Оригинал | Odaily Planet Daily(@OdailyChina)

Автор | Azuma(@azuma_eth)

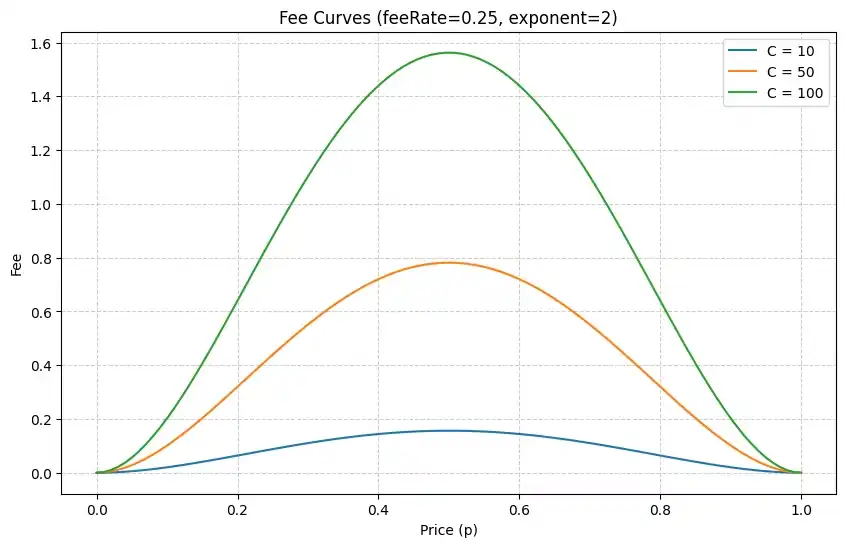

6 января этого года Polymarket официально начал взимать торговые комиссии за рынки, связанные с "15-минутными колебаниями криптовалют". Конкретный размер комиссии изменяется в реальном времени в зависимости от коэффициентов рынка — чем ближе коэффициент к 0% или 100%, тем ниже комиссия; наоборот, чем ближе коэффициент к 50%, тем выше комиссия, достигая максимум 1.56%.

Это первый раз, когда Polymarket, за исключением американского рынка (где взимается комиссия 0.01%), прекратил полностью бесплатный режим и начал взимать торговые комиссии за конкретный тип рынков. Прошло уже три недели, и накопилось достаточно данных для наблюдения, пришло время сделать приблизительную оценку доходности Polymarket.

