Оригинал| Odaily星球日报 (@OdailyChina)

Автор| Wenser (@wenser 2010 )

На продолжающемся падающем рынке две «звезды» казначейств DAT — компания Strategy и компания Bitmine — столкнулись с огромными нереализованными убытками.

Сегодня утром цена BTC в какой-то момент упала ниже 62 000 долларов, а на данный момент составляет около 63 800 долларов; ETH же упал ниже 1800 долларов и сейчас торгуется около 1780 долларов. По текущей цене нереализованные убытки Strategy достигли ошеломляющих 100 миллиардов долларов; нереализованные убытки Bitmine также достигли примерно 90 миллиардов долларов. В одно мгновение Майкл Сэйлор и Том Ли стали «братьями по несчастью», а Strategy и Bitmine заняли первые два места в списке «компаний DAT с наибольшими убытками».

Однако по сравнению со Strategy, которой необходимо постоянно выплачивать дивиденды по акциям, финансовая нагрузка на Bitmine меньше, и она сохраняет гибкость, такую как возможность привлечения средств через привилегированные акции STRC. Сообщается, что Bitmine планирует привлечь 300 миллионов долларов путем выпуска бессрочных привилегированных акций с годовой дивидендной доходностью 9,5%. Таким образом, Bitmine продолжает наращивать запасы ETH; в то время как дамоклов меч, нависший над Strategy, — откуда взять средства для последующих выплат дивидендов по акциям STRC? У кого из них больше финансовое давление? Odaily星球日报 проанализирует для читателей.

Bitmine против Strategy: совершенно разные пути удержания активов DAT

В связи с сегодняшним обвалом BTC участники сообщества пошутили с помощью ИИ над тем, как Сэйлор «продвигает» BTC: «Шестидесятилетний старик лично продвигает товар, наследственный BTC по цене всего 62 000 долларов за штуку».

Возвращаясь к Bitmine и Strategy, на данный момент финансовая структура Bitmine выглядит более безопасной; в то время как долговое давление Strategy больше.

Игра Bitmine с выпуском акций: модель DAT без долгового финансирования

По состоянию на 1 июня Bitmine владеет 5 416 901 ETH, что составляет около 4,49% от общего предложения ETH, что близко к «верхнему пределу в 5%», который неоднократно подчеркивал председатель совета директоров Bitmine Том Ли. Вчера Bitmine снова через BitGo увеличила свои резервы на 25 000 ETH, стоимостью на тот момент 48 миллионов долларов. В настоящее время её объём хранения достиг 5 441 901 ETH.

Причина, по которой у Bitmine есть уверенность продолжать наращивать резервы даже при падении рынка, многогранна. Главная причина в том, что источник средств Bitmine — это выпуск акций:

- В июне прошлого года при создании компании DAT для формирования казначейства ETH, Bitmine получила начальный стартовый капитал в размере 250 миллионов долларов, а также небольшое финансирование PIPE.

- После июля прошлого года Bitmine в основном полагалась на выпуск акций через ATM (механизм рыночного предложения), постепенно увеличивая эту сумму с 2 миллиардов до 24,5 миллиардов долларов.

Обилие средств дало Тому Ли достаточную уверенность, и денежные средства на балансе Bitmine также позволяют ей продолжать наращивать резервы — в объявлении компании от 1 июня также упоминалось: Стоимость доли этой компании в Beast Industries составляет 180 миллионов долларов; стоимость доли в Eightco Holdings — 93 миллиона долларов. Общая сумма денежных средств компании составляет 446 миллионов долларов.

Кроме того, Том Ли громко заявлял, что ежедневный доход Bitmine от стейкинга в казначействе Ethereum составляет 1 миллион долларов. Это относится к тому, что Bitmine застейкала около 87% (примерно 4,71 миллиона ETH) своих запасов ETH через свою сеть стейкинга MAVAN с ожидаемой годовой доходностью около 2,73%-3% (примерно 250-300 миллионов долларов), что также может обеспечить относительно стабильный денежный поток.

