Автор: KarenZ, Foresight News

Оригинальное название: Strategy жёстко отвечает MSCI: Исчерпывающая защита DAT

Продолжается борьба, определяющая развитие индустрии компаний с казначейскими цифровыми активами (DAT).

В октябре глобальная компания по составлению индексов MSCI выдвинула предложение об исключении компаний, у которых объём цифровых активов составляет 50% или более от общих активов, из своих глобальных инвестиционных рыночных индексов. Эта мера напрямую угрожает рыночной позиции таких компаний, как Strategy, и даже может изменить направление капиталовложений для всей индустрии компаний с цифровыми активами.

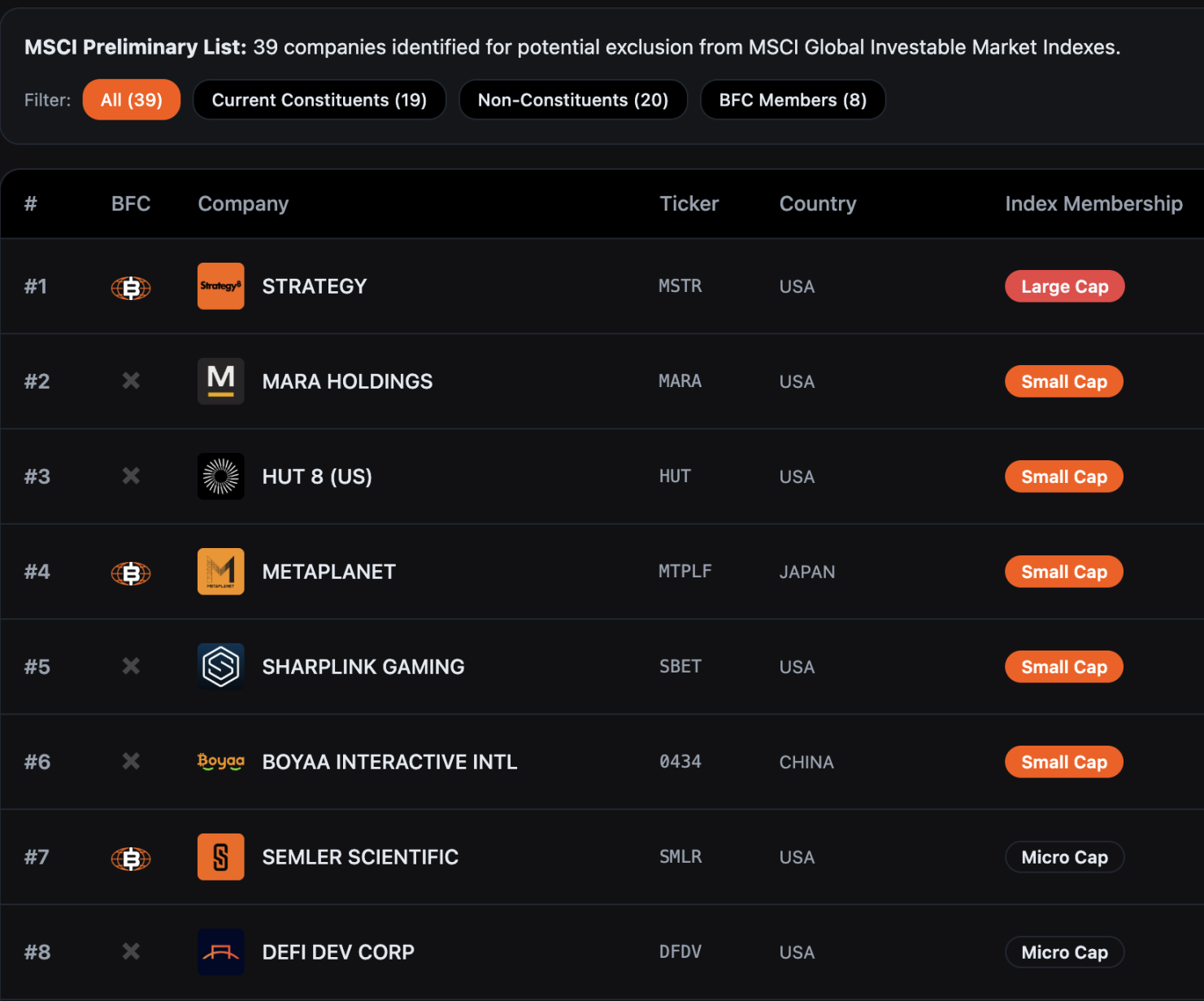

Согласно данным Bitcoin for Corporations, 39 компаний могут быть исключены из глобального инвестиционного рыночного индекса MSCI. Ранее аналитики JPMorgan предупредили, что одно только исключение Strategy может привести к оттоку почти 2,8 миллиардов долларов пассивных средств, а если другие провайдеры индексов последуют этому правилу, это может вызвать отток до 8,8 миллиардов долларов.

В настоящее время консультационный период по данному предложению MSCI продлится до 31 декабря 2025 года, окончательное решение ожидается до 15 января 2026 года, и любые корректировки будут официально внедрены в процессе пересмотра индексов в феврале 2026 года.

В ответ на эту срочную ситуацию Strategy 10 декабря направила в Комитет по фондовым индексам MSCI открытое письмо на 12 страницах с жёсткой формулировкой, подписанное исполнительным председателем и основателем компании Майклом Сейлором и президентом и CEO Фонгом Ле, в котором чётко выражено категорическое несогласие с данным предложением. В письме прямо говорится: «Это предложение вводит в серьёзное заблуждение и будет иметь далеко идущие разрушительные последствия для интересов глобальных инвесторов и развития индустрии цифровых активов. Мы настоятельно призываем MSCI полностью отозвать этот план».

Четыре ключевых аргумента защиты Strategy

Цифровые активы — это революционная базовая технология, преобразующая финансовую систему

Strategy считает, что предложение MSCI недооценивает стратегическую ценность биткоина и других цифровых активов. С момента появления биткоина 16 лет назад Сатоши Накамото, этот цифровой актив постепенно стал ключевым компонентом глобальной экономики с текущей общей рыночной стоимостью около 1,85 триллиона долларов.

