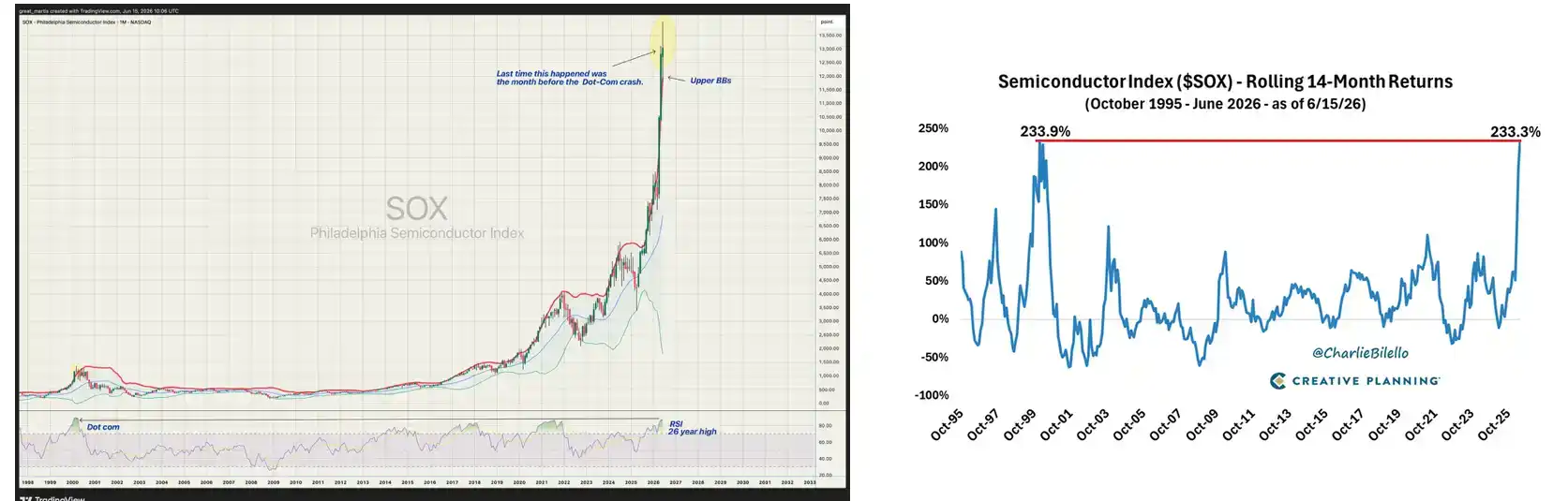

Американские акции закрылись на рассвете, индекс SOX Филадельфийской биржи полупроводников впервые преодолел отметку в 14000 пунктов, обновив исторический максимум.

В истории SOX было всего два периода, когда он рос более чем на 230% за 14 месяцев: с декабря 1998 по февраль 2000 года и с апреля 2025 года по настоящее время.

Доходность от этого бычьего рынка полупроводников была очень концентрированной и значительной. Годовой рост акций трёх гигантов памяти — Micron, SK Hynix, Samsung — составил примерно 141%, 186% и 114% соответственно. Американские депозитарные расписки (ADR) TSMC выросли за год более чем на 50%.

Nvidia 14 мая установила исторический максимум в $235,47. Broadcom, Marvell, ASML также обновили или приблизились к рекордам на своих рыночных нишах. 52-недельный минимум всего ETF SOXX составлял $148, а максимум приблизился к $369, амплитуда колебаний составила около 150%.

Goldman Sachs в апреле пересмотрел прогноз дефицита спроса и предложения DRAM на 2026 год с 3,3% до 4,9%, назвав его самым серьёзным дефицитом памяти за последние 15 лет. Цены на HBM ещё более впечатляющие: одна стекированная микросхема HBM3E стоит около $300, а предстоящая к выпуску HBM4 оценивается примерно в $500 за штуку. Производственные мощности Hynix на HBM на 2026 год уже полностью забронированы Microsoft, Google, Nvidia, некоторые клиенты даже заранее полностью оплатили депозиты, чтобы зарезервировать мощности.

Очевидно, что скорость строительства дата-центров для ИИ намного опережает скорость расширения производственных мощностей чипов.

Бычий рынок «узких мест»

Дефицит — самый прибыльный продукт.

