Автор: Клод, Deep Chao TechFlow

Введение Deep Chao: Переговоры между США и Ираном провалились, началась блокада Ормузского пролива, цены на нефть вернулись выше $100, но в понедельник S&P 500 вырос на 1%, полностью отыграв все потери с начала войны с Ираном и достигнув отметки 6886 пунктов. В тот же день JPMorgan, Morgan Stanley и BlackRock выступили с оптимистичными заявлениями, и их ключевая логика едина: прибыль компаний демонстрирует гораздо большую устойчивость, чем геополитические потрясения. На инвестиционном разделе Reddit разгорелись жаркие споры, частные инвесторы восклицают: «Рынок просто игнорирует новости!».

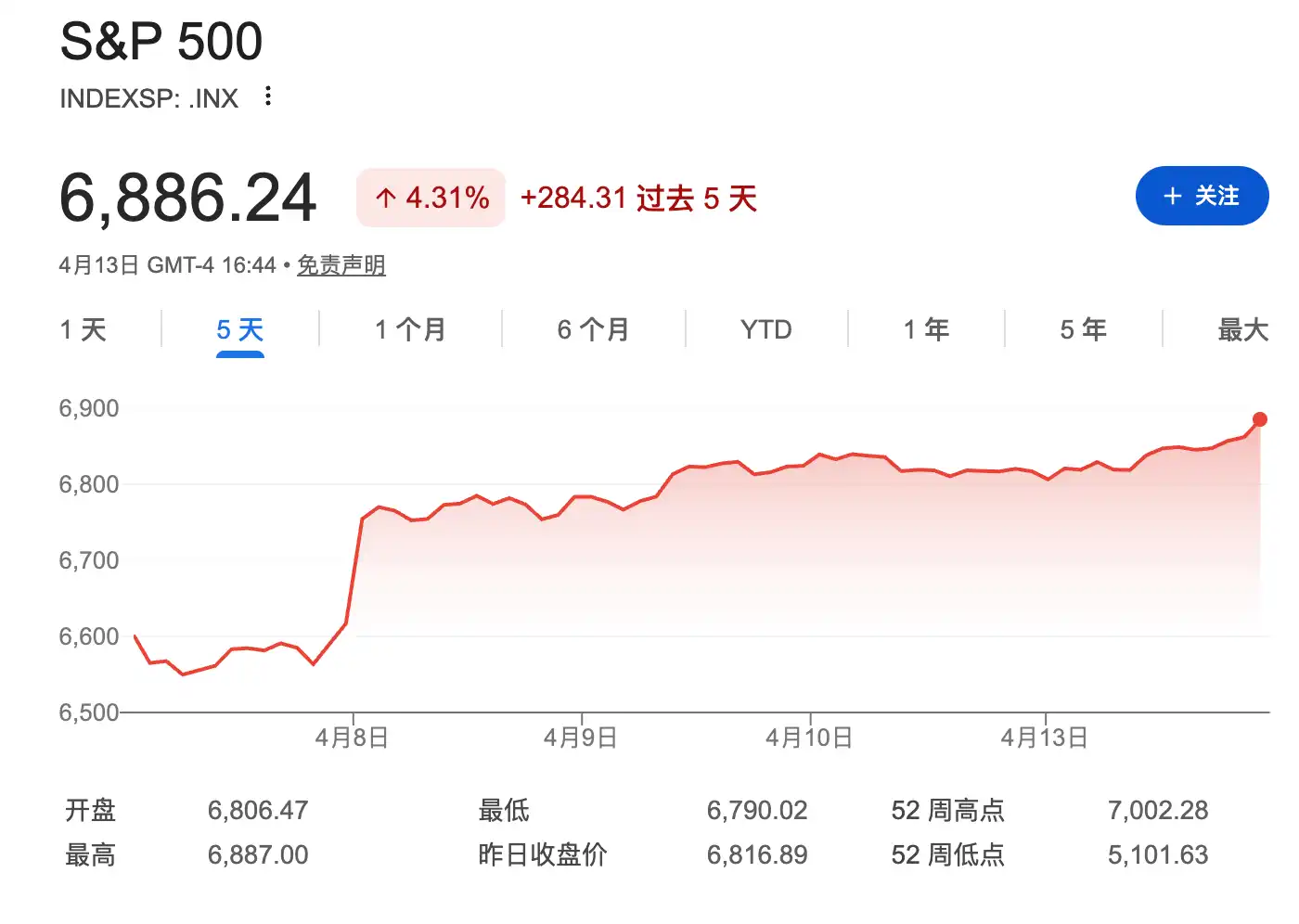

В первый торговый день после провала американо-иранских переговоров американский фондовый рынок продемонстрировал кривую, озадачившую всех.

13 апреля (понедельник) индекс S&P 500 вырос на 69 пунктов (1%) и закрылся на отметке 6886 пунктов; промышленный индекс Dow Jones вырос на 302 пункта (0,6%); композитный индекс Nasdaq вырос на 1,2%. В тот же день Трамп в социальной сети объявил о немедленном начале операции ВМС США по блокаде Ормузского пролива. Нефть марки Brent в ходе торгов превысила $100 за баррель, но затем отступила и закрылась на уровне около $98,16, нефть WTI закрылась на уровне $97,82.