По мнению Strategy, цифровые активы — это отнюдь не простой финансовый инструмент, а фундаментальная технологическая инновация, способная преобразовать глобальную финансовую систему — компании, инвестирующие в инфраструктуру, связанную с биткоином, строят новую финансовую экосистему, что ничем не отличается от ведущих компаний в истории, которые глубоко внедряли единые новые технологии.

Подобно тому, как Standard Oil в XIX веке глубоко занималась добычей нефти, а AT&T в XX веке全力 (полностью) строила телефонные сети, эти компании, благодаря前瞻性 (前瞻性) инвестициям в ключевую инфраструктуру, заложили прочную основу для последующей экономической трансформации и в конечном итоге стали отраслевыми эталонами. Strategy считает, что компании, фокусирующиеся на цифровых активах сегодня, повторяют этот путь «технологических основоположников» и не должны быть просто отвергнуты традиционными правилами индексов.

DAT — это операционные компании, а не пассивные фонды

Это ключевой тезис защиты Strategy — компании с казначейскими цифровыми активами (DAT) являются операционными предприятиями с完整的 (полной) бизнес-моделью, а не просто инвестиционными фондами, пассивно持有 (удерживающими) биткоин. Хотя Strategy в настоящее время持有 (держит) более 600 000 биткоинов, её основная ценность зависит не от волатильности цены биткоина, а от создания устойчивой доходности для акционеров через设计并推出 (разработку и выпуск) уникальных инструментов «цифрового кредита».

Если具体来看 (конкретнее), инструменты «цифрового кредита», выпускаемые Strategy, включают различные типы привилегированных акций с фиксированной дивидендной ставкой, плавающей дивидендной ставкой, разным уровнем приоритета и условиями кредитной защиты. Продажа этих инструментов позволяет привлечь средства, которые затем используются для увеличения持有 (удерживания) биткоина. До тех пор, пока долгосрочная投资回报 (доходность инвестиций) в биткоин превышает融资成本 (стоимость финансирования) Strategy в долларах США, это может принести стабильный доход акционерам и клиентам. Strategy подчеркивает, что эта модель «активного управления + прироста стоимости активов» fundamentally (фундаментально) отличается от логики пассивного управления традиционных инвестиционных фондов или ETF и должна рассматриваться как обычное операционное предприятие.

