Источник:arise

Компиляция|Odaily Planet Daily(@OdailyChina); Переводчик|Azuma(@azuma_eth)

Ключевое содержание этой статьи только одно — как подготовиться к потенциально крупнейшему дропу в нише рынков предсказаний.

Необходимо заявить о проблеме данных

Перед построением каждой модели нам нужны достоверные и надежные данные. Данные об объеме торгов Polymarket широко искажаются.

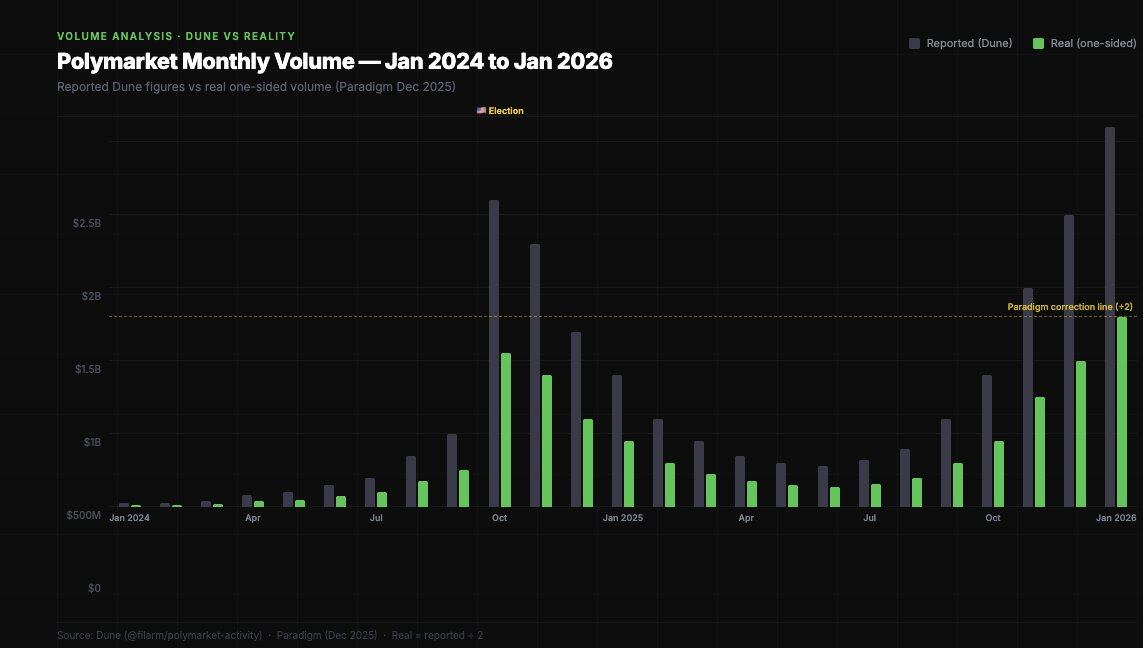

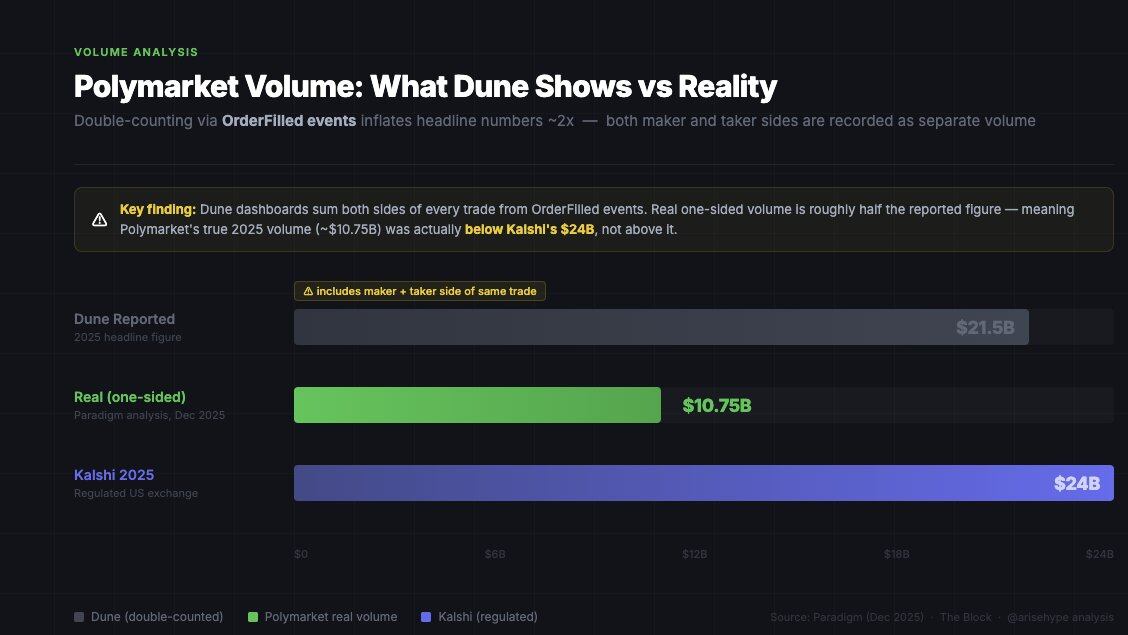

В декабре 2025 года Paradigm опубликовал исследование с ключевым выводом: большинство дашбордов Polymarket рассчитывают объем торгов путем суммирования всех событий «OrderFilled», но это событие срабатывает как со стороны размещения ордера (мейкера), так и со стороны его исполнения (тейкера) в одной сделке, что приводит к двойному счету. Реальный объем торгов составляет примерно половину от цифр на дашбордах.

Объем на дашборде vs односторонний объем — последний является действительно важной цифрой для моделирования дропа.

Это крайне важно для моделирования дропа. Если Polymarket будет рассматривать объем торгов как метрику, они будут использовать внутренние данные, а не различные статистики на Dune. Ваш фактический «счет» объема торгов, скорее всего, будет вдвое меньше, чем показывают такие инструменты, как Polycool.

Распределение пользователей

Что касается предположений о дропе, самый важный набор данных поступает из исследования IMDEA Networks Institute, которое охватило более 86 миллионов транзакций (апрель 2024 г. – апрель 2025 г.).

- Только 0.51% адресов получили прибыль свыше 1000 долларов;

- Только 1.74% адресов (оценочно) имели объем торгов свыше 50000 долларов;

- Топ-3 арбитражных адреса самостоятельно извлекли 4.2 миллиона долларов «безрисковой прибыли»;

- Лучшие трейдеры могли заработать десятки миллионов долларов.

В вознаграждениях LP (поставщиков ликвидности) стратификация еще более выражена.

79% трейдеров никогда не получали даже 1 доллара вознаграждения LP — это на данный момент самое игнорируемое взаимодействие. Среди 314 000 трейдеров только 66 567 кошельков когда-либо получали вознаграждение LP. Это означает, что только 21% трейдеров когда-либо предоставляли ликвидность. По сравнению с общим уровнем участия, этот механизм вознаграждения явно недооценен.

Более низкий уровень использования обычно рассматривается в моделях дропа как сигнал «недооцененности».

