Автор: Merkle3s Capital

Данная статья основана на ежегодном отчете Messari The Crypto Theses 2026, опубликованном в декабре 2025 года. Полный текст отчета превышает 100 000 слов, официальное время чтения составляет 401 минуту.

Этот контент подготовлен при поддержке Block Analytics Ltd X Merkle 3s Capital. Информация предоставляется исключительно в справочных целях, не является инвестиционным советом или предложением, мы не несем ответственности за ее точность и не принимаем на себя последствия, возникшие в результате ее использования.

«Интерпретация 100-тысячного ежегодного отчета Messari (Часть 1): Почему в 2025 году рыночные настроения полностью рухнули?»

Введение: Когда ETH начинает отставать, в чем на самом деле проблема?

За последний год то, что ETH отстает от BTC, стало практически неоспоримым фактом.

Будь то ценовые показатели, рыночные настроения или сила нарратива, BTC постоянно укрепляется как «единственный актив основной линии»:

ETF, институциональное распределение, макрозащита, хеджирование против доллара... Каждый нарратив концентрируется вокруг BTC.

В сравнении с этим положение ETH кажется несколько неловким.

Он по-прежнему остается самой важной базовой сетью для DeFi, стейблкоинов, RWA и ончейн-финансов, но продолжает отставать по показателям актива.

Это порождает вопрос, который многократно обсуждался, но так и не был认真 разобран:

ETH отстает от BTC потому, что его маргинализируют, или потому, что рынок использует ошибочный способ его оценки?

Ответ, данный Messari в их новом 100-тысячном ежегодном отчете, не угождает эмоциям и не встает на сторону какой-либо цепи.

Их больше волнует: куда на самом деле поступают средства, какие вещи институции realmente размещают в блокчейне.

И с этой точки зрения «проблема» ETH, возможно, отличается от той, которую представляет себе большинство.

Эта статья не будет обсуждать веру или сравнивать TPS, Gas или технические路线. Мы сделаем лишь одно:

Следуя данным Messari, мы разберем ситуацию с отставанием ETH от BTC.

Глава 1: Само по себе отставание ETH от BTC не является аномалией

Если смотреть только на ценовые показатели 2024–2025 годов, отставание ETH от BTC заставляет многих делать интуитивный вывод:

Неужели с ETH что-то не так?

Но с исторической и структурной точек зрения, отставание ETH от BTC само по себе не является «аномальным явлением».

BTC — это актив с высоко единой叙事.

Его логика ценообразования ясна, консенсус集中, переменных крайне мало.

Когда рынок вступает в фазу макронеопределенности, регуляторных изменений, переоценки институциями рисковых активов, BTC往往 первым получает премию.

С ETH все completely наоборот.

ETH одновременно выполняет три роли:

-

Децентрализованный settlement слой

-

Инфраструктура для DeFi и стейблкоинов

-

«Производственная сеть» с путем технических обновлений и исполнительными рисками

Это означает, что цена ETH отражает не только «макроконсенсус», но и вынуждена поглощать множество переменных, таких как технический ритм, изменения экосистемы, структура захвата стоимости и другие.

Messari в отчете четко указывает:

Проблема ETH не в «исчезновении спроса», а в том, что «логика ценообразования усложнилась».

