Автор: Dolphin Research

11 мая по восточному времени США перед открытием рынка компания-пионер стейблкоинов Circle опубликовала финансовые результаты за первый квартал 2026 года.

Необходимо отметить, что поскольку объём USDC и ставка по резервным активам являются общедоступной информацией, примерно 95% процентного дохода, по сути, можно определить заранее. Поэтому цена акций Circle большую часть времени колеблется вместе с изменением рыночной капитализации USDC, что, по своей сути, тесно связано с ожиданиями снижения процентных ставок, изменениями политики в отношении криптоактивов и т.д.

Информация о потенциальных неожиданностях, которую можно почерпнуть из финансового отчёта, связана с другими, не процентными доходами, эффективностью внутреннего управления, а также стратегическими целями, отражёнными в руководящих указаниях.

В целом, ключевым моментом первого квартала по-прежнему являются средства, сосредоточенные на разделе «Прочие доходы» в отчёте, что отражает устойчивую тенденцию расширения экосистемы USDC в сценариях за пределами криптовалют. Однако жёсткие инвестиции, необходимые для такого расширения экосистемы, также будут оказывать значительное давление и вызывать волатильность краткосрочной прибыли Circle.

Конкретно:

1. Развитие экосистемы:Старый сценарий, давление на криптоинвестиции, продолжается освоение новых сценариев