Понимание этой фразы, по сути, позволяет понять основную логику этого бычьего рынка полупроводников. Тот, кто контролирует узкие места в инфраструктуре ИИ, получает самую сильную ценовую власть. И наоборот, если ваш сегмент можно заменить, на него можно давить по цене, то даже при большом спросе цена акций не растёт.

Типичным примером последнего являются оптические модули. Отчет Photon Capital за апрель указывает, что китайские производители оптических модулей занимают семь из десяти первых мест в мире, но не зарабатывают много денег, прибыль по-прежнему получают компании-производители чипов. Zhongji Innolight и Suzhou New Sea-Union уже достигли мирового уровня по объёмам поставок и контролю затрат на оптические модули 800G и 1.6T, напрямую сжимая маржу прибыли американских компаний, таких как Coherent и Lumentum. Спрос удваивается, а маржа прибыли становится тоньше. Причина одна: сборка оптических модулей не является достаточно дефицитным звеном.

А память стала самой твёрдой основной темой в этом раунде бычьего рынка американских полупроводников. По сути, потому что она создала узкое место, и оно становится всё уже.

HBM — это не обычная DRAM. 3D-стэкирование, TSV (сквозные кремниевые отверстия), специализированные технологии упаковки — каждый уровень технологических барьеров является результатом более чем десятилетних инвестиций в основные средства. В мире всего три компании способны производить HBM, и Hynix занимает примерно половину рынка.

Интересно, что эта логика также работает на макроуровне государств.

Настоящими победителями в строительстве инфраструктуры дата-центров для ИИ являются не «все полупроводниковые страны», а те страны и регионы, которые за последние несколько лет или даже десятилетий как раз построили дефицитные промышленные кластеры в каком-то незаменимом звене. Дефицит — вот в чём суть.

У каждого региона своя основная ниша

В американском инвестиционном сообществе видел интересную точку зрения.

На вершине цепочки создания стоимости по-прежнему находятся США.

Дизайн ASIC от Nvidia, AMD, Broadcom, инструменты EDA от Synopsys и Cadence, AI-сети Arista, три крупных облачных провайдера, упаковывающих вычислительные мощности в услуги для всего мира. Google, Amazon, Microsoft ускоряют разработку собственных ASIC. Broadcom и Marvell вместе занимают около 95% рынка заказного дизайна ASIC, только Google ежегодно тратит на разработку TPU около $8 млрд для Broadcom.

Ключевые узлы производства находятся на Тайване и в Южной Корее, но они полностью питаются с разных столов.

На Тайване всё вращается вокруг TSMC и передовой упаковки. 3-нм и 2-нм техпроцессы в мире может производить только TSMC. Три фабрики TSMC по технологии CoWoS загружены полностью, срок поставки — от 52 до 78 недель, только Nvidia заблокировала от 60% до 70% мощностей CoWoS. TSMC увеличивает месячные производственные мощности с 35 тыс. пластин в конце 2024 года до 130 тыс. пластин к концу 2026 года, почти в четыре раза. Но даже после такого расширения мощности по-прежнему ограничены. Тайваньская система контрактного производства серверов — Foxconn, Quanta, Wistron — также наращивает объёмы вместе с поставками серверов для ИИ.

История Южной Кореи полностью связана с памятью. Hynix занимает примерно 50-55% мирового рынка HBM, Samsung — 19-35%, Micron — примерно 5-20%. HBM — это не то же самое, что обычная память. 3D-стэкирование, TSV, специализированные технологии упаковки — каждый уровень технологических барьеров является результатом многолетних непрерывных инвестиций южнокорейских компаний.

Роль Японии и Нидерландов также очень важна. Tokyo Electron производит полупроводниковое оборудование, Shin-Etsu Chemical и SUMCO — кремниевые пластины, Ajinomoto — материалы подложки ABF. Япония давно выбыла из конкурентной борьбы на рынке конечных продуктов чипов, но её позиции в материалах и прецизионной обработке до сих пор никто не может заменить.

С Нидерландами всё ещё проще: ASML монополизировала производство EUV-степперов. J.P. Morgan в январе значительно повысил целевую цену для ASML до 1400 евро, прогнозируя, что 2027 год станет годом с самым высоким ростом прибыли компании — рост EPS на 57%. Они основывают этот прогноз на трёх драйверах: более чем ожидаемое расширение мощностей передовых логических чипов, масштабное расширение производства в области памяти DRAM, а также общие показатели спроса лучше ожидаемых. Голландские компании по производству упаковочного оборудования, такие как BESI, также получили большое количество заказов на фоне взрывного роста спроса на упаковку чипов для ИИ.

