Автор: Nick Prince

Компиляция: TechFlow

Введение TechFlow: ИИ-агент самостоятельно выполнил работу, на которую команде инвестиционных аналитиков потребовались бы дни: прочитал 226-мегабайтный файл SpaceX S-1, купил данные реального рынка за USDC в сети Base, сгенерировал памятку для инвестиционного комитета, содержащую многосторонние аргументы, модель оценки и матрицу рисков. Весь процесс стоил всего 1,87 доллара США. Это не демо-версия, а реальные записи платных вызовов API. Когда ИИ-агент может сам платить за данные и самостоятельно принимать решения по пути анализа, способ работы на Уолл-стрит перестраивается.

ИИ-агент прочитал представленный в понедельник 226-мегабайтный файл SpaceX S-1, купил данные реального рынка за USDC в сети Base, а затем за 12 минут сгенерировал эту памятку для инвестиционного комитета. Общая стоимость: 6 платных вызовов API, 1,87 доллара USDC, без API-ключей.

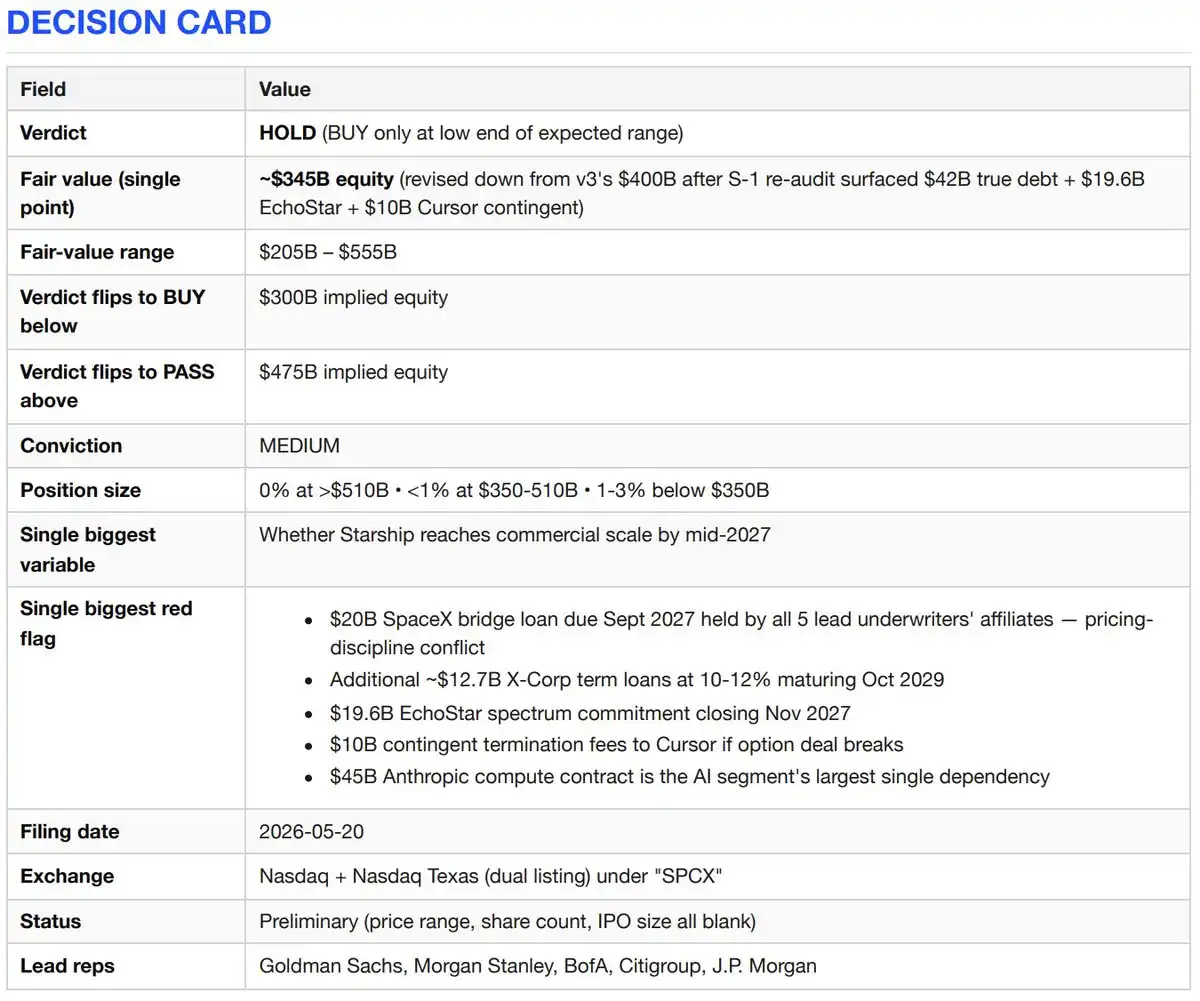

Карта решений (вывод = воздержаться от действий)

Аргументы "за"

SpaceX обладает тремя видами бизнеса, которые не могут быть воспроизведены конкурентами. Первое — это почти монопольное положение на рынке коммерческих космических запусков — с 2023 года на его долю приходится 80% глобальной массы, выведенной на орбиту, успешность миссий Falcon составляет 99%, а технология многоразового использования опережает конкурентов на 10 лет. Второе — единственная в мире развернутая сеть широкополосной связи на низкой околоземной орбите — Starlink имеет 10,3 миллиона подписчиков в 164 странах, рост на 49,8% в годовом исчислении, скорректированный EBITDA сегмента составляет 7,2 миллиарда долларов. Третье — с приобретением xAI в феврале 2026 года стала единственной вертикально интегрированной лабораторией искусственного интеллекта, интегрированной на уровне ракет-носителей, и в будущем планирует развернуть орбитальные вычислительные мощности. Независимо от того, какой разумный метод оценки используется, это актив поколения.