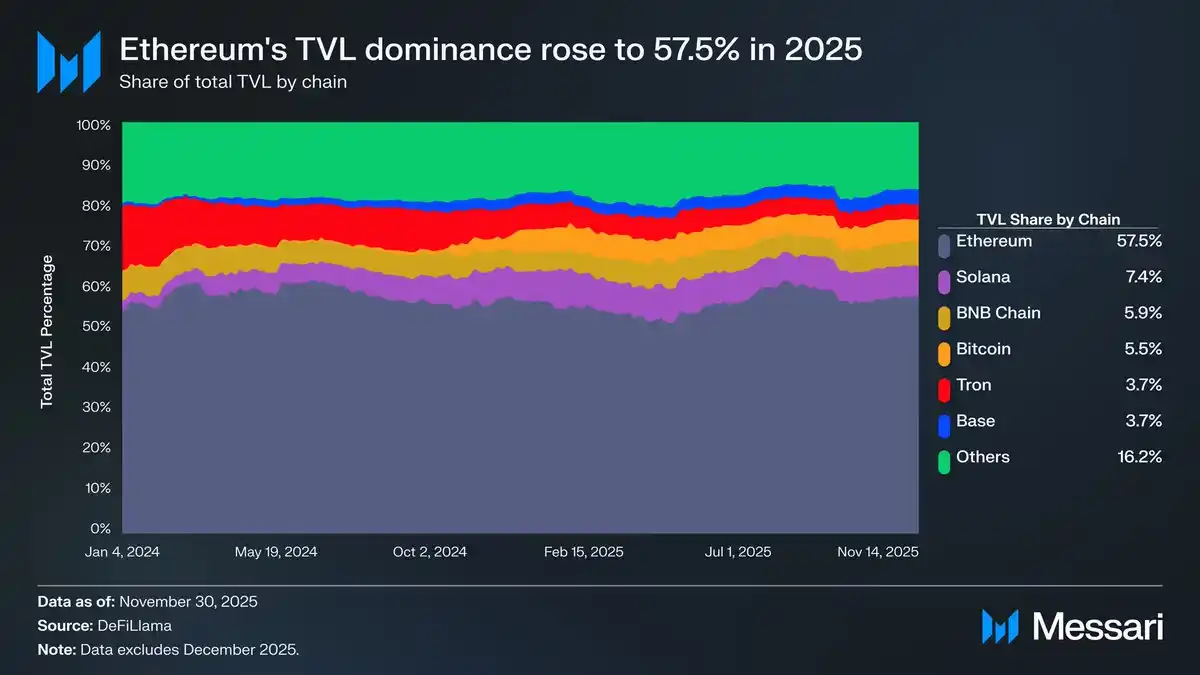

В 2025 году ETH по-прежнему занимал доминирующее положение по ключевым показателям: ончейн-активность, расчеты стейблкоинов, размещение RWA.

Но этот рост, в отличие от ETF BTC или макронарратива, не превращается немедленно в премию актива.

Другими словами, отставание ETH от BTC не означает, что рынок отвергает Ethereum.

Более вероятно, что рынок暂时 не знает, как его оценивать.

Настоящая причина для警惕 заключается не в самом факте отставания,

а в том: когда ETH активно используется, может ли это использование по-прежнему持续反馈 на актив ETH.

Это то, что realmente волнует Messari.

Глава 2: Использование растет, а стоимость нет? Дилемма захвата стоимости ETH

То, что realmente заставило рынок усомниться в ETH, — это не отставание в цене от BTC,

а более режущий глаз факт: Ethereum активно используется, но сам ETH от этого не выигрывает синхронно.