Кроме того, в письме Strategy задаётся вопрос: почему нефтяные гиганты, трасты недвижимости (REITs), лесные компании и другие могут集中持有 (концентрированно удерживать) активы одного класса, но не классифицируются как инвестиционные фонды и не исключаются из индексов? Установление特殊限制 (особых ограничений) только для компаний с цифровыми активами явно не соответствует принципу отраслевой справедливости.

Порог в 50% цифровых активов является произвольным, дискриминационным и нереалистичным

Strategy указывает, что предложение MSCI использует дискриминационные标准 (стандарты). Многие крупные компании в традиционных отраслях также高度集中持有 (высококонцентрированно удерживают) активы одного класса в своих активах, включая нефтегазовые компании, трасты недвижимости (REITs), лесные компании и предприятия энергетической инфраструктуры. Но MSCI установила特殊排斥标准 (особые стандарты исключения) только для компаний с цифровыми активами, что представляет собой очевидное несправедливое обращение.

С точки зрения осуществимости внедрения, это предложение также имеет серьёзные проблемы. Из-за высокой волатильности цен на цифровые активы одна и та же компания может в течение нескольких дней repeatedly进出 (неоднократно входить и выходить) из индекса MSCI из-за изменения стоимости активов, вызывая рыночный хаос. Кроме того, различия между accounting准则 (учётными стандартами) (разные подходы к обработке цифровых активов по американским стандартам GAAP и международным стандартам IFRS) приведут к тому, что компании с одинаковой бизнес-моделью будут получать дифференцированное待遇 (обращение) в зависимости от страны регистрации.

Нарушает принцип нейтральности индекса, вносит политический уклон

Strategy считает, что предложение MSCI по своей сути является суждением о ценности (оценкой) определённого класса активов, что противоречит основному принципу нейтральности, которого должен придерживаться провайдер индексов. MSCI заявляет рынку и регуляторам, что её индексы обеспечивают «исчерпывающее» покрытие,旨在反映 (предназначены для отражения) «эволюции базового рынка акций», и не должны «давать оценку тому, хорош или уместен любой рынок, компания, стратегия или инвестиция».

Путем выборочного исключения компаний с цифровыми активами MSCI фактически делает политическое заявление от имени рынка, чего провайдер индексов должен избегать.

Противоречит стратегии США в области цифровых активов

Strategy特别强调 (особо подчёркивает), что это предложение конфликтует со стратегической целью администрации Трампа по продвижению лидерства в области цифровых активов. Администрация Трампа в первую неделю своего пребывания у власти подписала исполнительный указ о содействии росту цифровых финансовых технологий и создала стратегические резервы биткоина,旨在使 (стремясь сделать) США全球领导者 (глобальным лидером) в области цифровых активов.

Но если предложение MSCI будет реализовано, это напрямую предотвратит (не позволит) инвестирование долгосрочных средств, таких как американские пенсионные фонды, планы 401(k), в компании с цифровыми активами, что приведёт к оттоку миллиардов долларов капитала из отрасли. Это не только помешает развитию американских инновационных компаний в области цифровых активов, но и может ослабить конкурентоспособность США в этой стратегической области, идя вразрез с установленной политикой правительства.

Strategy ссылается на оценки аналитиков, согласно которым только одна Strategy может столкнуться с принудительной продажей акций на сумму до 2,8 миллиардов долларов из-за предложения MSCI. Это наносит ущерб не только самой Strategy, но и окажет сдерживающий эффект (эффект сдерживания) на всю экосистему цифровых активов, например, может вынудить (заставить) майнинговые компании биткоина提前出售 (досрочно продавать) активы для调整资产结构 (корректировки структуры активов), thereby扭曲 (таким образом искажая) нормальные отношения спроса и предложения на рынке цифровых активов.