В тот день S&P 500 достиг самого высокого уровня с конца февраля, полностью восстановив все потери с момента начала войны с Ираном. Синхронный рост цен на нефть и фондового рынка кажется логически противоречивым. Однако крупнейшие институты Уолл-стрит дали очень схожее объяснение: прибыль компаний по-прежнему сильна, геополитический шок будет ограничен по продолжительности, и сейчас как раз окно для покупок на просадках.

Три крупные организации в один день выразили оптимизм, ключевая логика указывает на устойчивость прибыли

JPMorgan в отчете, написанном стратегом Миславом Матейкой, заявил, что падения, вызванные геополитическими потрясениями, в конечном итоге должны оказаться возможностью для покупок.

Команда стратега Morgan Stanley Майкла Уилсона оценила, что недавняя распродажа S&P 500 больше похожа на коррекцию, а не на начало устойчивого нисходящего тренда, а поддержку обеспечивают улучшение роста прибыли и возвращение к разумным оценкам. Morgan Stanley продолжает看好 циклические сектора, такие как финансы, промышленность и потребительские товары, а также качественные растущие активы, такие как ИИ и супермощные вычисления.

Институт инвестиционных исследований Blackrock в тот же день повысил рейтинг американских акций с «нейтрального» до «перевеса», став самой активной из трех организаций. Жан Бойвин, руководитель Института инвестиционных исследований Blackrock, заявил, что премия к оценке технологического сектора уже размыта, в то время как ожидаемые темпы роста прибыли сектора в 2026 году выросли до 43% по сравнению с 26% в прошлом году.

Blackrock в своем еженедельном отчете о рынке указал, что уже появились два ориентира, побудивших его вернуться к наращиванию позиций: во-первых, есть реальные доказательства восстановления судоходства через Ормузский пролив, во-вторых,持续性ный ущерб макроэкономике от конфликта оказался управляемым.

Три организации ссылаются на одни и те же данные: по данным LSEG I/B/E/S, по состоянию на 10 апреля ожидаемый рост прибыли S&P 500 в первом квартале составил 13,9%, что выше 12,7% до войны. Другими словами, за почти семь недель с начала конфликта аналитики не только не снизили ожидания по прибыли, но и повысили их.

Сокращение оценки «Великолепной семерки» стало причиной для покупок

JPMorgan в своем отчете特别 отметил, что премия к форвардному P/E «Великолепной семерки» (Magnificent Seven, т.е. NVIDIA, Apple, Microsoft, Meta, Google, Amazon и Tesla) значительно сократилась с предыдущего уровня в 1,7 раза выше S&P 500 до 1,2 раза.

Эти данные являются ключевым аргументом для быков Уолл-стрит: проблема концентрации в верхушке, которая подавляла широту рынка в последние два года, теперь自行缓解 due to возвращению оценок к норме.

Blackrock указал, что премия к оценке технологического сектора по сравнению с другими десятью секторами упала до самого низкого уровня с середины 2020 года. Компания заявила, что на фоне устойчивых ожиданий прибыли компаний и ограниченного ущерба глобальному росту, она выбрала возврат к наращиванию позиций в акциях США и развивающихся рынков.

Исторические данные поддерживают: геополитические шоки обычно消化ляются в течение шести недель

Оптимизм институтов Уолл-стрит не беспочвен. Исследование UBS показывает, что когда S&P 500 падает на 5-10% в течение трех-четырех недель, historically он обычно возвращается к уровню до конфликта в течение шести месяцев.

Обзор LPL Research событий геополитических потрясений со времен Второй мировой войны показывает, что средняя реакция в первый день составляет около -1%, среднее падение от пика до дна около 5%, среднее время достижения дна около 19 дней, а средний周期 восстановления около 42 дней.

UBS в отчете от середины марта указал, что с начала конфликта 28 февраля по 13 марта глобальные акции упали всего на about 5%, в то время как цены на нефть за тот же период выросли на about 40%. Сама «нечувствительность» фондового рынка к шоку цен на нефть подтверждает上述历史ческую закономерность.

UBS 6 апреля снизил целевую цену S&P 500 на конец года с 7700 до 7500, среднесрочную цель с 7300 до 7000, но сохранил общую оценку акций США как «привлекательных», прогноз прибыли на акцию на 2026 год остался неизменным на уровне $310.

Вопросы частных инвесторов на Reddit: «Рынок просто не смотрит новости»

Консенсус институтов еще можно объяснить данными, но реакция сообщества частных инвесторов более наглядно отражает текущие настроения на рынке.