Подводя итог, финансовое состояние Bitmine хорошее; и, по всей видимости, привлечение 300 миллионов долларов за счет привилегированных акций с последней объявленной годовой дивидендной доходностью 9,5% дополнительно снизит её финансовое давление. Для этой компании главные точки риска заключаются в размытии доли (выпуск новых акций) и дальнейшем падении акций из-за убытков на балансе, если mNVA продолжит быть < 1, это может спровоцировать распродажу акций.

Долговая игра Strategy с плечом: давление конвертируемых облигаций и дивидендов по привилегированным акциям

По сравнению с подходом Bitmine «покупать ETH на деньги инвесторов», финансовая нагрузка Strategy на покупку BTC больше, поскольку она в основном «занимает деньги для увеличения запасов BTC».

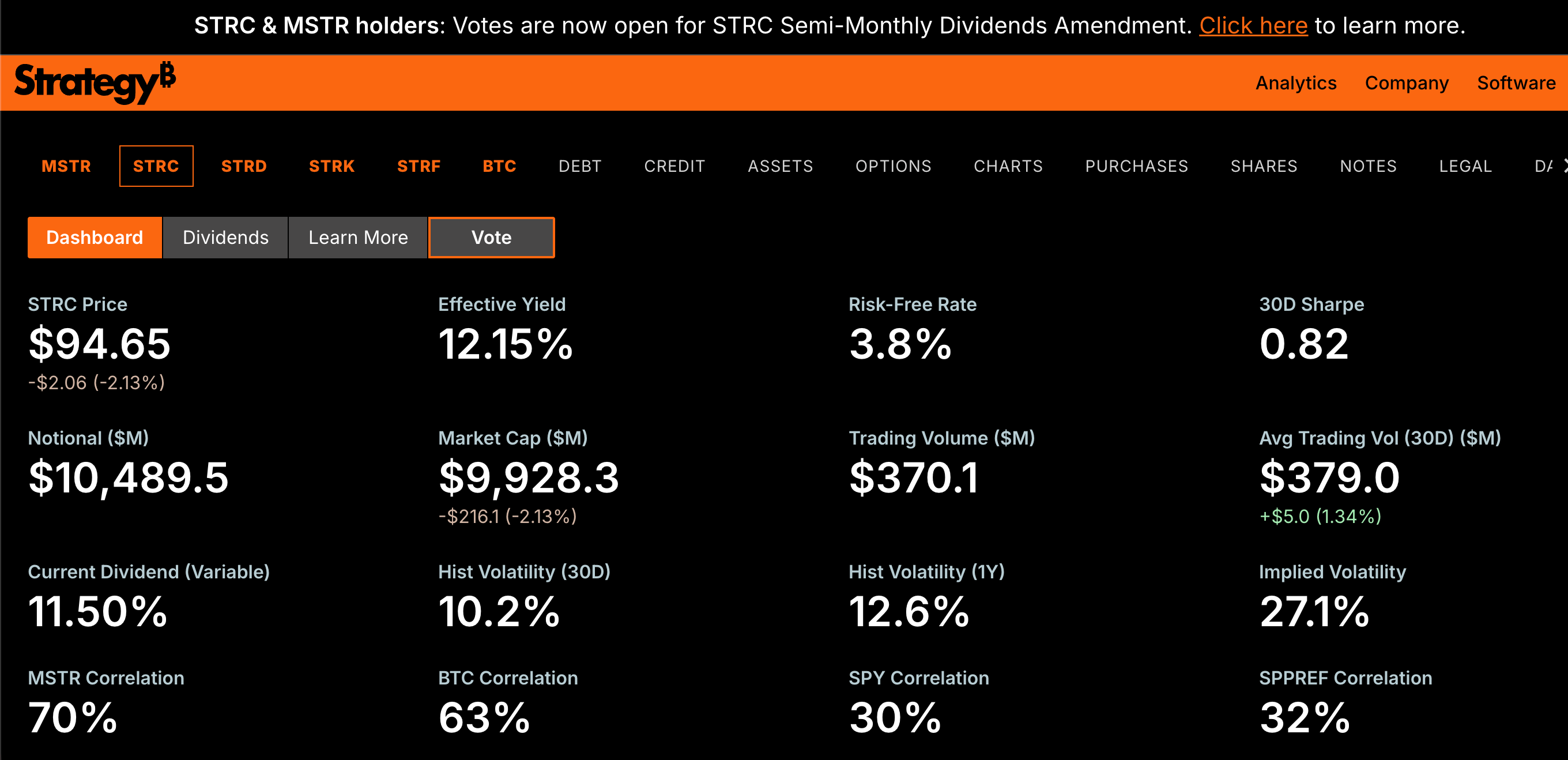

Согласно информации на сайте Strategy, в настоящее время Strategy имеет долг по конвертируемым облигациям на сумму около 6,7 миллиарда долларов плюс привилегированные акции STRC на сумму около 9,9 миллиарда долларов и акции STRD, STRK, STRF разной рыночной капитализации, что требует ежегодных огромных выплат дивидендов и процентов. В конце мая, после выкупа конвертируемого долга на 1,5 миллиарда долларов, денежные резервы Strategy сократились примерно до 871 миллиона долларов, что покрывает её предполагаемые годовые обязательства по выплате дивидендов по привилегированным акциям в размере 1,7 миллиарда долларов лишь примерно на 6 месяцев.