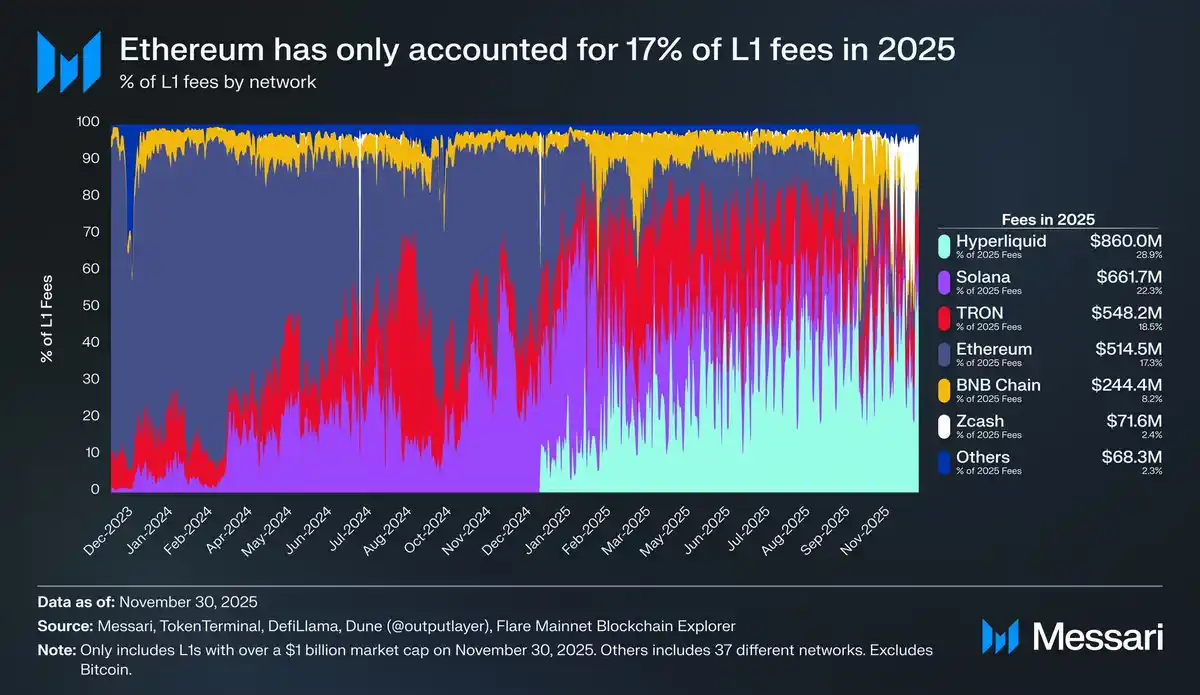

Messari в отчете приводит一组 ключевых данных:

С появлением конкурирующих L1, доля Ethereum в комиссиях L1 продолжает снижаться.

-

Solana в 2024 году вновь укрепила свои позиции как высокопроизводительный исполнительный слой,

-

Hyperliquid в 2025 году быстро набрал объемы в виде ончейн-деривативов,

-

Вместе они оказывают давление на долю Ethereum в измерении «непосредственной монетизации экономической активности».

К 2025 году доля комиссий L1 Ethereum упала примерно до 17%,

опустившись на четвертое место среди L1.

Всего год назад он прочно занимал первое место.

Комиссии — не единственный показатель ценности сети, но они являются极其 честным сигналом:

Где взимаются комиссии, там и происходят реальные交易行为 и проявляются риск appetite.

Именно здесь начинает проявляться核心矛盾 ETH.

Ethereum не потерял пользователей. Напротив, его позиции в таких областях, как стейблкоины, RWA, институциональные расчеты, стали еще более прочными. Проблема в том, что все больше этих активностей происходит на L2 или уровне приложений, а не напрямую отражается в доходах L1 от комиссий.

Другими словами: Ethereum как система становится все важнее, а ETH как актив все больше похож на «разбавленные права».

Это не технический провал, а неизбежный результат архитектурного выбора.

Путь масштабирования через Rollup успешно снизил стоимость транзакций, повысил пропускную способность, но также объективно ослабил способность ETH напрямую捕获 стоимость использования.

Когда использование «аутсорсится» на L2, доход ETH все больше зависит от абстрактной премии за безопасность и денежных ожиданий, а не от денежного потока.

Вот почему рынок начал колебаться при оценке ETH:

Является ли он активом, который будет приносить сложный процент по мере роста использования, или все более нейтральным settlement слоем, похожим на «общественную инфраструктуру»?

Этот вопрос стал еще более актуальным после обострения многоконкурентности.

Глава 3: Мультичейн — не угроза, настоящее давление исходит от «замены исполнительного слоя»

Если смотреть только на уровень叙事, у ETH, кажется, становится все больше对手.

