Вступление редактора: 14 мая Cerebras официально вышла на Nasdaq с тикером CBRS. В первый день котировки выросли примерно на 68% по сравнению с ценой размещения, сделав это IPO одним из самых заметных событий на рынке аппаратного обеспечения ИИ с 2026 года.

Эта статья написана Стивом Вассалло, одним из первых инвесторов Cerebras. В ней он вспоминает свои отношения с Эндрю Фельдманом, которые длились девятнадцать лет — от SeaMicro до Cerebras. Внешне это история венчурных инвестиций — от term sheet до IPO. На самом деле, это запись о том, как компания на переднем крае аппаратного обеспечения, вопреки общему мнению, пошла ва-банк на фундаментальную реконструкцию архитектуры вычислений для ИИ: проблемы, связанные с чипом размером с вафлю, узким местом пропускной способности памяти, питанием, охлаждением, электрической целостностью, — все это не отдельные технические вызовы, а целостное переизобретение современной вычислительной системы.

Самое примечательное не в том, что Cerebras в итоге создала чип размером с вафлю, который в 58 раз больше традиционного чипа, а в том, что компания с самого начала выбрала направление, противоположное инерции отрасли: когда GPU стали ответом по умолчанию для обучения ИИ, она попыталась переопределить, «что такое компьютер, созданный для ИИ». За этим стоят не только техническая проницательность, но и терпение капитала, а главное — долгосрочные, нетранзакционные отношения доверия между инвесторами и командой основателей.

Для сегодняшней конкуренции в аппаратном обеспечении ИИ значение Cerebras заключается в том, что она напоминает рынку: революция в вычислительной мощности заключается не только в добавлении большего количества GPU, но также может прийти из нового взгляда на саму архитектуру вычислений.

Далее следует оригинальный текст:

1 апреля 2016 года, в пятницу, я отправил Эндрю Фельдману письмо, в котором сообщил, что перелезу через забор на его заднем дворе и лично вручу ему term sheet для инвестиций в Cerebras.

Это был День смеха, но я не шутил.

Строго говоря, это не стандартная процедура для венчурной фирмы. Но к тому моменту я знал Эндрю уже девять лет и почти два года вместе с ним обсуждал его следующую компанию. Я не мог пропустить эту сделку из-за предложения, которое еще дорабатывалось в субботу днем.

Впервые я встретил Эндрю в октябре 2007 года. Тогда он и Гэри Лаутербах только что основали SeaMicro. Я не инвестировал в тот раунд, но мы очень хорошо сошлись характерами, особенно мне понравился их подход к решению проблем с нуля. С тех пор я следил за ними.

По-настоящему ценные отношения требуют времени. Как и по-настоящему ценная компания. Сегодня, снаружи, Cerebras — это компания, существующая десять лет и готовящаяся к IPO. Но для меня это отношения, которые длились девятнадцать лет, и наконец настал момент бить в колокол.

Глубокие отношения и неразумные амбиции

Когда в 2012 году AMD приобрела SeaMicro, у меня было предчувствие: Эндрю не задержится надолго в крупной компании. В нем сильны дух непокорности и мятежное сердце. К началу 2014 года он уже искал возможность уйти, и мы стали часто встречаться, обсуждая, что делать дальше.

В то время две вещи еще не стали консенсусом. Во-первых, что ИИ действительно станет полезным. Во-вторых, что GPU — не самая подходящая архитектура для ИИ.

По первому вопросу даже многие умные люди, которых я знал, расходились во мнениях. После появления AlexNet в 2012 году в некоторых уголках исследовательского сообщества с помощью сверточных нейронных сетей уже добивались почти волшебных результатов. Но в более широкой индустрии программного обеспечения ИИ все еще балансировал между маркетинговым хайпом и научно-исследовательским проектом.

