By | FunTalk, Author | Lin Shu, Editor | Liu Yuxiang

The battle of text-to-video AI is over.

On April 8th, a horse named HappyHorse descended from the sky, sweeping aside contenders like Seedance 2.0 and Kling 3.0 on the Artificial Analysis video evaluation leaderboard to claim the top spot. The mystery was solved—it came from Alibaba's ATH Innovation Business Unit, a unified Transformer video generation model with 15B parameters, supporting text and image joint generation of video with synchronized audio. The news sent shockwaves through the entire AI video sector.

Just a few days before HappyHorse's debut, another muffled sound came from across the ocean: on March 24th, OpenAI officially announced the shutdown of Sora, with the web and App versions going offline on April 26th, and the API being discontinued on September 24th. OpenAI's official shutdown of Sora came just three months after signing a multi-year cooperation agreement with Disney.

Two years ago, Sora's initial release amazed the entire tech world, while domestic video AI was still in its infancy.

Now, ByteDance's Seedance 2.0, released on February 7th, 2026, redefined industrial-grade AI video with native 2K clarity and director-level cinematography; Kuaishou's Kling 3.0 followed closely behind, topping the leaderboard with an Elo score of 1249 upon its release on February 5th; Alibaba's HappyHorse later surpassed them all, directly crushing its predecessors.

It is an indisputable fact that domestic AI has come from behind to lead the video generation track.

But on the other side of the dazzling fireworks, another hidden worry is approaching.

Across the ocean, Anthropic, which had never ventured into multimodal AI, stirred Washington and Wall Street with its latest Claude Mythos model. It not only significantly outperforms the previous flagship model in various capabilities but has also demonstrated the ability to autonomously discover network vulnerabilities and exploit them—which is why Anthropic claims it dares to publicly release the model, albeit with limited access only to a few vetted organizations.

According to media reports, after the release of Mythos, U.S. Treasury Secretary Besant and Federal Reserve Chairman Powell urgently met with CEOs of Wall Street giants like Citigroup, Morgan Stanley, and Bank of America at the Treasury Department headquarters in Washington. The core agenda was singular: the systemic cybersecurity risks that the Mythos model could trigger.

Similarly, on April 9th, OpenAI also released GPT-5.4-Cyber, a model with advanced cybersecurity capabilities, also available only to a limited number of partners—a direct response to Anthropic's Mythos.

This is the other portrayal of the current Sino-US AI landscape:

Using the same gunpowder, some make fireworks, while others have already forged weapons.

One's Poison, Another's Nectar

Besides shutting down Sora, OpenAI's main business is also struggling.

As of February 2026, ChatGPT's weekly active users had reached 900 million, boasting the largest AI user base globally. But these 900 million users do not equate to 900 million profits. The fundamental reality of its business model—earning $1 for every $1.7 burned—remains unchanged.

To this day, OpenAI still cannot shake Google and Meta's dominance in the digital advertising market, making it difficult to monetize through ad scale, and subscriptions alone cannot cover costs. OpenAI's 2026 ARR is approximately $24 billion, seemingly massive, yet it remains unprofitable.

In contrast, Anthropic never took the consumer route from the start. Claude was positioned as a productivity tool, with Claude Code capturing 54% of the AI programming market, serving over 300,000 enterprises. By April 2026, Anthropic's ARR had surpassed $30 billion, officially overtaking OpenAI. This figure was just $9 billion a year ago.

More crucially, over 1,000 of Anthropic's enterprise customers pay over $1 million annually, exhibiting extremely high customer stickiness—this is not luck; it's a victory of strategy.

Therefore, this year, OpenAI changed its core strategy, shifting from consumer entertainment products to enterprise productivity tools, streamlining its model product line and concentrating resources on the GPT-5.4 series and the next-generation "Spud" model. Sora's shutdown is a manifestation of this strategy.

It is foreseeable that this year's main AI battlefield will be in the to-B sector. Anthropic's series of new product releases and growth curve prove that the ceiling for AI To-B is high, and OpenAI, burdened with huge losses, is also adjusting its direction in time, continuing to double down on the productivity tool direction.

