Author: Deep Chao TechFlow

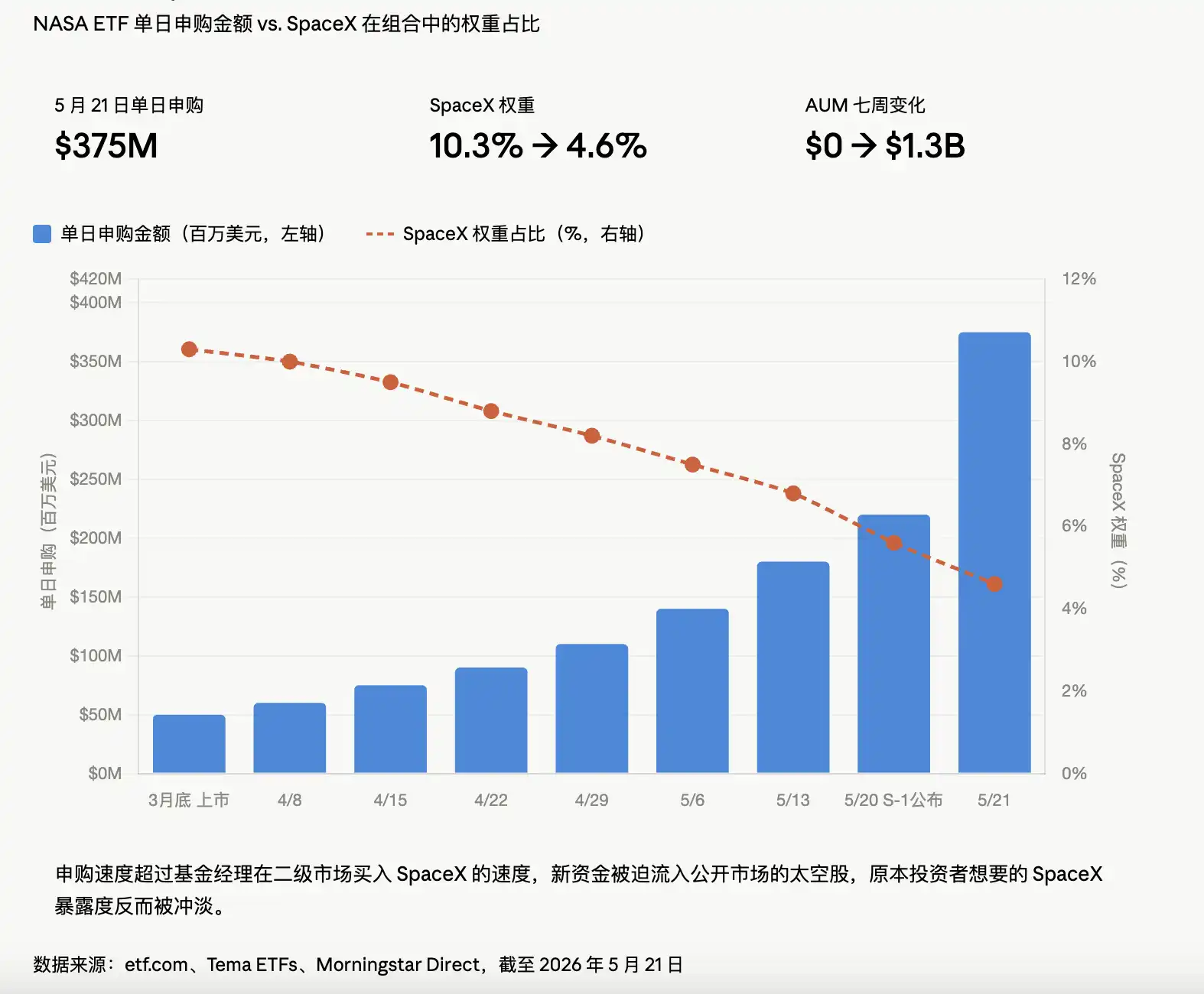

On May 20th, SpaceX's S-1 prospectus went live on the SEC website. The very next day, an ETF with the ticker symbol "NASA" saw a single-day inflow of $375 million, tripling its AUM within a week. It had been launched just seven weeks prior.

Seven weeks later, it's the world's largest space-themed ETF, far surpassing the seven-year-old veteran, UFO. The money it raised in those seven weeks exceeds all the money UFO gathered over seven years.

Everyone rushing into NASA wants to buy SpaceX. But the SpaceX they actually get in their hands is becoming less and less.

Where Did the Money Go?

The NASA ETF's claim to fame is being "the only pure-play space ETF in the market holding SpaceX." As of May 21st, NASA indirectly holds 232,000 common stock equivalents of SpaceX through an SPV, with a book value of $147.4 million, implying a valuation of around $1.51 trillion.

The numbers look solid. But there's a detail most ordinary investors wouldn't notice. According to ETF.com, a week ago, NASA's SpaceX position accounted for 10.3% of the fund. A week later, it was diluted to 4.6%.