Китай и Европа имеют разные точки входа, но логика схожа: они создали преимущество в затратах или способности к поставкам в каком-то конкретном звене инфраструктуры ИИ.

Zhongji Innolight и Suzhou New Sea-Union достигли мирового уровня по контролю над объёмами поставок и ценами на оптические модули 800G и 1.6T. Но анализ Photon Capital также указывает на важное временное окно: высокая маржа прибыли компаний, производящих оптические модули, в настоящее время обусловлена временной ценовой властью из-за этапного дефицита мощностей на 800G. Когда к концу 2026 — началу 2027 года начнётся массовое производство 1.6T, и производители второго и третьего эшелона также нарастят мощности, ценовое давление на сегмент модулей быстро возрастёт.

В Европе такие компании, как Schneider Electric, ABB, Vertiv, занимающиеся распределением электроэнергии и охлаждением, получили значительно больше заказов, чем ожидалось, на фоне резкого роста энергопотребления дата-центров. По оценкам Wedbush, расходы гиперскейлеров на инфраструктуру ИИ в 2026 году составят около $725 млрд, что на 77% больше, чем в прошлом году, причём энергетическая инфраструктура является одной из наиболее быстрорастущих подкатегорий.

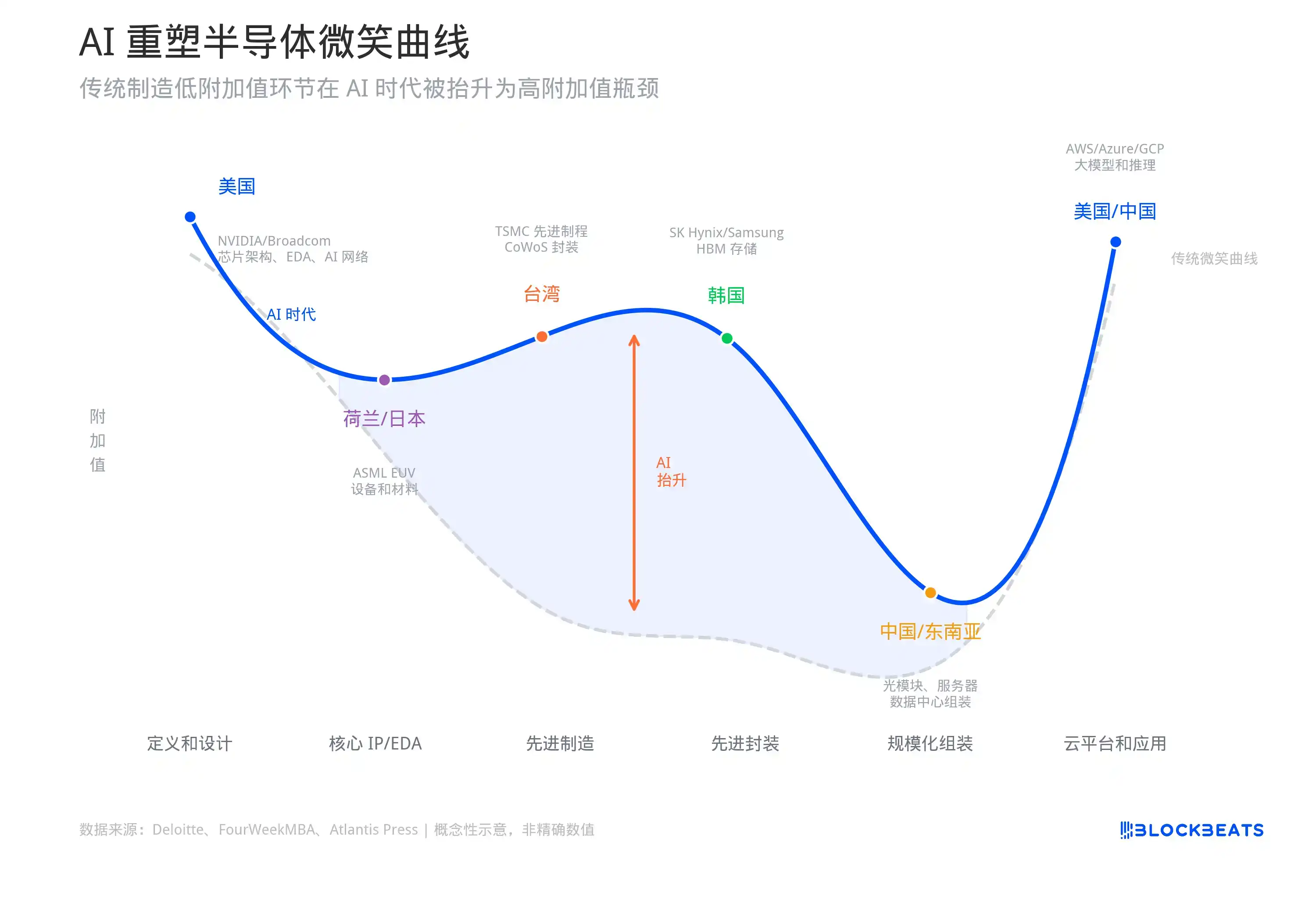

ИИ переосмысливает «кривую улыбки» полупроводников

Если подытожить эту картину с помощью кривой улыбки: левый конец (США) отвечает за «определение и дизайн», средний сегмент (Тайвань, Южная Корея, Нидерланды, Япония) — за «производство передовых чипов», нижний средний сегмент (Тайвань, Китай, Юго-Восточная Азия) — за «масштабную сборку», правый конец (США и Китай) — за «облачные платформы, модели и клиентские входы».

Автором этой кривой является основатель Acer Ши Чжэньжун, в 1992 году он использовал эту модель, чтобы объяснить, почему сборка ПК приносит наименьшую прибыль.

Но тридцать лет спустя дата-центры для ИИ меняют форму этой кривой.