Chinese manufacturers widely distributed red envelopes during the Spring Festival, with Yuanbao, Qwen, and Douban entering the下沉 (down-market) consumer market. Now, Seedance2.0, Kling 3.0, and "HappyHorse" have defeated Sora in the text-to-video field. On the surface, the main offensive directions on both sides of the Pacific have diverged.

Objectively speaking, Chinese manufacturers' AI products have cost advantages, with revenue mainly coming from API calls and C-end subscriptions. For example, Kuaishou's Kling ARR exceeded $300 million by January 2026, with single-month revenue surpassing $20 million in December 2025—a benchmark achievement domestically.

But compared to Anthropic's $30 billion ARR, the gap remains a hundredfold.

However, simply comparing revenue numbers is unfair and inaccurate. The Chinese AI market, unlike the US, has its own logic.

Sora is a pure money-loser in OpenAI's hands, but Seedance2.0 is a booster for ByteDance. Seedance 2.0 is part of the Douyin ecosystem; its task is not independent profitability but rather reducing creator costs on the supply side and injecting more content into the platform. Even if the model invocation cost is high and revenue cannot cover costs, as long as the created content enhances Douyin users' usage time and stickiness, leading to sustained growth in Douyin advertising, the overall account is still profitable. It is worth noting that, according to reports, Douyin's net profit reached $50 billion in 2025, approaching Meta's level.

The same logic applies to Kuaishou's Kling—it is the infrastructure of Kuaishou's content ecosystem, and Kuaishou is not stingy in continuously investing in infrastructure, with 2026 Capex expected to reach 26 billion RMB, most of which will be invested in Kling and basic large model computing power construction.

More importantly, Chinese big tech companies are both consumers and suppliers of AI. ByteDance and Alibaba are developing their own chips, and the optimization space for inference costs is far greater than outsiders imagine. Alibaba Cloud has seen triple-digit growth in AI-related product revenue for ten consecutive quarters, with Q3 cloud revenue in fiscal year 2026 increasing 36% year-on-year to 43.284 billion RMB.

It can be said that compared to Anthropic and OpenAI, which have to build their own commercial ecological闭环 (closed loops) alone, Chinese tech giants with rich ecosystems and application scenarios are much more从容 (composed/at ease).

Additionally, the B-end for Chinese manufacturers is not blank; it just follows an "embedded platform" route—embedding AI capabilities as infrastructure for Alibaba Cloud, Douyin, Taobao, rather than directly selling independent AI products like Anthropic.

But the problem is, while this "embedded" strategy is稳健 (steady/robust), it始终停留在 (always remains at) the level of helping creators and businesses "降本增效" (reduce costs and increase efficiency), or is concentrated in the cloud service field. High-barrier fields that truly determine digital world discourse power, like programming and cybersecurity, have not been deeply涉足 (ventured into) by Chinese manufacturers like Anthropic.

In contrast, Anthropic has made programming and security its core competitiveness since its founding. Most of the 250+ engineers on the Claude team work on programming language understanding, code auditing, and security reasoning—this is functional specialization. Domestic manufacturers treat programming tools as a "functional module" of the large model and will not invest hundred-person specialized teams to turn it into a moat-level product.

The Computing Power Chasm

That Sino-US AI have taken two截然不同的 (completely different) routes is, to some extent, the optimal solution each found under different computing power hierarchies.

Anthropic doesn't engage in multimodal AI, focusing solely on programming and security. This seems like克制 (restraint), but is actually a luxury. It is backed by $8 billion in real money from Amazon, plus 1 million TPUs provided by Google. With such an arsenal, Anthropic can focus single-mindedly on深度研发 (deep R&D) in one direction without having to急于 (rush to) prove its value through C-end monetization like Chinese manufacturers.