Второй вопрос, аппаратный, почти еще не поднимался серьезно. GPU стали выбором по умолчанию для обучения нейронных сетей в основном потому, что исследователи случайно обнаружили, что они «менее плохи» по сравнению с CPU. Создание новой вычислительной системы, специально предназначенной для рабочих нагрузок ИИ, означало бросить вызов доминирующей архитектуре, которую в то время использовало большинство исследователей мира.

Но Эндрю, Гэри и их соучредители Шон, Майкл и JP видели другое направление. У каждого из них за плечами были десятилетия опыта в области чипов и систем: у Гэри — фундаментальная работа в области потоков данных и неупорядоченного исполнения еще в 1980-х; Шон специализировался на передовых серверных архитектурах; Майкл отвечал за программное обеспечение и компиляторы; JP глубоко занимался аппаратным инжинирингом. Это была чрезвычайно редкая группа людей: каждый по отдельности был выдающимся, но вместе их способности умножились. Они могли представить себе совершенно новый компьютер.

Они верили, что если ИИ действительно раскроет свой потенциал, размер рынка, который он создаст, намного превысит сумму всех существующих вычислительных форм.

Они также ясно видели суть GPU: это был чип, изначально созданный для обработки графики, лишь временно «повышенный» до инструмента обучения ИИ на новом поле боя. Он действительно был лучше CPU в параллельной обработке, но если бы кто-то проектировал с нуля для рабочих нагрузок ИИ, никто бы не создал такую архитектуру, как у GPU. Истинным ограничителем возможностей нейронных сетей была не производительность вычислений, а пропускная способность памяти. Это означало, что чип, который им нужно было создать, должен был оптимизировать не матричные умножения в изолированных ядрах, а эффективность потока данных во всей вычислительной структуре.

Внутри фирмы инвестиции в Cerebras отнюдь не были решением, принятым по консенсусу. Некоторые из моих партнеров, видевшие, как предыдущий раунд полупроводниковых инвестиций принес почти одни убытки, очень откровенно высказали свои опасения. Но в итоге мы, как команда, пришли к согласию. В тот уикенд в апреле 2016 года мы четко сказали Эндрю: мы хотим стать первыми инвесторами, вручившими ему term sheet.

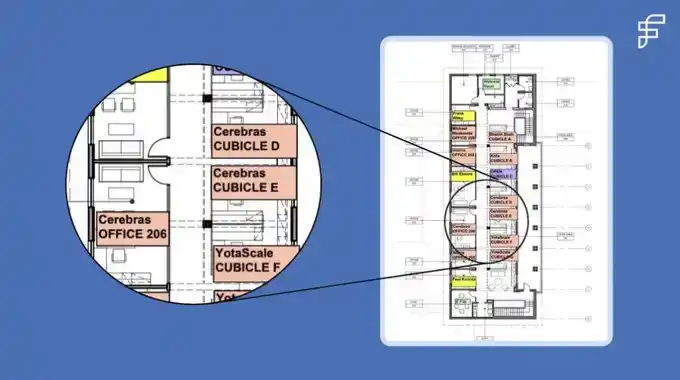

Несколько недель спустя Эндрю, Гэри, Шон, Майкл и JP переехали в наш EIR-офис на втором этаже по адресу 250 Middlefield. У меня до сих пор сохранился план этажа, нарисованный тогдашним офис-менеджером. На этом плане Cerebras располагалась рядом с одним из основателей Foundation, в нескольких дверях от Бхавина Шаха, позже основавшего Moveworks. Это был отличный этаж для роста стартапа.

Знать, какие правила можно согнуть, а какие — сломать

До Cerebras крупнейший чип в истории вычислений имел площадь около 840 квадратных миллиметров — примерно как кусочек кремния размером с почтовую марку. Чип Cerebras имеет площадь 46 000 квадратных миллиметров, что в 58 раз больше.

Выбор чипа размером с вафлю означал выбор всех связанных с этим сложных задач проектирования. За почти 80 лет истории вычислительной техники никто по-настоящему не делал этого раньше. А значит, никто системно не решал этих проблем: как питать такой огромный чип? Как его охлаждать? Как поддерживать электрическую целостность между десятками тысяч точек соединения?

