Автор: David Lopez Mateos

Компиляция: Deep Tide TechFlow

Введение от Deep Tide: СМИ любят обобщать взлеты и падения цен на вычислительные мощности GPU одним числом, но реальность такова: котировки, предоставляемые четырьмя провайдерами индексов на терминале Bloomberg, расходятся более чем на 2 доллара, и их направление и ритм также не совпадают. Автор этой статьи — Дэвид Лопес Матеос, основатель платформы для торговли вычислительными мощностями GPU Compute Desk. Используя данные первичных сделок, он разбирает реальную структуру ценообразования H100 и B200, раскрывая примитивный рынок без консенсусного бенчмарка, без стандартных контрактов, без форвардной кривой — вычислительные мощности накапливаются и пересдаются в аренду, как краткосрочные апартаменты.

Заголовки в СМИ заставят вас думать, что цены на вычислительные мощности GPU стремительно растут. Этот нарратив удобен, идеально вписывается в макроэкономическую рамку «сжатие предложения + бездонный спрос на ИИ» и намекает на успокаивающий факт: у нас есть хорошо функционирующий рынок с четкими и читаемыми ценовыми сигналами.

Но у нас его нет. Почти полностью этот нарратив построен на единственном индексе, и он намекает на то, на что не должен намекать: рынок аренды GPU стал настолько эффективным, что его глобальное состояние можно представить одним числом.

Дефицит предложения реален, но разные люди ощущают его совершенно по-разному — в зависимости от того, кто вы, где вы находитесь, с какими контрактами и какими вычислительными активами вы имеете дело. Столкнувшись с такой непрозрачностью, естественной реакцией рынка становится не упорядоченное ценовое обнаружение, а накопление: блокировка времени использования GPU, которое вам, возможно, еще не нужно, потому что вы не уверены, сможете ли вы купить его в следующем месяце по любой цене. Там, где есть накопление и нет прозрачного бенчмарка, появляется фрагментированный вторичный рынок. В Compute Desk мы уже способствовали тому, что арендаторы пересдают свои кластеры, как пересдают апартаменты во время крупных мероприятий. Это не предположение, это происходит прямо сейчас.