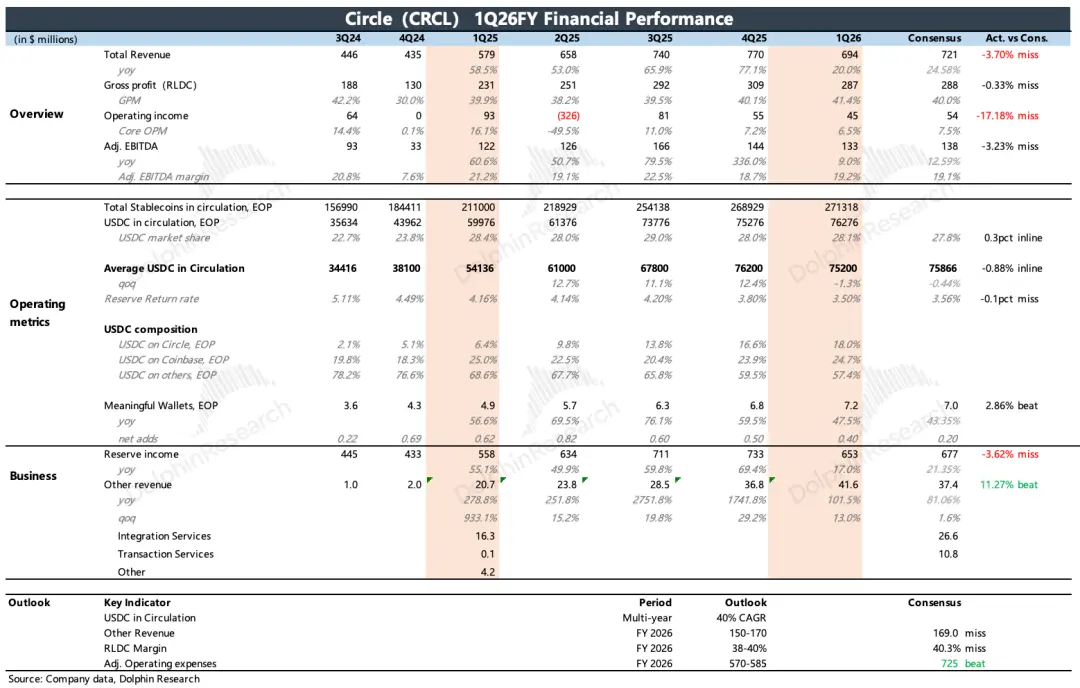

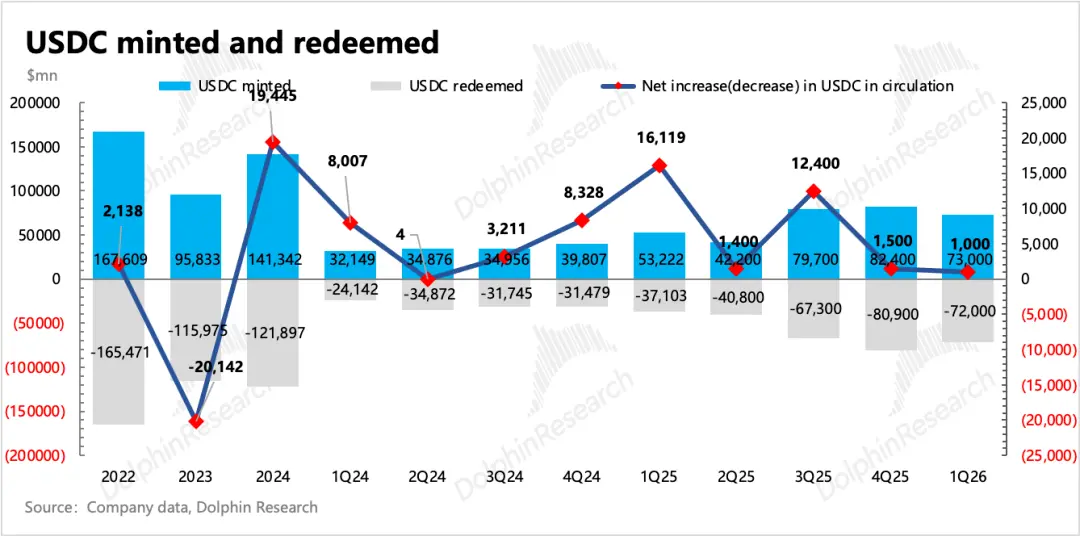

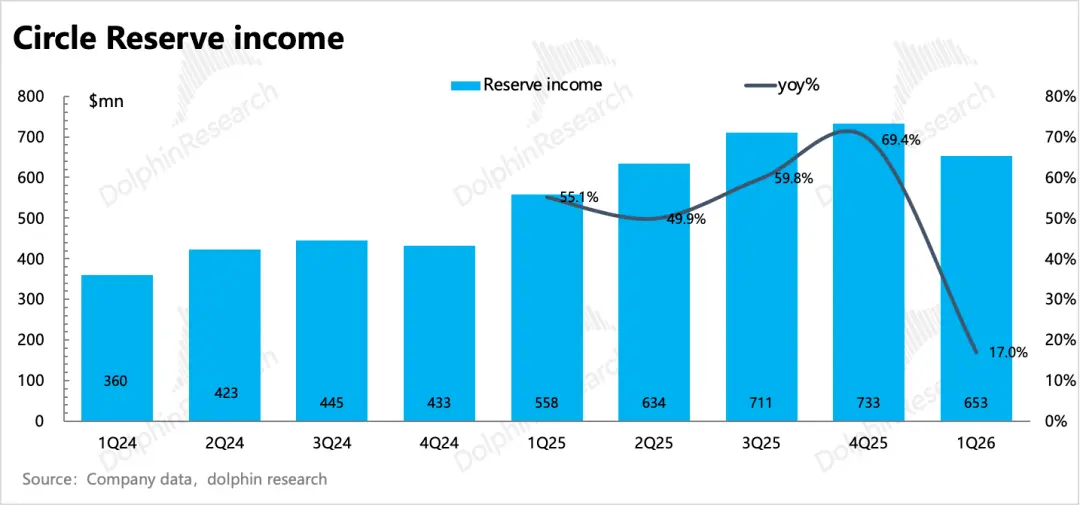

(1) Средний объём обращения USDC в первом квартале составил 75,2 млрд долларов, достигнув дна в феврале, но к концу квартала в неблагоприятных условиях геополитической напряжённости медленно вырос до почти 77 млрд долларов, увеличившись на 2% по сравнению с предыдущим кварталом, что примерно аналогично предыдущему кварталу. Объём новой эмиссии в текущем периоде составил 73 млрд долларов, снизившись по сравнению с предыдущим кварталом, что обусловлено слабыми показателями рынка криптоактивов в первом квартале. Однако, если исключить это влияние, объёмы эмиссии по-прежнему остаются на высоком уровне, что свидетельствует о расширении сфер спроса за пределами инвестиций в криптоактивы.

При этом объём погашения составил 72 млрд долларов, с более быстрым ростом по сравнению с предыдущим периодом, что отражает давление на рынке криптоактивов, где часть пользователей фиксирует прибыль или переходит в другие процентные продукты.