Аргументы "против"

Бизнес Connectivity является реальным и прибыльным. Но все остальное либо сжигает деньги с потрясающей скоростью — подразделение ИИ в 2025 году при доходе в 3,2 миллиарда долларов понесло убытки в 6,4 миллиарда долларов — либо ставится на Starship, который завершил 11 летных испытаний, но еще не вывел полезную нагрузку на орбиту. Это IPO отчасти является событием рефинансирования. SpaceX взяла 20 миллиардов долларов бридж-кредита для приобретения xAI, срок погашения — сентябрь 2027 года, а кредитором этого бридж-кредита являются андеррайтеры текущего IPO. Если оценка превысит 500 миллиардов долларов, вы платите за еще не реализованную исполнительную способность, корпоративное управление, которое вы не имеете права обсуждать, и за сделку по рефинансированию, в успехе которой андеррайтеры обязаны быть заинтересованы.

Инвестиционный тезис

Starlink — это превосходный самостоятельный бизнес. Выручка в 2025 году составила 11,4 миллиарда долларов (+49,8%), операционная прибыль — 4,4 миллиарда долларов (+120%), скорректированный EBITDA сегмента — 7,2 миллиарда долларов (+86%). Дорогие подписные услуги, 10,3 миллиона платных пользователей.

Запуски уникальны. С 2023 года на его долю приходится более 80% глобальной массы, выведенной на орбиту, успешность Falcon превышает 99%, первая ступень Falcon 9 летала до 34 раз.

Вертикальная интеграция реальна и создает кумулятивный эффект. Ракеты → спутники → частотный спектр (сделка EchoStar AWS-4/H диапазона уже одобрена FCC) → вычислительные мощности ИИ (два кластера COLOSSUS около 1 ГВт).

Зависимость правительства — это ров, а не риск. Ключевой поставщик запусков для национальной безопасности США: в 2025 году выполнил 11 из 12 миссий по запускам для национальной безопасности в космосе, все 5 пилотируемых и грузовых полетов NASA.

Стоимость опциона на орбитальные вычислительные мощности ИИ, планируется развернуть в 2028 году. Если Starship достигнет даже 50% заявленной экономической эффективности — снижение стоимости запусков на 99% — доступный рынок расширится на порядок.