Solana, различные высокопроизводительные L1, аппчейны, даже специализированные торговые цепи появляются одна за другой,

что легко приводит к выводу: ETH маргинализируется «многоконом миром».

Но оценка, данная Messari, более冷静 и более жестока.

Сам по себе мультичейн не является угрозой для ETH.

Реальное давление создает持续замена исполнительного слоя, в то время как стоимость settlement слоя难以直接 оцениваться рынком.

Возьмем пример Solana:

-

Solana в 2024–2025 годах вернула себе主场高频交易 и активность розничных инвесторов,

-

Она явно лидирует по объемам спот-торговли, ончейн-активности, опыту с низкой задержкой.

Но этот рост больше отражает «опыт交易» и «плотность трафика», а не расчеты стейблкоинов, хранение RWA или институциональные расчеты.

Messari в отчете反复подчеркивает факт:

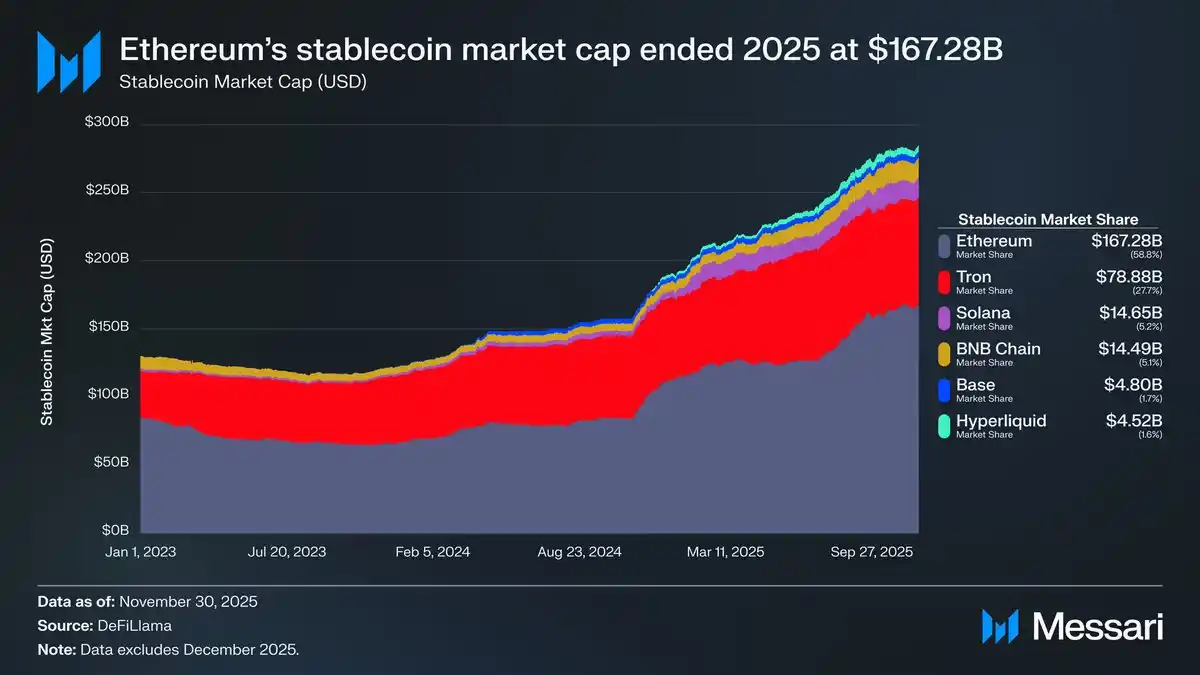

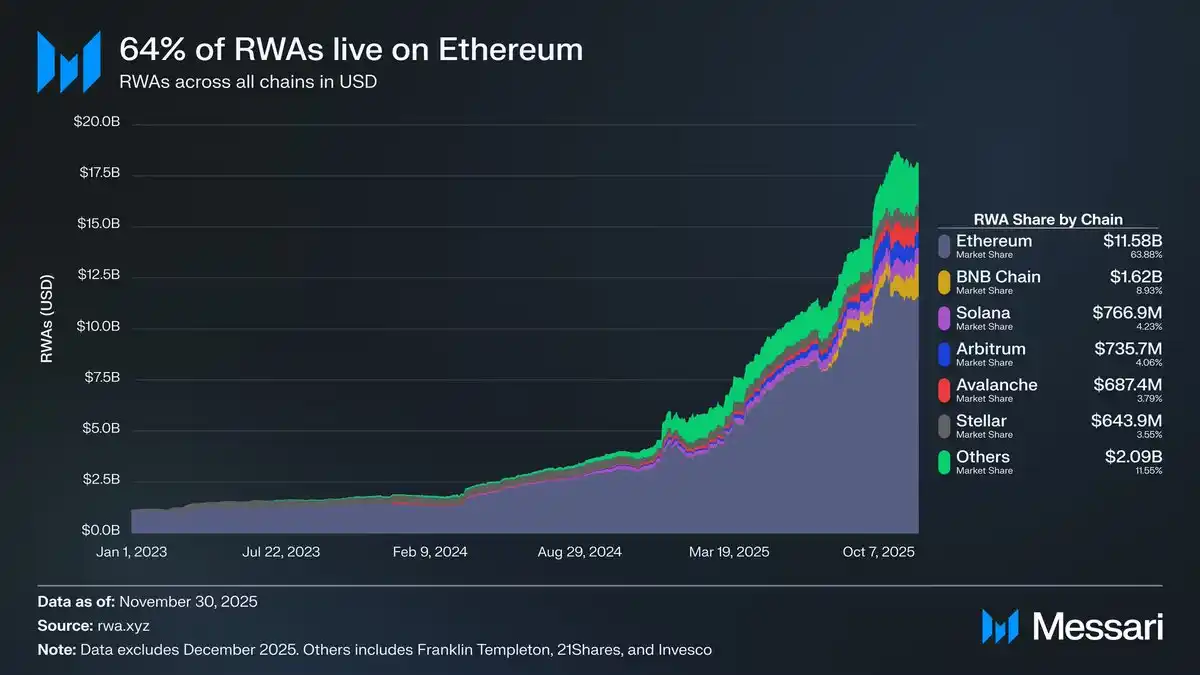

Когда институции realmente размещают деньги в блокчейне, они по-прежнему выбирают Ethereum.

Выпуск стейблкоинов, Tokenized T-bills, ончейн-доли фондов, пути compliant хранения — эта самая «скучная», но критически важная финансовая инфраструктура — по-прежнему高度сконцентрирована в экосистеме Ethereum.

Это также объясняет кажущееся противоречие: цена актива ETH испытывает давление, но Ethereum в измерении «блокчейн, который институции готовы использовать», напротив, еще больше укрепил лидирующие позиции.

Проблема в том, что рынок не будет платить премию просто за «важность».

Когда доход исполнительного слоя уходит другим цепям, а стоимость settlement слоя больше отражается в «безопасности» и «соответствии/надежности», логика ценообразования ETH неизбежно становится абстрактной.

Другими словами:

ETH сталкивается не с «заменой», а с вынужденным принятием роли, более похожей на общественную инфраструктуру.

А инфраструктура, как правило, чем выше利用率, тем сложнее рассказывать истории о премии актива.

Именно здесь фундаментальное различие между ETH и BTC начинает彻底分化.

Глава 4: ETH по-прежнему离不开 «макроякоря» BTC

Если предыдущие три главы отвечали на вопрос — был ли ETH маргинализирован?

То эта глава сталкивается с более жестокой и более реальной оценкой:

Даже если ETH не заменят, на уровне ценообразования активов он по-прежнему глубоко зависит от BTC.

