По последним сообщениям, Moonshot AI уведомила акционеров о начале официального процесса ликвидации структуры VIE и красной структуры, чтобы расчистить путь к IPO в Гонконге.

Всего полгода назад основатель Moonshot AI Ян Чжилинь в своем внутреннем письме вновь заявлял, что "в краткосрочной перспективе не торопимся с выходом на биржу".

"Этот шаг больше похож на расчистку структурных барьеров перед выходом на биржу, то есть компания уже серьезно вступила в подготовительный период к IPO, но впереди еще несколько этапов: структура акционерного капитала, общение с регуляторами, регистрация в материковом Китае, проверка безопасности, подача документов в Гонконгскую биржу, аудит финансовой отчетности и выбор временного окна для выхода." — заявил Хуан Личун, президент International Capital House. По его словам, ликвидация VIE и красной структуры по сути означает приведение контрольных прав, ответственного субъекта и регуляторных границ в более четкое положение. Если все пойдет гладко, окно для выхода может составить от полугода до года, но если вопросы регулирования, акционеров, налогообложения и иностранного капитала окажутся сложными, процесс может затянуться.

«Phoenix WEEKLY Finance» направил запрос в Moonshot AI по вопросам, связанным с выходом на биржу, но к моменту публикации ответа не получил.

Ожидания рынка уже получили отражение в оценках. В 2023 году, при создании, оценка Moonshot AI составляла около 3 миллиардов долларов США, а к маю 2026 года эта цифра превысила 200 миллиардов долларов.

Фактически, после того как Zhipu AI и MiniMax последовательно вышли на Гонконгскую биржу, логика оценки компаний-разработчиков больших языковых моделей на вторичном рынке внезапно изменилась. Модель поддержки оценок за счет нарративов на первичном рынке ушла в прошлое, а сам "выход на биржу" превращается из результата в способ конкуренции.

"Действия Moonshot AI обусловлены как стремлением использовать золотое окно для выхода на Гонконгскую биржу, так и необходимостью активного позиционирования под давлением конкуренции в отрасли", — сказал Чжан И, генеральный директор группы iMedia Consulting.

Возможно, для Moonshot AI реальным вопросом уже является не "выходить или не выходить на биржу", а то, что когда другие конкуренты уже перешли к следующему этапу, Moonshot AI не может оставаться на месте.

Оценка в 200 миллиардов долларов может содержать эмоции рынка

С начала 2026 года "атмосфера" капитала в отрасли больших языковых моделей быстро накалилась.

За последние три года китайские стартапы в области ИИ прошли путь от незамеченных до любимчиков капитала, но настоящий поворот в настроениях отрасли произошел после выхода на биржу в начале этого года сначала Zhipu AI, а затем MiniMax.

8 января 2026 года Zhipu AI первой вышла на Гонконгскую биржу по цене размещения 116 гонконгских долларов. В первый день торгов цена акций закрылась на уровне 131,5 гонконгского доллара за акцию, поднявшись на 13,17%, а общая капитализация достигла 578,9 миллиарда гонконгских долларов. В последующие месяцы цена акций Zhipu AI продолжала расти, и по состоянию на закрытие торгов 26 мая ее общая рыночная капитализация превысила 5,996 триллиона гонконгских долларов, увеличившись почти в 10 раз по сравнению с началом размещения.

9 января MiniMax последовала примеру и вышла на Гонконгскую биржу по цене размещения 165 гонконгских долларов. В первый день торгов цена акций закрылась на уровне 345 гонконгских долларов за акцию, резко подскочив на 109% по сравнению с ценой размещения, а общая капитализация превысила 1,067 триллиона гонконгских долларов. На данный момент ее общая рыночная капитализация превышает 2,411 триллиона гонконгских долларов.

Это стало ориентиром для ценообразования во всей отрасли. С этого момента ИИ перестал быть историей о технологиях и стал рассматриваться как следующая возможность платформенного уровня.

На этом фоне оценка Moonshot AI также быстро выросла.

