (сколько протокол может оставить от общих комиссий)

- Коэффициент начисления = Доход держателей ÷ Доход протокола (какая часть оставшегося в конечном итоге доходит до держателей)

Эти два коэффициента в сочетании могут иметь совершенно разный эффект:

- HYPE: Коэффициент удержания 89,6%, коэффициент начисления 100%. Из почти 900 млн долларов комиссий 805,7 млн долларов в конечном итоге пошли держателям.

- Maple: Коэффициент удержания 13% (140,5 млн комиссий → 18,3 млн доход протокола), коэффициент начисления 25,1% (18,3 млн доход протокола → 4,6 млн доход держателей). Совокупная проходимость всего 3%, а у HYPE — 90%.

В рамках одного framework: один 3%, другой 90%. Если вы напрямую сравните эти два протокола с помощью «EV/Комиссии» или даже «EV/Доход протокола», разница будет колоссальной.

Почему в знаменателе используется «Доход держателей», а не «Доход протокола»?

В традиционных финансах EV/Доход可行, потому что держатели акций имеют остаточные права требования — по закону всё принадлежит им. Но у держателей токенов такого права нет, они получают только ту часть, которую предусматривает токеномика. Если доход лежит в казначействе, контролируемом командой, без каких-либо механизмов распределения между держателями, то простое владение governance-токеном не делает этот доход «вашим».

Использование «Дохода протокола» в знаменателе приукрашивает протоколы с низким коэффициентом начисления, заставляя их выглядеть «дешевле», чем они есть на самом деле. Я называю этот разрыв «дисконтом начисления».

На примере Maple:

- EV/Доход протокола = 14,5x

- EV/Доход держателей = 57,7x

Целых 4 раза разницы! На основе одних и тех же данных, но разных знаменателей, ваше суждение о том, «сколько просит рынок», будет совершенно разным.

3. Затраты: разводнение тоже бывает разным

Слово «разводнение» в криптосфере используется слишком широко; неправильная классификация ведёт к ошибке в оценке.

Тип 1: Стимулирование команды (опционы) — Это операционные затраты

Баффетт decades ago: если стимулирование — не затраты, то что это? Подарок? В традиционных финансах это отражается в отчёте о прибылях и убытках, уменьшая прибыль. В криптомире это проявляется как поступление новых токенов на рынок, но экономическая суть完全相同 — это реальная стоимость ведения бизнеса.

- HYPE: Годовое стимулирование команды 464,9 млн долларов, потребляет 57,7% дохода держателей.

- PUMP: Годовое стимулирование команды 128,5 млн долларов.

Это должно учитываться в мультипликаторах оценки.

Тип 2: Операционные затраты в токенах (стимулирование экосистемы, привлечение пользователей и т.д.) — Это тоже операционные затраты

Они действуют как стоимость привлечения пользователя, также являются реальными расходами и должны учитываться в мультипликаторах. У PUMP, помимо стимулирования команды, есть операционные затраты в токенах в размере 77 млн долларов, общие затраты в токенах составляют 205,5 млн долларов.

Критерий прост: Создаётся ли новое предложение токенов?

Если протокол просто распределяет существующий доход среди стейкеров, не эмитируя новые монеты, то затраты уже отражены в предыдущем денежном потоке (т.е. разница между доходом протокола и доходом держателей).

Если протокол чеканит или разблокирует токены, которых ранее не было в обращении, это реальное разводнение, стоимость бизнеса.

Тип 3: Разблокировка инвесторами после окончания периода блокировки — Это рыночное событие, а не операционные затраты

Вы не вычитаете продажи венчурных капиталистов из прибыли Apple, чтобы получить «скорректированную прибыль». Точно так же это не должно учитываться в операционных мультипликаторах.

Годовой потенциальный объём продаж инвесторов PUMP составляет 83,5 млн долларов, или 7,3% рыночной капитализации. Это оказывает огромное влияние на движение цен и рыночную динамику, но не является операционными затратами. Я помещаю это отдельно в диагностический показатель под названием «Общий налог на держателей токенов» (т.е. затраты в токенах + потенциальный объём продаж инвесторов, в процентах от дохода держателей), но не включаю в основные мультипликаторы оценки.

4. Четыре основных мультипликатора и один диагностический показатель

Основываясь на приведённой логике, мы получаем следующие показатели (здесь даны единые определения, далее будут использоваться ссылки):

- EV/Доход держателей (ключевой показатель): Сколько вы платите за каждый доллар дохода, который в конечном итоге попадает в ваш карман.

- Рыночная капитализация / Доход держателей: То же самое, но без корректировки на казначейство. Разница между ними отражает влияние балансового отчёта.

- EV/(Доход держателей - Затраты в токенах) (мультипликатор с учётом затрат): Вычитает реальные бизнес-затраты (стимулирование команды, операционные затраты), но исключает объём продаж инвесторов.

- EV/Доход протокола (только для справки): Разница с EV/Доход держателей показывает величину «дисконта начисления».

- Общий налог на держателей токенов (диагностический показатель): = (Затраты в токенах + Объём продаж инвесторов) ÷ Доход держателей. Он одним числом отражает двойное влияние бизнес-затрат и давления предложения. Например, PUMP — 60,3%, означает, что на каждый 1 доллар дохода, поступающий держателям, приходится дополнительные 0,603 доллара в виде нового предложения, обрушивающегося на рынок. Само по себе это число не говорит прямо о valuation, но показывает динамику между денежным потоком и предложением.

