Автор статьи:Thejaswini M A

Перевод статьи:Block unicorn

Предисловие

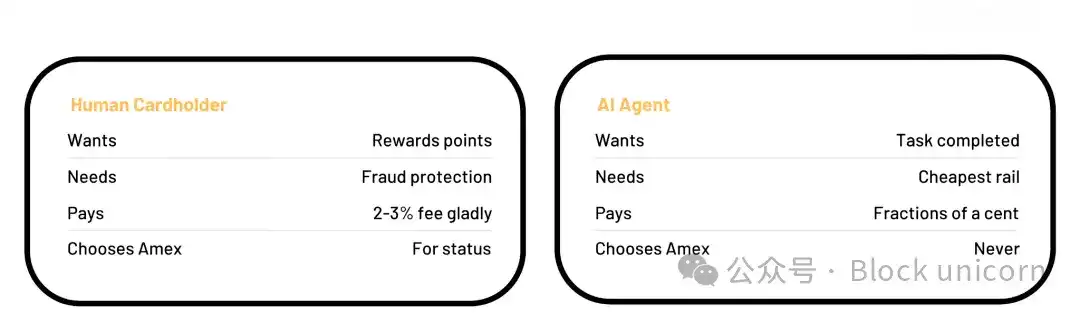

Вся бизнес-модель Visa построена на ставке на человеческое поведение. Это связано с человеческим потреблением и психологией. Накопленные вами бонусные баллы, защита от мошенничества, на которую вы полагаетесь, заветная карта Centurion, политика нулевой ответственности, которая успокаивает вас при использовании банкоматов за границей — всё это существует не потому, что перевод средств сложен, а потому, что люди тревожны, стремятся к статусу и не умеют читать условия. Visa использовала этот когнитивный разрыв, чтобы построить компанию стоимостью 500 миллиардов долларов.

Однако у ИИ-агентов этих черт нет.

Он не накапливает баллы, не ищет защиту от мошенничества и не жаждет получить черную карту. У него только одна инструкция: выполнить задачу. И когда задача включает оплату, агент выполняет сложные вычисления, которые человек никогда не потрудился бы сделать: самый дешевый путь,最快的结算, самые низкие комиссии. Каждый раз, автоматически, без эмоций.

В прошлом месяце статья в SubStack под названием «Глобальный кризис интеллекта 2028 года» привела к тому, что акции Visa упали на 4% за один день, Mastercard — на 6%, а American Express — на 12%. В отчете было указано, что это «анализ сценария», а не «прогноз» (sic). Но рынок этому не поверил. Технические аргументы также не имели значения. Проблема в том, что к 2027 году агенты будут обходить торговые центры и использовать стейблкоины для расчетов. Visa потратила пятьдесят лет на совершенствование своего продукта, а теперь ее клиентская база заменяется.

В бизнесе «машина-машине» комиссия за обмен в 2-3% явно является целью. Это и есть центральный тезис данного утверждения Citrini Research. Это не означает, что искусственный интеллект завтра уничтожит Visa. Но структура комиссий, на которой Visa построила свою империю, по сути является налогом на иррациональное поведение человека, в то время как сами транзакторы полностью рациональны. В этом и заключается суть существования Visa.

Что продает Visa?

Чтобы понять, почему это важно, вы должны знать, на что фактически идут interchange-комиссии.