The benefits of this frontal assault are obvious. Claude Code capturing 54% of the AI programming market is the best example of technical depth transforming into a commercial moat. The Mythos model is so strong it can discover vulnerabilities in software systems that are difficult for human engineers to detect. This capability is both a defensive weapon and a potential offensive one.

OpenAI closely followed with the release of GPT-5.4-Cyber, indicating that the US AI industry has formed a consensus: AI in cybersecurity and programming is the true strategic high ground.

But this model also has its cost: The support from Amazon and Google is essentially a form of "computing power feudalism"—exchanging TPUs and Trainium for equity and technical binding with AI companies.

In April 2026, Anthropic signed a 3.5GW TPU contract with Google and Broadcom, expected to go online in 2027.

This means Anthropic cannot摆脱 (break away from) Google's chips in the short term. Even if Nvidia's GPUs are better, it must优先跑在 (prioritize running on) Amazon's own chips.

This is also why Anthropic is cooperating with Broadcom to develop its own chips—a measure to hedge the risks of this dependency.

The fundamental reason Chinese manufacturers focus on 2C is the lack of computing power hegemony to依附 (attach to). Every penny spent must be reflected in growth on the financial statements.

This is no exaggeration. According to incomplete statistics, as of the end of 2025, the US actually controlled about 75% of the world's leading AI computing power, while China accounted for about 17%–18%, and a considerable part of that was存量 (stock) Nvidia chips purchased before the export controls were implemented.

Currently, the global AI training computing power总量 (total) is on the order of 10^27 FLOPS. The computing power单独拥有 (individually owned) by a leading US tech giant may exceed the sum total of all Chinese enterprises. More棘手的是 (troublesome is), due to the lower energy efficiency of domestic chips, Chinese enterprises consume about 40% more electricity to achieve the same FLOPS of computing power. Of course, the good news is that domestic computing chips are catching up, and electricity prices are cheaper than in the US.

Besides the gap in computing power, the willingness of the US B-end to pay also provides soil for this route difference. Taking just the cybersecurity field targeted by Mythos as an example, the US cybersecurity market size in 2026 is about $100 billion, and globally it exceeds $520 billion. Such a huge market is enough to support Anthropic's massive investment in Mythos.

In contrast, the advantage of Chinese AI in the consumer track reflects the genes of the entire Chinese internet: the world's most competitive short video ecosystem, the most discerning content creators, and the most完善的 (complete) mobile payment system. This soil naturally孕育出 (gives birth to) the explosive power of C-end AI products.

But翻到硬币的另一面 (turning to the other side of the coin), the reality of China's B-end is: GDP has reached 70% of the US, but the enterprise SaaS market size is less than one-twentieth of the US's. This悬殊的比例 (disparate ratio) is not entirely due to technological backwardness but is rooted in deeper market structures—Chinese enterprises have long been accustomed to buyout software, have low willingness to pay, and renewal culture is far less mature than in the US.

This structural difference directly determines the business logic: In China, making high-barrier, high-unit-price B-end AI products has a天然失衡 (naturally imbalanced) input-output ratio. The market does not reward depth, only scale.

AI Dark Forest

If AI were purely about market competition, then both sides could go their own ways based on their respective resource endowments. But now AI is no longer just about economic benefits, especially after the advent of Mythos.

Mythos's ability is to find vulnerabilities, but the other side of the coin is offense. When an AI model can find security vulnerabilities in large financial systems within minutes, it is only a thin layer of policy constraints away from being used as a cyber weapon.

In this sense, the AI competition is shifting from "whose PPTs and videos look better" to "who can destroy the opponent's digital infrastructure." This is not alarmism but the industry direction indicated by the simultaneous appearance of Mythos and GPT-5.4-Cyber.

Anthropic甩出 (threw out) Mythos, and OpenAI's comprehensive shift to enterprise productivity tools both预示 (foreshadow) that the AI competition has entered the second half, which we might call the "Dark Forest Competition"—the competition for To-B hard power. Economies lacking relevant capabilities will become prey for others.