В ноябре 2025 года оценка Moonshot AI составляла 43 миллиарда долларов; к маю 2026 года она превысила 200 миллиардов долларов. Всего за полгода оценка увеличилась почти в 4 раза, при этом компания привлекла более 32 миллиардов долларов, что стало редким для китайских стартапов в области больших языковых моделей скачком в капитализации.

"Доход — это основа, капитал в основном обращает внимание на три вещи: во-первых, способности базовой модели; во-вторых, точки входа для пользователей и экосистему разработчиков; в-третьих, пространство для воображения будущей платформы." — считает Хуан Личун. По его мнению, для таких компаний, как Moonshot AI, капитал покупает не сегодняшний отчет о прибылях и убытках, а дефицитный входной билет в китайскую гонку больших языковых моделей. Тот, кто станет следующим ИИ-интерфейсом, может получить доступ к новым источникам прибыли, таким как поиск, офисные приложения, инструменты для разработчиков, корпоративные услуги, выполнение агентами.

В этом году на рынке даже начали часто появляться предложения доли в компании, не связанные с официальным финансированием Kimi.

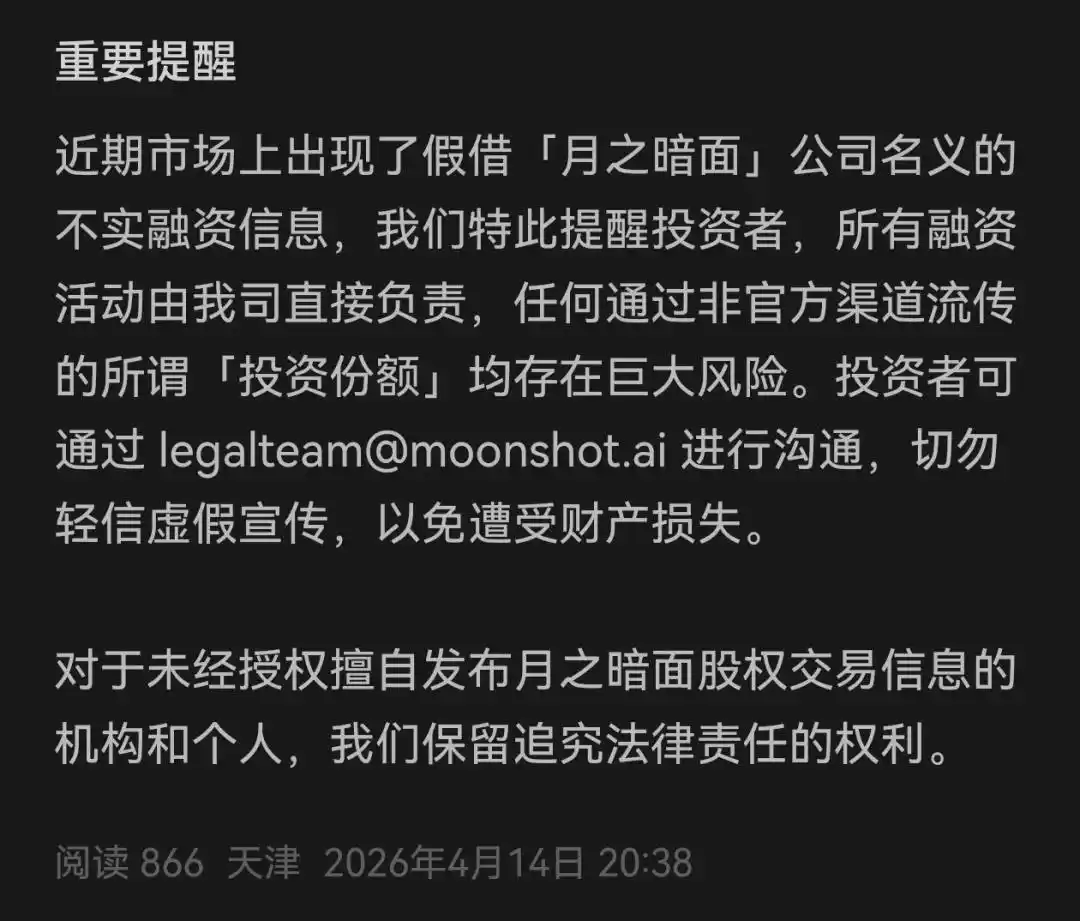

В апреле Kimi официально опровергла слухи, заявив: "В последнее время на рынке появилась ложная информация о финансировании от имени компании 'Moonshot AI'. Напоминаем инвесторам, что вся финансовая деятельность осуществляется непосредственно Moonshot AI. Любые так называемые 'инвестиционные доли', распространяемые через неофициальные каналы, несут значительные риски."

Скриншот ответа Kimi.

Когда капитал начинает лихорадочно искать "следующего Zhipu" или "следующего MiniMax", Moonshot AI уже не может так просто отказывать капиталу.

"Оценка в 200 миллиардов долларов больше похожа на авансовое списание будущего." — считает Чжан И. По его мнению, это ценообразование, при котором рынок капитала заранее конвертирует дивиденды роста.