Чтобы реализовать вычисления на уровне вафли, Cerebras практически должна была одновременно заново изобрести каждый аспект современных вычислений: полупроводники, системы, структуры данных, программное обеспечение и алгоритмы. Каждое из этих направлений само по себе могло бы стать стартапом. Эндрю и его команда решили начать с решения самых сложных технических проблем. Благодаря их интенсивной, почти неутомимой работе, эти проблемы решались одна за другой.

Каждые шесть-восемь недель у нас проходило заседание совета директоров. Они рассказывали нам о том, что пробовали с момента прошлой встречи: новый вариант системного дизайна, новая схема электропитания или доработка системы теплосъема. Из-за постоянного столкновения с системными проблемами со всех сторон они выработали редкую способность ясно выражать свои мысли. Они объясняли, что, по их мнению, пошло не так, и что они собираются попробовать в следующий раз.

Мы задавали вопросы, а затем углублялись вместе с командой, привлекая необходимых людей, ресурсы и связи, чтобы помочь им найти новые пути. Через шесть-восемь недель, когда мы снова собирались, история повторялась уже на другой технической проблеме: еще одна граница, которую нужно было исследовать. Каждое решение выявляло следующую проблему, которую необходимо было решить.

Их первый прототип вафли задымился при первом же включении. Команда назвала это «тепловым событием» — именно так обычно называют пожар, когда не хотят пугать совет директоров или арендодателя.

Я все время подсчитывал энергопотребление на квадратный миллиметр, отчасти из любопытства, отчасти потому, что цифры казались нереально высокими. Тогда мы пригласили инженеров из Exponent. Эта компания занимается анализом отказов, а ее прежнее название было как раз Failure Analysis. Они подтвердили, что цифры энергопотребления действительно были такими же смелыми, как и казалось, и помогли нам продумать ряд решений, не бросающих вызов второму закону термодинамики. В конце концов, это был закон, против которого даже Эндрю, при всей его проницательности, спорить бы не стал.

Дисциплина инженера заключается в том, чтобы знать, какие правила можно сломать, какие — согнуть, а какие — нужно уважать. У Эндрю и его команды было практическое чутье на эту разницу. Они знали, когда они бросают вызов устоявшейся практике — это именно то, чем они хотели заниматься; а когда они бросают вызов законам физики — этим они заниматься не собирались.

Когда вы создаете передовые технологии, неудачи неизбежны. Единственный способ пройти через них — дисциплина, настойчивость и, что самое важное, доверие: доверие к миссии, доверие друг к другу и вера в то, что после того, как первый прототип самоуничтожится, вы на следующее утро вернетесь в лабораторию, чтобы начать следующую итерацию.

У такой работы нет транзакционной версии. Есть только долгосрочная: оставаться в комнате, среди еще не завершенных решений и терпеливых объяснений. Чтобы, когда она наконец увенчается успехом, вы были там и видели это своими глазами.

Этот момент наступил в августе 2019 года. Эндрю, Шон и их команда стояли в лаборатории и наблюдали, как впервые запускается новый компьютер, который они сами спроектировали. Для непосвященного внешне он не делал ничего интересного. По словам Эндрю, это зрелище было примерно таким же захватывающим, как наблюдение за высыхающей краской. Но разница была в том, что раньше такая «краска» никогда не высыхала. Они вместе постояли там минут тридцать, а потом вернулись к работе.

С кем строить — это очень важно

Некоторые выбирают проблемы, исходя из того, что, как они знают, могут решить. Эндрю выбирает проблемы, исходя из того, какие, по его мнению, заслуживают решения. Постепенные улучшения его не вдохновляют, он хочет скачка в 1000 раз. С первого дня он хотел сделать Cerebras компанией поколения, уникальной.