On the C-end, the battle lines are relatively solidified, and no major changes are expected. Whether Chinese tech giants or US companies like Google and Meta, they all have rich ecosystems and scenarios. AI is just the icing on the cake,提高流量的货币化速率 (increasing the monetization rate of traffic). In the short term, AI newcomers cannot shake their status.

This is perhaps the reason why Anthropic and OpenAI turned to the B-end one after another. In the B-end and G-end markets, the winner-takes-all rule applies, which refers not only to market share but also to the fact that for AI products面向 (facing) enterprises and governments, the loser stands to lose not just revenue and advertising fees, but potentially the initiative of the entire digital security system.

In the foreseeable future, countries will increasingly重视 (pay attention to) this field. But有趣的是 (interestingly), this field may not be the best battlefield for existing giants like Alibaba and ByteDance. Their positioning, ecology, and organizational structure are naturally more suitable for large-scale C-end applications. Although big tech companies have cloud security departments, those are more of a supportive existence. None of the major companies have such huge independent budgets and computing power to create a Chinese version of Mythos.

After all, even in the US, Mythos was not created by big companies like Microsoft or Google.

Mythos's security capabilities (like discovering zero-day vulnerabilities, writing exploits) were not obtained through specialized training but were "natural emergences" resulting from the comprehensive improvement of code, reasoning, and autonomy capabilities. This is precisely the opportunity for the "AI Six Little Dragons" and emerging AI startups.