Хуан Личун заявил: "Эта оценка будет оправдана только при выполнении трех условий: сохранение лидерства модели, постоянное расширение коммерциализации и снижение удельных затрат на вычисления. В противном случае это эмоциональная оценка."

Темп НИОКР может быть ограничен, коммерциализация выйдет на передний план

Среди китайских стартапов в области больших языковых моделей Moonshot AI является "исключением".

Ян Чжилинь долгое время был одним из самых типичных представителей "технического" направления среди китайских предпринимателей в области ИИ. По сравнению с борьбой за трафик и коммерческим расширением, он больше подчеркивал способности базовой модели, эффективность организации и долгосрочные инвестиции в НИОКР. Это также долгое время позволяло рассматривать Moonshot AI как команду, наиболее близкую по подходу к OpenAI и Anthropic в Китае.

Данные QuestMobile показывают, что количество ежемесячных активных пользователей приложения Kimi снизилось с 21,653 млн в первом квартале 2025 года до 9,027 млн в четвертом квартале.

В своем письме сотрудникам в конце 2025 года Ян Чжилинь четко определил направление корректировки на этом этапе: сосредоточиться на агентах, не ставить целью абсолютное количество пользователей, продолжать стремиться к максимальному интеллекту и ценности производительности, а также значительно сократить годовые расходы на рекламу, перейдя на коммерциализацию, движимую технологиями.

В январе 2026 года Kimi выпустила флагманскую модель K2.5. Согласно сообщениям ряда СМИ, менее чем через месяц после запуска модели доход компании за последние 20 дней превысил общий доход за весь 2025 год; по состоянию на апрель 2026 года годовой регулярный доход (ARR) компании превысил 200 миллионов долларов США, а платные подписки и доход от API постепенно становятся новыми двигателями роста.

Moonshot AI пытается доказать внешнему миру, что, несмотря на снижение MAU, коммерческие возможности Kimi сохраняются.