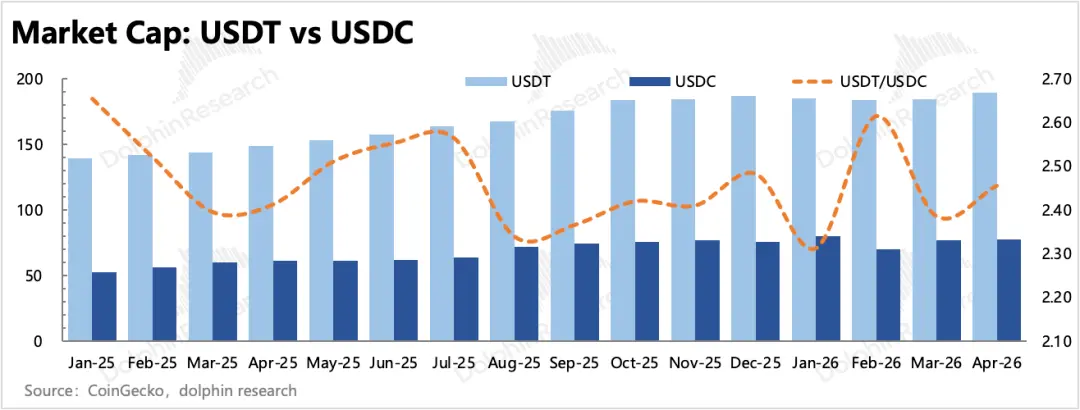

Доля конкурента USDT по сравнению с USDC, снизившись в январе, быстро восстановилась в последующие два месяца, поэтому с точки зрения конкурентных отношенийугроза конкуренции со стороны USDT по-прежнему значительна. После хакерской атаки на Drift в апреле негативная реакция в адрес Circle, активная помощь Tether проекту Drift реальными деньгами, в результате чего Circle потеряла клиентов.

В настоящее время всё ещё находится на ранней стадии расширения общего пирога стейблкоинов, поэтому конкуренция пока не станет основным фактором, влияющим на рост USDC.

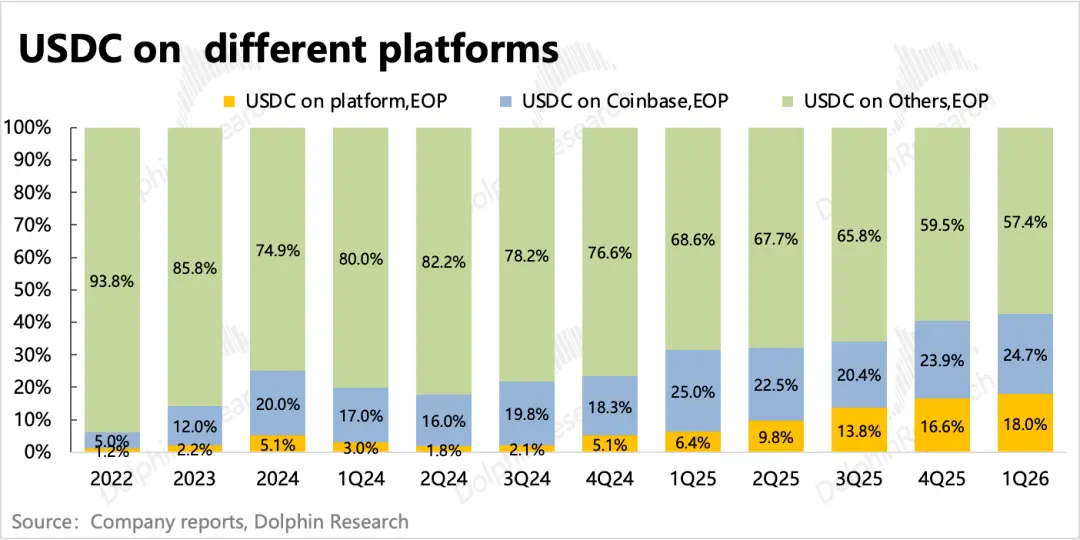

(2) Распределение внутри экосистемы USDC:Доля внутри Circle дополнительно увеличилась до 18%, среднедневной коэффициент удержания также составил 17,2%, за последний год постепенно вырос с 6% до текущего уровня, при этом доля резервных процентных доходов, распределяемых вовне, незначительно снизилась на 1 п.п., что в будущем может способствовать дальнейшей оптимизации и повышению рентабельности.На Coinbase приходится почти 25%, по сравнению с предыдущим кварталом по-прежнему наблюдается тенденция к активному удержанию.