Контраргументы

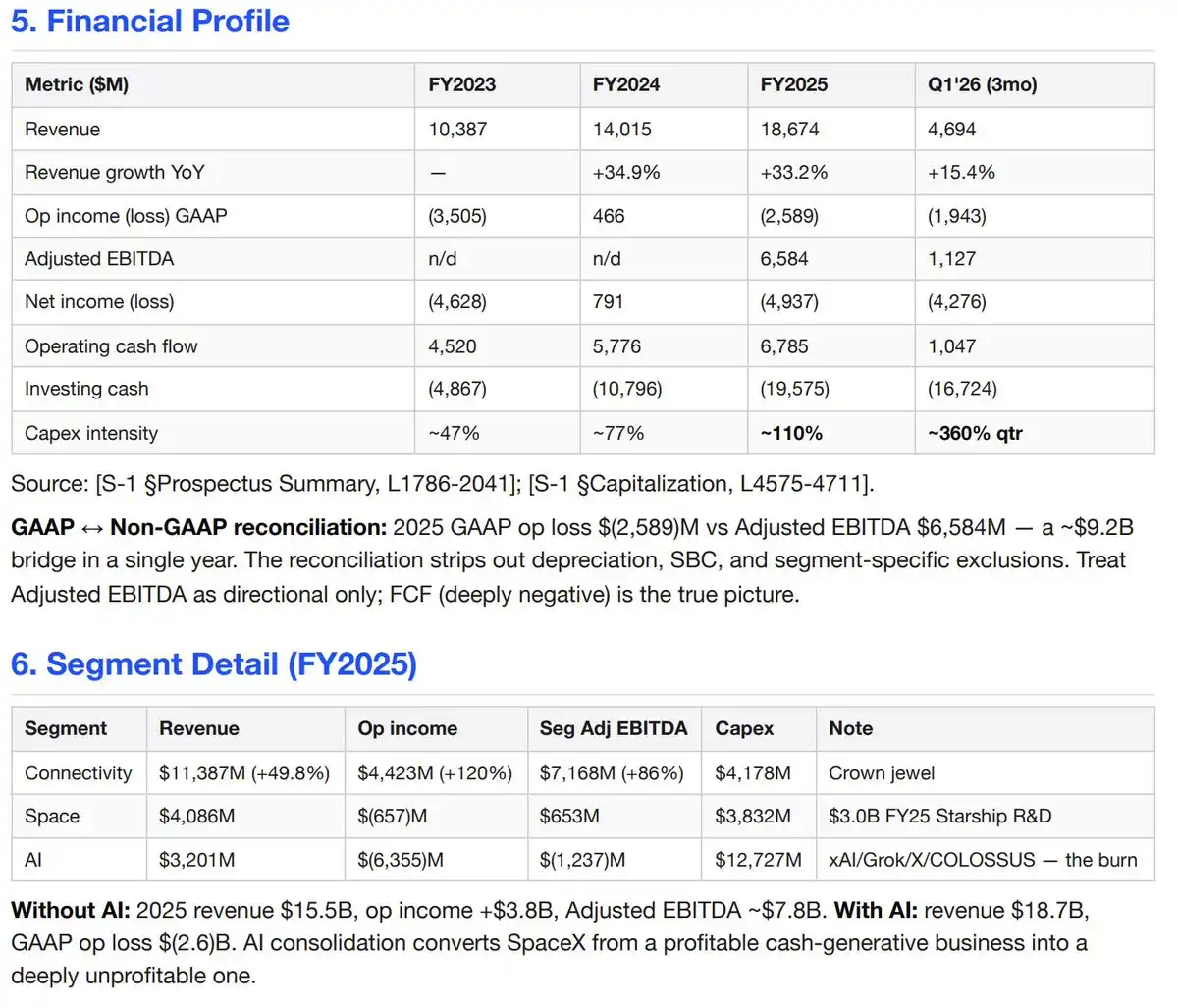

Подразделение ИИ — это бездонная яма, ежегодно сжигающая более 6 миллиардов долларов. 2025 год: выручка 3,2 миллиарда долларов против операционных убытков в 6,4 миллиарда долларов, скорректированный EBITDA сегмента отрицательный 1,2 миллиарда долларов, капитальные затраты 12,7 миллиарда долларов. Только первый квартал 2026 года: выручка 818 миллионов долларов против операционных убытков в 2,5 миллиарда долларов, капитальные затраты 7,7 миллиарда долларов. Годовые капитальные затраты на ИИ теперь превышают 30 миллиардов долларов, в то время как выручка от ИИ составляет всего 3,2 миллиарда долларов.

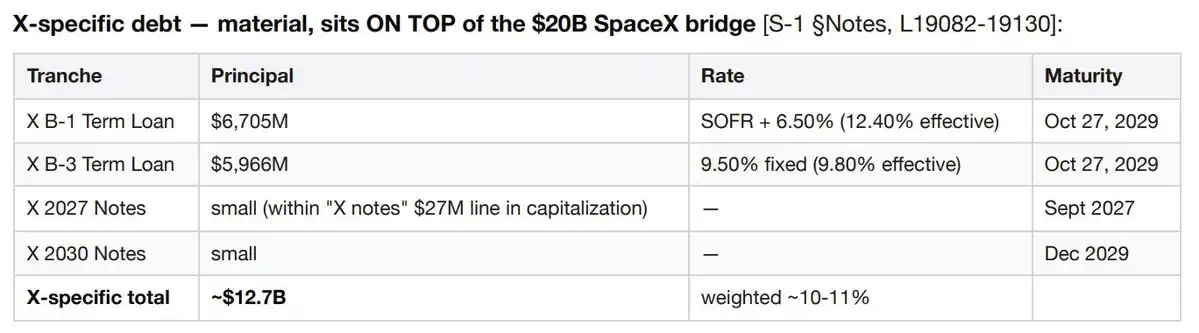

Реальный размер долга составляет около 42 миллиардов долларов, а не 29 миллиардов долларов, указанных в заголовке. Состав: около 20 миллиардов долларов бридж-кредита SpaceX (срок погашения сентябрь 2027 года), около 6,7 миллиарда долларов синдицированного кредита B-1 компании X и около 6 миллиардов долларов синдицированного кредита B-3 компании X (оба со сроком погашения в октябре 2029 года, эффективная ставка 10-12%), а также около 9,1 миллиарда долларов "прочего финансирования", включая обязательства, возникшие в результате неудачной продажи с обратной арендой инфраструктуры ИИ. Только кредиты, связанные с X, ежегодно генерируют процентные расходы примерно в 1,2-1,3 миллиарда долларов, которые учитываются в подразделении ИИ.

Обязательство по сделке со спектром EchoStar на 19,6 миллиарда долларов должно быть завершено в ноябре 2027 года. Цена в виде акций и наличных в обмен на 65 МГц американского спектра и лицензии на глобальную подвижную спутниковую связь. Это обязательное капитальное обязательство в дополнение к бридж-кредиту и капитальным затратам 2026 финансового года.

Опционное соглашение с Cursor может привести к выплате неустойки до 10 миллиардов долларов. SpaceX в апреле 2026 года — за месяц до подачи этого документа S-1 — заключила с Anysphere (Cursor) соглашение о вычислительных мощностях и опционах, подразумевающее оценку Cursor в 60 миллиардов долларов. Если любая сторона расторгнет соглашение, SpaceX должна будет выплатить Cursor 1,5 миллиарда долларов неустойки плюс 8,5 миллиарда долларов отсроченных плат за услуги, наличными или акциями класса А.

Контракт с Anthropic на 45 миллиардов долларов является крупнейшим единственным внешним источником дохода подразделения ИИ. Соглашение об облачных услугах, подписанное в мае 2026 года, предусматривает ежемесячные платежи Anthropic в размере 1,25 миллиарда долларов до мая 2029 года. SpaceX продает свои вычислительные мощности COLOSSUS компании-разработчику передовых моделей, являющейся прямым конкурентом, что создает крайнюю концентрацию контрагентского риска.

На балансе признан резерв на судебные разбирательства в размере 530 миллионов долларов для коллективного иска о генерации изображений Grok — дело Jane Doe против X.AI Corp (январь 2026), дело Jane Doe 1 (март) и дело Baltimore (март). Истцы требуют компенсационного, установленного законом и штрафного ущерба. В S-1 четко указано, что диапазон дополнительных убытков невозможно оценить.

Темп роста выручки в первом квартале 2026 года замедлился до 15,4% (4,69 миллиарда долларов против 4,07 миллиарда долларов в годовом исчислении), что ниже уровня за весь 2025 год в 33,2%.

SpaceX станет контролируемой компанией с четырьмя классами акций. Маск будет обладать большинством голосов после IPO. Компания будет полагаться на исключения для контролируемых компаний Nasdaq, освобождающие от требований независимого комитета по вознаграждениям и независимого комитета по назначениям.

Скорректированный EBITDA улучшает показатели примерно на 9 миллиардов долларов. Управленческая цифра в заголовке за 2025 год составляет 6,6 миллиарда долларов "скорректированного EBITDA", в то время как операционный убыток по GAAP составил отрицательные 2,6 миллиарда долларов. Корректировки исключают амортизацию, акционерные компенсации и исключения, специфичные для сегментов.