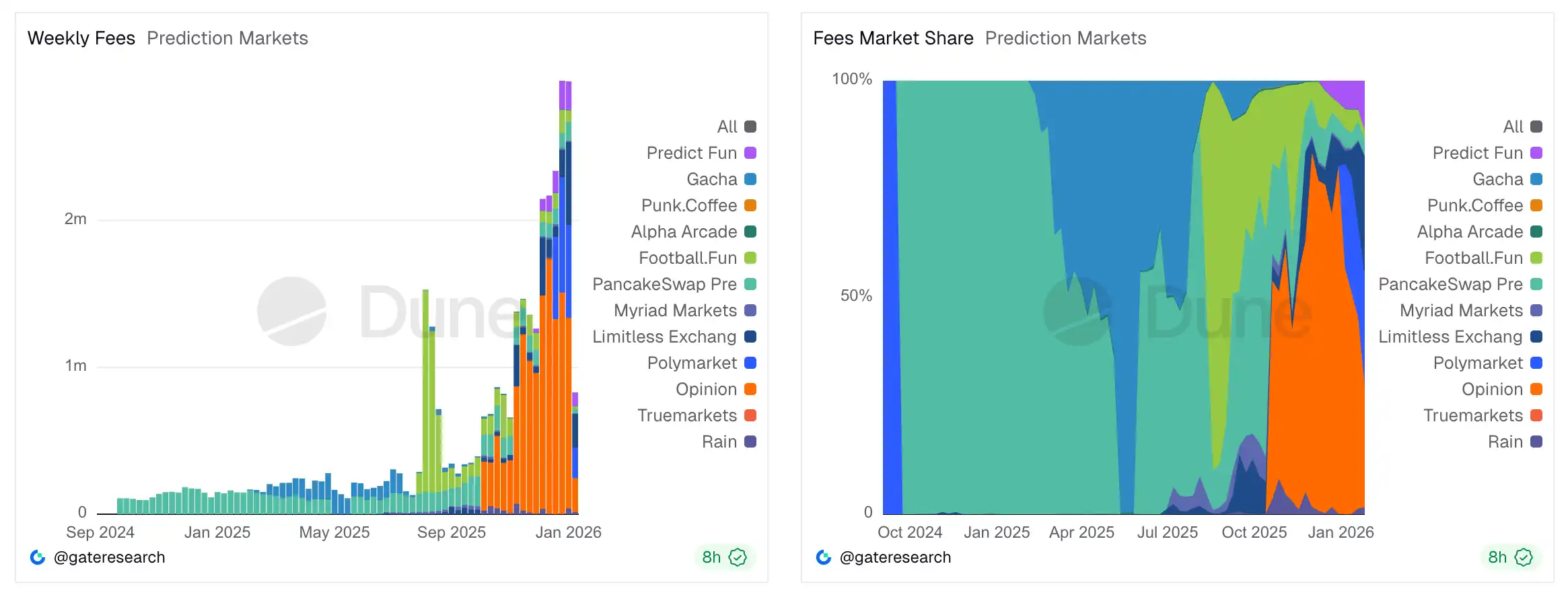

Сначала рассмотрим масштаб доходов от комиссий. Согласно данным, составленным Gate Research на Duna, с момента введения комиссий Polymarket накопил около 2.19 миллиона долларов дохода от комиссий, в среднем около 730 тысяч долларов в неделю — экстраполируя эти данные статически, при условии неизменности объема торгов и структуры торговой активности на соответствующих рынках, ожидается, что это принесет Polymarket около 38 миллионов долларов дохода в год.

Можно предположить, что Polymarket не ограничит сферу взимания комиссий только категорией "15-минутные колебания криптовалют". После официального введения комиссий для этой категории рынков Polymarket долгое время сохранял полностью бесплатный режим, одновременно самостоятельно subsidizing ликвидность рынка. В конце прошлого года сам Коплан признал, что Polymarket работает в убыток... Но мы уже видели слишком много подобных историй "сжигания денег" на интернет-рынках. По мере того как пользовательские привычки и рыночная позиция Polymarket постепенно укрепляются, в будущем не исключено введение комиссий на更多的 рынков.

- Прим. Odaily: По вопросу доходов Polymarket см. предыдущий выпуск чайной беседы редакции Odaily «Чайная беседа редакции Odaily (7 января)».

Предполагая, что Polymarket в будущем продолжит применять текущие стандарты комиссий на других рынках, мы можем, сравнив объем торгов на рынках "15-минутных колебаний криптовалют" с общим объемом торгов на всей платформе Polymarket, оценить теоретический потолок доходов Polymarket при текущем уровне объемов торгов — чем больше рынков с комиссиями, тем выше доходы.

Данные, собранные Odaily, показывают, что за последнюю неделю общий объем торгов на рынках "15-минутных колебаний криптовалют" на Polymarket составил около 159 миллионов долларов США (среди четырех основных токенов: BTC — 114 миллионов долларов, ETH — 30.29 миллионов долларов, SOL — 8.93 миллионов долларов, XRP — 5.73 миллионов долларов), что составляет около 9.1% от общего объема торгов Polymarket за прошлую неделю, который составил около 1.75 миллиарда долларов — Основываясь на этой пропорции и статической экстраполяции, при текущем уровне объемов торгов и структуре торгов, если Polymarket введет аналогичную модель комиссий на всех рынках, ожидается, что это принесет платформе около 418 миллионов долларов годового дохода.

Необходимо пояснить, что все вышеперечисленное является расчетами Odaily, основанными на исторических данных, реальная ситуация с доходами Polymarket неизбежно будет иметь погрешности из-за различных переменных — во-первых, взимание комиссий Polymarket длится всего три недели, размер выборки все еще мал; во-вторых, Polymarket может не применять аналогичный механизм ставок на других рынках, и различия в торговых привычках пользователей на разных рынках также приведут к различиям в окончательных результатах комиссий при динамическом механизме ставок; в-третьих, и это最关键, Polymarket все еще находится в состоянии强劲 роста, ожидается, что с дальнейшим распространением концепции预测 рынков, а также потенциальными всплесками в связи с Чемпионатом мира 2026 года и промежуточными выборами, объем торгов на платформе будет продолжать расти.

Но даже с учетом этих неопределенностей, тренд уже достаточно ясен — Polymarket демонстрирует потенциал доходности этой全新的 отрасли预测 рынков, это уже не какая-то新奇ная инновационная концепция, а настоящий, устойчивый, способный к самовоспроизводству бизнес с极具 воображения пространством для доходов.