Messari в отчете反复подчеркивает факт, который многие упускают из виду:

Рынок оценивает не «блокчейн-сети», а то, что можно абстрагировать как макроактив.

В этом点различие между BTC и ETH极其清晰.

Нарратив BTC был彻底упрощен до трех вещей:

-

Актив для макрхеджирования

-

Цифровое золото

-

«Денежный актив», приемлемый для институций, ETF, национальных балансов

А нарратив ETH гораздо сложнее.

Он является и settlement слоем, и технической платформой, и承载финансовую активность, и постоянно проходит обновления и структурные调整.

Это мешает ETH, как BTC, быть直接 включенным в «макрокорзину активов».

Эта разница особенно заметна в потоках средств ETF.

В начале 2024 года, когда только запустился спотовый ETF на ETH, рынок一度 считал: у институций практически нет интереса к ETH.

Первые шесть месяцев приток средств в ETF на ETH был заметно слабее, чем в BTC, что укрепило нарратив «BTC — единственный институциональный актив».

Но Messari указывает, что этот вывод сам по себе вводит в заблуждение.

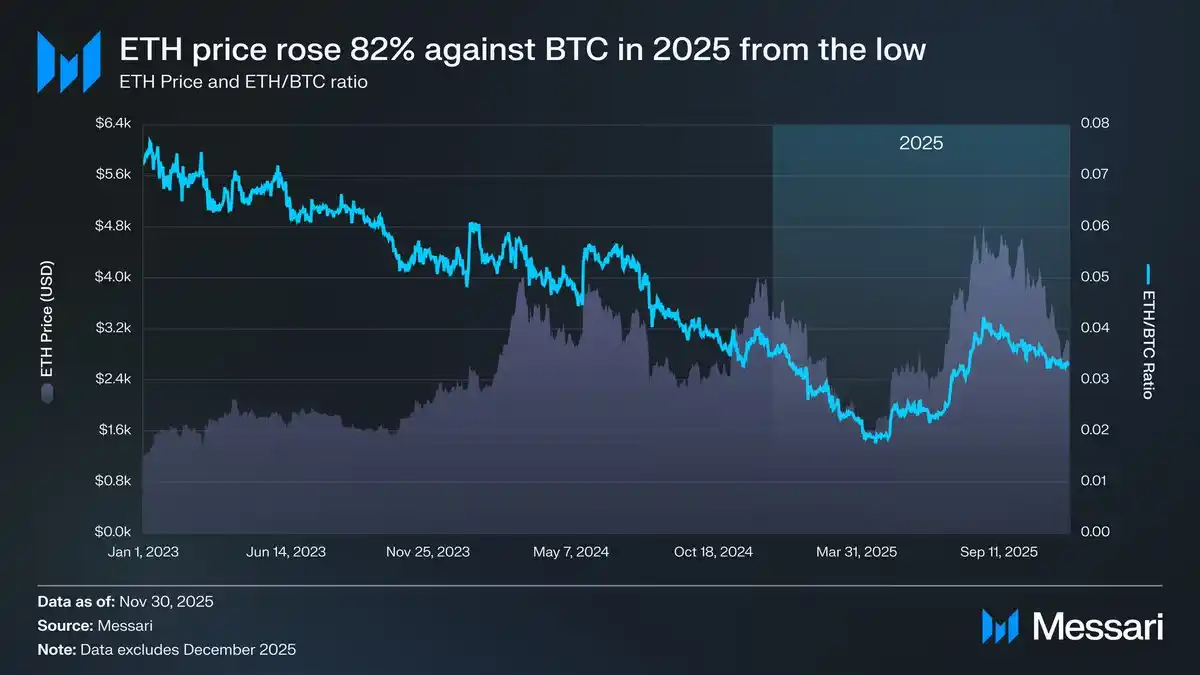

С синхронным отскоком цены ETH и соотношения ETH/BTC в середине 2025 года, поведение средств начало меняться.