Эта движущая сила частично исходит от его характера. Эндрю описывает это как «болезнь» архитектора компьютеров — десятилетиями быть одержимым одной идеей. Но, на мой взгляд, это в более широком смысле «болезнь» основателя. Он смотрит на проблему и сначала спрашивает себя: могу ли я создать что-то, что даст скачкообразное улучшение? Затем он спрашивает: если у меня получится, будет ли это кому-то нужно? Если оба ответа утвердительные, он посвящает этому следующие десять лет своей жизни.

Другая часть этой движущей силы происходит из его среды воспитания. Эндрю вырос в окружении гениев так же естественно, как большинство детей растут перед телевизором. Его отец был новаторским профессором эволюционной биологии и каждое воскресенье играл в парный теннис по очереди с шестью людьми. Трое из них позже получили Нобелевскую премию, а один — Филдсовскую премию.

По словам Эндрю, эти титаны терпеливо объясняли ему свою работу в области физики, математики и молекулярной биологии на языке, понятном ребенку. У него сложилось глубокое впечатление о том, как выглядит настоящий ум; и он также понял, как сказала его мать, что быть умным не означает быть негодяем.

Позже я осознал, что это одна из самых ключевых черт Эндрю — наравне с его мятежными амбициями и почти инстинктивным чутьем на действительно стоящие проблемы. Он глубоко убежден, что самые выдающиеся люди, которых он встречал, часто оказываются и самыми добрыми.

Это убеждение сформировало то, как его команда собирается вместе, чтобы выполнять невероятно сложные задачи. Первые 30 человек, нанятых в Cerebras, уже работали с ним раньше; некоторые были с ним с 1996 года. Сейчас в Cerebras около 700 сотрудников, и примерно 100 из них прошли с ним через несколько компаний.

Важно то, что доброта и дух соперничества не противоречат друг другу. Эндрю страстно жаждет победы. Он любит говорить, что он профессиональная версия Давида, сражающегося с Голиафом. Голиаф медлителен и всегда готов к лобовой атаке, что оставляет пространство для всех остальных тактик. Преимущество Давида в том, чтобы появляться там и таким образом, где и как Голиаф не может.

Во времена SeaMicro основным партнером Эндрю по каналам сбыта в Японии была NetOne. Основным поставщиком NetOne был Cisco, который развлекал партнеров частными самолетами и яхтами стоимостью выше, чем большинство домов в Пало-Альто. Бюджет Эндрю был куда скромнее, поэтому он пригласил генерального директора NetOne на барбекю к себе во двор. Позже тот генеральный директор сказал ему, что он десятилетиями вел дела с Cisco, но никогда не был приглашен к кому-нибудь домой. Этот небольшой, но очень человечный жест — то, о чем Голиаф даже не подумал бы, — укрепил их отношения.

От первого term sheet до IPO

Сегодня утром Эндрю ударил в колокол, открывая торги на Nasdaq. Я стоял рядом с ним. Прошло десять лет и 2600 миль с тех пор, как все началось в нашем офисе на 250 Middlefield.

Сегодня все еще есть редкие основатели, которые делают то же, что делал Эндрю тогда: рисуют схемы на доске в три часа ночи, сражаясь с еще не решенными техническими задачами. Они так же обладают сильным духом непокорности и мятежным сердцем. Они пытаются найти партнера, который действительно готов сражаться бок о бок: залезть и помочь решить проблему, когда первый прототип не включается; и оставаться рядом, пока он наконец не заработает.

Именно таких основателей я хочу поддерживать: тех, кто выбирает проблемы, стоящие решения, представляет решения, которые в 1000 раз лучше нынешнего положения дел, и оттачивает, настаивает, доводит до конца, несмотря на неизбежные вызовы на этом пути.

Для таких основателей, как Эндрю, Гэри, Шон, Майкл и JP, я готов в субботу днем перелезть через забор на заднем дворе и лично вручить им term sheet.