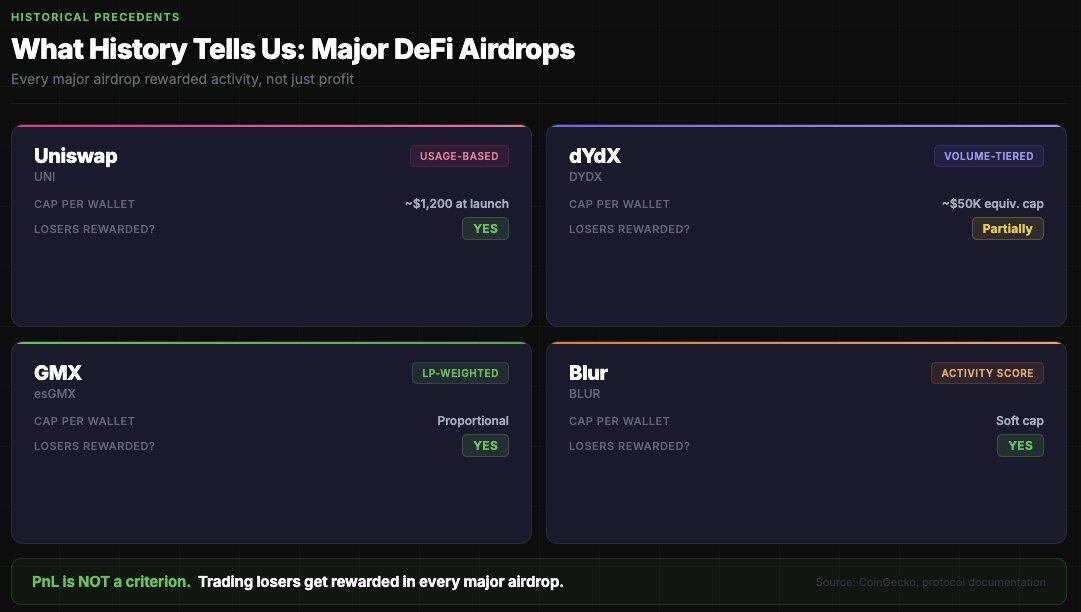

Прецеденты дропов: Что нам говорит история?

Все крупные DeFi-дропы вознаграждают «активное поведение», а не «прибыльность». Polymarket, вероятно, последует той же логике.

Общие черты всех крупных дропов включают:

- Чистое равное распределение будет злоупотреблено сибил-атаками (Polymarket точно не будет делить поровну);

- Чистое распределение по объему торгов приведет к чрезмерной концентрации дропа у китов (риски для PR + риски SEC);

- Лучшая стратегия: стратификация по уровням + лимиты на вознаграждения + множественные измерения (объем торгов + LP + разнообразие + длительность активности);

- Во всех основных дропах убыточные участники также получают вознаграждение — прибыль/убыток (PnL) не является критерием.

Последний пункт очень важен: если вы провели сделок на 100 000 долларов и потеряли 20 000, у вас больше шансов получить вознаграждение, чем у того, кто провел сделок на 1000 долларов и заработал 500. Платформа не хочет поощрять только прибыльные сделки — так легче отсеять инсайдеров.

Обратное мышление: Как ограничить китов?

Некоторые калькуляторы дропов на рынке используют простейшую модель пропорции объема: доля дропа = личный объем / общий объем × размер дропа.

Это ошибочно, поскольку основные дропы всегда используют «нисходящую кривую».