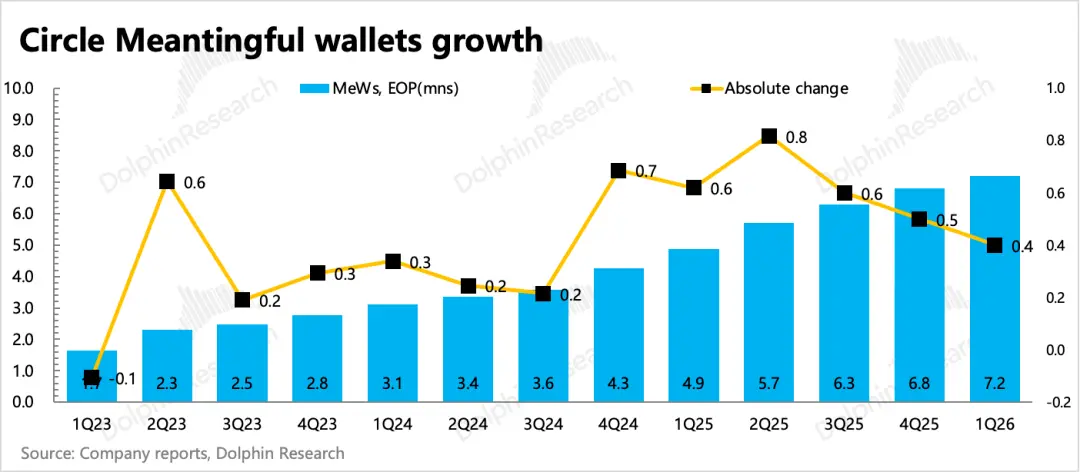

(3) По состоянию на конец первого квартала количество цифровых кошельков MeWs (криптокошельков на блокчейне с балансом более 10 долларов) достигло 7,2 миллиона, чистый прирост за квартал составил 400 000, что превысило рыночные ожидания и отражает рост пользовательской базы, напрямую подключённой к платформе.

(4) В плане новостей об экосистемных расширениях в первом квартале в основном велось сотрудничество с Cash App, Polymarket и Kyriba (поддержка нативной торговли USDC на платформах), одновременно продвигались масштабы блокчейна Arc, а также объёмы транзакций CPN.

Общий объём ончейн-транзакций USDC в первом квартале достиг 21,5 триллиона долларов, увеличившись на 263% по сравнению с аналогичным периодом прошлого года. Годовой объём транзакций CPN по состоянию на март составил 8,3 миллиарда долларов, в апреле был запущен новый продукт Managed Payments, позволяющий финансовым учреждениям внедрять платежи стейблкоинами без необходимости управления цифровыми активами.

2. Выручка имеет светлые моменты, но не так впечатляет, как в прошлом квартале: внепроцентный доход превысил ожидания, но замедлился в квартальном выражении.

Вышеупомянутые экосистемные расширения, ориентированные на B2B-сегмент, также приносят Circle доход помимо резервных процентов — он учитывается в статье «Прочие доходы». Поэтому помимо помощи в расширении рынка USDC, это также вторая кривая роста, которую Circle развивает для противодействия давлению снижения роста резервных процентных доходов в условиях цикла снижения ставок.

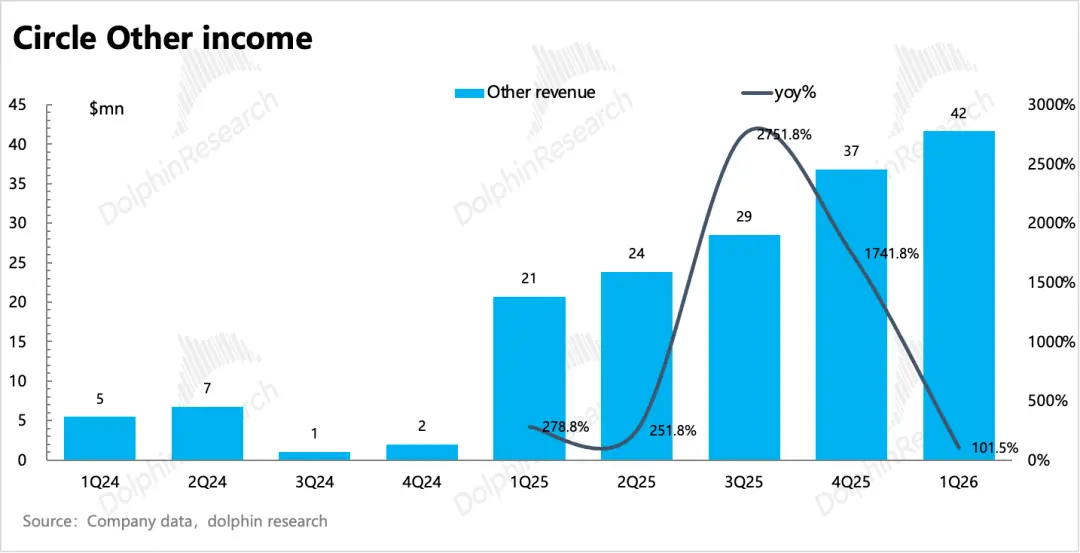

В первом квартале прочие доходы составили 42 миллиона долларов, и хотя их доля по-прежнему невелика (6%), они продолжают удваиваться на растущей базе. Однако с точки зрения тренда, квартальный рост в 13% по сравнению с 29% в предыдущем квартале несколько замедлился, что не так впечатляет, как в прошлом квартале.