Индексы не сходятся

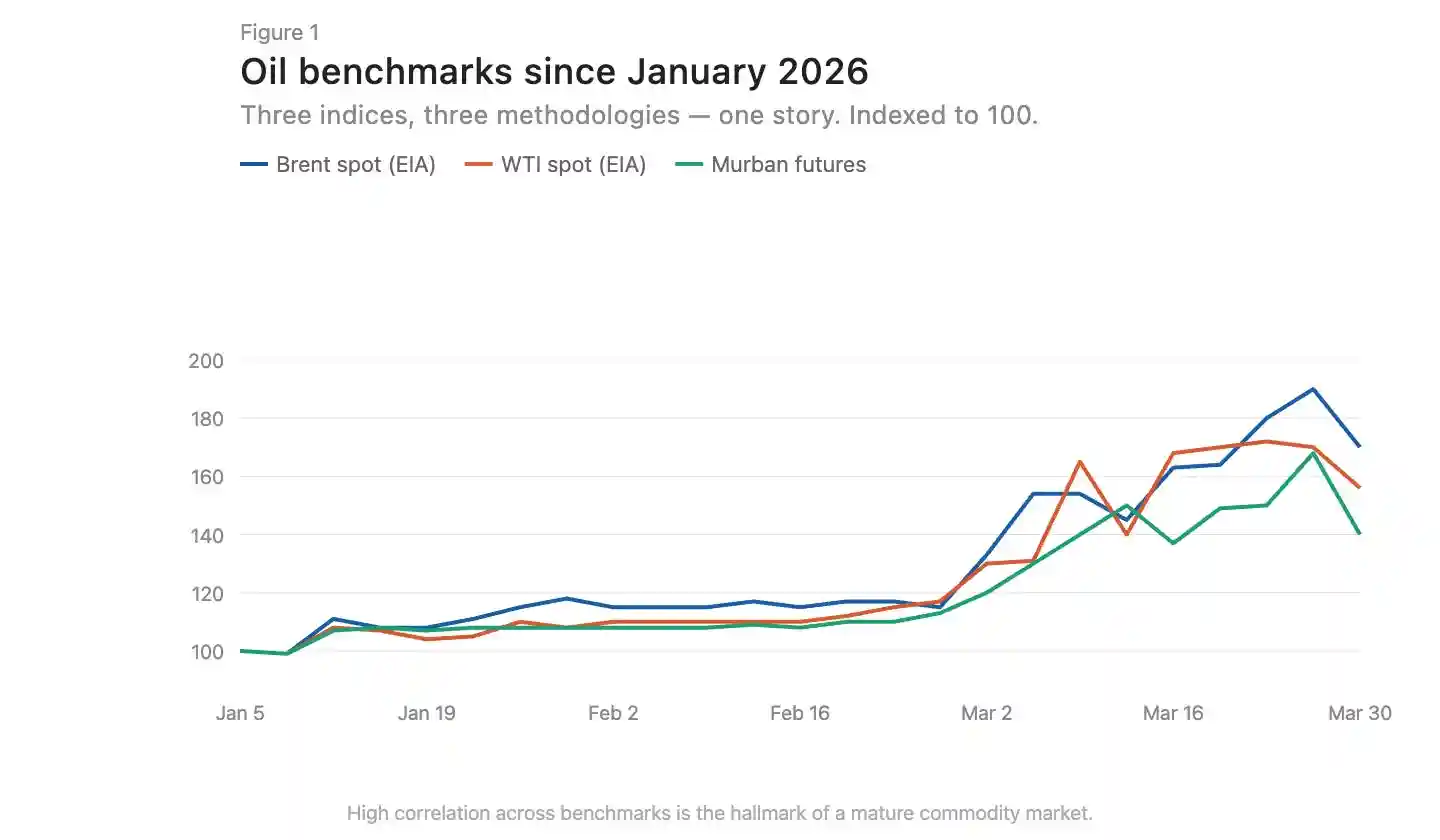

На зрелых товарных рынках индексы, построенные на основе различных методологий, стремятся к сближению. Цены на нефть Brent и WTI могут иметь разницу в несколько долларов из-за географического положения и качества нефти, но по направлению они движутся синхронно (Рис. 1). Такая конвергенция является признаком эффективного рынка.

Подпись к рисунку: Сравнение динамики цен на нефть Brent и WTI, высокая согласованность направления