Профиль компании

SpaceX (Space Exploration Technologies Corp.; SEC CIK 0001181412) проектирует и эксплуатирует многоразовые ракеты, крупнейшую в мире группировку спутников на НОО (около 9600 широкополосных спутников плюс около 650 спутников прямой связи с мобильными телефонами), а также — после приобретения xAI в феврале 2026 года — гигаваттную инфраструктуру для обучения ИИ. Три отчетных сегмента: Космос, Связь (10,3 миллиона подписчиков Starlink) и ИИ (модель Grok, социальная платформа X с 550 миллионами ежемесячных активных пользователей, а также вычислительные кластеры COLOSSUS/COLOSSUS II). Выручка за 2025 год: 18,7 миллиарда долларов; операционный убыток по GAAP: отрицательные 2,6 миллиарда долларов; денежные средства в наличии: 15,85 миллиарда долларов против долгосрочного долга в 29,1 миллиарда долларов, указанного на обложке таблицы капитализации.

X (социальная платформа) — это бизнес-единица, а не сноска

Цепочка корпоративных событий заслуживает повторного рассмотрения. SpaceX приобрела xAI в феврале 2026 года. xAI приобрела X Holdings в марте 2025 года. X Holdings приобрела Twitter в октябре 2022 года. Результат: Twitter/X теперь включен в подразделение ИИ SpaceX, имеет собственные статьи баланса, собственные судебные разбирательства и собственную структуру долга.

Масштаб. За последние 12 месяцев поддерживалось 1,3 миллиарда аккаунтов, 550 миллионов ежемесячных активных пользователей (выше, чем 520 миллионов в декабре 2025 года), 350 миллионов постов в день. Из этих ежемесячных активных пользователей 117 миллионов используют функцию Grok — X является основным каналом распространения этой модели. Продукт Money (платежи, банкинг, финансовые услуги) был запущен в бета-версии в ноябре 2025 года и продвигается к полной доступности. X Ads Manager начал поэтапный запуск в апреле 2026 года.

Финансовый вклад. Выручка подразделения ИИ в 2023-2024 годах почти полностью поступала от X — реклама, подписки X Premium и лицензирование данных. Только в 2024 году рекламная выручка снизилась на 595 миллионов долларов из-за "потери X рекламных партнеров", что частично компенсировалось увеличением выручки от подписок X Premium на 157 миллионов долларов и увеличением лицензирования данных на 90 миллионов долларов.

Добавив 20 миллиардов долларов бридж-кредита SpaceX (сентябрь 2027 года) и 9,1 миллиарда долларов статьи "прочее финансирование", общий долгосрочный долг составляет около 42 миллиардов долларов — а не 29 миллиардов долларов, указанных в заголовке на обложке капитализации.

Специфические риски X, отсутствующие в других бизнесах SpaceX. Правоприменение Регламента ЕС о цифровых услугах (DSA) к очень крупным онлайн-платформам. Возможность отмены краткосрочных рекламных контрактов с обратимостью безопасности бренда рекламодателей — массовый исход 2024 года может повториться в рамках одного новостного цикла. Продукт Money запускает регулирование платежей/денежных переводов/банковской деятельности во всех 50 штатах США и в каждой зарубежной юрисдикции. Изменение политики модерации контента может одновременно вызвать приостановку рекламодателей и миграцию пользователей.

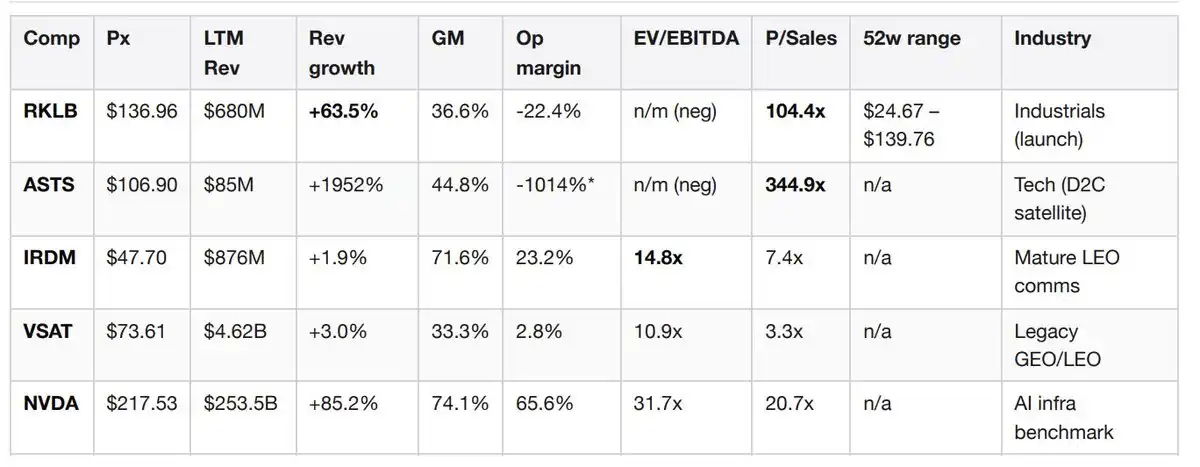

Положение на рынке — данные сравнения в реальном времени

Эта сравнительная таблица была собрана в реальном времени в процессе анализа путем оплаты 0,10 доллара США за пакетные фундаментальные данные по всем пяти компаниям, сравнимым с анализируемой, через конечную точку GraphQL Jintel. Не требуется терминал Bloomberg, не требуется контракт FactSet.

Операционная маржа ASTS отражает масштабные инвестиции до поступления выручки. Источник: получено через x402 на Base из Jintel entitiesByTickers, дата получения 2026-05-22.