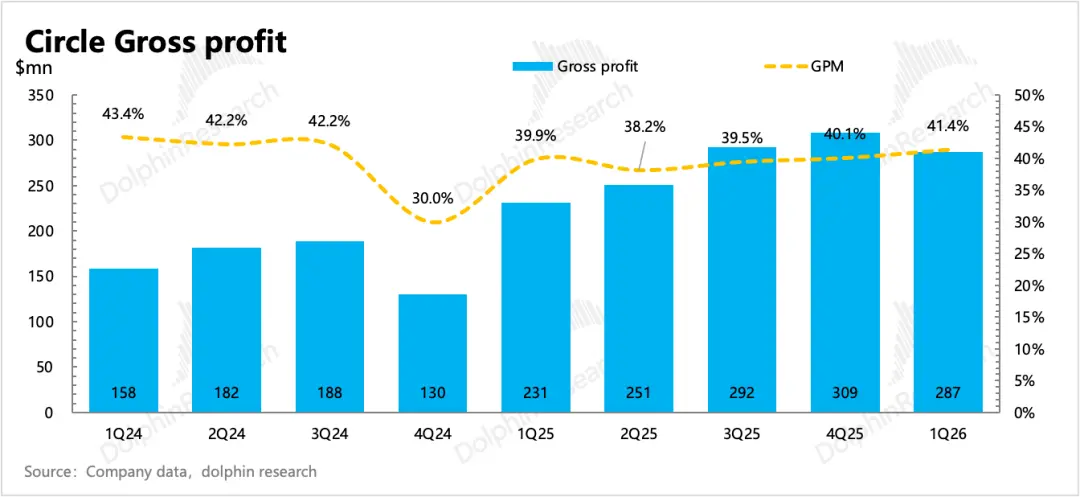

3. Валовая прибыль: увеличение доли удержания смягчает давление распределения

Ранее рынок беспокоился, что Circle при расширении экосистемы одновременно должна делиться доходами от резервных процентов с партнёрами, а также отчёт Coinbase показывает рост доли USDC у них, что повышаетканальные затраты на дистрибуцию Circle и создаёт давление на валовую прибыль.

В действительности Circle продолжает снижать давление роста затрат за счёт увеличения доли самоудерживаемого USDC.В частности, доля затрат на Coinbase в общих затратах на распределение снижается (с 97% до 75%). Следует отметить, что Coinbase обладает наибольшим влиянием в партнёрстве с Circle, поэтому их доля распределения в 50% также является самой высокой.

Кроме того, доходы от программного обеспечения, платежей и других инфраструктурных услуг в составе прочих доходов в основном относятся к высокомаржинальным видам деятельности, в этом квартале другие виды деятельности росли быстрее, а доля их вклада в выручку также увеличилась.В конечном итоге валовая прибыль составила 41,4%, продолжив улучшение на 130 базисных пунктов в квартальном выражении.