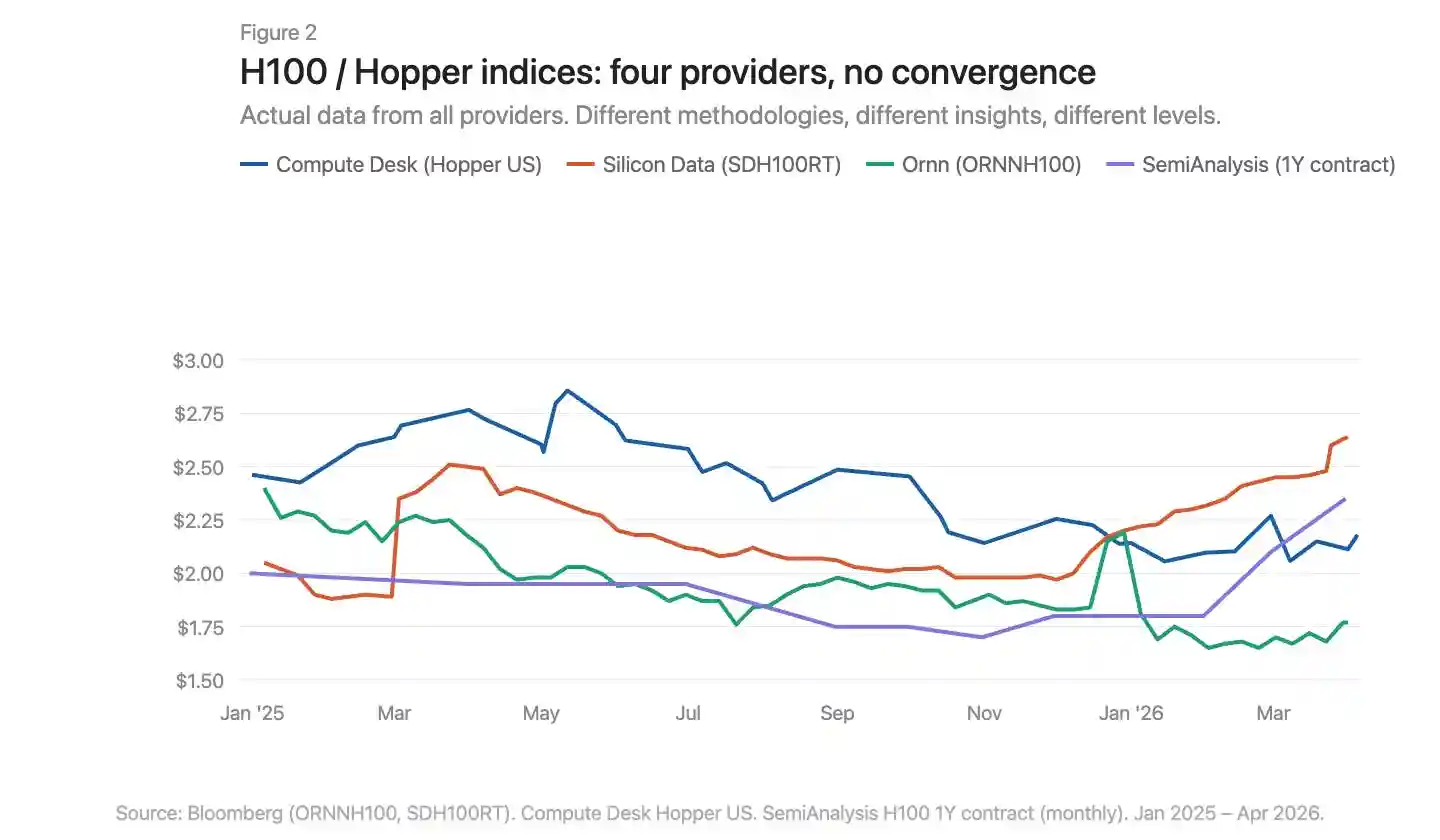

Сейчас на терминале Bloomberg представлены три провайдера индексов цен на GPU: Silicon Data, Ornn AI и Compute Desk. SemiAnalysis недавно опубликовал четвертый — ежемесячный индекс цен на годовые контракты H100, основанный на данных опроса более 100 участников рынка. Silicon Data и Ornn публикуют ежедневные индексы аренды H100, Compute Desk агрегирует данные на уровне архитектуры Hopper, а SemiAnalysis фиксирует договорные цены после переговоров, а не цены предложений или парсинга. Разные методологии, разная частота, разные углы зрения на один и тот же рынок. Если наложить их друг на друга, расхождения становятся очевидными (Рис. 2).

Подпись к рисунку: Наложение и сравнение четырех индексов GPU, явные расхождения в уровнях цен и тенденциях

