Когда рынок переживает резкое падение, нарративы быстро находят видимый источник.

В последнее время рынок активно обсуждает обвал 5 февраля и отскок почти на десять тысяч долларов 6 февраля. Советник Bitwise и главный инвестиционный директор ProCap Джефф Парк считает, что эта волатильность теснее связана с системой биткоин-ETF, чем кажется, и ключевые подсказки сосредоточены на вторичном рынке и рынке опционов биткоин-траста iShares (IBIT) от BlackRock.

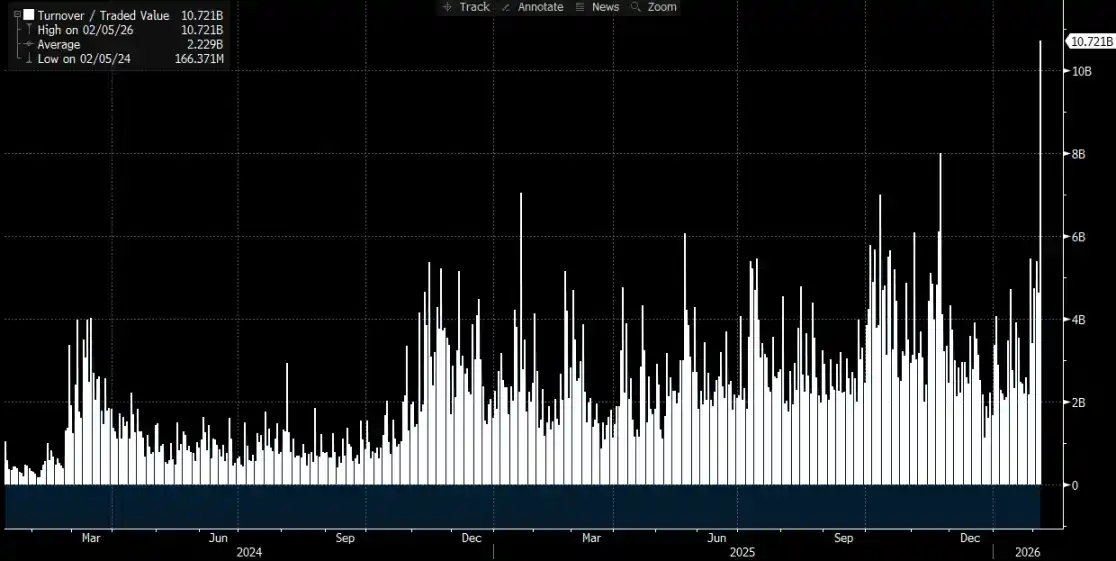

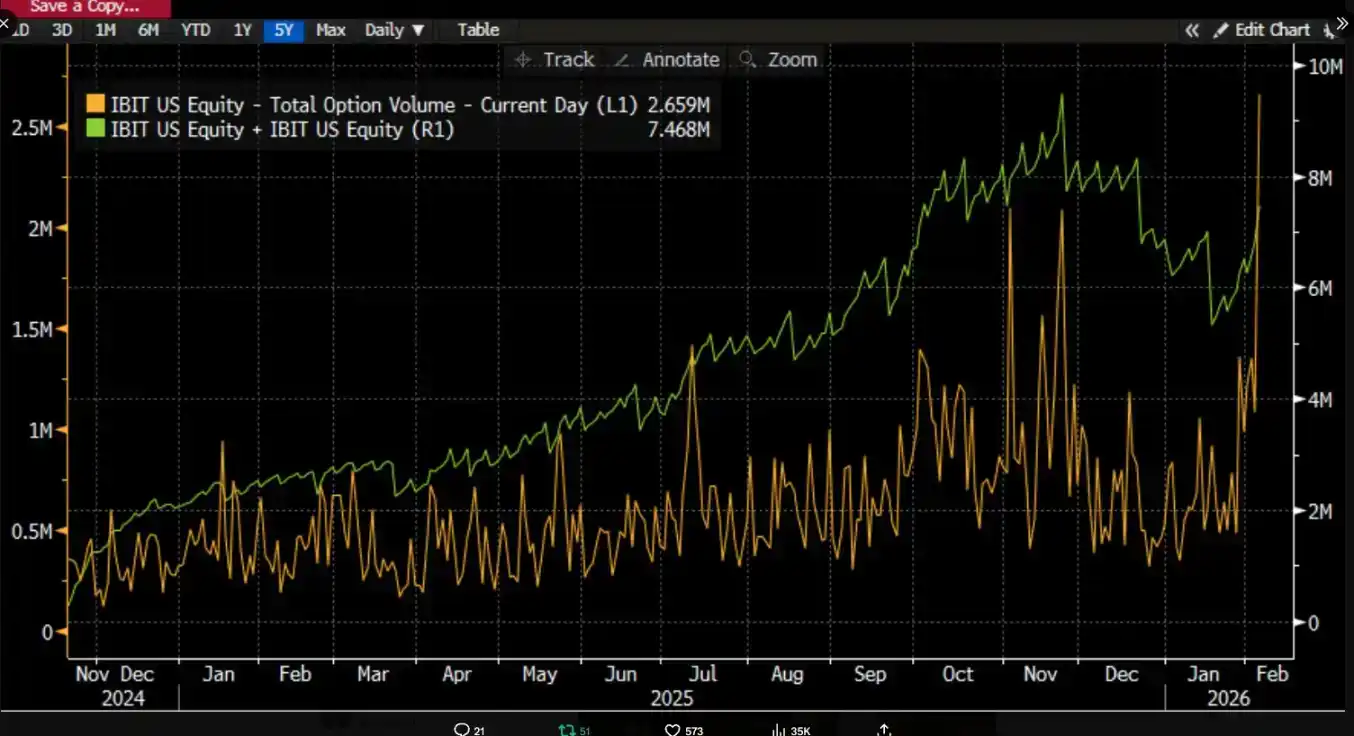

Он указывает, что 5 февраля на IBIT был зафиксирован рекордный объем торгов и активность опционов, при этом масштаб торгов был значительно выше обычного, а структура опционных сделок была смещена в сторону пут-опционов. Что еще более контринтуитивно, так это то, что по историческим меркам, если цена падает на двузначное число за один день, рынок обычно видит чистый выкуп и отток средств, но в данном случае произошло обратное. IBIT зафиксировал чистое создание, новые доли推动规模上升推动规模上升, и весь портфель спотовых ETF также показал чистый приток.

Джефф Парк считает, что такая комбинация «обвала и чистого создания» ослабляет объяснительную силу единственного пути, согласно которому инвесторы ETF в панике выкупают доли, вызывая падение. Вместо этого это больше соответствует ситуации, когда внутри традиционных финансовых систем происходит снижение левериджа и рисков, а дилеры, маркет-мейкеры и мульти-активные портфели вынуждены снижать риски в рамках деривативов и хеджирования. Давление продаж в большей степени исходит от корректировки позиций бумажной денежной системы и сжатия цепочек хеджирования, что в конечном итоге передает удар на цену биткоина через вторичные рыночные сделки IBIT и опционное хеджирование.

Многие рыночные дискуссии легко связывают клиринг институциональных инвесторов IBIT с тем, что рынок следует за ним вниз, в одно предложение, но если не разобрать механистические детали этой причинно-следственной цепи,很容易把顺序写反很容易把顺序写反. Торгуемым активом на вторичном рынке ETF являются доли ETF, а создание и выкуп на первичном рынке соответствуют изменениям BTC на стороне хранения. Линейное отображение объемов торгов на вторичном рынке в эквивалентные продажи спота логически lacks несколько необходимых объяснений环节.