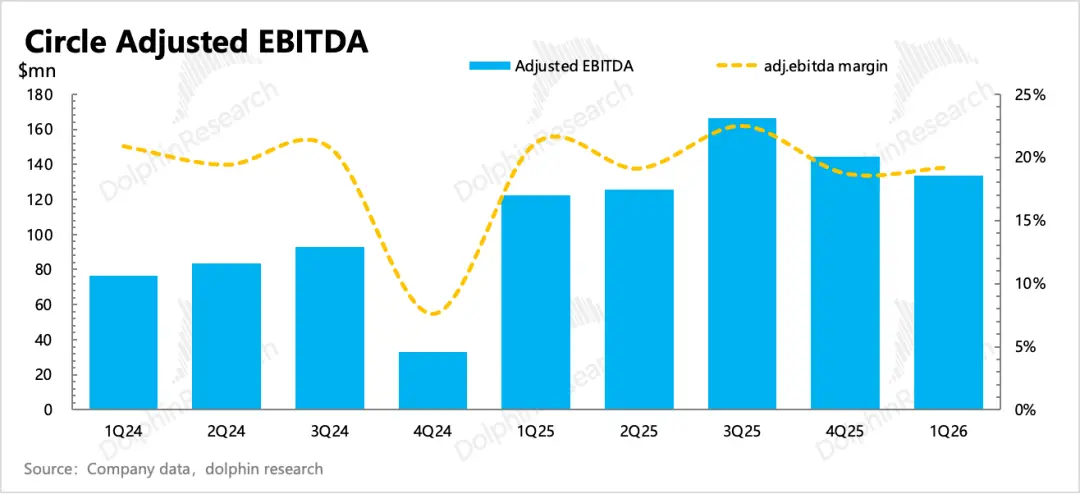

4. В условиях жёсткого инвестиционного цикла прибыль испытывает давление:Операционная прибыль значительно снизилась в годовом выражении, что также объясняется жёстким инвестиционным циклом, при котором любые воздействия на долю процентного дохода, составляющую большую часть, будут очень чувствительны к изменениям прибыли.

Однако в руководящих указаниях на 2026 финансовый год в отчёте за первый квартал руководство сохранило неизменным прогнозный диапазон скорректированных операционных расходов за год (570-585 миллионов долларов), что лучше более высоких ожиданий рынка по инвестициям (725 миллионов долларов).

5. Будущий рост: руководящие указания без изменений, краткосрочная волатильность по-прежнему требует осторожности

(1) Что касается перспектив роста объёмов USDC на многолетней основе, руководство в первом квартале по-прежнему сохраняет ожидания среднегодового темпа роста (CAGR) на уровне 40%.Но, как и в прошлом квартале, Dolphin Research считает, что следует сохранять осторожность и не спешить с оценкой:Учитывая значительные изменения на рынке, этим можно временно пренебречь; по ситуации прошлого года, эти качественные ориентиры на среднесрочную и долгосрочную перспективу не обязательно будут достигнуты в краткосрочной перспективе.

(2) Цель по прочим доходам также сохраняется на уровне 150-170 миллионов долларов, что соответствует росту на 46% в годовом выражении. Если просто годовой показатель на основе первого квартала, то это 167 миллионов долларов, что как раз попадает в целевой диапазон. ОднакоDolphin Research считает, что с эффективным продвижением закона CLARITY, у этого руководства есть большие шансы на превышение.

6. Важные финансовые показатели

Мнение Dolphin Research

Показатели первого квартала похожи на «усиленную» версию четвёртого квартала прошлого года — настроения на рынке торговли криптоактивами ещё больше охладились, но Circle не остановила шаги по расширению в другие сценарии, что привело к ещё большему краткосрочному давлению на прибыль.

Хотя Coinbase и Circle относятся к разным звеньям одной цепочки создания стоимости, и при слабой конъюнктуре на рынке криптоактивов степень влияния на них различается (влияние на Circle несколько меньше), и между ними существует проблема распределения прибыли, в краткосрочной перспективе они в целом следуют одинаковой торговой динамике.

Поэтому, если в прошлом квартале в условиях давления на криптоактивы и неясных временных рамок политики мы уделяли внимание ценовому уровню безопасности, то в этом квартале мы склонны больше обращать внимание на оставшееся пространство для восстановления вверх. Текущая оценка в 28 миллиардов долларов соответствует нашему первоначальному нейтральному прогнозу при первом охвате в прошлом году (можно обратиться к ретроспективе«Coinbase против Circle: симбиотическая борьба в мире стейблкоинов, кто будет править бал?»).

Однако, учитывая значительную краткосрочную волатильность, мы оцениваем на основе прогнозов по результатам деятельности в этом году:

Предположим, что в оставшихся трёх кварталах этого года рынок криптоактивов стабилизируется, но, возможно, из-за инфляции и ожиданий по ставкам, показатели прошлого года будет трудно повторить, поэтому ожидается, что объём стейблкоинов будет расти на 5% в квартальном выражении (в прошлом году рост с второго по третий квартал составлял 12% в квартальном выражении), к концу года достигнув 87 миллиардов долларов. При неизменной федеральной ставке в 3,5%, совокупный годовой процентный доход составит 2,8 миллиарда долларов, прочие доходы, как ожидается, превысят верхнюю границу руководства в 1,7 миллиарда долларов, общая выручка составит 3 миллиарда долларов, рост на 9% в годовом выражении.