5. Краткий обзор данных и ключевые моменты кейсов

- HYPE: Коэффициент начисления 100%, 9,4x доход держателей. Но высокие затраты на стимулирование команды, мультипликатор с учётом затрат повышается до 22,2x. Структура дохода прозрачна, сложность не на стороне дохода.

- PUMP: Кажется самым дешёвым (2,4x), коэффициент начисления 98,8%. Но казначейство невозможно извлечь, и в августе 2026 года ожидается массовая разблокировка. Мультипликатор с учётом затрат повышается до 4,2x, общий налог на держателей токенов достигает 60,3% (максимум в выборке).

- MAPLE: Самый большой дисконт начисления (4x). Доход протокола 14,5x против дохода держателей 57,7x — огромная разница. Нет затрат в токенах, поэтому мультипликатор с учётом затрат не меняется.

- JUP: Самый чистый балансовый отчёт. Благодаря управлению «чистым нулевым выбросом», нет затрат в токенах, нет объёма продаж инвесторов, нет извлекаемого казначейства. Все мультипликаторы стремятся к 7,7x.

- SKY: Коэффициент начисления 45,8%, лучший пример, демонстрирующий «как выбор знаменателя влияет на оценку». Мультипликатор дохода протокола 7,3x (кажется дешёвым), а мультипликатор дохода держателей 16,0x (уже не так дёшево). Казначейство в основном (99,9%) состоит из собственных токенов, стоимость требует дисконтирования.

6. Заключение

У этого framework certainly есть недостатки:

- Дисконт на право требования казначейства субъективен: я ставлю 25%, вы можете поставить 50%, и никто никого не переубедит.

- Суждение «была ли эмиссия» может усложниться: у некоторых протоколов функция чеканки включена, но каналы распределения мертвы, токены накапливаются в нераспределённом пуле, ситуация становится размытой.

- Источники данных зашумлены: Годовые данные DeFiLlama за 30 дней могут из-за different месяцев снимка заставить один и тот же протокол выглядеть дешевле или дороже в два раза.

Но это, по крайней мере, рабочая отправная точка. EV/Доход держателей с корректировкой на балансовый отчёт и реальные бизнес-затраты позволяет чётче понять: за каждый уплаченный вами доллар, сколько дохода вы realmente получаете в свой карман.

Разрыв между деньгами, которые зарабатывает протокол, и деньгами, которые получают держатели, — это крупнейшее фундаментальное несоответствие на текущем рынке. Многие протоколы генерируют сотни миллионов долларов комиссий, а держатели получают лишь крохи, и большинство frameworks оценки даже не различают эти два понятия.

Хорошо, что индустрия начинает уделять внимание capture стоимости: включаются fee switch, выкуп заменяет инфляционный стейкинг, governance голосует за приостановку стимулирования. Мы создаём инструменты, чтобы точнее измерять то, что realmente происходит.

7. Источники данных и методологические примечания

Данные о доходах: Годовые данные DeFiLlama (последние 30 дней × 12). Преимущество — более чувствительны, чем полугодовые данные, недостаток — помехи из-за месячной волатильности.

Доход держателей: Непосредственно используется поле «Holder Revenue» DeFiLlama, включает только выкуп, сжигание, прямое распределение.

Данные казначейства:

MAPLE: 9,36 млн долларов (DeFiLlama, 99,7% стейблкоины)

SKY: 140,3 млн долларов (DeFiLlama, 99,9% собственные токены)

JUP: 0 долларов (закрыто)

PUMP: Стейблкоины, медианная оценка 500 млн долларов (фактический диапазон 286–800 млн долларов)

Затраты в токенах:

MAPLE: 0 долларов. Предложение MIP-019 (октябрь 2025) завершило распределение через стейкинг. Хотя смарт-контракт с инфляцией 5% может всё ещё чеканить, каналов распределения нет. (Источник: docs.maple.finance, The Defiant 2025/10/31)

SKY: 0 долларов. Модуль сбережений (STR) теперь распределяет SPK и Chronicle Points, а не токены SKY. (Проверено в марте 2026 на app.sky.money/rewards). Данные Rune за август 2024 года о «600 млн SKY в год» устарели, но governance может в любое время перезапустить. (Источник: sky.money FAQ, vote.sky.money)

JUP: 0 долларов. Предложение «Net Zero Emissions» (75% за), принятое 22 февраля 2026 года. Казначейство DAO закрыто до 2027 года.

Объём продаж инвесторов:

PUMP: Стабильный годовой объём 83,5 млн долларов. Фактический обрыв блокировки начинается в августе 2026 года, фактический объём продаж в следующие 12 месяцев составляет около 48,7 млн долларов (рассчитано как 7/12 месяцев).

Показатели кредитных протоколов:

MAPLE: Используется фактический Assets Under Management (AUM) (3,79 млрд долларов, отчёт за Q1 2026), а не TVL DeFiLlama (1,945 млрд долларов). Чистая процентная маржа (NIM) = Доход протокола / AUM. Подробные показатели см. в приложении Excel.

Операционные денежные расходы: Не оценивались. Поскольку протоколы не раскрывают, предположения создадут ложную точность.

Оценка опционов: Рассчитана по текущей цене токена. Чувствительна к изменению цены.