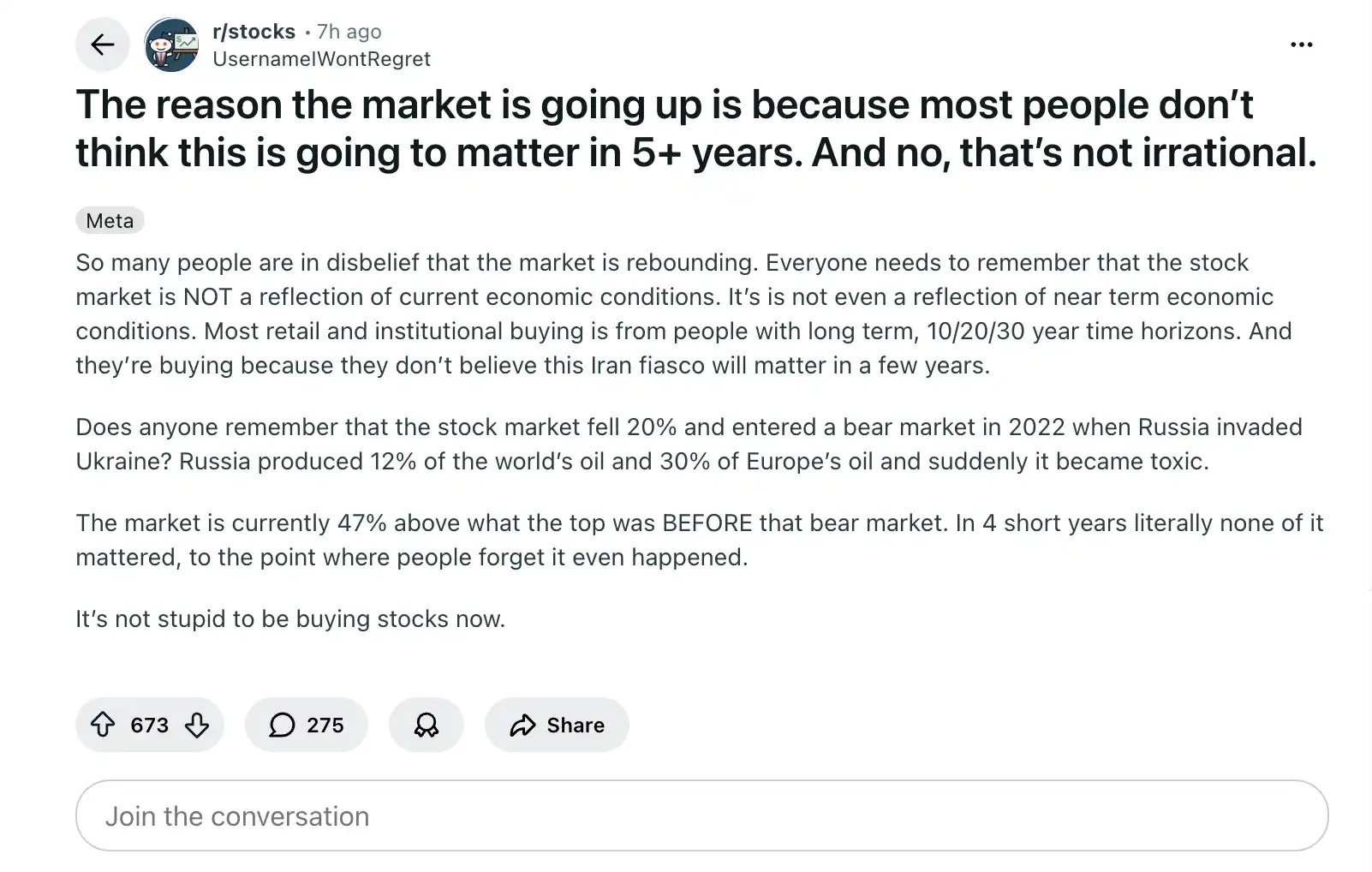

В разделе r/stocks на Reddit пост с заголовком,大致 означающим «Вы теперь верите? Рынок не движется из-за новостей», получил 923 лайка и 159 комментариев. Основная идея автора: рынок движется first, а затем ищет причины. Эта блокада Ормуза является для него самым ярким примером, множество комментариев выражают недоумение по поводу отрыва геополитических рисков от рыночных цен.

«Рынок растет, потому что большинство считает, что через 5 лет это не будет иметь значения, это не нерационально». Этот пост получил 344 лайка и 199 комментариев, представляя типичную позицию долгосрочных инвесторов.

В разделе r/wallstreetbets пост, набравший 504 лайка, указал, что физический нефтяной рынок «кричит о шоке предложения», но фондовый рынок остается спокойным, противоречивые сигналы между двумя рынками сбивают с толку трейдеров.

Недоумение частных инвесторов и уверенность институтов形成鲜明对照, но лежащая в основе логика其实是 две стороны одной медали: институты делают ставку на устойчивость прибыли и ограниченность конфликта, а частные инвесторы недоумевают, почему плохие новости не превращаются в падение.

Ответ может быть прост: рынок уже завершил цикл ценообразования в марте, и сейчас находится на стадии отскока «на выходе плохих новостей».