При валовой прибыли в 42% и ориентировочных скорректированных операционных расходах в 580 миллионов долларов, скорректированная операционная прибыль составит 680 миллионов долларов. По закрытию вчерашних торгов ****(*** заблокированное содержание и подробный анализ стоимости опубликованы в LongBridge App в разделе «Динамика — Глубина» в статье с тем же названием).

Таким образом, текущий процесс восстановления Circle в основном завершён. Открытие дальнейшего пространства будет зависеть от прогресса расширения стейблкоинов и USDC.В краткосрочной перспективе, благодаря эффективному продвижению закона CLARITY, при отсутствии системных рисков в макроэкономике, можно ожидать некоторого позитивного настроя, который поддержит текущую оценку.

Ниже приведён подробный анализ

一、Основная бизнес-структура Circle

Circle является эмитентом стейблкоина USDC, её основные доходы поступают от: (1) процентов по резервным активам, эта часть дохода связана с объёмом USDC в обращении на рынке и ставками по казначейским облигациям. (2) Прочие доходы, включающие плату за Web3-программное обеспечение для клиентов (подписка SaaS), платежи CPN (плата на основе суммы/количества транзакций), а также плату за услуги или комиссию за газ в блокчейне Arc (плата за каждую транзакцию).

Чтобы избавиться от влияния снижения ставок, Circle активно развивает другие источники доходов, в 2025 году в основном продвигая платежи CPN и бизнес блокчейна Arc, в настоящее время доля прочих доходов постепенно приближается к 5%, ожидается, что в дальнейшем рост ускорится и масштабы расширятся.

В части расходов, внутренние операционные затраты Circle в основном состоят из вознаграждений сотрудников, внешние затраты в основном представляют собой канальные отчисления и транзакционные издержки, составляющие около 60% выручки (большая часть идёт Coinbase), скорректированная на амортизацию и стимулирование акциями рентабельность по EBITDA составляет около 20%, что ниже, чем у большинства финтех-платформ. Поэтому при расширении экосистемы ожидания увеличения затрат на распределение также вызывают опасения у некоторых инвесторов относительно краткосрочного давления на прибыль Circle.

С точки зрения среднесрочной и долгосрочной перспективы, важность расширения экосистемы выше. В настоящее время доля USDC на всем рынке стейблкоинов занимает второе место, по сравнению с лидером USDT, её преимущество заключается в соответствии нормативным требованиям. После принятия закона CLARITY, USDC сможет в полной мере проявить своё «относительное» преимущество, привлекая больше институциональных средств.

二、Экосистема USDC: ускорение новой эмиссии, краткосрочное влияние давления на криптоактивы

Средний объём обращения USDC в первом квартале составил 75,2 миллиарда долларов, снизившись в квартальном выражении, но к концу квартала вырос до 77 миллиардов долларов, увеличившись на 2% в квартальном выражении. Объём эмиссии в текущем периоде составил 73 миллиарда долларов, погашение — 72 миллиарда долларов, чистый прирост эмиссии по сравнению с третьим кварталом значительно замедлился. Согласно данным Coinmarketcap, в январе остаток в обращении USDC быстро снизился на фоне панического падения криптоактивов, и восстановился только в начале февраля.

1. Доля USDC на внешнем рынке

На всем рынке стейблкоинов доля USDC стабильно составляет 28% в квартальном выражении. По сравнению с прямым конкурентом USDT, USDC не демонстрирует устойчивого конкурентного преимущества.

2. Внутренняя канальная конкуренция USDC

В распределении USDC по разным каналам доля внутреннего удержания Circle продолжает увеличиваться, достигнув 18%.

Согласно отчёту Coinbase за первый квартал, их доля в обращении USDC в квартальном выражении выросла до 25%, по сравнению с предыдущим кварталом по-прежнему наблюдается тенденция к активному удержанию.

Другой ключевой показатель, отражающий развитие экосистемы — количество активных цифровых кошельков, по состоянию на конец первого квартала количество цифровых кошельков MeWs (криптокошельков на блокчейне с балансом более 10 долларов) достигло 7,2 миллиона, чистый прирост за квартал составил 400 000, предположительно, в основном из-за продолжающегося охлаждения на фоне давления на рынок криптоактивов.

三、Прочие доходы продолжают превышать ожидания, но тренд недостаточно позитивный

Поскольку в доходах Circle около 95% приходится на процентный доход от резервных активов, который по сути является публичной информацией, потенциальные неожиданности в основном связаны с прочими доходами, и в первом квартале они снова превысили ожидания.