Так называемый «масштабный клиринг, вызванный IBIT», на самом деле спор о пути передачи

Споры вокруг IBIT в основном сосредоточены на том, на каком уровне рынка ETF и через какой механизм давление передается на сторону ценообразования BTC.

Более распространенный нарратив фокусируется на чистом оттоке с первичного рынка. Его интуиция проста: если инвесторы ETF выкупают доли в панике, эмитенты или уполномоченные участники (AP) должны продавать базовый BTC для удовлетворения требований по выкупу, давление продаж попадает на спотовый рынок, падение цен进一步引发强平进一步引发强平, образуя давку.

Эта логика звучит完整, но часто忽略рует факт. Обычные инвесторы и绝大多数机构绝大多数机构 не могут напрямую申购或赎回申购或赎回 доли ETF, только уполномоченные участники могут делать创建与赎回创建与赎回 на первичном рынке.通常所说的通常所说的 «ежедневный чистый приток/отток», общепринятая методология指的是指的是 изменений общего количества долей на первичном рынке,无论 вторичный рынок无论 вторичный рынок торгуется多么 активно, это только меняет держателей долей, не меняет автоматически общее количество долей, и уж тем более не приводит автоматически к增减增减 BTC на стороне хранения.

Аналитик Phyrex Ni заявляет, что Парк говорит о клиринге именно спотового ETF IBIT, а не о клиринге биткоина. Для IBIT,买卖的买卖的 на вторичном рынке — это только акция IBIT, цена привязана к BTC, но сама торговая активность完成换手完成换手 только внутри фондового рынка.

Единственный环节, который真正触及вает BTC, происходит на первичном рынке, а именно创建与赎回创建与赎回 долей, и этот канал выполняется AP (можно理解为做市商做市商). При создании, новые доли IBIT требуют от AP предоставления соответствующего BTC или денежного эквивалента, BTC попадает в систему хранения, регулируется, эмитенты и связанные机构机构 не могут随意动用随意动用. При выкупе, сторона хранения передает BTC AP, который завершает последующее处置处置 и结算结算 средств выкупа.