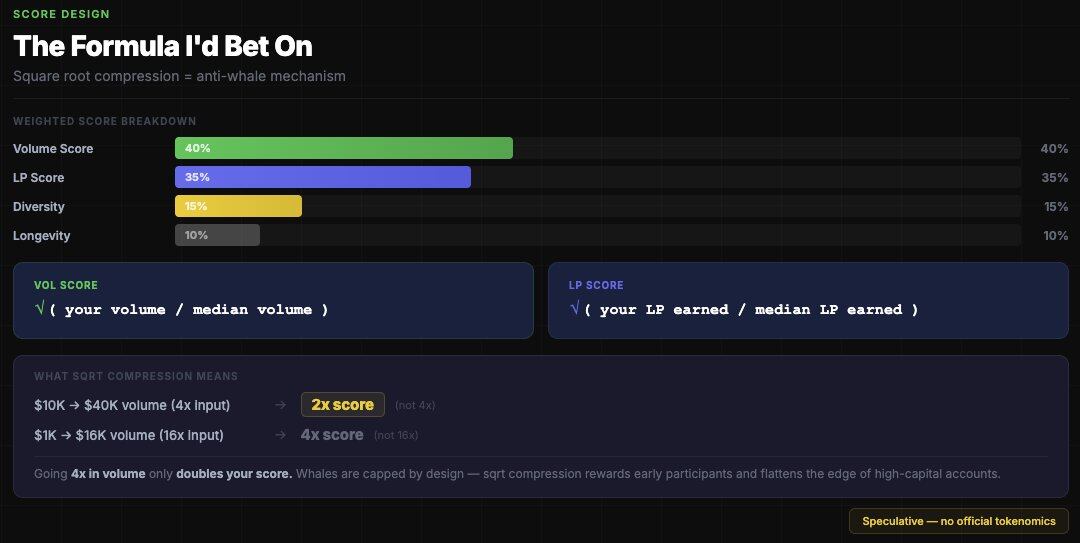

Модель, на которую я бы скорее поставил, заключается в том, что Polymarket использует сжатие по квадратному корню для ограничения размера дропа для китов — например, при увеличении объема в 4 раза, счет увеличивается только в 2 раза, что кардинально изменит результат дропа для китоподобных групп.

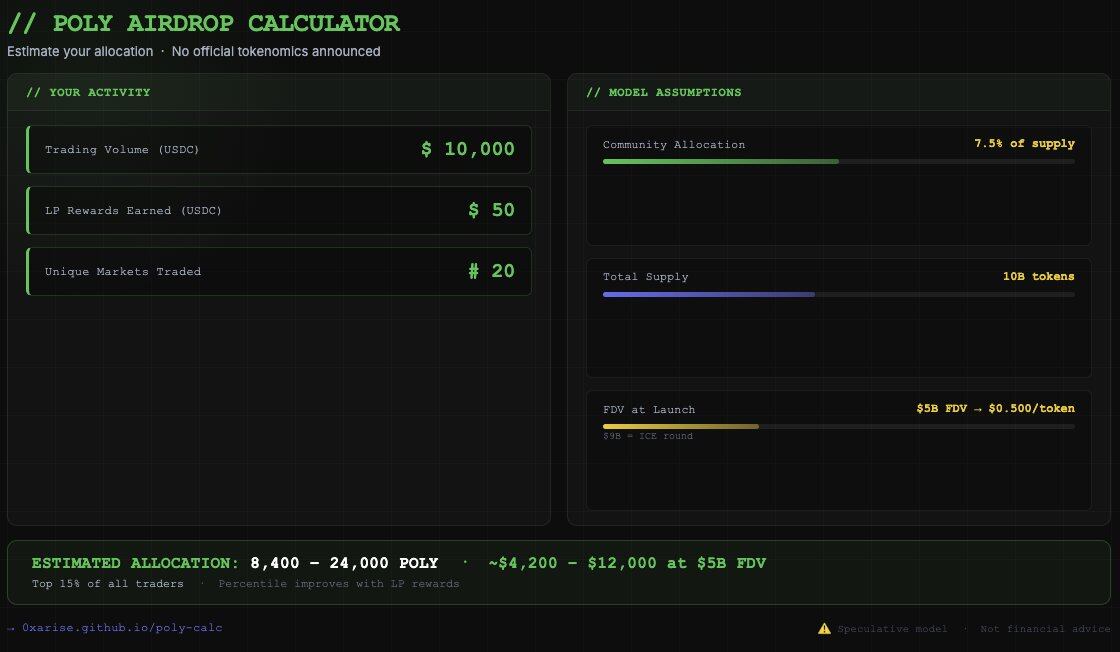

Сколько же получат топовые кошельки? Предположим, общее предложение POLY составляет 10 миллиардов токенов, из которых 7.5% предназначены для комьюнити-дропа (750 миллионов POLY), а FDV на момент TGE составляет 30–90 миллиардов долларов.