Интерпретация группы сравнения. Коэффициент цена/выручка Rocket Lab в 104 раза является ближайшим нарративным аналогом — инвесторы готовы платить чрезвычайно высокую кратность за масштабируемые многоразовые запуски плюс опционную стоимость НОО, даже при отрицательной марже. SpaceX заслуживает более высокой кратности, чем RKLB, но слепое применение коэффициента 104 к выручке только бизнеса Connectivity SpaceX в 11,4 миллиарда долларов подразумевает капитализацию в 1,2 триллиона долларов, что не может быть привязано ни к чему. Коэффициент AST SpaceMobile в 345 раз — это чисто нарративная оценка до поступления выручки, служащая только ориентиром для верхней границы опционной стоимости прямой связи с мобильными телефонами. Коэффициент Iridium 7,4x к выручке и 14,8x к EBITDA представляют собой пример зрелой прибыльной связи на НОО — применение коэффициента 7,4 к 11,4 миллиарда долларов Starlink дает оценку независимого бизнеса Starlink в 84 миллиарда долларов (якорная точка для аргументов "против"). Коэффициент NVIDIA 31,7x EV/EBITDA соответствует росту выручки на 85% — это уровень, до которого необходимо вырасти подразделению ИИ, чтобы оправдать оценку, основанную на фундаментальных показателях. Сейчас до этого еще далеко.

Примечательный сигнал. Rocket Lab 20 мая 2026 года подала поправку 424B5 к проспекту эмиссии — в тот же день, когда SpaceX опубликовала S-1. RKLB проводит вторичное размещение акций в новостном цикле SpaceX, что указывает на то, что руководство считает окно IPO открытым и давление конкурентного предложения неизбежным.

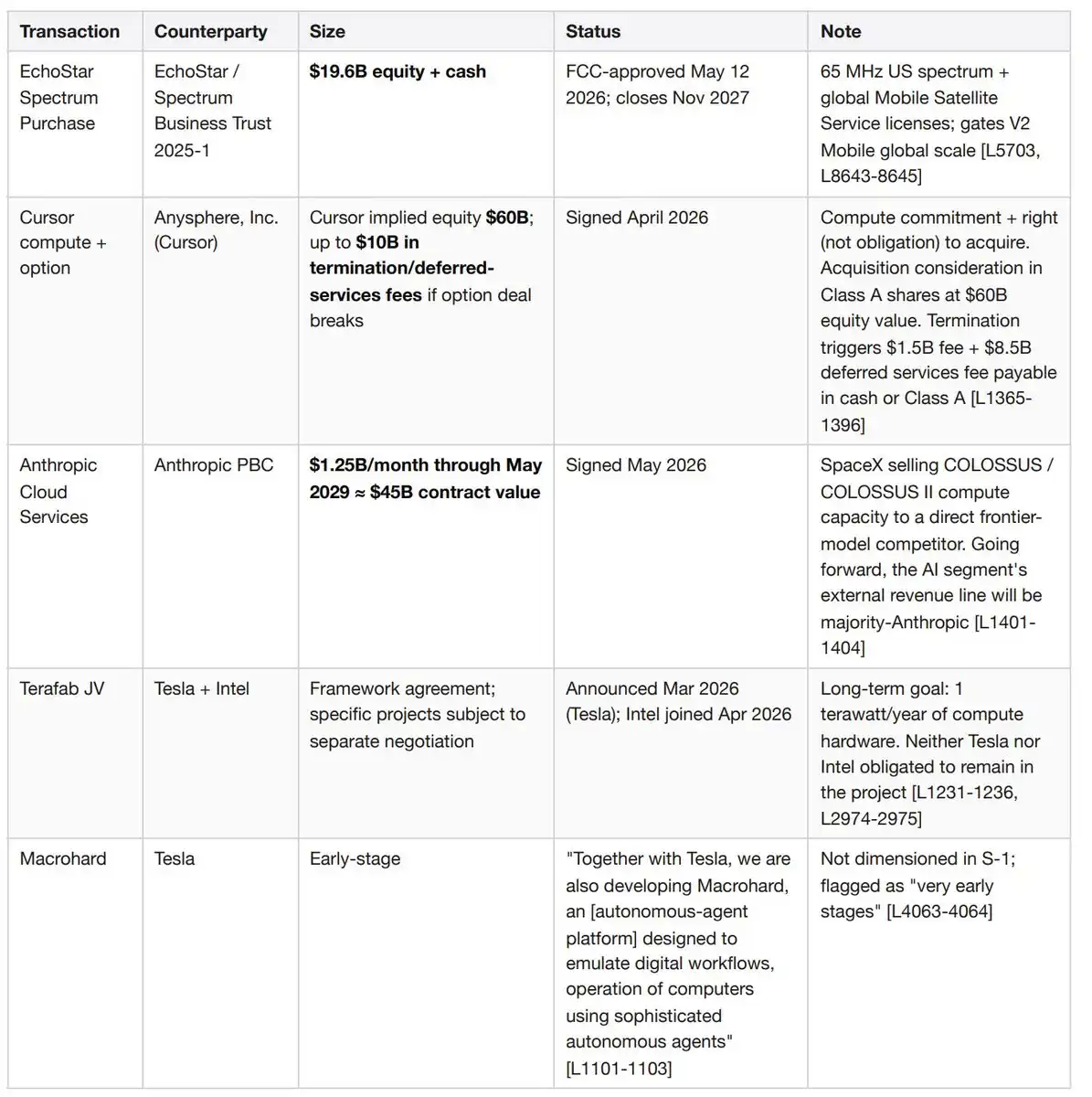

Ожидающие завершения крупные сделки и условные обязательства

Каждая из этих четырех сделок является существенной и они накладываются друг на друга. Две из них были подписаны в течение 60 дней до подачи этого документа S-1.

Почему это важно для оценки. Четкая перспектива "скорректированных чистых обязательств" такова: общий долг 42 миллиарда долларов плюс обязательство EchoStar 19,6 миллиарда долларов плюс условные обязательства перед Cursor до 10 миллиардов долларов, минус 15,85 миллиарда долларов наличных средств в наличии, равняется примерно 55 миллиардам долларов чистых обязательств, и это еще без учета любых средств, привлеченных в ходе IPO. Это в три-четыре раза больше, чем цифры, полученные при простом прочтении обложки капитализации, что существенно меняет сценарий аргументов "против".