Более того, Strategy ранее инициировала голосование «о предложении увеличить выплату дивидендов по STRC с 1 до 2 раз в месяц», голосование началось 28 апреля и завершится в день собрания 8 июня. Если предложение будет одобрено, первая дата закрытия реестра по новому графику — 30 июня, а первая дата выплаты — 15 июля. Акционеры, имеющие право голоса (два типа акционеров: MSTR и STRC), должны были владеть акциями на 17 апреля.

Кроме того, стоит отметить, что авторизованный лимит выпуска акций STRC составляет примерно 28,3 миллиарда долларов. Возможно, под влиянием продолжающегося падения BTC и потери доверия на рынке, сегодня утром STRC упал ниже 95 долларов и в настоящее время торгуется около 94,65 долларов, «отклонившись» более чем на 5% от целевой цены в 100 долларов.

По сравнению с Bitmine, Strategy в настоящее время сталкивается с проблемой огромного разрыва между высокой суммой привлечения средств через привилегированные акции и выплатой дивидендов, усугубляемой продолжающимся падением BTC, и, в отличие от ETH, у которого есть возможность стейкинга для получения дополнительной ликвидности, у BTC нет доступной экосистемы стейкинга.

Поэтому после продажи Strategy в прошлом месяце 32 BTC, рынок начал сомневаться в идентичности «Strategy — алмазные руки, которые только покупают и не продают». При продолжающемся падении BTC, Strategy может столкнуться с серией кризисов ликвидности, что приведёт к невозможности выплаты долгов и дивидендов, и, как следствие, к дальнейшей продаже BTC и обвалу рынка. По сути, Strategy играет в «игру с высоким долговым плечом, делая ставку на то, что цена BTC не упадёт до определённого уровня».