Анализ цепочки создания стоимости FourWeekMBA и статья, опубликованная Atlantis Press в этом году, указывают на один и тот же вывод: ИИ снова поднимает средний сегмент традиционной кривой улыбки. Передовая упаковка CoWoS от TSMC, стекирование HBM от Hynix, EUV-степперы ASML — эти звенья в кривой улыбки традиционного производства относятся к сегменту «производства» с самой тонкой маржой, но в эпоху ИИ они стали самым дефицитным ресурсом, и их рентабельность и ценовая власть не ниже, чем у сегментов дизайна и применения.

Данные из статьи показывают, что валовая маржа Nvidia в 2023-2024 годах составила 72,72%, чистая маржа — 48,85%. Но валовая маржа TSMC в первом квартале 2026 года также достигла 66,2%, чистая маржа — 50,5%. Разрыв в рентабельности между сегментами дизайна и производства сокращается, что беспрецедентно в истории полупроводниковой отрасли.

Традиционная кривая улыбки считала производственное звено наименее прибыльным. ИИ превратил самые сложные производственные звенья в самый дефицитный ресурс.

В отчёте J.P. Morgan по азиатским полупроводникам за март содержится аналогичный вывод: цикл ИИ в 2023-2024 годах в основном был сосредоточен на GPU, в 2025-2026 годах спрос начал распространяться на более широкую цепочку поставок, память, передовая упаковка, заказные ASIC, сети дата-центров принимают эстафету.

Каждый раунд смены узких мест выводит на передний план группу ранее игнорируемых компаний, одновременно отправляя лидеров предыдущего раунда роста на этап консолидации.

Как далеко может забежать бык? Борьба мнений быков и медведей

Давайте сначала послушаем быков. Дэн Айвс из Wedbush в мае на CNBC прямо заявил, что Nasdaq в ближайший год достигнет 30000 пунктов, причина — спрос на чипы для ИИ по-прежнему намного превышает предложение. Goldman Sachs даёт более конкретные цифры: мировые капитальные расходы на ИИ в 2026 году составят около $765 млрд, а к 2031 году вырастут до $1,6 трлн.

J.P. Morgan в мартовском отчёте по азиатским полупроводникам ясно написал: инвестиции в вычислительные мощности для ИИ по-прежнему находятся на стадии расширения, полупроводниковая отрасль вступает в новый структурный цикл спроса.