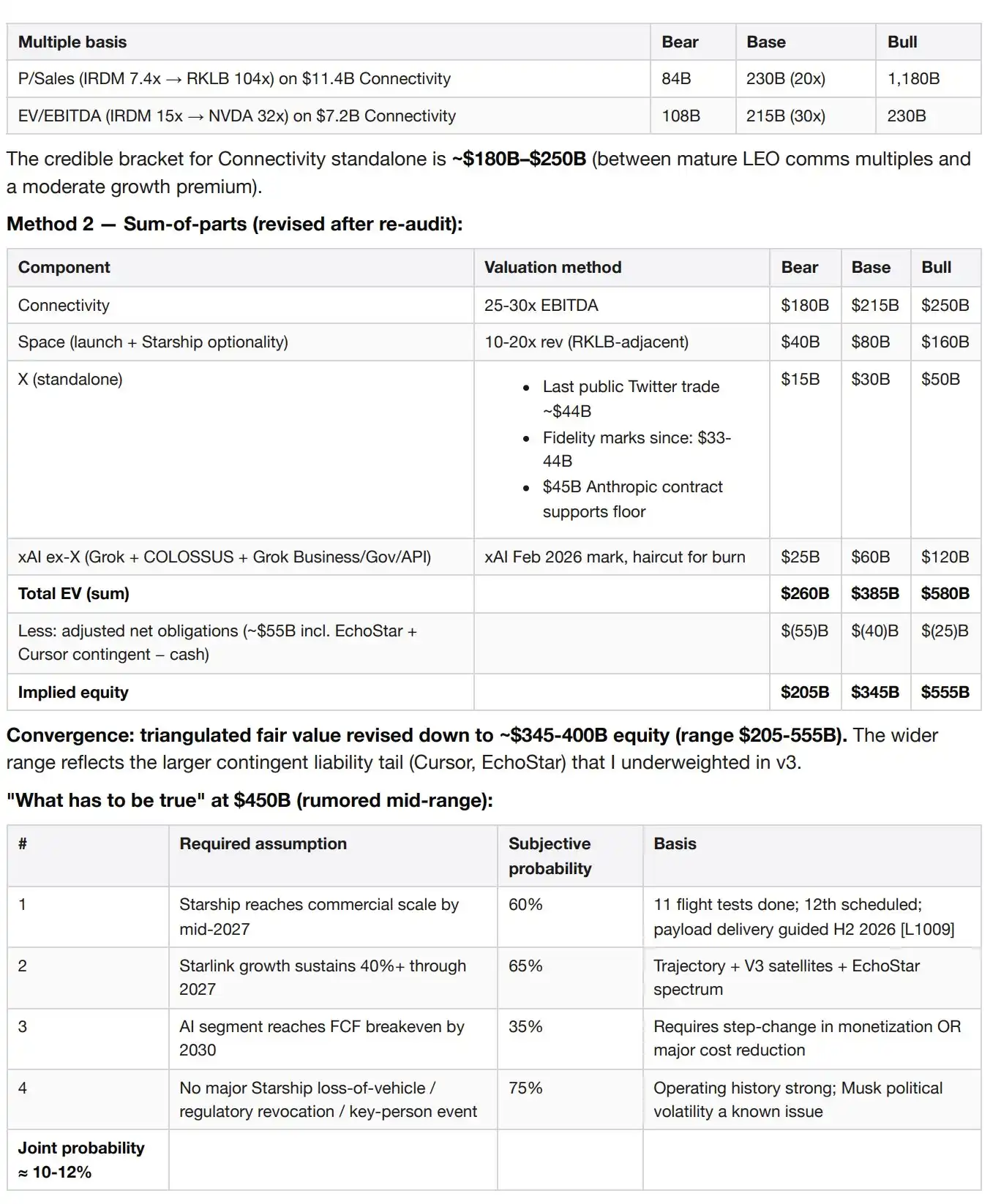

Оценка

Метод 1 — на основе кратных показателей независимых сделок сегмента Connectivity, поскольку это единственный сегмент с положительной независимой экономикой.