Конечные требования Strategy

Strategy выдвигает два основных требования в открытом письме:

Первое — надежда (надежда), что MSCI полностью отозвёт это предложение об исключении, позволив рынку通过自由竞争检验 (проверить через свободную конкуренцию) ценность компаний с казначейскими цифровыми активами (DAT), чтобы индекс мог нейтрально и忠实地反映 (верно отражать) тенденции развития финансовых технологий следующего поколения;

Второе — если MSCI будет настаивать на «особом обращении» с компаниями с цифровыми активами, то необходимо расширить范围行业咨询 (сферу отраслевых консультаций),延长咨询时间 (продлить время консультаций) и предоставить более充分的逻辑支撑 (достаточное логическое обоснование) для объяснения разумности правил.

Strategy не одинока в этой борьбе

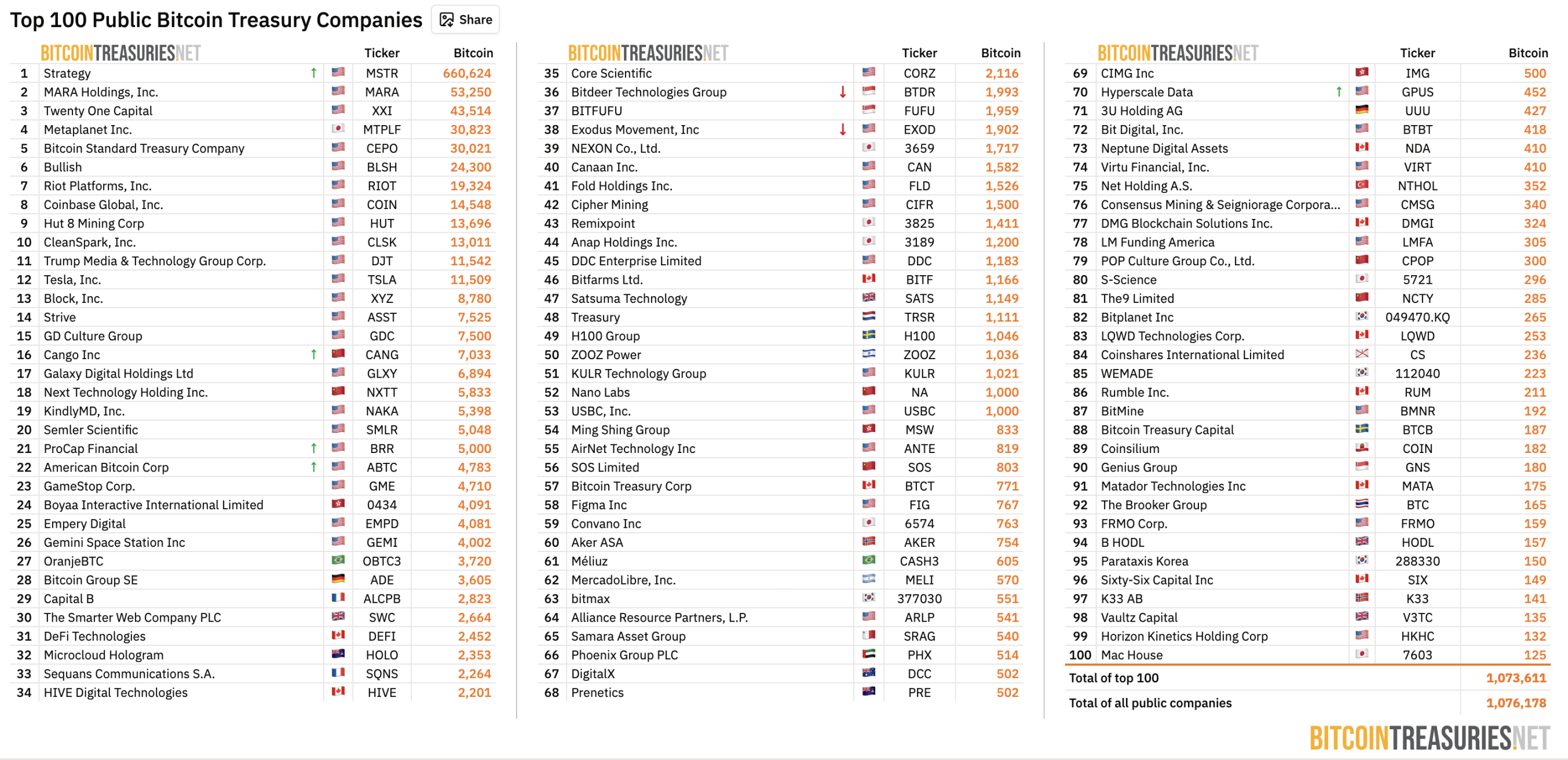

Strategy не одинока в этой борьбе. Согласно данным BitcoinTreasuries.NET, по состоянию на 11 декабря 208 публичных компаний по всему миру持有 (удерживают) более 1,07 миллиона биткоинов, что превышает 5% от общего предложения биткоина, а текущая стоимость составляет около 1000 миллиардов долларов.

Источник: BitcoinTreasuries.NET

Эти компании с казначейскими цифровыми активами стали важным мостом для институционального принятия криптовалют, предоставляя пенсионным фондам, endowment基金 (эндаумент-фондам) и другим традиционным финансовым институтам合规的间接敞口 (соответствующий нормам косвенный доступ).

Ранее публичная компания,持有比特币 (удерживающая биткоин), Strive предложила, чтобы MSCI предоставила «право выбора» в отношении компаний с цифровыми активами самому рынку. Простое и прямое решение — создать версии существующих индексов «исключая компании с казначейскими цифровыми активами», например, индекс MSCI USA ex Digital Asset Treasuries и индекс MSCI ACWI ex Digital Asset Treasuries. Через прозрачный механизм筛选 (отбора) инвесторы смогут самостоятельно выбирать отслеживаемый benchmark (бенчмарк), сохраняя целостность индекса и удовлетворяя потребности различных инвесторов.