-

ETH/BTC отскочил с минимума 0.017 до 0.042, рост более чем на 100%

-

Цена ETH в долларах за тот же阶段выросла почти на 200%

-

Приток средств в ETF на ETH начал显著ускоряться

В некоторые периоды времени новый приток в ETF на ETH даже временно превышал BTC.

Это говорит об одном:

Институции не не хотят покупать ETH, а ждут «叙事определенности».

Но даже так, Messari все равно дает冷静вывод:

Денежная премия ETH至今остается «вторичным производным» денежного консенсуса BTC.

Другими словами, причина, по которой рынок готов в某个阶段вновь обратиться к ETH, не в том, что ETH стал независимым макроактивом, а в том, что макронарратив BTC по-прежнему действует и перетекает на внешнюю кривую риска.

Пока BTC остается якорем ценообразования всего крипторынка, сила ETH неизбежно будет измеряться в его тени.

Это не означает, что у ETH нет пространства для роста. Как раз наоборот, при условии成立тренда BTC, ETH часто обладает более высокой弹性 и более сильной Beta.

Но это также означает:

Нарратив актива ETH еще не завершил «де-BTC-зацию».

Пока ETH не сможет на более длительных циклахпродемонстрировать более низкую корреляцию с BTC, более стабильные независимые источники спроса и более четкий путь захвата стоимости,

он будет по-прежнему рассматриваться рынком как:

Актив信念 второго уровня, построенный поверх BTC.

Глава 5: Будет ли ETH под угрозой? Настоящая проблема никогда не в победе или поражении

Обсуждая до этого момента, мы уже можем ответить на反复задаваемый вопрос:

Будет ли ETH «заменен» другими цепями?

Ответ Messari очень ясен:

Нет.

По крайней мере, в обозримом будущем, Ethereum по-прежнему остается базой по умолчанию для ончейн-финансов, стейблкоинов, RWA и институциональных расчетов.

Это не самая быстрая цепь, но это цепь, которой最先разрешают承载реальные деньги.

Настоящее беспокойство должно вызывать не «проиграет ли ETH Solana, Hyperliquid или следующей новой цепи»,

а другой, более неудобный вопрос:

Может ли актив ETH по-прежнему持续извлекать выгоду из успеха Ethereum?

Это структурная проблема, а не техническая.

Ethereum становится все больше похож на «общественную финансовую инфраструктуру»:

-

Объем использования растет

-

Системная важность повышается

-

Институциональная зависимость углубляется

Но в то же время, захват стоимости ETH все больше зависит от:

-

Денежной премии

-

Премии за безопасность

-

Перетока макро risk appetite

А не от прямого денежного потока или роста комиссий.

Вот почему表现актива ETH все больше напоминает «актив с высокой Beta, производный от BTC», а не сетевые права с независимой системой ценообразования.

В многоконом мире исполнительный слой можно конкурировать, трафик можно分流, но settlement слой не будет часто мигрировать.

Ethereum как раз находится на этой самой стабильной и最难вознаграждаемой рыночными настроениями позиции.

Поэтому, отставание ETH от BTC не означает失败.

Это больше похоже на результат разделения ролей:

-

BTC承担макронарратив, денежный консенсус и якорение активов

-

ETH承担расчеты, финансовую инфраструктуру и системную безопасность

Проблема лишь в том, что рынок更愿意платить премию за первое и сохранять сдержанность по отношению ко второму.

Вывод Messari не радикален, но足够честен:

Денежная история ETH修复лена, но еще не завершена. Он может сильно расти при成立тренда BTC, но еще не доказал, что может оцениваться независимо в отрыве от BTC.

Это не отрицание ETH, а своего рода阶段性的позиционирование.

В эпоху, когда BTC остается единственным макроякорем крипторынка,

ETH больше похож на финансовую операционную систему, построенную поверх этого якоря.

Он важен, он незаменим, но он暂时еще не тот «актив, который оценивают первым».

По крайней мере, сейчас еще нет.