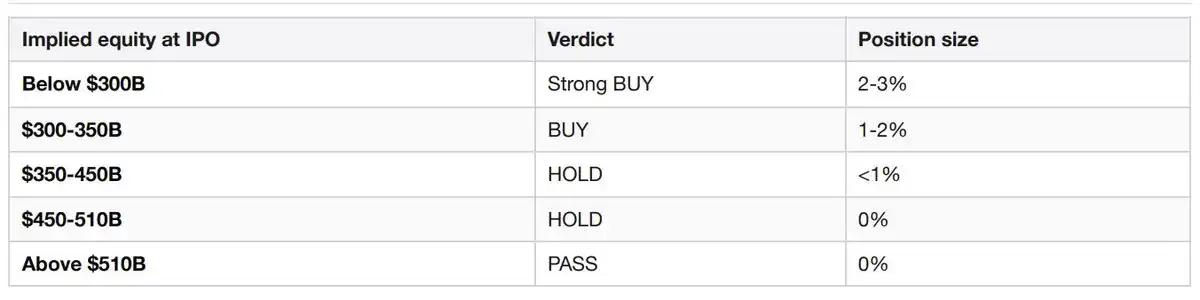

Лестница размера позиции

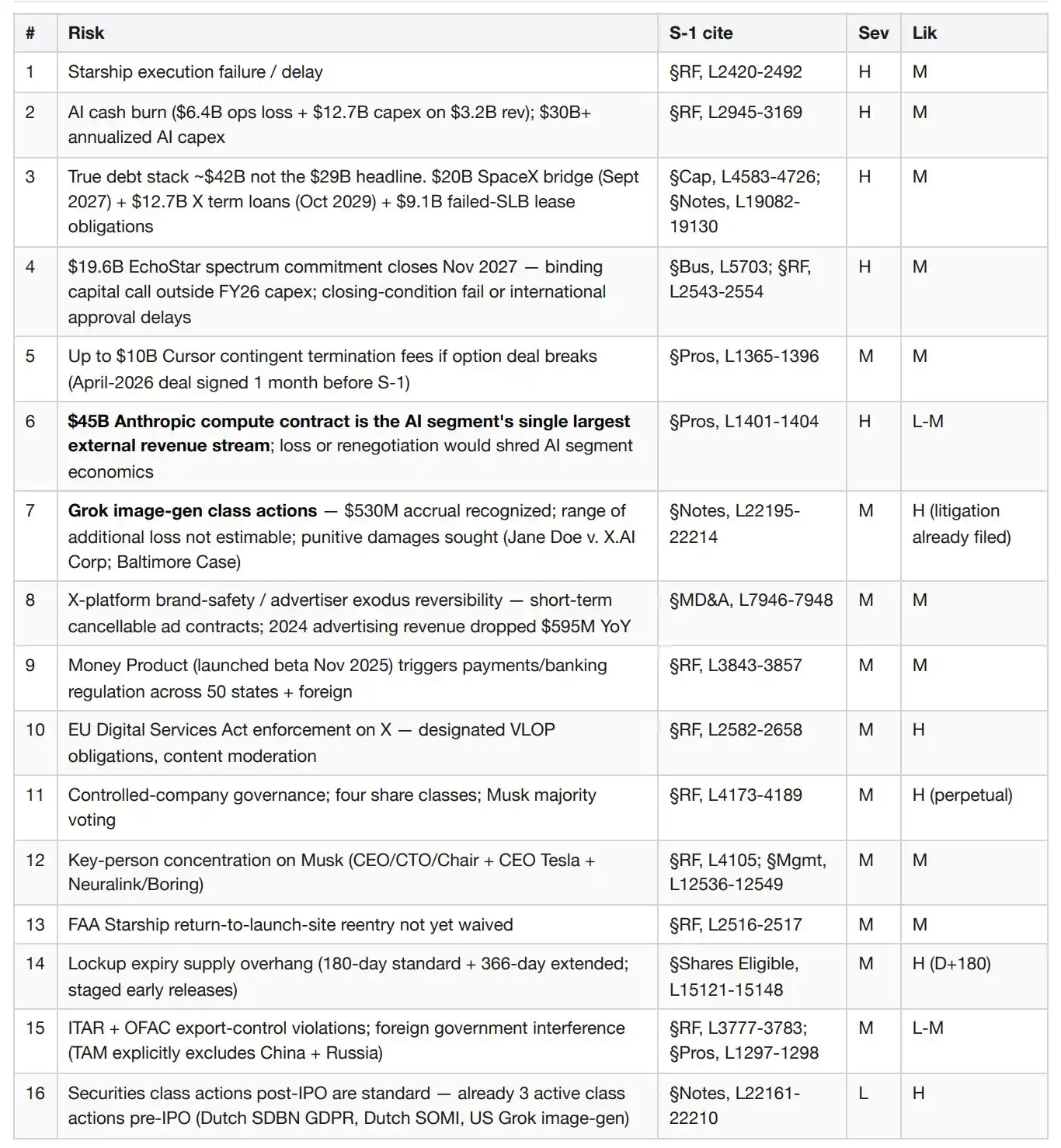

Ключевые риски (серьезность × вероятность)