Кроме того, отраслевая организация Bitcoin for Corporations инициировала совместное обращение (петицию), призывая MSCI отозвать это предложение по цифровым активам, и主张 (утверждает), что классификация должна основываться на фактической бизнес-модели компании, финансовых результатах и операционных характеристиках, а не просто на划线 (проведении черты) по доле активов. Согласно显示 (показаниям) на сайте организации, на данный момент 309 компаний или инвесторов подписали совместное письмо. Среди подписавшихся, помимо Strategy, есть высшее руководство известных отраслевых компаний, таких как Strive, BitGo, Redwood Digital Group, 21MIL, Btc inc, DeFi Development Corp, а также众多 (многочисленные) индивидуальные разработчики и инвесторы.

Резюме

Это противостояние между Strategy и MSCI по своей сути является фундаментальными дебатами о том, как «новые финансовые инновации интегрируются в традиционную систему». Компании с казначейскими цифровыми активами (DAT), как «跨界者» (кросс-отраслевые игроки) между традиционными финансами и миром криптовалют, не являются ни чисто технологическими предприятиями, ни простыми инвестиционными фондами, а представляют собой全新的商业模式 (новую бизнес-модель), построенную на основе цифровых активов.

Предложение MSCI пытается с помощью стандарта «50% доли активов» отнести эти сложные实体 (сущности) к «инвестиционным фондам» и исключить их из индексов; а Strategy настаивает на том, что такое упрощённое处理 (обращение) является серьёзным непониманием их商业本质 (бизнес-сущности) и, более того, отходом от принципа нейтральности индексов. По мере приближения даты принятия решения 15 января 2026 года, результат этой борьбы不仅将决定 (не только определит) «право на вход» в индекс для многих биткоин-持有上市公司 (удерживающих публичных компаний), но и очертит ключевые «границы выживания» для будущего положения индустрии цифровых активов в глобальной традиционной финансовой системе.

Twitter:https://twitter.com/BitpushNewsCN

Группа общения比推 TG (Bitpush TG):https://t.me/BitPushCommunity

Подписка比推 TG (Bitpush TG): https://t.me/bitpush