Bitcoin пытается вырваться из медвежьей рыночной структуры, которая сохраняется с конца октября. Несмотря на несколько кратковременных восстановительных ралли, движение цены продолжает отражать слабость: быки не могут отбить ключевые уровни сопротивления или создать устойчивый импульс.

По мере того как на рынке распространяются неопределенность и усталость, многие участники задаются вопросом, соответствует ли текущее поведение Bitcoin традиционной циклической модели, которая определяла предыдущие бычьи и медвежьи фазы.

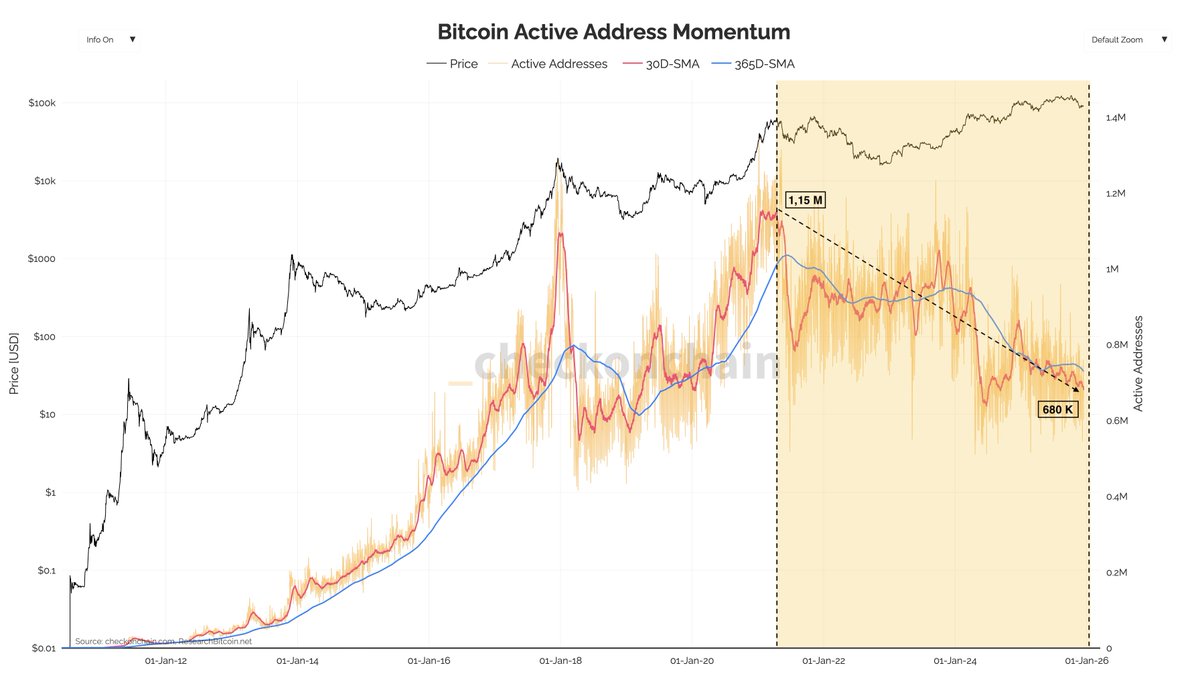

Недавний анализ Darkfost выделяет структурный сдвиг, который добавляет важный контекст в эту дискуссию. Согласно данным, количество активных адресов Bitcoin неуклонно снижается с апреля 2021 года. Исторически бычьи фазы характеризовались четким расширением активных адресов, поскольку новые инвесторы выходили на рынок, а активность в блокчейне резко возрастала. Этот рост обычно достигал пика около вершин цикла, после чего следовало сжатие во время медвежьих рынков по мере сокращения участия.

Однако этот цикл выглядит заметно иначе. Даже в периоды сильных ценовых показателей с 2022 года активные адреса не смогли значительно восстановиться и продолжают снижаться. Это расхождение предполагает, что рыночная структура Bitcoin, возможно, эволюционирует от розничной, ориентированной на ончейн-участие модели, к чему-то более концентрированному и подверженному институциональному влиянию.

В то время как Bitcoin пытается стабилизироваться после недель нисходящего давления, понимание этих структурных изменений становится критически важным. Спад активных адресов может сигнализировать не просто о слабости, а о трансформации того, как Bitcoin хранится, торгуется и оценивается в этом цикле.

Активные адреса сигнализируют о структурном сдвиге на рынке

Анализ предполагает, что, несмотря на сильные ценовые показатели Bitcoin с 2022 года, ончейн-активность продолжает ухудшаться. Активные адреса вновь приближаются к самым низким уровням, наблюдавшимся в этом цикле, что подчеркивает растущий разрыв между движением цены и активностью сети. На пике в апреле 2021 года Bitcoin зафиксировал примерно 1,15 миллиона активных адресов. Сегодня этот показатель почти halved, находясь near 680,000, и это сжатие нельзя игнорировать.

Это снижение трудно attributed to a single cause. Вместо этого оно, вероятно, отражает комбинацию структурных изменений в том, как Bitcoin хранится и используется. Одним из способствующих факторов, по-видимому, является рост количества неактивных адресов. Хотя точные критерии классификации vary, более широкий тренд указывает на более сильную ментальность долгосрочного хранения, когда монеты остаются бездействующими, а не активно перемещаются в ончейне. Такое поведение снижает видимую активность сети без necessarily implying медвежьего убеждения.

В то же время часть участников рынка, возможно, полностью перешла от прямого ончейн-использования. Централизованные биржи, кастодиальные платформы и финансовые продукты, такие как ETF, предлагают экспозицию к Bitcoin без необходимости ончейн-взаимодействия. В результате спрос на блок-пространство снижается, даже при том что аллокация капитала в Bitcoin остается значительной.

В совокупности устойчивое падение активных адресов suggests, что рыночная структура Bitcoin эволюционирует. Сеть становится менее driven розницей и более концентрированной, что reinforces идею о том, что традиционные циклические метрики, возможно, теряют часть своей объясняющей силы в этой среде.