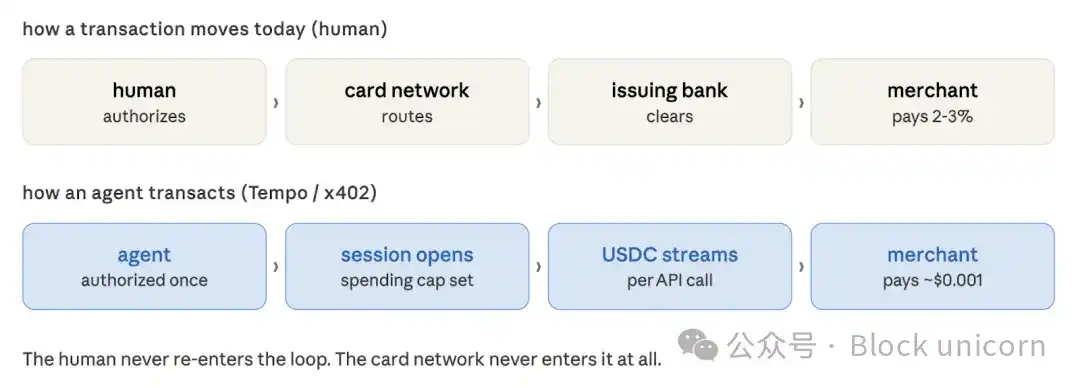

Когда вы совершаете покупку с помощью кредитной карты, merchant платит платежной сети и вашему банку-эмитенту комиссию в размере 2-3%. Эти сборы оплачивают ваши бонусные вознаграждения, защиту от мошенничества, страховку покупок и услуги по урегулированию споров. Вся потребительская ценность кредитных карт оплачивается merchant'ом, который в конечном итоге перекладывает расходы на потребителя, немного повышая цены на товары. Это отлаженная и стабильная система, работающая уже пятьдесят лет, потому что потребитель в сделке готов нести все эти расходы, просто он платит не напрямую.

ИИ-агентам это не нужно. Он не будет оспаривать сборы или требовать возврата средств. Обоснованность взимания этой платы заключается в том, что она защищает от человеческой ошибки, мошенничества и импульсивного поведения. Если в транзакции нет человека, этот сбор полностью теряет смысл.

American Express является самым ярким проявлением этой проблемы. Его клиенты — это состоятельные, много тратящие и амбициозные держатели карт премиум-класса. Его годовая плата выше, чем у Visa или Mastercard, именно потому, что его клиенты готовы платить за статус и привилегии. Эта модель основана на том, что покупка совершается человеком, и клиент выбирает American Express вместо Visa, потому что доступ в залы ожидания того стоит. Агент не будет активно выбирать American Express, он будет искать самый дешевый вариант для совершения сделки. В мире, где программное обеспечение управляет кредитными картами, премиальных уровней членства не существует.

Коммерческая маршрутизация под руководством агентов, обходящая interchange-комиссии, представляет больший риск для кредитных банков и монобанков-эмитентов, которые сильно зависят от доходов от комиссий в 2-3% и строят весь свой бизнес вокруг программ вознаграждений, субсидируемых merchant'ами. У Visa и Mastercard есть сетевой бизнес, который может адаптироваться. У тех эмитентов, которые строят всю свою модель прибылей и убытков вокруг interchange-комиссий и программ вознаграждений, пути к отступлению нет.

Неделя, когда все отправили одновременно

Отчет Citrini и запуск инфраструктурных проектов совпали в одни и те же три недели.

Tempo официально запустила основную сеть в прошлую среду. Платежный блокчейн, разработанный совместно Stripe и Paradigm, созданный для расчетов стейблкоинами с высоким объемом транзакций, был запущен одновременно с протоколом машинных платежей (MPP). MPP — это открытый стандарт, позволяющий агентам искусственного интеллекта автономно оплачивать услуги без индивидуального одобрения человеком. Протокол вводит сеансовый механизм. Агент просто авторизует лимит расходов один раз, а затем может производить микроплатежи по мере потребления таких услуг, как данные, вычисления или вызовы API. Средства оплачиваются с аутентификацией OAuth. Пользователь авторизует бюджет, агент тратит. Весь процесс обходится без использования банковской карты на каждом шагу.

Anthropic, DoorDash, Mastercard, Nubank, OpenAI, Ramp, Revolut, Shopify, Standard Chartered и Visa были указаны в качестве партнеров по проектированию Tempo. Вся экосистема платежей и электронной коммерции признала эти структурные изменения.

В тот же день, когда была запущена Tempo, криптографическое подразделение Visa выпустило инструмент интерфейса командной строки для оплаты агентами искусственного интеллекта через терминал без API-ключей, без учетных записей и без человеческого одобрения. Visa назвала это «коммерцией из командной строки» — машины могут совершать сделки без вмешательства человека.