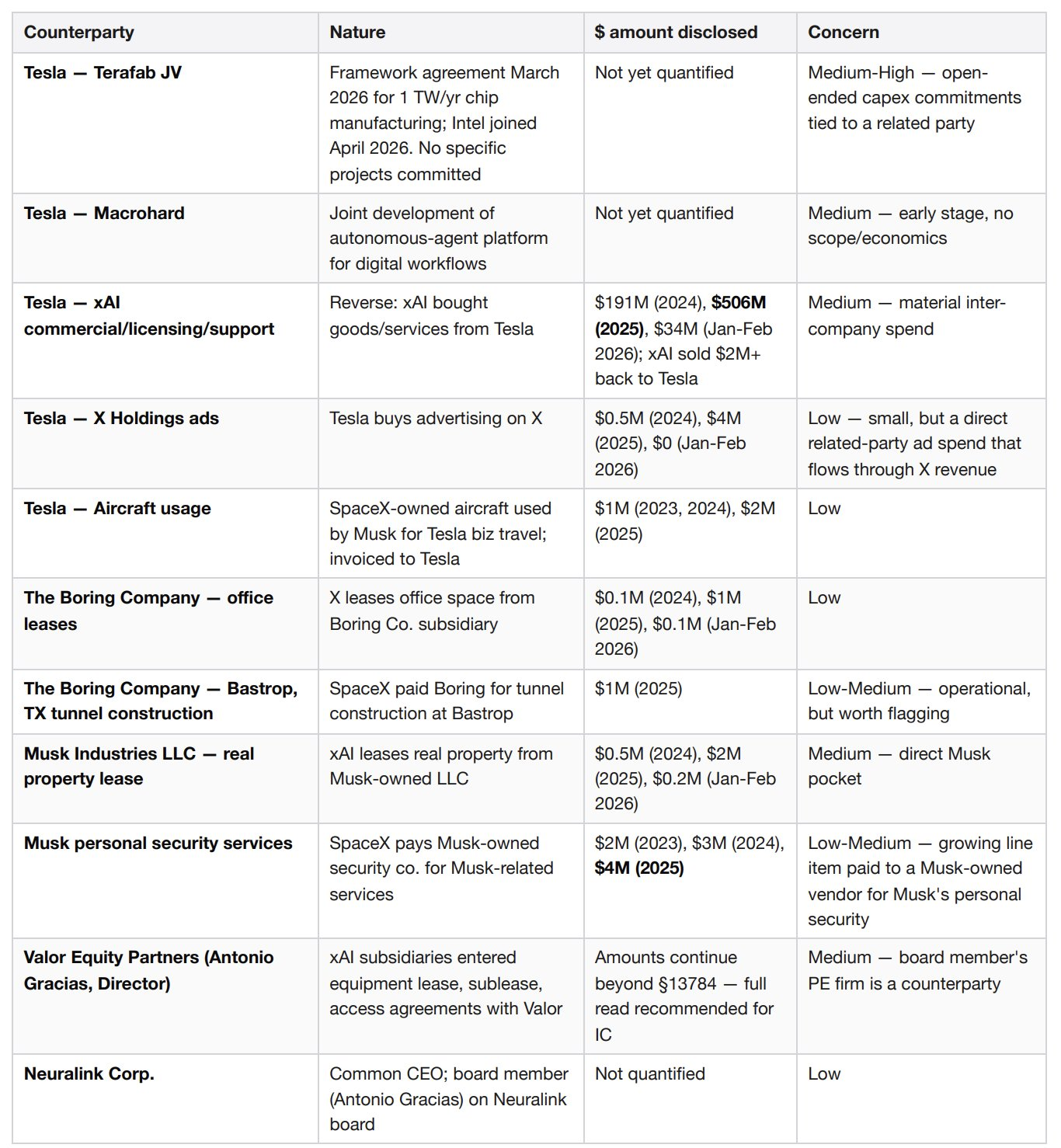

Конфликт интересов андеррайтеров

Этот момент глубоко запрятан в разделе об андеррайтинге, о нем мало пишут в новостях, но он имеет значение. Аффилированные лица пяти ведущих андеррайтеров (Goldman Sachs, Morgan Stanley, Bank of America, Citi, JPMorgan) плюс пяти дополнительных со-менеджеров (Barclays, Deutsche Bank, RBC, UBS, Wells Fargo) являются кредиторами по 20-миллиардному бридж-кредиту SpaceX, а сейчас они устанавливают цену IPO, предназначенного для рефинансирования этого кредита. Morgan Stanley также выступала консультантом SpaceX по приобретению xAI (финансируемому за счет бридж-кредита). Андеррайтинговый синдикат имеет прямую финансовую заинтересованность в максимизации суммы привлечения средств в ходе IPO. Это должно заставить инвестиционный комитет быть бдительным в отношении ценовой дисциплины.

Плотность аффилированных лиц

Ни один пункт в отдельности не выглядит тревожным. Тревожит плотность — сеть контролируемых Маском юридических лиц имеет как минимум девять различных точек финансового контакта со SpaceX. Комитеты по корпоративному управлению публичных компаний обычно рассматривают одну или две такие связи. Здесь их на порядок больше.

Триггерные точки для решений

Повысить до "перевеса", если сделка оценивается по подразумеваемой капитализации в 350 миллиардов долларов или ниже, и если Starship, как указано в руководстве, начнет коммерческие поставки полезной нагрузки во второй половине 2026 года, и если рост выручки бизнеса Connectivity во втором квартале 2026 года превысит 40% в годовом исчислении.

Понизить до "отказа", если сделка оценивается выше 510 миллиардов долларов, или если у Starship произойдет событие потери летательного аппарата, приводящее к задержке развертывания спутников V3 до 2027 года или позже, или если сжигание денег в подразделении ИИ во втором-третьем кварталах 2026 года ускорится до годового операционного убытка более 8 миллиардов долларов, или если FAA наложит долгосрочный запрет на полеты Starship.

Список наблюдения на первые 180 дней плюс последующие годы

D+1: Бенчмарк роста в первый день по сравнению с аналогичными IPO

D+30: Первые квартальные отчеты (второй квартал 2026 года) — триггер для раннего освобождения от блокировки (немедленное освобождение 20%, еще 10%, если цена акций превышает цену размещения на 30%)

D+70, +90, +105, +120, +135: Этапы раннего освобождения от блокировки, по 7% каждый

D+90: Окончание периода молчания, запуск покрытия аналитиками продающей стороны

D+180: Окончание всех стандартных периодов блокировки

Вторая половина 2026 года: Выполнение руководящих указаний Starship по коммерческим поставкам полезной нагрузки

Второй-третий квартал 2026 года: Процессуальные вехи коллективного иска о генерации изображений Grok (следить за увеличением резерва в 530 миллионов долларов)

Апрель 2027 года: Годовщина опционного соглашения с Cursor — следить за сигналами об исполнении или расторжении

Сентябрь 2027 года: Истечение срока 20-миллиардного бридж-кредита SpaceX (должен быть рефинансирован или погашен)

Ноябрь 2027 года: Завершение сделки со спектром EchoStar на 19,6 миллиарда долларов — глобальный запуск V2 для мобильных устройств зависит от этого

Май 2029 года: Окончание контракта на вычислительные мощности с Anthropic на 45 миллиардов долларов; условия продления будут определять экономику подразделения ИИ на последующие годы

Октябрь 2029 года: Истечение срока синдицированных кредитов B-1 и B-3 компании X на общую сумму 12,7 миллиарда долларов

Источники

SpaceX S-1, регистрационный номер SEC 0001628280-26-036936, дата подачи 2026-05-20

Сравнимые фундаментальные данные в реальном времени через Jintel GraphQL entitiesByTickers, сеть Base x402, дата получения 2026-05-22

Комплексный архив SEC в реальном времени через x402helper /companies/profile для RKLB, IRDM, VSAT, дата получения 2026-05-22

Фон отраслевых IPO через Parallel Search, сеть Base x402, дата получения 2026-05-22

Четыре сценария IPO SpaceX — Acadian Asset Management

Сгенерировано пакетом анализа IPO на agentic.market. 6 платных вызовов x402. 1,87 доллара USDC в сети Base. Без API-ключей. Без регистрации. Оплата по запросу.

Место на терминале Bloomberg стоит 24000 долларов в год. Эта памятка показывает, что теперь могут производить агенты, когда они могут самостоятельно платить за данные.