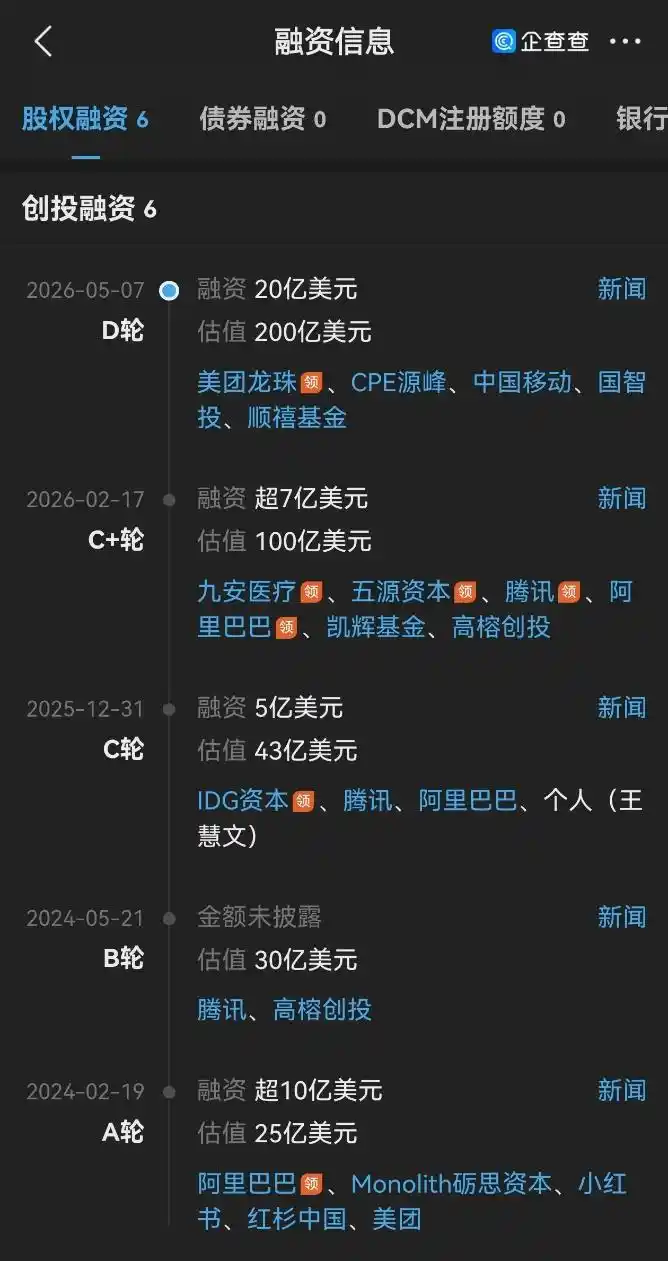

Данные Qichacha показывают, что в мае этого года Moonshot AI вновь завершила раунд финансирования серии D на сумму 20 миллиардов долларов США, который возглавил Meituan Longzhu, при участии China Mobile, CPE Source и других институциональных инвесторов. Это может означать, что капитал одобряет корректировку бизнес-модели Kimi.

Скриншот информации о финансировании Moonshot AI серии D на 20 миллиардов долларов.

Однако даже после привлечения финансирования ИИ-компании не могут избежать непрерывной гонки инвестиций. Вычислительные мощности для обучения, затраты на инференс, ресурсы данных и кадровый резерв — каждый пункт означает огромные финансовые затраты.

При выходе на вторичный рынок правила начнут меняться: помимо инвестиций, инвесторы также потребуют соответствующей отдачи.

Хуан Личун прогнозирует, что после выхода Moonshot AI на биржу многое изменится. Во-первых, организация станет более громоздкой. Финансовая отчетность, внутренний контроль, соответствие требованиям, безопасность моделей, управление данными — все это будет институционализировано. Во-вторых, темпы НИОКР будут более ограниченными. Раньше можно было говорить только о прорыве в моделировании, после выхода на биржу придется объяснять соотношение затрат и результатов, расходы на вычисления, границы убытков и пути коммерциализации. В-третьих, коммерциализация выйдет на передний план. Инвесторы не будут долго платить только за "лидерство модели", им нужно будет видеть подписки, API, корпоративных клиентов, доход от агентов и валовую маржу.

"Только привлечение финансирования без лидерства в моделировании в конечном итоге будет опровергнуто. Только создание моделей без капитала и коммерциализации также не дотянет до финала." По мнению Хуан Личуна, настоящее испытание для Moonshot AI после выхода на биржу заключается в том, сможет ли она превратить "технологическую уникальность" в "устойчивый доход" и "объяснимую оценку".

(Изображение: официальный источник Moonshot AI)

Эта статья взята из официального аккаунта WeChat "Phoenix WEEKLY Finance", автор: Ван Хань