Бычьи прогнозы по памяти ещё более агрессивны. Goldman Sachs недавно пересмотрел прогнозы дефицита спроса и предложения DRAM на 2026-2028 годы в сторону более глубокого дефицита, на 2027 год с предыдущих -2,5% до -5,9%, почти вдвое. Их суждение таково: этот цикл памяти отличается от прошлых, спрос со стороны серверов для ИИ имеет более высокую предсказуемость, рост предложения заблокирован долгосрочными соглашениями о предварительных заказах, а рост цен продлится дольше, чем ожидает рынок.

Goldman Sachs даже одним махом повысил прогноз операционной прибыли Kioxia на три года — с 2027 по 2029 год — на величину от 16% до 48%, аргументируя это тем, что высокая прибыльность может сохраняться два-три года. Для компании, занимающейся таким сильноцикличным бизнесом, как память, давать прогноз «высокой прибыли в течение трёх лет» — большая редкость на Уолл-стрит.

Изменение позиции J.P. Morgan ещё интереснее. В 2024 году они ещё кричали о «зиме DRAM», прогнозируя многолетнее падение цен с четвертого квартала 2024 года. А в 2025 году они резко развернулись в сторону теории суперцикла, прогнозируя рост цен на DRAM на 62% в 2026 году, а прибыль Hynix и Samsung превысит консенсус-прогнозы на 30-50%.

Но и у медведей голос громкий, и имена у них известные.

Майкл Бэрри в мае публично предупредил, что эта полупроводниковая динамика очень похожа на последние месяцы интернет-пузыря 1999-2000 годов. SOX вырос на 65% с начала года, на 10% за неделю, ETF SOXX торгуется на 60% выше 200-дневной скользящей средней — такая степень технического растяжения редко может сохраняться в истории. Раскрытие позиций SEC показывает, что он купил большое количество путов (put options) на SOXX, QQQ, Nvidia, Palantir и Oracle с датой истечения в январе 2027 года и ценой исполнения значительно ниже текущих цен акций.

Man Group (один из крупнейших в мире публичных хедж-фондов) в июне опубликовал длинную статью, специально разбирающую риски пузыря ИИ. Их основная точка зрения: финансовая архитектура, построенная вокруг ИИ, стала слишком большой, чрезмерно закредитованной и чрезмерно зависимой от нескольких взаимосвязанных участников.

Они особенно отметили, что строительство многих дата-центров для ИИ финансируется через частный кредит, а залогом по этим кредитам являются «аппаратные средства, которые быстро обесцениваются, как смартфоны, а не долгосрочные активы, такие как здания». Первая волна дефолтов может появиться в 2027-2028 годах, когда истечёт срок первых арендных договоров, и разрыв между допущениями финансирования и реальностью станет непреодолимым.

Если смотреть вперёд, стоит обратить внимание на несколько временных точек.

Micron опубликует финансовый отчёт 24 июня, перспективные ориентиры по спросу на HBM и распределению мощностей определят динамику всего сектора памяти на всё лето. Следующий отчёт Nvidia также критически важен: если появятся даже малейшие сигналы замедления спроса на чипы для ИИ, настроения во всём секторе будут переоценены заново.

Если смотреть дальше, график выхода новых мощностей — настоящий водораздел. Фабрика M15X Hynix, как ожидается, начнёт выпуск продукции в середине 2027 года, новая фабрика в Йонине перенесена на февраль 2027 года. Фабрика P5 Samsung начнёт работу в 2028 году. Fab 1 Micron в Айдахо, как ожидается, начнёт вносить вклад в производство в середине 2027 года.

В сумме отраслевые мощности увеличатся на 20-30% во второй половине 2027 — первой половине 2028 года. Вопрос в том, что совокупный годовой темп роста спроса на HBM также превышает 40%. Успеет ли предложение догнать спрос, зависит от того, замедлится ли к тому времени капитальные расходы на ИИ.

Последняя переменная — геополитика. Чем выше концентрация полупроводниковых цепочек поставок, тем сильнее удар «чёрного лебедя». На долю одной компании TSMC приходится более 90% мирового производства по передовым техпроцессам — на бычьем рынке это эффективность, а в сценарии конфликта — это системный риск. Тайваньский пролив, путь ужесточения экспортного контроля США в отношении Китая, степень сотрудничества Японии и Нидерландов в контроле за оборудованием — эти факторы в хорошие времена никто не хочет обсуждать, но в случае происшествий цены отреагируют быстрее, чем любые изменения фундаментальных показателей.