ETF实际上实际上是两层市场两层市场, первичный рынок — это в основном покупка и выкуп биткоина, эта часть почти полностью обеспечивается ликвидностью AP, по сути, это то же самое, что генерировать USDC за USD, и AP редко торгуют BTC через交易平台交易平台, поэтому最大的用处最大的用处 покупки спотовых ETF заключается в том, что они锁住了锁住了 ликвидность биткоина.

Даже при выкупе, продажа AP не обязательно должна проходить через открытый рынок, особенно через спотовый рынок бирж. У самих AP может быть库存库存 BTC, или они могут использовать более гибкие способы в течение T+1结算窗口结算窗口 для завершения расчетов и安排资金安排资金.因此, даже во время масштабного клиринга 5 января, BTC, выкупленный инвесторами BlackRock, составил менее 3000 монет, а все американские спотовые ETF-机构机构 выкупили в сумме менее 6000 BTC, то есть ETF-机构机构抛售抛售 на рынок максимум 6000 BTC. И эти 6000 монет还不未必都是还不未必都是 переведены на交易平台中的交易平台中的.

А то, о чем говорит Парк, клиринг IBIT,实际上实际上 произошел на вторичном рынке, общий объем торгов составил около 10,7 миллиарда долларов, это действительно крупнейший объем торгов за всю историю IBIT, и он确实 также引发了一些引发了一些机构的清算,但需要注意的是但需要注意的是, эта часть清算清算 — это только清算 IBIT, а не清算 биткоина, по крайней мере, эта часть清算并没有传导到并没有传导到 первичный рынок IBIT.

所以所以 резкое падение биткоина только引发了引发ло清算 IBIT, но не привело к клирингу BTC, вызванному IBIT. Торгуемым активом на вторичном рынке ETF по сути仍然是仍然是 ETF, а BTC — это лишь价格锚定价格锚定 ETF.能够对市场产生影响能够对市场产生影响 максимум — это清算, вызванный продажей BTC на первичном рынке, а не IBIT.实际上实际上, хотя цена BTC в четверг упала более чем на 14%, но фактически чистый отток BTC из ETF составил только 0,46%. В тот день спотовые ETF на BTC总共持有总共持有 1,273,280 BTC, общий отток — 5,952 BTC.

Передача от IBIT к споту

@MrluanluanOP считает, что когда происходит клиринг длинных позиций по IBIT, на вторичном рынке происходит集中抛售集中抛售, и если естественные покупатели не могут поглотить его в достаточной степени, IBIT будет торговаться с дисконтом дисконтом к своей隐含净值隐含净值. Чем больше дисконт, тем больше арбитражное пространство арбитражное пространство, и у AP и рыночных арбитражеров больше стимулов покупать дисконтированный IBIT, поскольку это их основной日常 способ заработка. Пока дисконт покрывает издержки, теоретически всегда найдутся профессиональные资金资金, готовые承接承接, поэтому не стоит беспокоиться о «抛压无人接» («давлении продаж без покупателей»).

Но после поглощения проблема переходит к управлению рисками. После покупки долей IBIT, AP не может немедленно выкупить и变现变现 эти доли по текущей цене, выкуп требует времени и流程成本流程成本. В течение этого времени цена BTC и IBIT может колебаться, AP сталкивается с риском чистого敞ения чистого敞ения, поэтому немедленно проводит хеджирование хеджирование. Методы хеджирования могут включать продажу现货库存现货库存 или открытие коротких позиций short positions по BTC на фьючерсном рынке.

Если хеджирование заключается в спотовой продаже, это напрямую давит на спотовую цену; если хеджирование заключается в short по фьючерсам, это сначала проявляется в изменении спредов спредов и базисов базисов, а затем через量化量化, арбитраж или межрыночную торговлю进一步影响进一步影响 спот.

После завершения хеджирования AP имеет относительно нейтральную или полностью хеджированную позицию и может на操作层面操作层面 более гибко выбирать, когда обрабатывать эти доли IBIT. Один вариант — выбрать выкуп у эмитента в тот же день, тогда в официальных данных о притоке/оттоке после закрытия будет отражен выкуп и чистый отток. Другой вариант —暂不赎回暂不赎回, дождаться восстановления настроений на вторичном рынке или отскока цены и затем напрямую продать IBIT обратно на рынок, заверши thus整套交易整套交易 без прохождения первичного рынка. Если на следующий день IBIT восстановит премию премию или дисконт сузится, AP может продать позицию на вторичном рынке, реализовав прибыль от разницы в цене, и одновременно закрыть ранее созданные короткие фьючерсные позиции или выкупить先前卖出先前卖出的现货库存.

即使即使最终处理处理 долей в основном происходит на вторичном рынке, и на первичном рынке может не быть значительного чистого выкупа, передача от IBIT к BTC все равно может произойти, потому что хеджирующие действия, предпринятые AP при поглощении дисконтированных позиций, могут передать давление на спотовый или деривативный рынок BTC, thus形成形成 путь, по которому давление продаж на вторичном рынке IBIT через хеджирование переливается на рынок BTC.