Где именно происходит рост цен

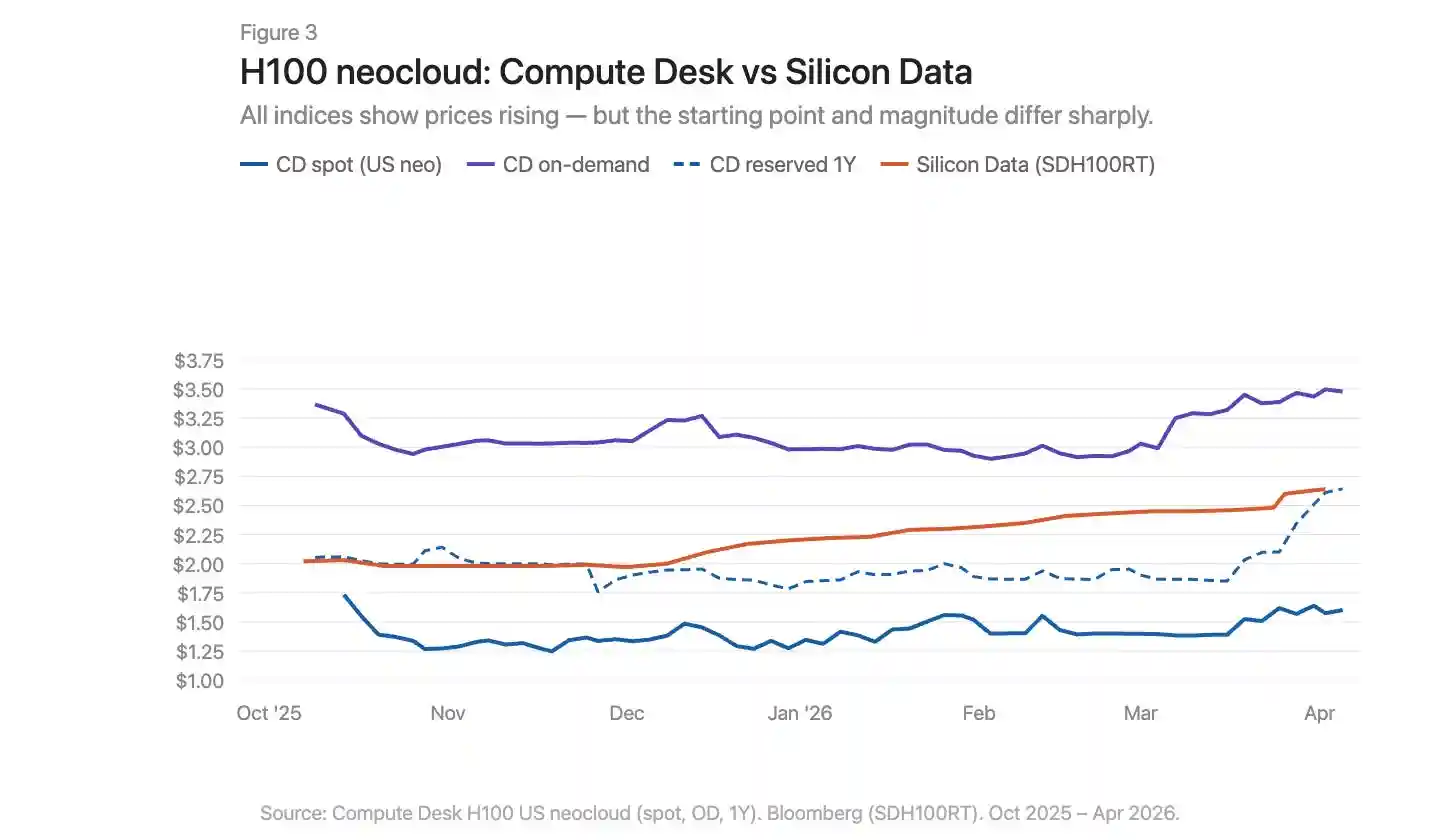

Используя данные Compute Desk, мы можем разбить изменение цен на H100 по типам поставщиков и структуре контрактов и наложить индекс SDH100RT от Silicon Data (Рис. 3). Все показатели показывают рост цен, но начальная точка и幅度 (размах) сильно различаются в зависимости от индекса и типа контракта.

Подпись к рисунку: Динамика цен H100 с разбивкой по типам контрактов в наложении с индексом SDH100RT

Данные Compute Desk по H100 «неооблаку» (neocloud) рассказывают более конкретную историю, чем агрегированный индекс. Ценообразование по требованию (on-demand) оставалось относительно стабильным в течение зимы, около 3.00 долларов в час, а затем в марте резко подскочило до 3.50 долларов. Спотовое ценообразование было более волатильным и более низким, и лишь в марте наметилась небольшая восходящая тенденция. Индекс SDH100RT от Silicon Data демонстрировал более плавный steady рост, поднявшись за тот же период с 2.00 долларов до 2.64 долларов. Два индекса постоянно находятся на разных ценовых уровнях и по-разному описывают временной ритм: Compute Desk говорит о скачке в марте, Silicon Data — о медленном ползучем росте.

Цены на годовые резервирования (reserved instances) до февраля оставались в основном flat, а затем в конце марта резко подскочили с 1.90 доллара до 2.64 доллара — не постепенное догоняющее движение, а внезапный пересмотр цен. Это больше похоже на то, что поставщики скорректировали тарифы по контрактам после ужесточения рынка по требованию, а не на устойчивый структурный спрос.