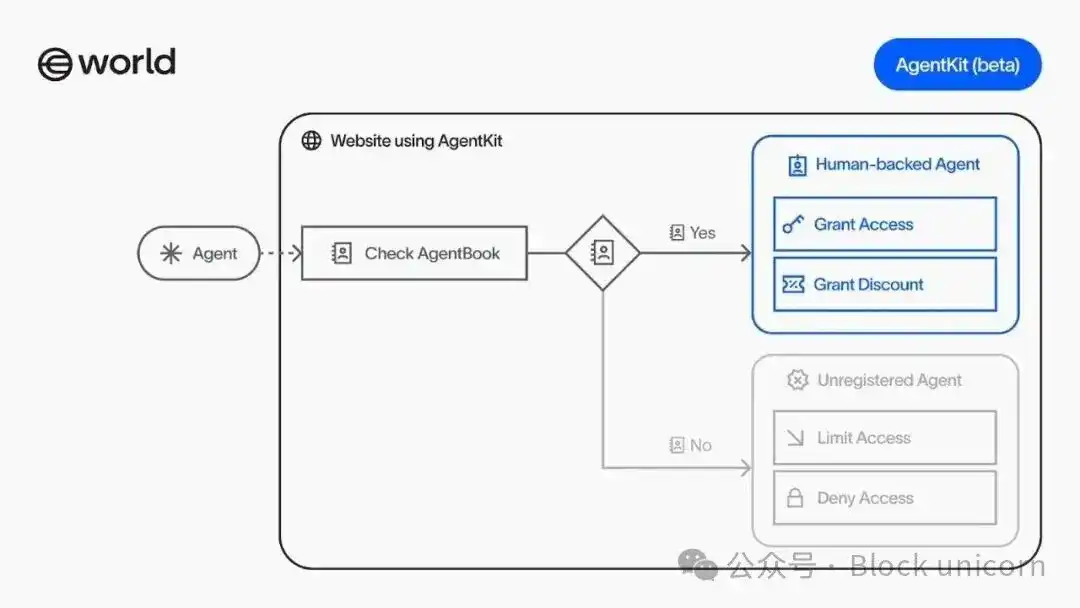

Mastercard согласилась приобрести стартап инфраструктуры стейблкоинов BVNK за 1,8 миллиарда долларов. Circle запустила на тестовой сети Nanopayments, это транзакции USDC стоимостью менее цента и без комиссии Gas, созданные для агентов, использующих API с оплатой за использование без учетных записей или учетных данных. Проект World Сэма Олтмана выпустил AgentKit, позволяющий агентам携带 криптографические доказательства того, что они представляют реального человека, этот инструмент напрямую интегрирован с платежной системой Coinbase, позволяя платформам проверять личность агента, не препятствуя законным транзакциям.

На мой взгляд, то, что произошло на прошлой неделе, — это то, что компании спешат стать новой Visa, пока Visa не осознала, что она потеряла.

Очевидный парадокс

Теперь уже совершенно ясно, что Visa не стоит на месте.

Она участвовала в разработке протокола машинных платежей (MAPPS) Tempo, запустила Visa Crypto Lab, и ее глава по криптовалютам написал статью в Fortune, объясняя, как агенты могут использовать карты для оплаты через новые стандарты. Mastercard вкладывает 1,8 миллиарда долларов в инфраструктуру стейблкоинов. Stripe приобрела Bridge и Privy. Нынешние игроки осознают этот сдвиг и готовятся до того, как новая инфраструктура полностью заработает.

Аргумент Visa заключается в том, что она может расширить свои рельсы до бизнеса, управляемого агентами, до того, как бизнес, управляемый агентами, построит рельсы, которые сделают Visa неактуальной.

Это утверждение не совсем ошибочно. Stripe обработала 1,9 триллиона долларов общего объема платежей в 2025 году, что на 34% больше, чем годом ранее. Эти компании не сокращаются. Сетевые дистрибьюторские преимущества карточных сетей трудно скопировать. Я признаю, что неохотно говорю это публично, потому что исторически, как только кто-то выдвигает такой аргумент, выходит новый продукт, который заставляет их выглядеть глупо.

