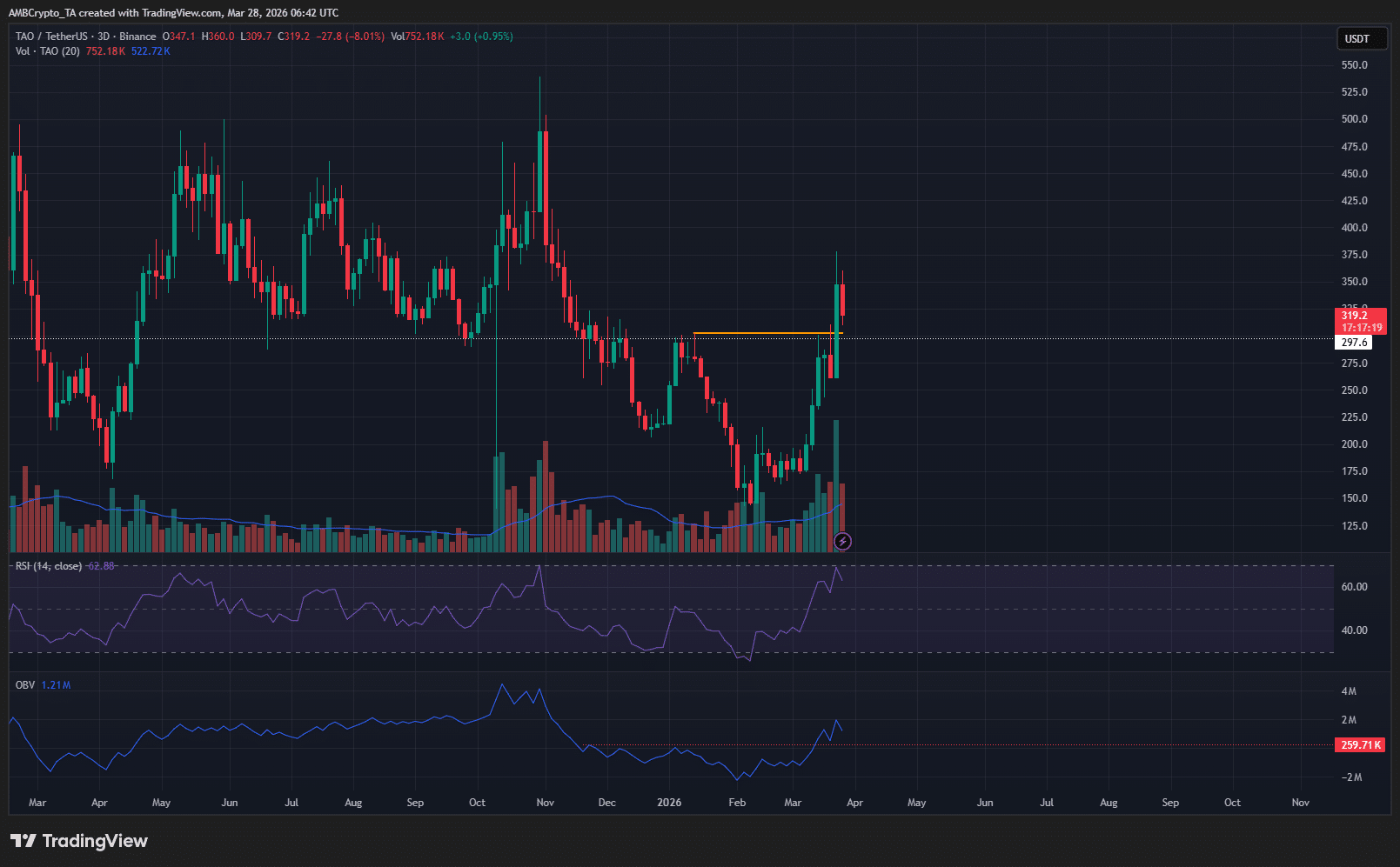

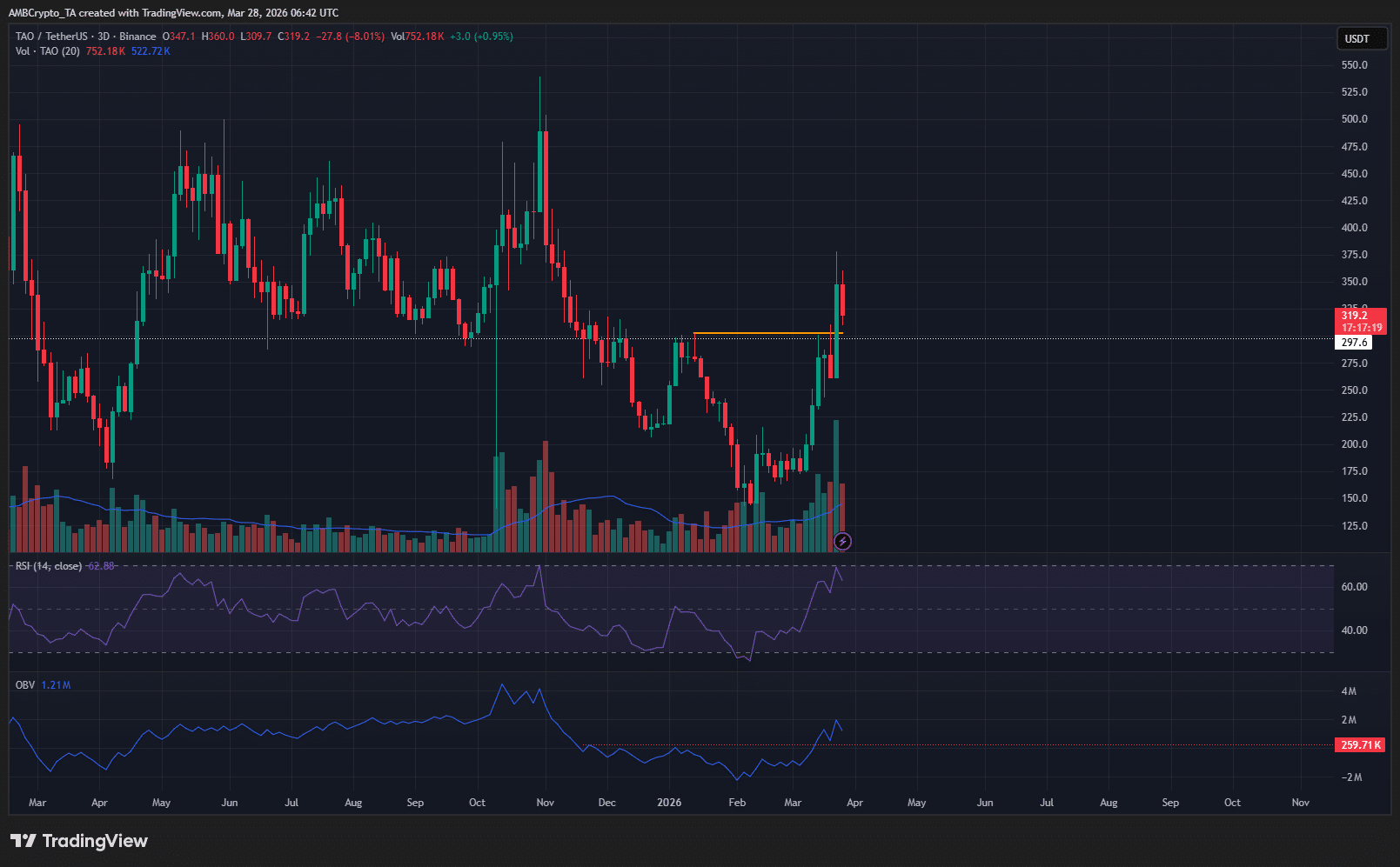

Bittensor [TAO] продолжил торговаться выше психологического уровня в $300. В то время как лидеры рынка Bitcoin [BTC] и Ethereum [ETH] столкнулись с сильным давлением продаж на прошлой неделе и были вынуждены зафиксировать потери, TAO продолжил восходящий тренд.

Таким образом, уровень в $300 был важным уровнем поддержки, за которым следует внимательно следить свинг-трейдерам. Является ли устойчивый восходящий тренд еще одной возможностью для покупки трейдеров TAO, или им следует фиксировать прибыль и ожидать глубокой коррекции в дальнейшем?

Бычья свинг-структура TAO подтверждает направление тренда

Превышение отметки в $302.4 на прошлой неделе ознаменовало бычий сдвиг свинг-структуры для TAO на 3-дневном графике. В то же время, индикатор OBV (On-Balance Volume) обновлял локальные максимумы, а психологическое сопротивление круглого числа было преодолено.

Эти события были примечательны, особенно учитывая, что Bitcoin и многие альткойны были вынуждены снижаться или торговаться в боковом тренде. Относительная сила AI-токена, вероятно, объясняется спросом на децентрализованную инфраструктуру искусственного интеллекта.