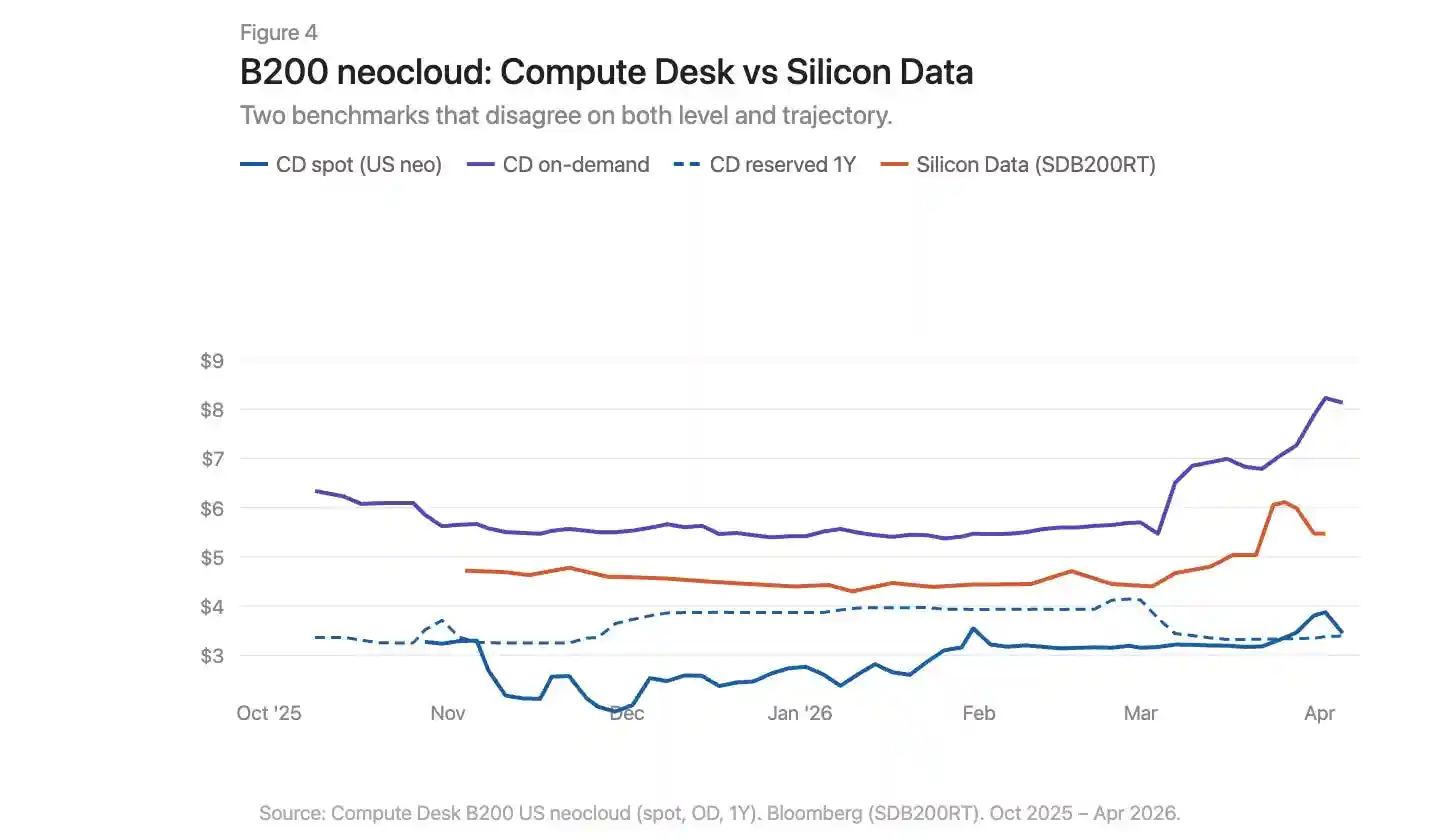

История B200 в марте еще более впечатляющая (Рис. 4). Он-лайн индекс Compute Desk за несколько недель взлетел с 5.70 долларов до более чем 8.00 долларов. Индекс SDB200RT от Silicon Data взлетел с 4.40 долларов до 6.11 долларов, а затем отступил до 5.47 долларов. Оба индекса зафиксировали этот всплеск, но их starting point отличался более чем на 2 доллара, а форма роста и отката также differed. У B200 меньше пяти месяцев данных, меньше поставщиков, больше спредов — два индекса смотрят на одно и то же событие через очень разные линзы.