Итак, вот дыра в этом аргументе: дистрибьюторское преимущество Visa построено на отношениях с merchant'ами и доверии потребителей. Merchant'ы принимают Visa, потому что у потребителей есть Visa; потребители имеют Visa, потому что merchant'ы принимают Visa. Весь цикл работает благодаря людям. Как только агенты станут основными покупателями в какой-либо значительной сфере коммерции, этот маховик замедлится. У агентов нет лояльности к бренду и нет кошелька. У них есть только бюджет и инструкции. Любой маршрут, который является самым дешевым и быстрым, получит их бизнес, и стоимость переключения равна нулю.

Я хочу точно указать, где мы находимся, потому что в настоящее время повествование развивается быстрее, чем данные.

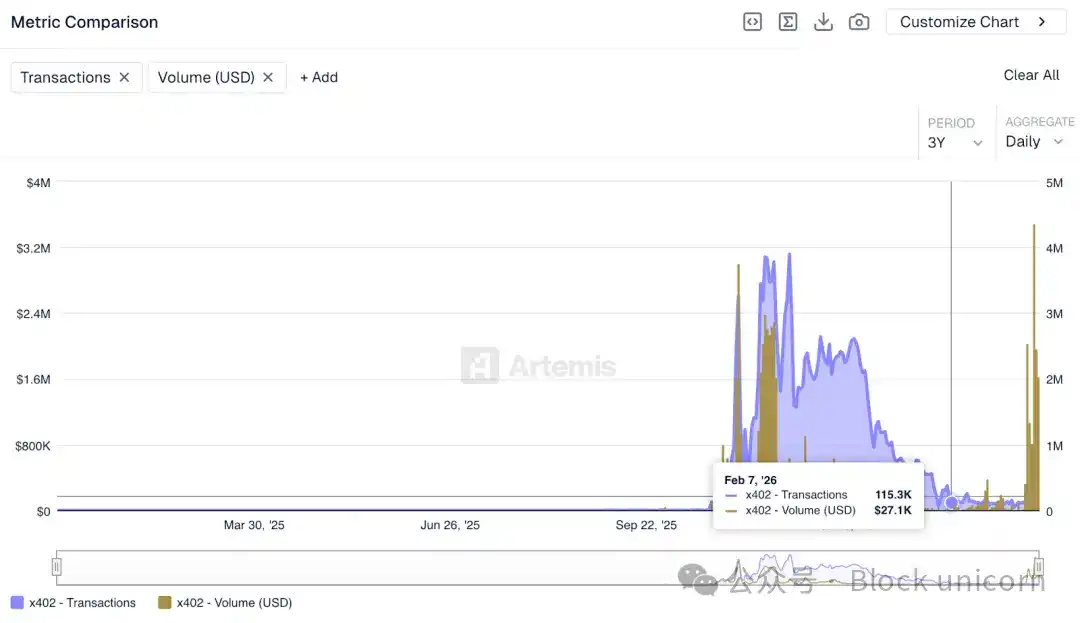

Несмотря на то, что экосистема вокруг x402 оценивается примерно в 7 миллиардов долларов, данные в链上 показывают, что на прошлой неделе дневной объем транзакций по протоколу составлял всего около 28 000 долларов, большая часть из которых приходилась на тестирование, а не на реальные транзакции. Эта цифра ничтожна по сравнению с дневным объемом транзакций Visa.

Количество транзакций x402 превысило 50 миллионов. Хотя суммы отдельных транзакций невелики, количество транзакций указывает на то, что инфраструктура используется. Разработчики строят на ее основе. Сервисы на стороне merchant'ов, принимающие платежи от агентов, продолжают расти. Так и начинаются платежные сети.

По оценкам McKinsey, к 2030 году агенты искусственного интеллекта могут способствовать глобальным потребительским сделкам на сумму от 3 до 5 триллионов долларов. Эта оценка может быть верной, а может быть и оптимистичной. Но неоспоримо, что бизнес-модели, управляемые агентами, еще не получили широкого распространения. Merchant'ы, создающие нативные сервисы для агентов, предприятия, для которых агенты являются основными покупателями, и объемы транзакций, которые действительно проверяют экономику транзакций, все еще развиваются.

Отчет Citrini вызвал панику на рынке, потому что он смоделировал последовательность правдоподобных событий. В отчете Mastercard за первый квартал 2027 года замедление объема транзакций не будет объяснено «ценовой оптимизацией под руководством агентов». По крайней мере, пока нет.