Откат к $300 стал бы возможностью для покупки для трейдеров и инвесторов Bittensor. Их следующими целями были бы уровни в $450-$500.

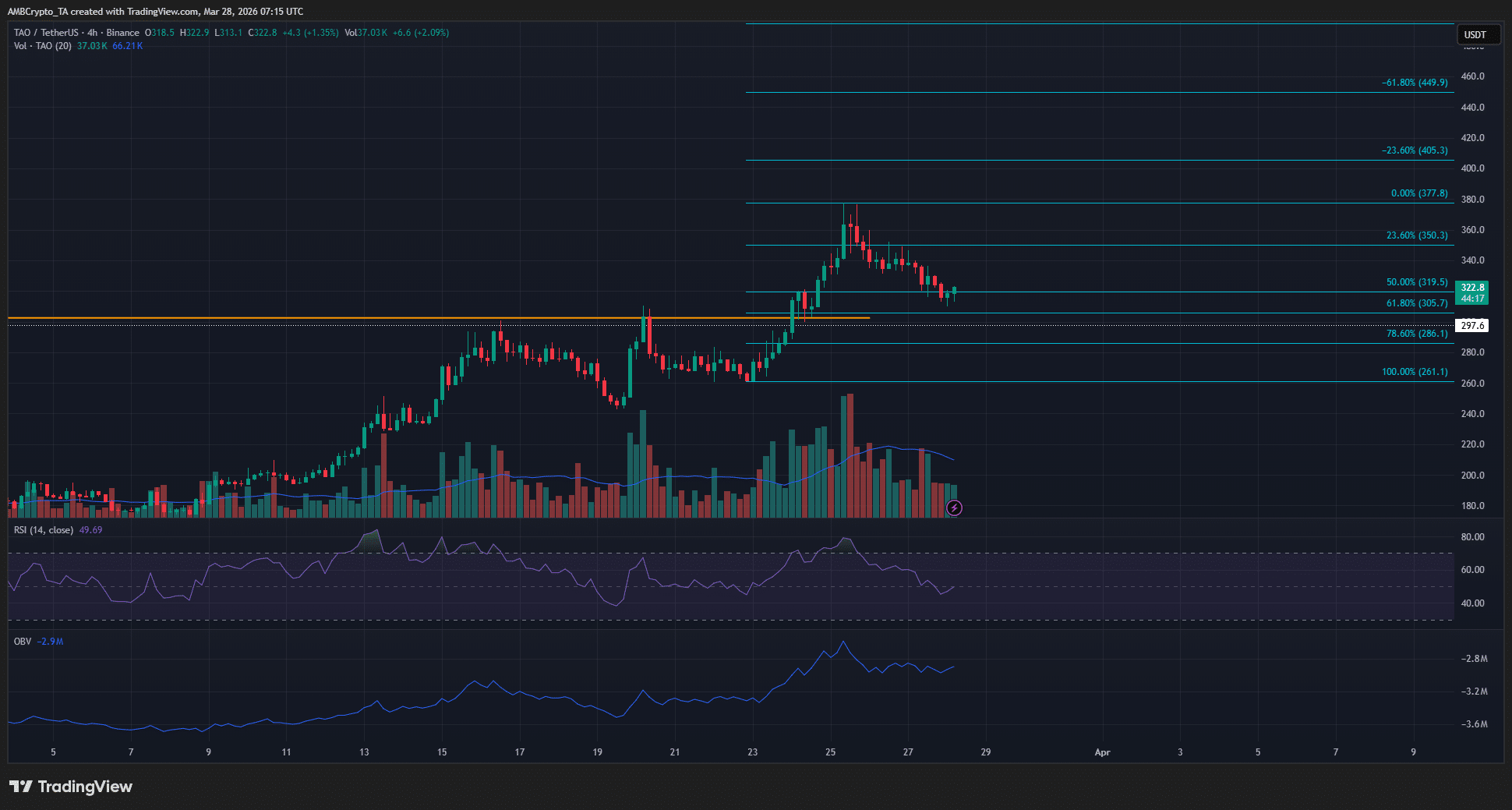

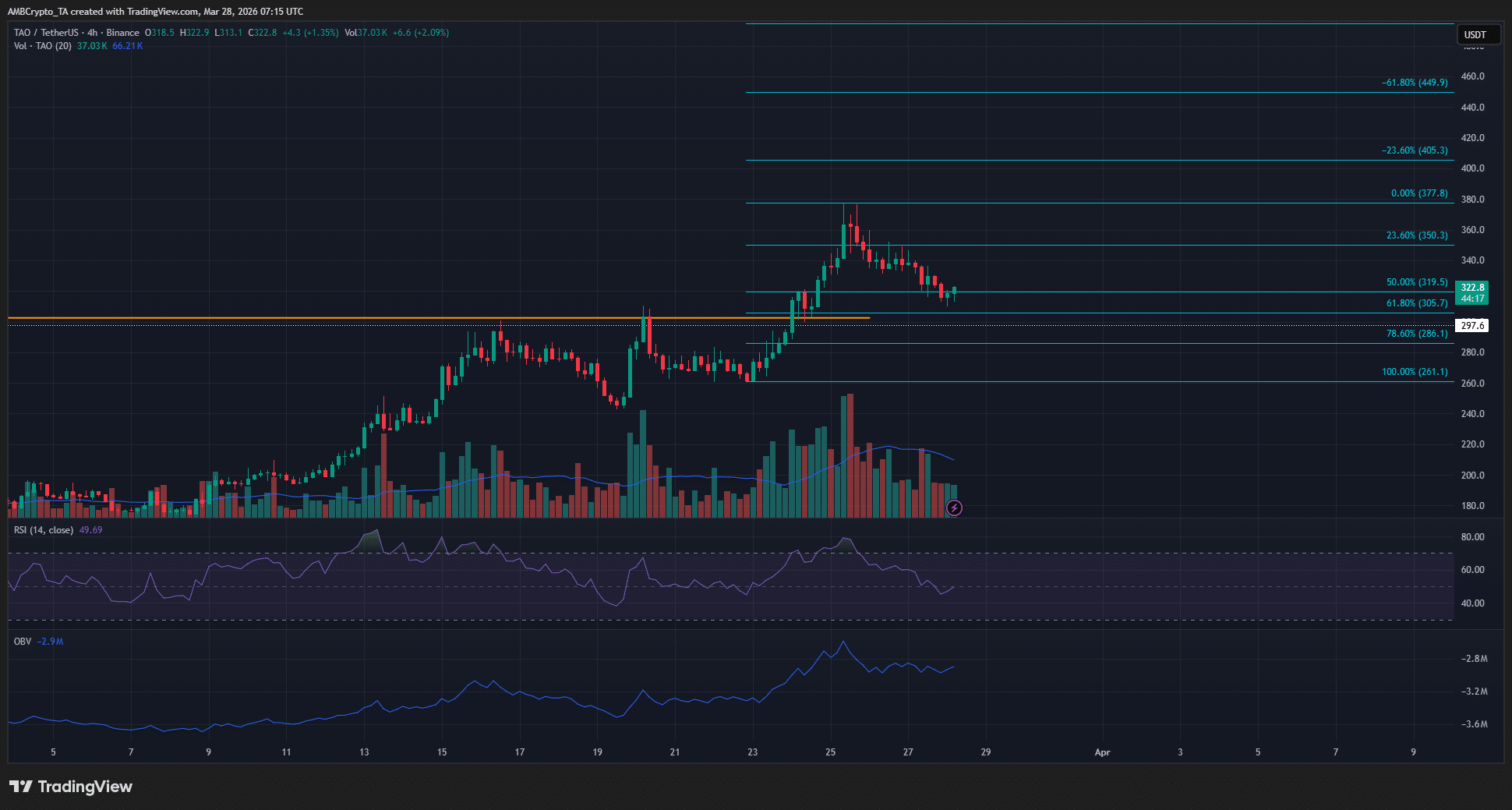

Почему трейдерам стоит покупать сейчас

4-часовой график выглядел довольно обнадеживающе. На этом таймфрейме ценовая структура была явно бычьей. Технические индикаторы также поддерживали восходящий импульс и отражали стабильное давление покупателей на альткойн.

Уровни Фибоначчи (голубые) показали, что коррекция происходит. Зона в $286-$305 была бы идеальной для покупки, но неясно, получим ли мы это снижение.

Трейдеры могут рассматривать возможность покупки в любом месте области $286-$319, поскольку многие трейдеры и аналитики также считают 50%-ную коррекцию ключевой поддержкой при восходящем тренде. В любом из сценариев, следующими целями будут уровни $405 и $449.

Падение ниже отметки в $261.1 сместит структуру на H4 в медвежью сторону и аннулирует бычью setup, изложенную выше.

Итоговое резюме

- Bittensor продолжил торговаться выше уровня в $300, несмотря на коррекцию на криптовалютном рынке за последние два дня.

- Эта демонстрация относительной силы может привести к очередному восходящему тренду на следующей неделе, где следующими целями будут $409 и $450.