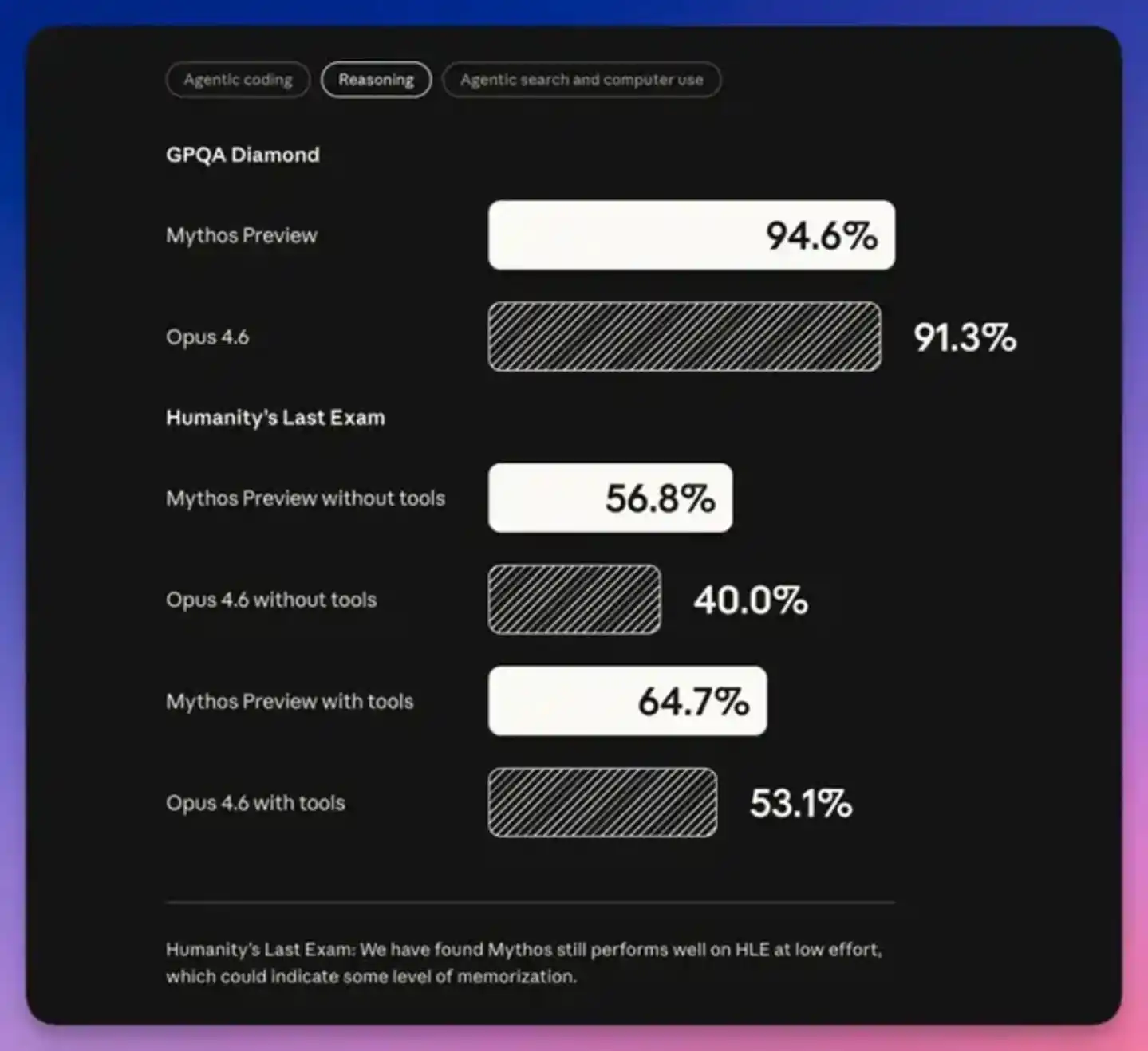

On March 27th, 2026, Zhipu AI released GLM-5.1,刷新了 (refreshed) the global best score on the SWE-bench Pro benchmark, surpassing Claude Opus 4.6 and GPT-5.4. With 754B parameters, its programming capability reached 94.6% of Claude Opus 4.6's, but the price was only one-fifth, and the weights were open-sourced under the MIT license.

The emergence of GLM-5.1 proves one thing: In the critical field of programming, the technical gap of Chinese models can be narrowed.

But expecting the Six Little Dragons to produce products comparable to Mythos in the short term can easily slide into a kind of armchair idealism.

Yang Zhilin, Yan Junjie, and others certainly know the strategic value of the programming and cybersecurity fields. But if computing power is firmly卡住 (stuck), if the domestic B-end/G-end market暂时给不出 (temporarily cannot provide) hundreds of billions of dollars in ARR to support R&D, if even生存的现金流 (survival cash flow) is a problem, then mere "awareness and vigilance" obviously cannot conjure up tens of thousands of H100s to train a monster like Mythos.

Since the frontal battlefield is constrained by the iron curtain of computing power, what Chinese AI manufacturers really should conduct is an asymmetric war. They must advance on both software and hardware fronts. On one hand, big tech companies and the Six Little Dragons increase investment in coding. For example, Alibaba has been enhancing the coding capability in the Qwen foundation model and launched a dedicated Coding model; Kimi K2.5's Coding capability, released in early 2026, was widely regarded as one of the strongest code generation models among domestic open-source models.

On the other hand, domestic models are also being adapted to domestic computing power infrastructure (chips, interconnects, frameworks). It is reported that progress is being made in this regard, and during this period, they must also keep the technology stack from falling behind.

In terms of commercialization, if a domestic Mythos appears, there will definitely be G-end orders, and B-end financial institutions also have demand. Besides, there is also出海 (going global). Vast markets in the Global South—Southeast Asia, the Middle East, Africa, Latin America—enterprises in these markets同样有 (also have) B-end digitalization and cybersecurity needs. If Anthropic and OpenAI continue to hide and conceal, then it is likely to replicate the scene with open-source models—US manufacturers固守 (hold fast to) the closed-source market, maintaining profit margins, but the vast market space is occupied by Chinese open-source models.

Cybersecurity is a bit like the dark forest法则 (law) in Liu Cixin's writing—everyone wants to protect themselves, but if possible, also wants to destroy others. You are not sure if others have good intentions. The safest strategy is to think the worst of them, prepare for battle, and a猜忌链 (chain of suspicion) forms.

In the dark forest, the one who shoots first may not necessarily survive to the end, but the one without a gun definitely cannot walk out of the forest alive.