Сначала пострадают микроплатежи за инфраструктуру искусственного интеллекта, а не потребительская коммерция.

Агент, выполняющий исследовательскую задачу, вызывает сотни специализированных API данных за один сеанс. Каждый вызов стоит доли цента. За неделю эти вызовы могут принести разработчику, управляющему сервисом, 40 долларов дохода. Кредитные карточные сети не могут справиться с этим. Экономика минимальной суммы транзакции не работает. Процесс onboarding merchant'ов не работает. Структура комиссий не работает. Такая бизнес-модель обречена на провал в рамках Visa. Для этого нужна совершенно новая модель, и x402, Nanopayments и Tempo строят ее.

Как показала модель, построенная Citrini, подрыв потребительской коммерции, если он произойдет, произойдет позже. Для этого требуется, чтобы агенты обрабатывали значительную часть дискреционных расходов, что, в свою очередь, требует, чтобы потребители доверяли агентам принимать решения о покупках, которые они сейчас принимают сами.

Visa сталкивается с более качественным клиентом. Клиентом, которому больше не нужны те элементы, на которых Visa построила свой успех. Комиссия за обмен в 2-3% — это не налог на транзакции, а налог на иррациональное поведение человеческой природы. А агенты полностью рациональны.

Откуда я знаю, что это важно? Потому что на прошлой неделе Visa потратила 1,8 миллиарда долларов, чтобы确保自己不会被排除在答案之外 (гарантировать, что ее не исключат из ответа).

Трендовые криптовалюты

Связанные с этим вопросы

QПочему модель бизнеса Visa уязвима перед лицом ИИ-агентов?![]()

AМодель Visa основана на человеческом поведении: стремлении к статусу, наградам и защите от мошенничества. ИИ-агенты рациональны, не ценят эти преимущества и всегда выбирают самый дешёвый и эффективный способ оплаты, что делает комиссии Visa необоснованными.

QКакие технологические разработки угрожают доминированию Visa в платежах?![]()

AПроекты вроде Tempo, x402, Nanopayments и MPP создают инфраструктуру для микроплатежей и расчётов в стейблкоинах, позволяя агентам проводить транзакции без посредников, минуя высокие комиссии традиционных сетей.

QКак Visa и другие компании реагируют на эту угрозу?![]()

AVisa и Mastercard активно инвестируют в новые технологии: участвуют в разработке Tempo, приобретают стартапы в области стейблкоинов и создают инструменты для платежей через ИИ-агентов, пытаясь адаптироваться к меняющейся среде.

QВ каких сферах ИИ-агенты начнут вытеснять традиционные платежи в первую очередь?![]()

AСначала в микротранзакциях для ИИ-инфраструктуры: оплата API-вызовов, данных и вычислений. Крупные потребительские расходы будут затронуты позже, когда люди начнут доверять агентам больше решений о покупках.

QПочему комиссия Visa в 2-3% нежизнеспособна для ИИ-агентов?![]()

AЭта комиссия — плата за человеческие слабости: страх, статус и ошибки. Агенты лишены этих качеств, действуют рационально и всегда ищут оптимальный путь, что делает высокие fees экономически невыгодными и бессмысленными.

Похожее

Торговля

Популярные статьи

AI Companions: Новое определение взаимодействия человека с ИИ

AI Companions (AIC) - это инновационная платформа, объединяющая ИИ, VR/AR и блокчейн-технологии, созданная с целью переосмыслить опыт виртуального общения.

3.0k просмотров всегоОпубликовано 2025.05.07Обновлено 2025.05.07

HTX Learn: пройдите обучение по "AI Companions" и разделите 10 000 USDT!

Чтобы вы лучше поняли суть проекта AI Companions, команда HTX Learn запускает кампанию в формате "Учитесь и Зарабатывайте".

2.1k просмотров всегоОпубликовано 2025.05.08Обновлено 2025.05.14

Неделя обучения по популярным токенам (2): 2026 может стать годом приложений реального времени, сектор AI продолжает оставаться в тренде

2025 год — год институциональных инвесторов, в будущем он будет доминировать в приложениях реального времени.

1.9k просмотров всегоОпубликовано 2025.12.16Обновлено 2025.12.16