Конкретно, прочие доходы в основном включают доход от эмиссии, транзакций, кастодиальных услуг, набор Web3 API, токенизированный фонд USYC, а также комиссии CPN, запущенные в апреле прошлого года (фиксированная плата за подключение + плата за расчёт/аудит за каждую транзакцию, комиссия за газ в сети Arc и т.д.).

Прочие доходы в первом квартале составили 42 миллиона долларов, рост на 13% в квартальном выражении, несколько замедлился, не так впечатляет, как в прошлом квартале. При этом руководство компании сохраняет прогноз по прочим доходам на весь год на уровне 150-170 миллионов долларов, с точки зрения тренда квартального роста, фактически не слишком активно. Dolphin Research считает, что при нормальном расширении USDC, вероятно, будет возможность снова превысить прогноз.

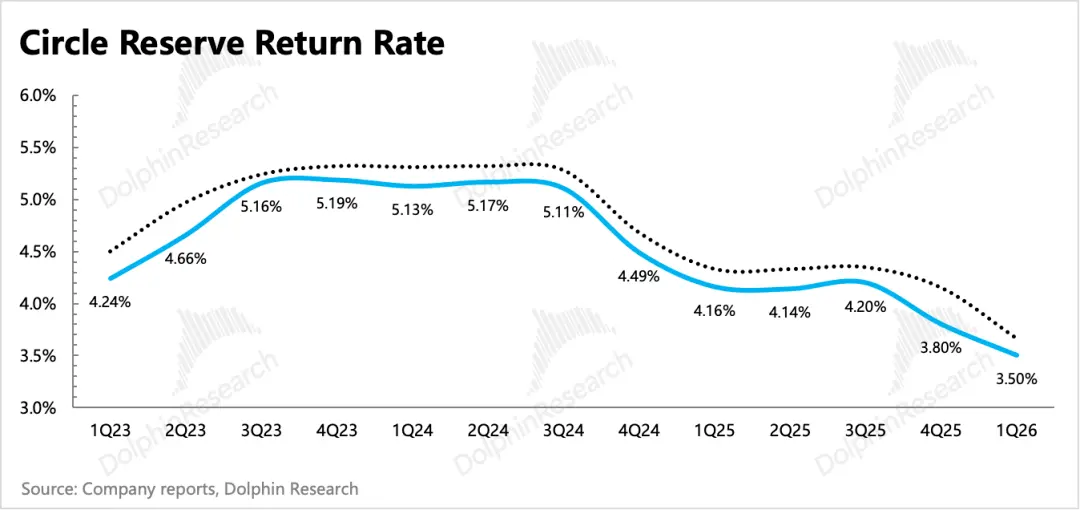

Основной доход, составляющий большую часть, зависит от темпов расширения USDC, а также текущей среды процентных ставок по казначейским облигациям. Средний объём USDC в первом квартале вырос на 70% в годовом выражении, ставка снизилась до 3,5%, снижение на 64 базисных пункта в годовом выражении, в итоге рост процентного дохода от резервов составил 17%, что уже быстро замедлилось.

Однако ожидания дальнейшего снижения ставок практически сошли на нет, поэтому при стабильных ставках, при нормальном расширении объёмов в оставшихся трёх кварталах (рост более 5% в квартальном выражении), то в течение года, несмотря на давление со стороны ставок в годовом выражении, всё же можно надеяться на рост в 5-10%.

四、Прибыль под давлением в условиях жёстких инвестиций

Валовая прибыль в первом квартале увеличилась на 130 базисных пунктов в квартальном выражении, достигнув 41,4%. Circle продолжает снижать давление роста канальных затрат за счёт увеличения доли самоудерживаемого USDC. Кроме того, доходы от программного обеспечения, платежей и других инфраструктурных услуг в основном относятся к высокомаржинальным видам деятельности, в этом квартале другие виды деятельности росли быстрее, а доля их вклада в выручку также увеличилась.

Несмотря на замедление роста выручки в первом квартале, соотношение различных расходов к выручке по-прежнему оставалось высоким, в итоге скорректированная EBITDA составила 133 миллиона долларов, рентабельность 19,2%, улучшившись на 50 базисных пунктов в квартальном выражении.

Компания сохраняет руководящие указания по общим затратам и операционным расходам на 2026 финансовый год (исключая SBC и амортизацию) без изменений, по-прежнему на уровне 570-585 миллионов долларов, рост на 10% в годовом выражении, что ниже рыночных ожиданий.