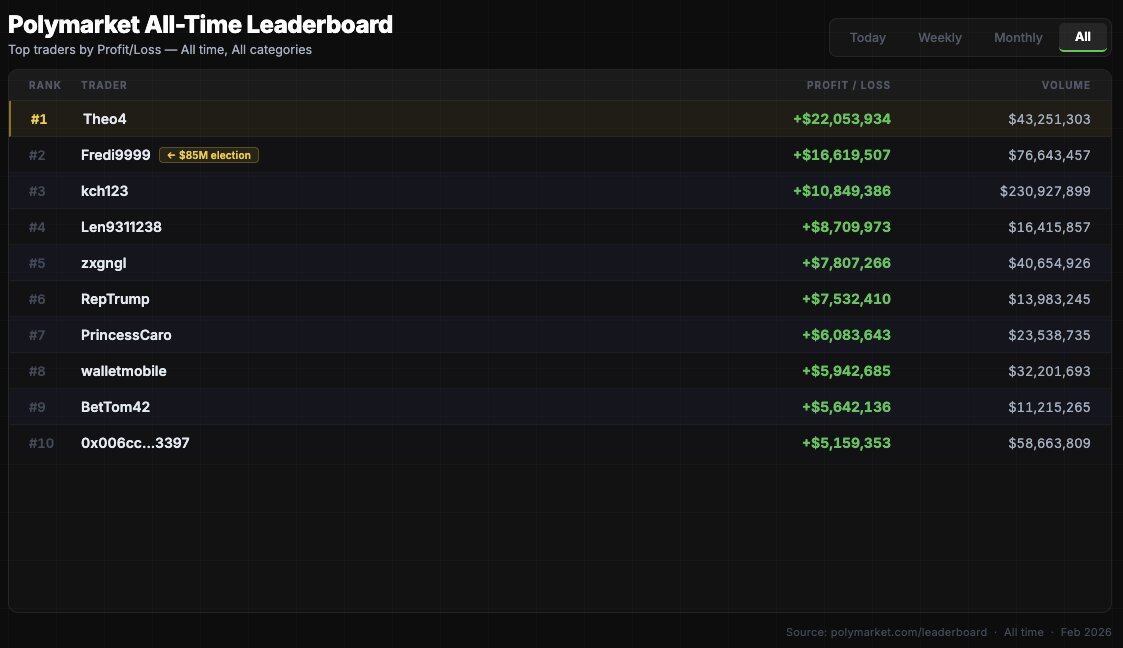

Без ограничения на сумму дропа для одного адреса, при объеме торгов в 85 миллионов долларов (на примере топового трейдера fredi999), модель прогнозирует получение около 300–500 миллионов POLY. При FDV в 90 миллиардов долларов это эквивалентно 300–450 миллионам долларов. Теоретически это возможно, но это крайне негативно для PR.

Более реалистичный сценарий — установление лимита на сумму дропа для одного адреса, например,上限 может составлять 50–200 миллионов POLY. При FDV в 50 миллиардов долларов топовый адрес может получить около 45–100 миллионов долларов.

«LP» и «Объем торгов»: Где сегодняшние возможности?