Подпись к рисунку: Динамика цен B100 по требованию и с резервированием, наложение данных Compute Desk и Silicon Data

Проблема инфраструктуры, а не только региональные различия

На товарных рынках существует базисная разница (basis differential). Природный газ Аппалачей — это классический пример: огромные запасы сидят на структурно ограниченных пропускных способностях трубопроводов, уровень использования в коридоре Пенсильвания-Огайо часто превышает 100%, а новые проекты, такие как трубопровод Borealis, будут запущены только к концу 2020-х годов.

На рынке GPU наблюдается аналогичная ситуация: один H100 в Вирджинии и один H100 во Франкфурте — это не один и тот же экономический товар. Но только географическими различиями нельзя объяснить, почему индексы, измеряющие один и тот же рынок, так сильно расходятся. Перекос на рынке GPU глубже, чем на рынке газа Аппалачей. Проблема газа — единственное отсутствующее звено: пропускная способность трубопроводов, соединяющих спрос и предложение. Пробелы в инфраструктуре рынка вычислительных мощностей существуют как на стороне спроса, так и на стороне предложения. Физическая инфраструктура — согласованные сети, надежная доставка вычислительных мощностей, предсказуемые конфигурации, предсказуемая доступность — еще незрела, а иногда просто не работает. Финансовая инфраструктура — стандартизированные контракты, которые могут сжать спреды, несмотря на физические различия, прозрачные бенчмарки, механизмы арбитража — также еще не существует.

Данные рассказывают одну историю. Реальный опыт попыток закупить вычислительные мощности в начале 2026 года рассказывает более болезненную историю. Фактически вся он-лайн мощность всех типов GPU распродана. Найти даже 64 H100 сложно: Compute Desk показывает, что 90% поставщиков имеют нулевую доступность он-лайн кластеров, и рынок резервирования ненамного лучше. На хорошо функционирующем рынке такая степень дефицита уже давно подняла бы цены до новой точки равновесия. Но на самом деле этого не произошло. Это говорит о том, что сами поставщики также缺乏 (не имеют) оперативной информации о ценах для корректировки. Цены растут, но слишком медленно, чтобы очистить рынок. Разрыв между объявленными ценами и реальной готовностью платить заполняется накоплением, пересдачей и неформальными сделками на вторичном рынке.

Что нужно изменить

На текущем рынке вычислительных мощностей GPU существует семь核心 (ключевых) проблем:

Нет консенсусного бенчмарка. Существуют несколько индексов с разными методологиями, выводы которых противоречат друг другу.

Агрегированный нарратив скрывает структуру. Одно число «цена H100» скрывает огромные различия между разными типами поставщиков и сроками контрактов.

Нехватка данных на уровне сделок. На двусторонних рынках расхождение между объявленными ценами и фактическими ценами сделок очень велико.

Отсутствие стандартизации контрактов. Большинство аренд GPU являются двусторонними переговорами с различными условиями. Более короткие, более стандартизированные сроки контрактов могут улучшить ликвидность и ценовое обнаружение.

Нет гарантий качества предоставления услуг. Топологии interconnect, pairing CPU, сетевые стеки и время работы сильно различаются. Покупателям необходимо знать, какого качества вычислительные мощности они покупают, прежде чем брать на себя обязательства.

Контракты неликвидны. Если спрос изменится в течение периода резервирования, выбор ограничен: либо нести costs, либо неофициально пересдавать. Рынку нужна инфраструктура для передачи или перепродажи承诺 (зарезервированных) мощностей, чтобы capacity направлялась к тем, кто в ней больше всего нуждается.

Нет форвардной кривой. Нельзя определить цену на будущее, нельзя хеджировать. Именно поэтому кредиторы дают скидку 40-50% на залоговые GPU, а стоимость financing remains высокой.

Построение нормально функционирующего рынка для самого важного товара века не может продвигаться только по одному направлению. Измерение, стандартизация, структура контрактов, качество предоставления услуг, ликвидность — все это должно двигаться forward синхронно, и до тех пор никто не сможет с уверенностью сказать, сколько действительно стоит один час GPU.