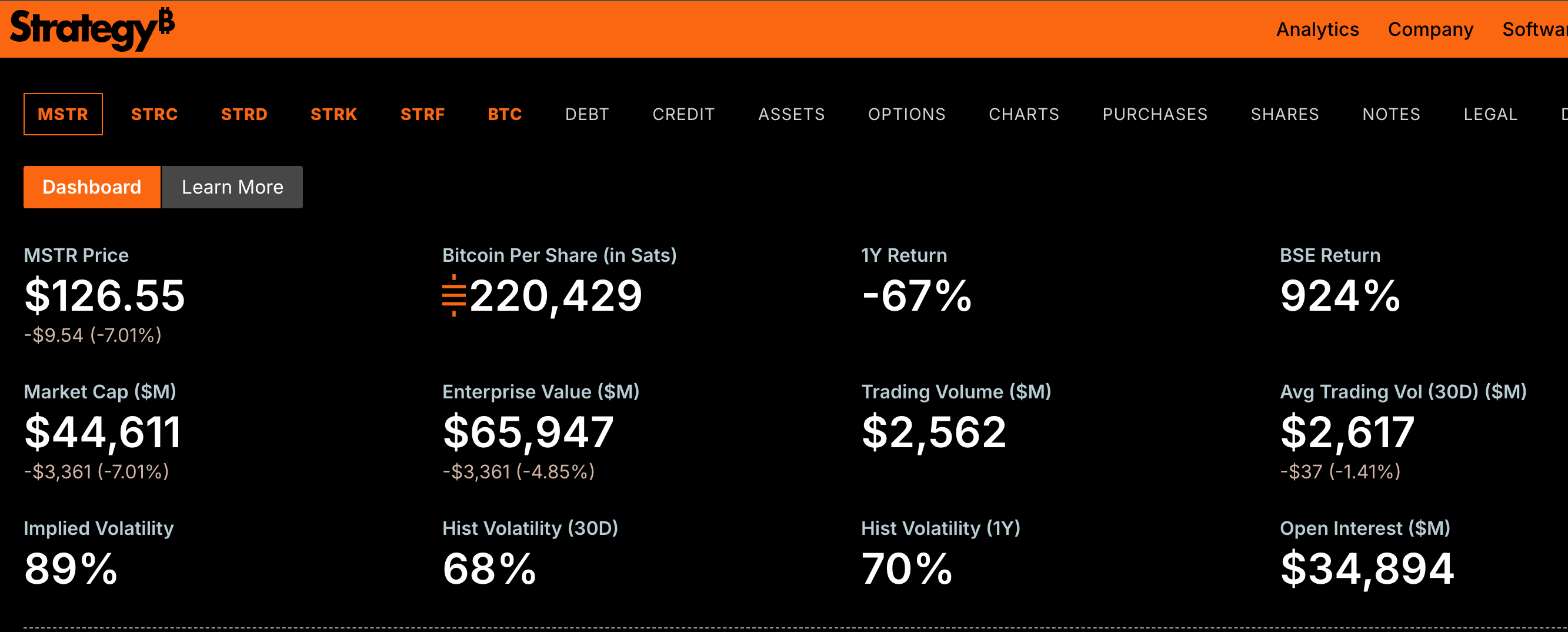

Таким образом, учитывая текущее значение mNAV Strategy в 0,83, рынок всё ещё сильно сомневается в последующих показателях её акций. Вчера её рыночная капитализация уже выпала из топ-200 американских компаний. В настоящее время акции Strategy (MSTR) торгуются около 126 долларов, снизившись на 7% за 24 часа; рыночная капитализация составляет около 44,6 миллиарда долларов.

Конечно, будучи ведущей компанией с казначейством DAT, председатель Bitmine Том Ли по-прежнему весьма оптимистично оценивает Strategy, ранее заявив: «Продажа биткоинов Strategy и отток из ETF — это типичное поведение при формировании дна, а не сигнал риска». А на недавней конференции «Proof of Talk 2026» в парижском Лувре Том Ли сделал смелое заявление: «Поскольку искусственный интеллект и токенизация стимулируют масштабные изменения финансовой инфраструктуры, ETH в конечном итоге может достичь 250 000 долларов». Однако, говоря о «действиях Bitmine после достижения её долей в 5% от общего количества ETH», он также выразил осторожность в отношении дальнейшего наращивания резервов ETH. (Подробнее см. в статье «Том Ли подкрепляет веру: криптовалютная весна наступила, ETH вырастет до 250 000 долларов»).

На данный момент рыночная ситуация Bitmine и Strategy очень похожа, но финансовое состояние Bitmine немного лучше; Strategy же стоит перед выбором между «продажей большего количества BTC для получения денежных средств на выплату дивидендов» и «бездействием при продолжающемся падении BTC с дальнейшим увеличением долга для наращивания резервов или просто сохранением текущей позиции».