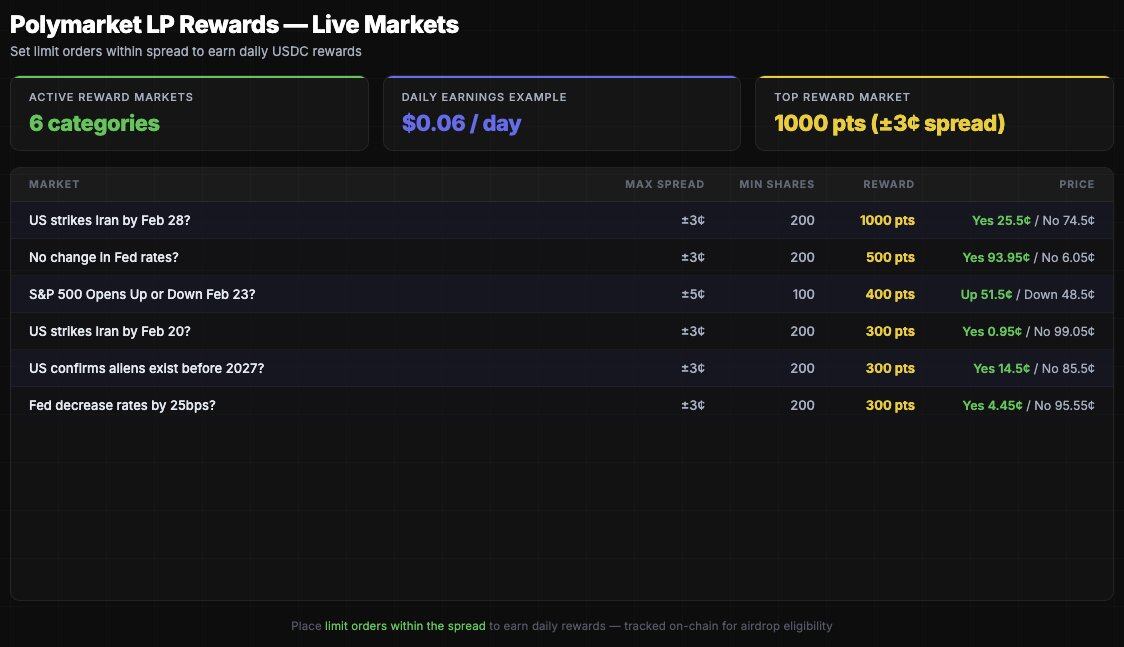

Если начать взаимодействие с Polymarket в феврале 2026 года с капиталом в 5000 долларов, математически для новых участников более выгодным вариантом будет размещение LP.

- Чтобы заработать 49 долларов вознаграждения LP (топ-10%), вам нужно постоянно выставлять лимитные ордера на рынках с высоким вознаграждением. При использовании средств в размере 500–1000 долларов этого можно достичь за 30–60 дней.

- Чтобы заработать 1563 доллара вознаграждения LP (топ-1%), потребуется более высокий капитал или постоянное высокочастотное участие.

Что касается объема торгов, вам нужно накапливать реальный объем, не накручивая его:

- Торгуйте на 5 и более различных рынках (политика, крипто, спорт, наука, культура);

- Держите позиции открытыми как минимум 1–24 часа перед закрытием;

- Не совершайте встречные сделки на одном рынке с разных адресов;

- Терпите умеренные убытки — это доказательство «реального участия»;

- Целевой объем рынка > 500 000 долларов (Polymarket может фильтровать микрорынки);

- Размер одной ставки: 50–500 долларов.

Предположения модели дропа

Дроп будет не таким, как ожидает большинство.

Большинство предположений о дропе основаны на простейшем взвешенном по объему распределении, но Polymarket подойдет к этому умнее и интереснее. У них есть данные по LP в链上, они чистые, проверяемые и все в долларовом выражении. У них также есть данные об объеме торгов, которые можно отфильтровать от сибил-атак. У них также есть данные о возрасте кошелька, разнообразии рынков и географическом распределении.

Вот моя модель — Polymarket еще ничего не подтвердил, так что это всего лишь мое предположение.

- Вес объема торгов: 40%: будет использоваться формула сжатия по квадратному корню, минимальный порог около 500 долларов;

- Вес вознаграждений LP: 35%: проверяемо в链е, устойчиво к сибил-атакам;

- Вес разнообразия рынков: 15%: количество уникальных рынков, на которых участвовали;

- Вес длительности активности: 10%: количество месяцев активности до снепшота.

Кроме того, Polymarket установит лимит на вознаграждение для одного адреса (возможно, 50 000 долларов), иначе топ-50 адресов получат слишком большую долю, разрушив нарратив сообщества. Убыточные участники получат такое же вознаграждение, как и прибыльные при同等 объеме торгов, прибыльность не является критерием — это философски неоправданно и создает искаженные стимулы.

79% трейдеров никогда не получали 1 доллар вознаграждения LP. Если вес LP в формуле дропа составляет 35%, то в настоящее время наиболее капиталоэффективным поведением является выставление лимитных ордеров на рынках с высоким объемом торгов и начало накопления проверяемого в链е доказательства вклада.

Короче говоря, POLY может стать крупнейшим дропом в истории рынков предсказаний. При расчетном FDV в 90 миллиардов долларов общая стоимость комьюнити-дропа может составить 450–900 миллионов долларов. Даже если захватить всего 0.1% от этого, это 450 000 долларов. Вот почему сейчас важно抓紧 оптимизировать данные LP, и это важнее, чем осознает большинство.