Because subscription money came in too fast, the fund manager simply couldn't acquire SpaceX shares on the secondary market quickly enough. A large portion of the new money was forced to buy publicly listed space stocks, which in turn diluted the very SpaceX exposure investors were seeking.

Retail investors rush in wanting SpaceX, but what they end up buying is Rocket Lab plus AST SpaceMobile plus a bunch of other holdings.

More subtly, there's the valuation mechanism. The SPV's holding value only updates when Tema itself makes a trade. In other words, no matter how SpaceX's secondary market quote fluctuates, that portion of NASA's holding sits unchanged on the books.

No one cares about this setup in a bull market. But if the stock falls after the IPO, the SPV portion will "react" in an almost eerie, delayed manner. Not to mention, this SPV is locked up for 6 months after SpaceX's official IPO. If the stock tanks at the open, retail investors can sell the ETF shares, but the SPV can't sell its SpaceX shares.

The ETF charges a 0.87% annual management fee, but a whopping 65% of its apparent gains this year came from stocks like Rocket Lab and Intuitive Machines that had already skyrocketed. SpaceX? It hasn't contributed much at all.

The essence of NASA now is a thematic fund that uses SpaceX as bait, while serving a platter full of other space-related small-cap stocks. The bait's scent is important, but it's not what's actually on the plate.

Valuation Dislocation

What many people don't realize is that some of the major names in this sector have already had a big run-up.

Rocket Lab is up 357% in the past 12 months; Planet Labs up 979%; LUNR up 212%. ARKX is up 62% over the past year, ROKT up 75%. SpaceX merely lit a fire under kindling that was already smoldering.

When you lay these numbers out, the question arises. Planet Labs rose 979% in a year, but this company's main business is selling satellite image data. Do its fundamentals justify a nearly 10x increase in share price?

There were 102 orbital launches globally in 2019, and 342 in 2025—twice the peak of the 1967 space race. Grand View Research predicts the global space economy will grow from $466 billion in 2024 to $769 billion by 2030.

But here's the issue: the industry growing from $466 billion to $769 billion—why should that correspond to a 10x gain in the secondary market?

This is the classic script of valuation dislocation. Fundamentals move linearly, while stock prices move exponentially. The gap is filled by "narrative premium." And the source of that narrative premium is one thing only: SpaceX's impending IPO.

What are the actual buyers at the end of this chain really getting?

Returning to SpaceX itself.

2024 revenue was $18.67 billion, up from $10.3 billion in 2023. But 2024 saw a loss of $4.59 billion, compared to a profit of $791 million in 2023—a direct swing from profit to loss.

CNN's reporting cites a loss of nearly $5 billion last year, with the reason being heavy spending by the AI division on building data centers.

SpaceX's prospectus reveals that xAI has been merged into SpaceX, and X (formerly Twitter) is also included. This so-called "space IPO" is essentially a grand repackaging of all Musk's assets. The prospectus also discloses that Musk controls 85% of the voting rights—no one can oust him unless he votes to fire himself.

The $1.75 trillion valuation for SpaceX corresponds to a four-in-one narrative of "Space + AI + Satellite Internet + Social Media." The bigger the narrative, the more inflated the price.

But the secondary market doesn't care about this. What the secondary market cares about is: if everyone is rushing to get on board, then I must get on too.

After all this circling, the biggest winners aren't the future retail shareholders of SpaceX, because they're not on board yet; nor are they the ETF investors rushing into NASA, because their SpaceX exposure is being diluted.

The biggest winners are the ETF issuers. NASA's expense ratio is 0.87%, the third highest among its peers. $1.3 billion in AUM means over $11 million in annual management fee income.

The essence of launching an ETF is the same as launching a token: you need a story, a timing, and a seemingly reasonable benchmark. SpaceX provides all three.

Before the IPO

On June 12th, SpaceX is scheduled to list on Nasdaq under the ticker SPCX. The underwriting syndicate, led by the world's largest investment banks, aims to raise $40 to $80 billion, far surpassing the record set by Saudi Aramco in 2020.

This will be the largest IPO in human history.

If the stock falls on the first day of trading, all the ETF investors who bought in following the SpaceX story will find that their SPV portion is still marked at the "stale price" from months ago. They cannot immediately cut losses, nor can they immediately exit.

If the stock soars, those who didn't buy the ETF will rush in, pushing the ETF's premium even higher and diluting SpaceX's actual weight within the ETF further, creating a comical reverse flywheel: the more people buy, the less SpaceX each person actually gets.

After SpaceX, a host of industry giants are queuing up to go public. Each listed "flagship concept" will spawn a batch of new ETFs. Each new batch of ETFs will repeat the same dilution game.

The industry isn't short on new stories; what's lacking are people who ask, "Did I really buy what I thought I was buying?" After June 12th, there will be answers. But by then, the people rushing into NASA today won't care about the answers anymore—they'll either be counting their money, or seeking legal redress.